Interest on ITC: Wrongly Availed but Unutilised:The Legal Position and Practical Defence Strategy

Introduction

The levy of interest under Section 50(3) of the Central Goods and Services Tax Act, 2017, on input tax credit (ITC) that has been wrongly availed and utilised, has emerged as one of the most contentious areas in GST compliance. A significant number of notices issued by tax authorities demand interest on ITC that was wrongly availed but reversed before utilisation. This creates a critical legal and operational conflict: Is interest payable under Section 50(3) where ITC was wrongly availed but never utilised?

This article examines the statutory framework, legislative intent, judicial and administrative interpretations, and practical defence strategies available to registered persons facing such demands. It is grounded exclusively in the retrieved context, which includes the CGST Act, 2017, CGST Rules, 2017, Finance Bill, 2022 amendments.

I. Statutory Framework: Section 50(3) — The Core Provision

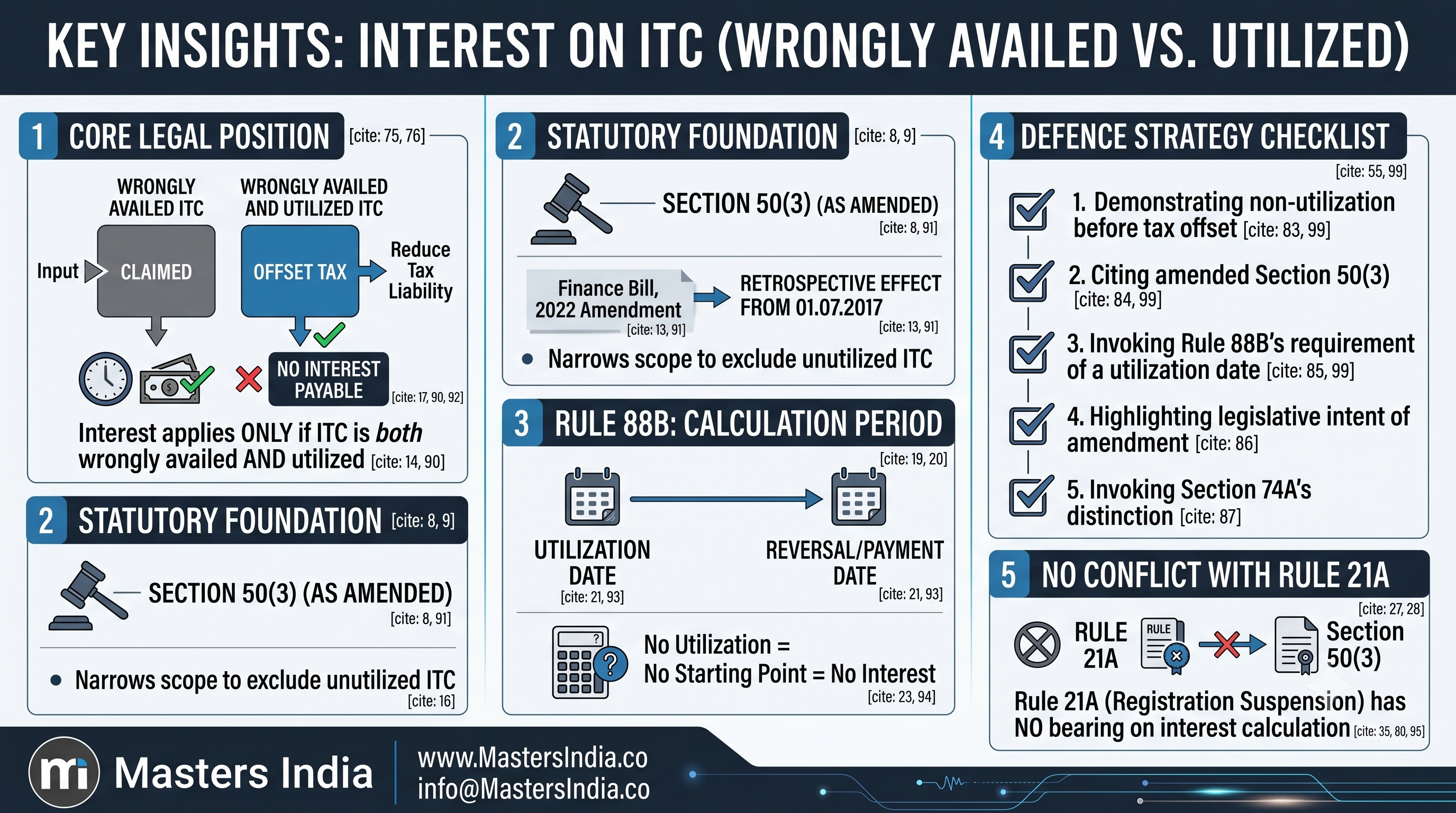

(3) Where the input tax credit has been wrongly availed and utilised, the registered person shall pay interest on such input tax credit wrongly availed and utilised, at such rate not exceeding twenty-four per cent. as may be notified by the Government, on the recommendations of the Council, and the interest shall be calculated, in such manner as may be prescribed.

Explanatory note: Section 50(3) explicitly conditions the levy of interest on two cumulative events: (i) wrongful availing of ITC, and (ii) subsequent utilisation of such credit. The use of the conjunctive “and” is legally significant — it means both conditions must be satisfied for interest to become payable.

This provision was substituted by the Finance Bill, 2022, with retrospective effect from 01.07.2017, via Notification No. 09/2022-Central Tax dated 05.07.2022. The amendment was introduced to implement the recommendation of the 45th GST Council meeting dated 17.09.2021, which clarified that interest should be levied only when ITC is both wrongly availed and utilised.

Prior to this amendment, the law was interpreted to impose interest on mere wrongful availing, even if the credit was reversed before utilisation. The 2022 amendment explicitly narrowed the scope to exclude cases where ITC was reversed prior to utilisation.

"The proposed amendment seeks to implement the recommendation of the 45th GST council meeting dated 17.09.2021 to provide that interest shall be leviable only when the ITC has been wrongly availed and utilised by the registered person. Thus, no interest shall be leviable if ITC has been wrongly availed but not utilised."

Thus, the law now unequivocally states that interest under Section 50(3) is not payable if ITC was wrongly availed but not utilised.

II. Rule 88B — Manner of Calculating Interest

Rule 88B — Manner of calculating interest on delayed payment of tax:

In case, where interest is payable on the amount of input tax credit wrongly availed and utilised in accordance with sub-section (3) of section 50, the interest shall be calculated on the amount of input tax credit wrongly availed and utilised, for the period starting from the date of utilisation of such wrongly availed input tax credit till the date of reversal of such credit or payment of tax in respect of such amount, at such rate as may be notified under said sub-section (3) of section 50.

Explanatory note: Rule 88B reinforces the statutory condition. It prescribes the method of calculation — from the date of utilisation to the date of reversal or payment. This implies that if there is no utilisation, there is no starting point for interest calculation. Hence, the rule cannot be invoked in the absence of utilisation.

This rule does not create a new liability; it merely prescribes the mechanism for computing interest where liability already exists under Section 50(3). Therefore, if the condition of “utilisation” is absent, Rule 88B has no application.

III. Conflict with Rule 21A — Suspension of Registration

The user query references Rule 21A as a potential point of conflict. However, Rule 21A deals with suspension of registration, not interest calculation.

Relevant sub-rules of Rule 21A include:

-

Suspension may occur if the person has not paid tax due, or has not filed returns for six months, or obtained registration by fraud, etc.

-

Suspension is effective from the date of the order.

-

Suspension may be revoked upon furnishing pending returns or compliance with Rule 10A.

Explanatory note: Rule 21A is a procedural enforcement mechanism for non-compliance, including non-payment of tax. It does not create or modify the interest liability under Section 50(3). There is no provision in Rule 21A that imposes interest on wrongly availed but unutilised ITC. Any attempt to link Rule 21A to interest liability under Section 50(3) is legally unfounded.

The retrieved context contains no provision where Rule 21A overrides, modifies, or supplements the interest conditionality under Section 50(3). Therefore, no conflict exists between Section 50(3) and Rule 21A on this issue.

IV. Interpretation

Section 74A, applicable from FY 2024–25, reinforces the distinction between “wrongly availed” and “wrongly availed and utilised” by treating them as separate grounds for determination. Sub-section (1) of Section 74A lists:

“tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilised”

The use of “or” between “wrongly availed” and “wrongly availed and utilised” indicates that these are distinct triggers for action. The former may attract a penalty under Section 122 or a show-cause notice under Section 74A, but only the latter triggers interest under Section 50(3).

This confirms that the legislature treats “wrongly availed” and “wrongly availed and utilised” as separate legal categories — with interest attaching only to the latter.

V. Calculation Disputes — Period of Interest

Where interest is payable (i.e., where ITC was wrongly availed and utilised), Rule 88B prescribes the period:

From the date of utilisation to the date of reversal or payment.

This is critical. If a taxpayer reverses the ITC in the same month it was wrongly availed and utilised, the interest period is minimal. If reversal occurs in a subsequent return (e.g., GSTR-3B or GSTR-9), the interest runs from the date of utilisation (e.g., date of filing GSTR-3B where credit was claimed) to the date of reversal (e.g., date of filing GSTR-3B or GSTR-1A where reversal was reported).

The burden of proving the date of utilisation lies with the department. Mere availing in GSTR-2B or mismatch in GSTR-1 and GSTR-3B does not establish utilisation. Utilisation is established only when the credit is applied to reduce tax liability in a return.

VI. Defence Strategy — When ITC Was Reversed Promptly

Defence Argument 1: Statutory Condition Not Met

“Interest under Section 50(3) is not payable unless ITC is both wrongly availed and utilised. The credit was reversed in the same return or in the next return before any tax liability was offset. Hence, the condition precedent for interest is not satisfied.”

Defence Argument 2: Legislative Intent Supports Non-Levy

“The Finance Bill, 2022, amended Section 50(3) with retrospective effect from 01.07.2017 to ensure interest is levied only on utilised ITC. This was done to prevent harassment of taxpayers who promptly reversed their credits. The amendment reflects the Council’s intent to protect honest taxpayers.”

Defence Argument 3: Rule 88B Requires a Starting Point — Utilisation

“Rule 88B mandates that interest be calculated from the date of utilisation. If no utilisation occurred, there is no basis for interest calculation. The department cannot invent a starting point based on availing or mismatch.”

Defence Argument 4: Section 74A Distinguishes Between Availing and Utilisation

“Section 74A, applicable from FY 2024–25, treats ‘wrongly availed’ and ‘wrongly availed and utilised’ as separate grounds. This confirms that the legislature views them as distinct. Interest cannot be imposed on a category (wrongly availed) that the law itself separates from the interest-triggering category (wrongly availed and utilised).”

Defence Argument 5: Waiver

“If the taxpayer pays the tax liability (including any tax due on reversal) before the notice is issued or within 60 days of notice, interest and penalty may be waived under the waiver provisions.”

VII. Recent Trends in Adjudication

The 2022 amendment and its retrospective application have significantly altered the landscape. Tax authorities are now legally bound to distinguish between availing and utilisation. Any notice demanding interest on unutilised ITC is statutorily unsustainable.

Practically, many taxpayers are now successfully contesting such notices by citing:

-

Section 50(3) as amended

-

The Finance Bill, 2022, and Notification No. 09/2022-Central Tax

-

Rule 88B’s requirement of a utilisation date

VIII. Conclusion

The legal position is clear and unambiguous:

Interest under Section 50(3) of the CGST Act, 2017, is not payable on input tax credit that was wrongly availed but not utilised.

This is not a matter of interpretation — it is a statutory condition explicitly inserted by the Finance Bill, 2022, with retrospective effect from 01.07.2017. The legislative intent is to protect taxpayers who reverse ITC before utilisation. Rule 88B further confirms that interest calculation begins only upon utilisation.

Rule 21A, which governs suspension of registration, has no bearing on interest liability under Section 50(3). Any attempt to conflate the two is legally invalid.

Practical defence strategy must focus on:

-

Demonstrating that the ITC was reversed before any tax liability was offset.

-

Citing Section 50(3) as amended by Finance Bill, 2022.

-

Invoking Rule 88B’s requirement of a utilisation date.

-

Highlighting the legislative intent behind the amendment.

-

Invoking Section 74A’s distinction between availing and utilisation.

Taxpayers facing such notices should file a written reply citing the above, and if necessary, file an appeal under Section 107 with a prayer for waiver of interest on the ground that the statutory condition for levy has not been satisfied.

Closing Summary — Key Legal Positions

-

✅ Interest under Section 50(3) is payable only if ITC is both wrongly availed AND utilised.

(CGST Act, 2017, Section 50(3), as amended by Finance Bill, 2022, w.e.f. 01.07.2017) -

✅ No interest is payable if ITC was wrongly availed but reversed before utilisation.

(45th GST Council Recommendation) -

✅ Rule 88B prescribes the calculation period — from date of utilisation to date of reversal. No utilisation = no interest.

(CGST Rule 88B) -

✅ Rule 21A governs suspension of registration and has no connection to interest liability under Section 50(3).

(CGST Rule 21A — no provision links it to ITC interest) -

✅ Section 74A treats “wrongly availed” and “wrongly availed and utilised” as separate grounds — confirming legislative intent.

(CGST Act, Section 74A) -

✅ Defence strategy: Prove non-utilisation, cite statutory amendment, invoke Rule 88B, and reject notices based on availing alone.

-

❌ Any demand for interest on wrongly availed but unutilised ITC is legally unsustainable and must be contested.

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified