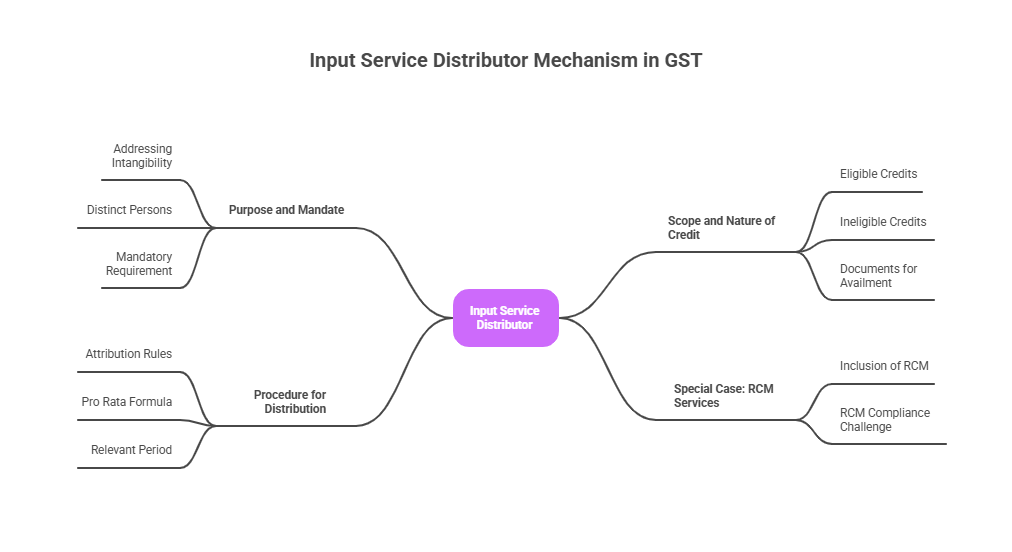

Distribution of Common Input Service Credit by Input Service Distributors (ISD) under GST

The distribution of common input service credit by an Input Service Distributor (ISD) is a crucial mechanism within the GST framework designed to ensure the seamless flow of Input Tax Credit (ITC) for services procured centrally but consumed across multiple registered locations belonging to the same legal entity.

The sources provide extensive detail on the purpose, scope, and mandatory requirements for distributing this credit in the larger context of the ISD mechanism:

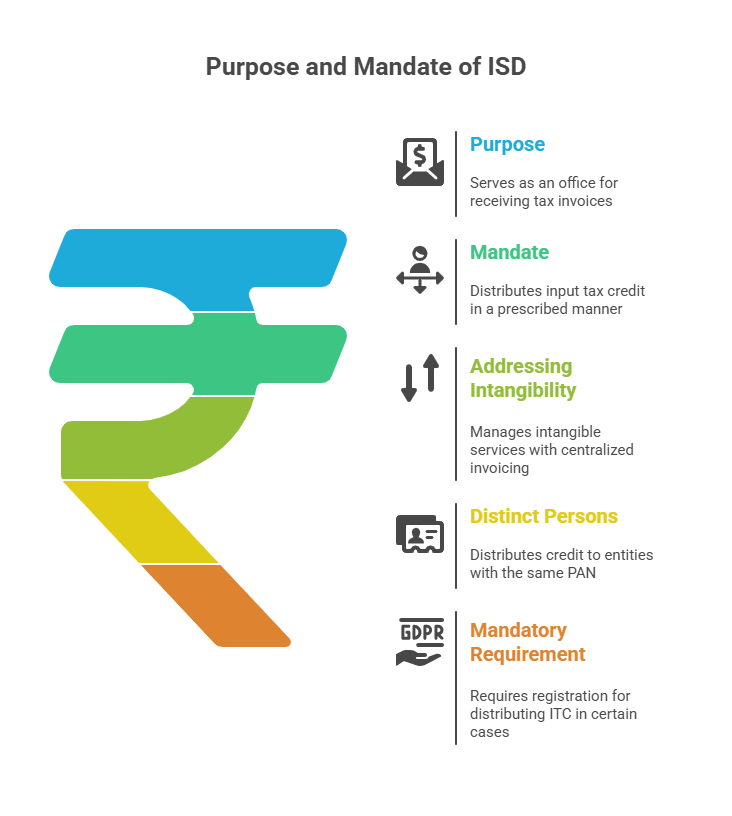

1. The Purpose and Mandate of ISD

The primary purpose of an Input Service Distributor (ISD) is to serve as an office of the supplier of goods or services (or both) that receives tax invoices towards the receipt of input services. This office is liable to distribute the input tax credit in respect of such invoices in the prescribed manner.

• Addressing Intangibility: The need for the ISD mechanism arises because services are intangible, making it not practicable to trace every service to the ultimate recipient. Centralised invoicing (e.g., at a Head Office) for common services like auditing, maintenance, or software licenses means the credit cannot be claimed wholly at that location if the benefit is spread across distinct branch offices.

• Distinct Persons: The distribution must be performed for or on behalf of distinct persons referred to in Section 25. A "recipient of credit" is defined as the supplier of goods or services or both who has the same Permanent Account Number (PAN) as that of the Input Service Distributor.

• Mandatory Requirement (Post-Amendment): The law regarding ISD registration was significantly amended (via the Finance Act, 2024, notified to be effective from 01.04.2025) to make the ISD mechanism mandatory for distributing ITC in certain cases. Consequently, any office receiving invoices for input services on behalf of distinct persons shall be required to be registered as Input Service Distributor.

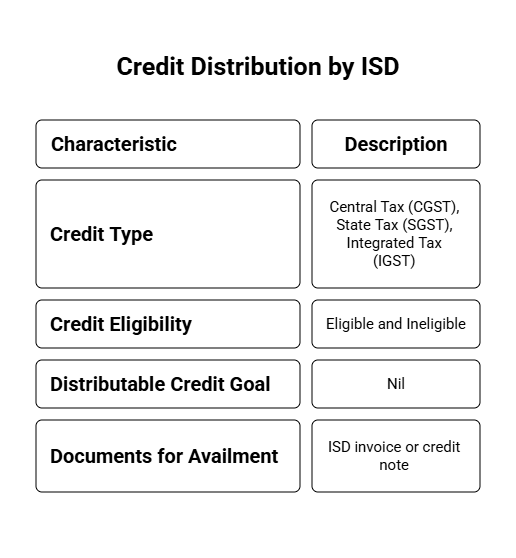

2. Scope and Nature of Credit Distributed

The ISD mechanism specifically deals with the distribution of credit related to input services.

• What is Distributed: The ISD distributes the credit of Central Tax (CGST) or State Tax (SGST) or Integrated Tax (IGST) charged on the invoices received by it.

• Eligible and Ineligible Credits: The ISD must separately distribute the amount of ineligible input tax credit (ineligible under Section 17(5) or otherwise) and the amount of eligible input tax credit. The goal is that the ISD distributes all credit such that the distributable credit is 'nil' each month, leaving it to the recipient branch to disallow the ineligible credits.

• Documents for Availment: The recipient can avail ITC on the basis of an Input Service Distributor invoice or Input Service Distributor credit note issued by the ISD. This document must clearly indicate that it is issued only for the distribution of input tax credit.

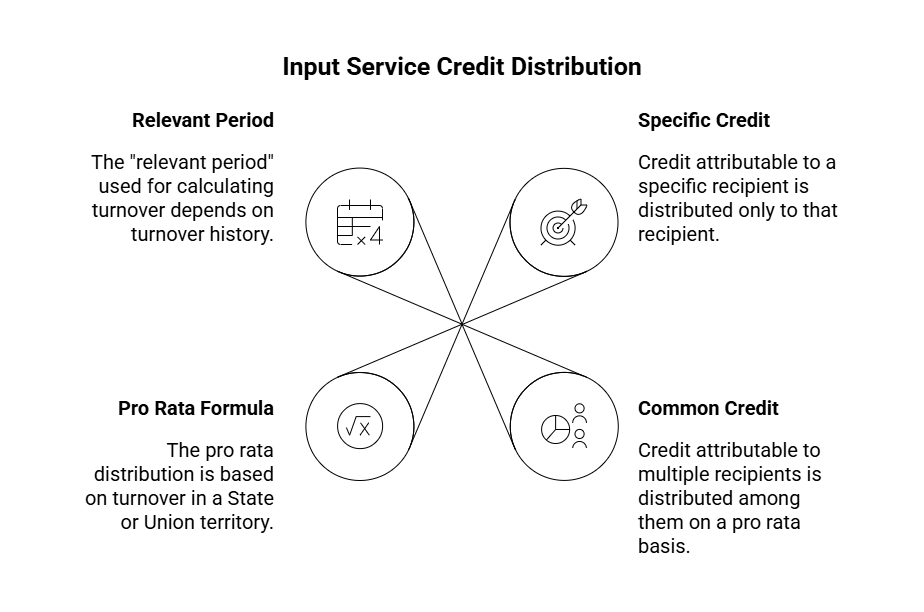

3. Procedure for Distributing Common Input Service Credit (Pro Rata)

When input services are attributable to more than one recipient (i.e., they are common), the law prescribes a strict methodology for distribution based on turnover.

A. Attribution Rules (Section 20(2), Rule 39):

1. Specific Credit: Credit of tax paid on input services attributable to a specific recipient of credit shall be distributed only to that recipient.

2. Common Credit: Credit of tax paid on input services attributable to more than one recipient must be distributed among those recipients on a pro rata basis.

B. Pro Rata Formula:

The pro rata distribution of common credit is based on the turnover in a State or Union territory of the recipient unit during the relevant period.

The formula for calculating the credit () attributable to one recipient () is:

• C: Amount of credit to be distributed.

• : Turnover of person during the relevant period.

• T: Aggregate turnover, during the relevant period, of all recipients to whom the input service is attributable.

C. Determination of Relevant Period:

The "relevant period" used for calculating turnover is:

• The preceding financial year, if the recipients had turnover in their States or Union Territories in that year.

• The last quarter for which turnover details of all recipients are available, if some or all recipients do not have turnover in the preceding financial year.

4. Special Case: Reverse Charge Mechanism (RCM) Services

Recent statutory changes have clarified the distribution of credit for common input services that are subject to tax under RCM.

• Inclusion of RCM: The definition of ISD now explicitly includes offices that receive tax invoices towards input services, including invoices in respect of services liable to tax under sub-section (3) or sub-section (4) of section 9 (RCM provisions). This inclusion ensures RCM services used by distinct persons must be distributed through the ISD mechanism.

• The RCM Compliance Challenge: An ISD is not permitted to discharge any tax liability under GST, including those arising under reverse charge

Asmt 13 in GST | Powers of GST Officers | Functions of accounting | GST Audit procedure | GST Slab for bakery products

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified