The Invoice Management System (IMS) Under GST: Features, Benefits, and Operational Insights

IMS Under GST

The Invoice Management System (IMS) will be introduced by the Goods and Services Tax Network (GSTN) on October 1, 2024, as part of an upgrade to its GST portal. With this new feature, taxpayers will have an easier time managing and validating invoices, which will expedite the Input Tax Credit (ITC) claim process.

In this blog, we'll delve into the key features, benefits, and operational details of the IMS. Continue reading to find out how this technology can make GST compliance easier for you.

What is the Invoice Management System (IMS) Under GST?

To help with better invoice handling, the GST portal is integrating a new feature called the Invoice administration System (IMS). Recipient taxpayers can choose to accept, reject, or hold onto bills for further action. The widespread problem of discrepancies between recipient returns and supplier bills, which frequently makes ITC claims more difficult, is addressed by this concept.

Recipients will be able to verify the legitimacy of received invoices using the IMS, ensuring that only accurate invoices are included in their GSTR-2B for Input Tax Credit (ITC) reasons.

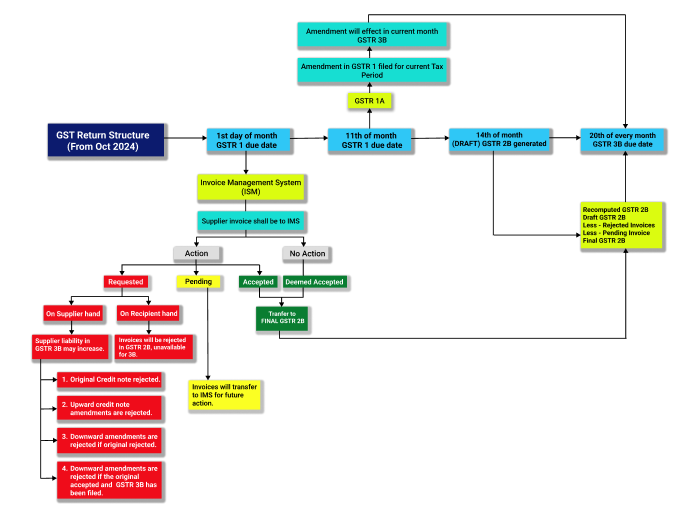

Date of Implementation

The IMS will be available on the GST portal starting 1st October 2024.

How Does the Invoice Management System Work?

Here’s a step-by-step breakdown of how the IMS will operate:

-

Supplier Submissions: Suppliers will use GSTR-1, GSTR-1A, or the Invoice Furnishing Facility (IFF) to upload and send invoices. The recipient's IMS dashboard will thereafter see these invoices.

-

Recipient Actions: Recipients can take one of three actions on each invoice:

-

ACCEPT: The invoice will be included in the recipient’s GSTR-2B as eligible ITC.

-

REJECT: The invoice will not be included in the GSTR-2B and will be marked as rejected.

-

PENDING: The invoice will not be included in the current month’s GSTR-2B but will be carried forward for future action.

-

-

Default Action: The invoice will be "Deemed Accepted" and included in the GSTR-2B if the recipient does not take any action by the twentieth of the month.

-

Amendments: When suppliers make changes to an invoice, the recipient must act on the revised version as the amended invoice will take the place of the original in the IMS.

-

Future Claims: PENDING invoices can be reviewed and acted upon in future months, subject to the limits prescribed by Section 16(4) of the CGST Act, 7.

-

GSTR-2B Generation: The supplier's invoices alone will be taken into account for Input Tax Credit (ITC) in GSTR-2B. Every month on the 14th, the draft GSTR-2B will be published. Recipients can still take action on invoices up until the GSTR-3B is filed.

Key Features of the Invoice Management System (IMS)

-

Enhanced Communication: In order to improve record matching and ITC claim accuracy, the IMS implements a new communication procedure that addresses invoice changes and revisions directly through the portal.

-

Unified Dashboard: All supplier-submitted invoices will be visible on the IMS dashboard, enabling recipients to effectively handle them.

-

No Additional Compliance Burden: At the time of GSTR 2B generation, a record will be considered as ‘Deemed Accepted’ if no action is taken on that record in IMS. Hence IMS is optional for taxpayers and will not add any further compliance for taxpayers.

-

Detailed Categorization: Invoices will be categorized based on recipient actions:

-

Deemed Accepted: Invoices with no action taken will be treated as accepted at the time of GSTR-2B generation.

-

Accepted: Invoices will be included in GSTR-2B.

-

Rejected: Invoices will not be considered for GSTR-2B.

-

Pending: Invoices will be carried forward for future action.

-

-

Support for QRMP Taxpayers: QRMP taxpayers will see records from IFF flow to IMS and be part of GSTR-2B as per actions taken. GSTR-2B for QRMP taxpayers will be generated quarterly, excluding the first two months of a quarter.

-

GSTR 2B will be sequential now i.e. system will generate GSTR 2B of a return period only if GSTR 3B of the previous return period is filed.

-

All the accepted/ deemed accepted/ rejected records will move out of the IMS dashboard after the filing of respective GSTR 3B.

Benefits of the Invoice Management System

-

Improved Audit Precision: IMS allows auditors to verify invoices with greater accuracy, reducing the chances of errors.

-

Error Minimization in GSTR-3B: By providing a summary view of all inward invoices, IMS helps ensure that no invoice is missed before filing GSTR-3B.

-

Simplified Pending Invoice Management: Pending invoices will be carried forward without affecting the current month’s GSTR-2B and GSTR-3B, easing the reconciliation process.

-

Efficient Invoice Amendments: The system will streamline the process for managing amended invoices, ensuring that updates are reflected promptly.

Flow of IMS and Key Points

-

Action Categories:

-

Accept: Invoices will appear in the ‘ITC Available’ section of GSTR-2B and auto-populate in GSTR-3B.

-

Reject: Invoices will be categorized under ‘ITC Rejected’ in GSTR-2B and will not affect GSTR-3B.

-

Pending: These invoices will remain in IMS for future action but will not be included in GSTR-2B or GSTR-3B.

-

-

Record Management: Actions on records must be taken before filing GSTR-3B. Any changes to records or invoices before filing GSTR-1/GSTR-1A/IFF will reset the record’s status on the recipient’s IMS dashboard.

-

Sequential GSTR-2B Generation: GSTR-2B for a period will be generated only after GSTR-3B for the previous period has been filed.

-

Impact on Supplier Liabilities: Rejected invoices, including credit notes and amendments, will impact the supplier’s GSTR-3B for subsequent periods.

Know Your GST | GST Verification | GST Calculator | HSN Code Search | GST Return Status

Frequently Asked Questions

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified