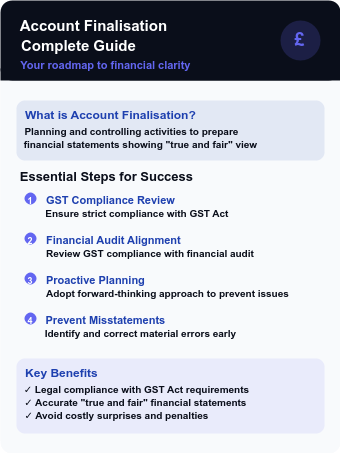

Welcome to your ultimate guide on finalising your accounts! Think of this as your personal roadmap to financial clarity. Finalisation of accounts is the crucial process of planning and controlling activities to prepare your financial statements so they show a "true and fair" view of your business while strictly complying with the law, particularly the Goods and Services Tax (GST) Act.

By adopting a proactive approach and reviewing your GST compliance alongside your financial audit, you will prevent material misstatements and avoid nasty surprises. Let us break down the most important aspects of finalisation into easy, manageable steps.

A: The Pre-Flight Checklist (Reconciliations)

Before you dive into the deep end of your balance sheet, you need to align your worlds. Discrepancies between your books and your GST returns can lead to severe tax liabilities.

Harmonise Your Data

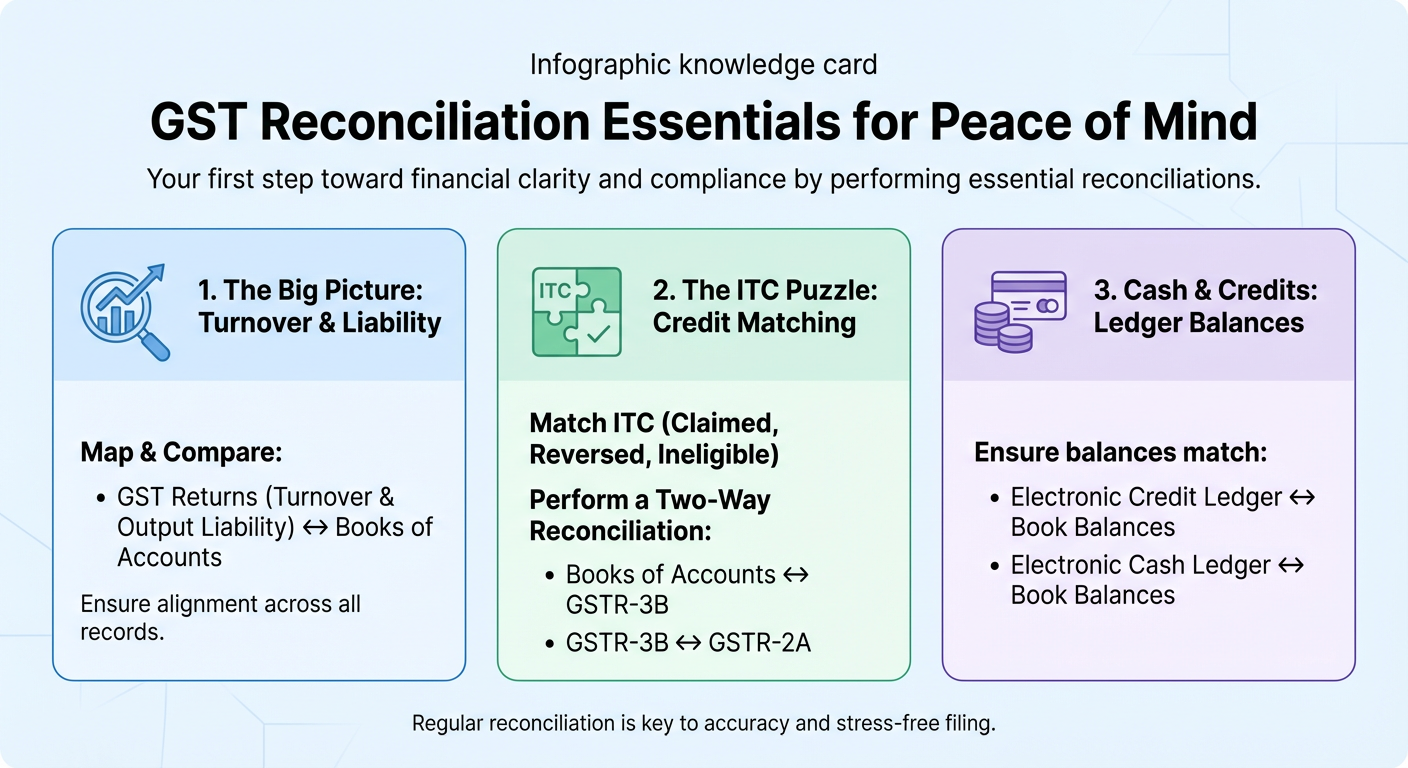

Your first step toward peace of mind is to perform essential reconciliations. Make sure to map and compare the following:

- The Big Picture: Reconcile the turnover and output liability in your GST returns with your books of accounts.

- The ITC Puzzle: Match the Input Tax Credit (ITC) claimed, reversed, and deemed ineligible in your returns with your financial records. Perform a two-way reconciliation: check your books against GSTR-3B, and GSTR-3B against GSTR-2A.

- Cash and Credits: Ensure the balances in your Electronic Credit Ledger and Electronic Cash Ledger match your book balances.

B: Master Your Balance Sheet

Your balance sheet tells the story of what you own and what you owe. Let us ensure it is GST-compliant.

1. Property, Plant, and Equipment (Fixed Assets)

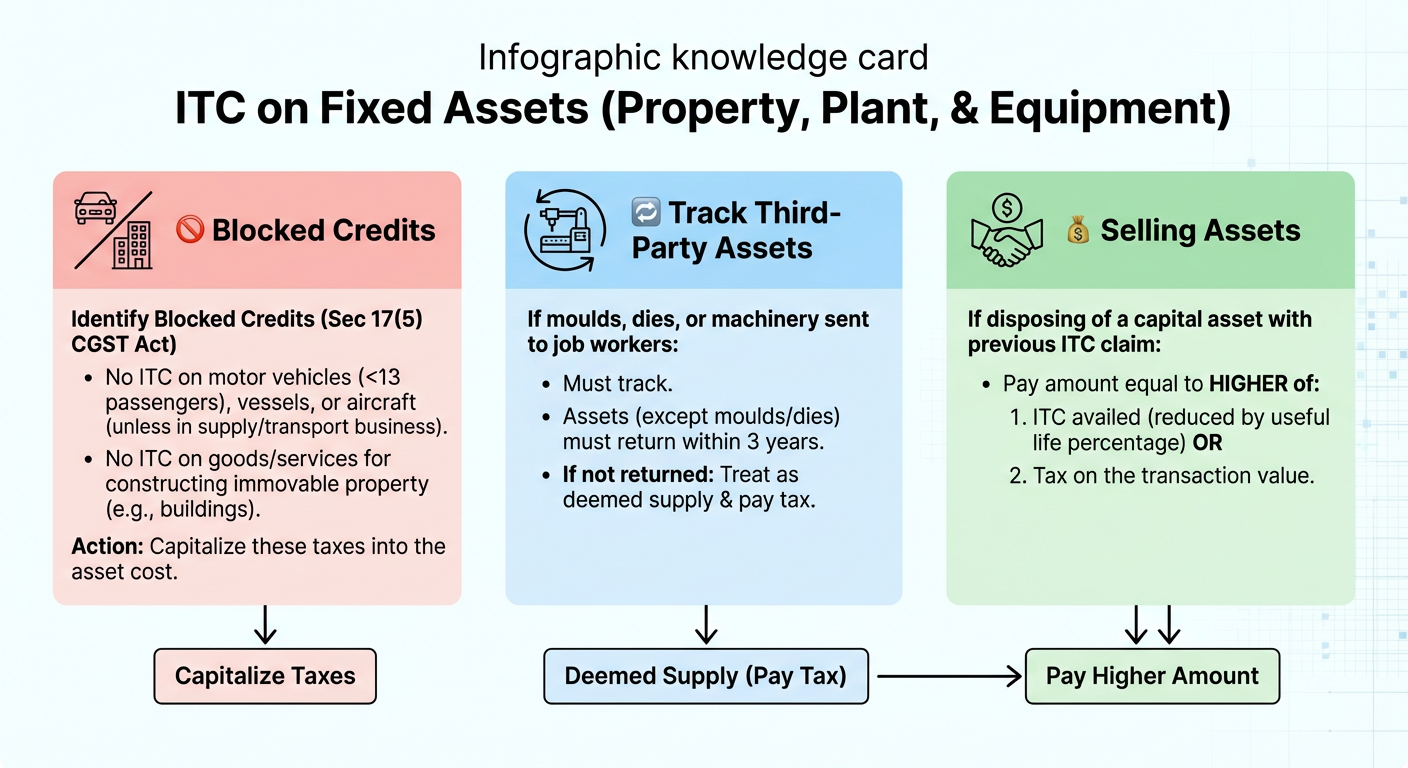

When building your empire, you will buy assets. While you generally get ITC on these purchases, you must be extremely cautious of blocked or ineligible credits.

- Identify Blocked Credits: Under Section 17(5) of the CGST Act, you cannot claim ITC on motor vehicles (for fewer than 13 passengers), vessels, or aircraft, unless you are in the business of supplying them or transporting passengers. You also cannot claim ITC on goods or services used to construct an immovable property (like a building). Action: Capitalize these taxes into the cost of the asset instead of claiming them as ITC.

- Track Third-Party Assets: If you send moulds, dies, or machinery to job workers, you must track them. Assets (other than moulds and dies) must be returned within 3 years. If they are not, you must treat them as a deemed supply and pay tax.

- Selling Assets: If you dispose of a capital asset on which you previously claimed ITC, you must pay an amount equal to the ITC availed (reduced by a prescribed percentage for its useful life) or the tax on the transaction value — whichever is higher.

2. Inventories

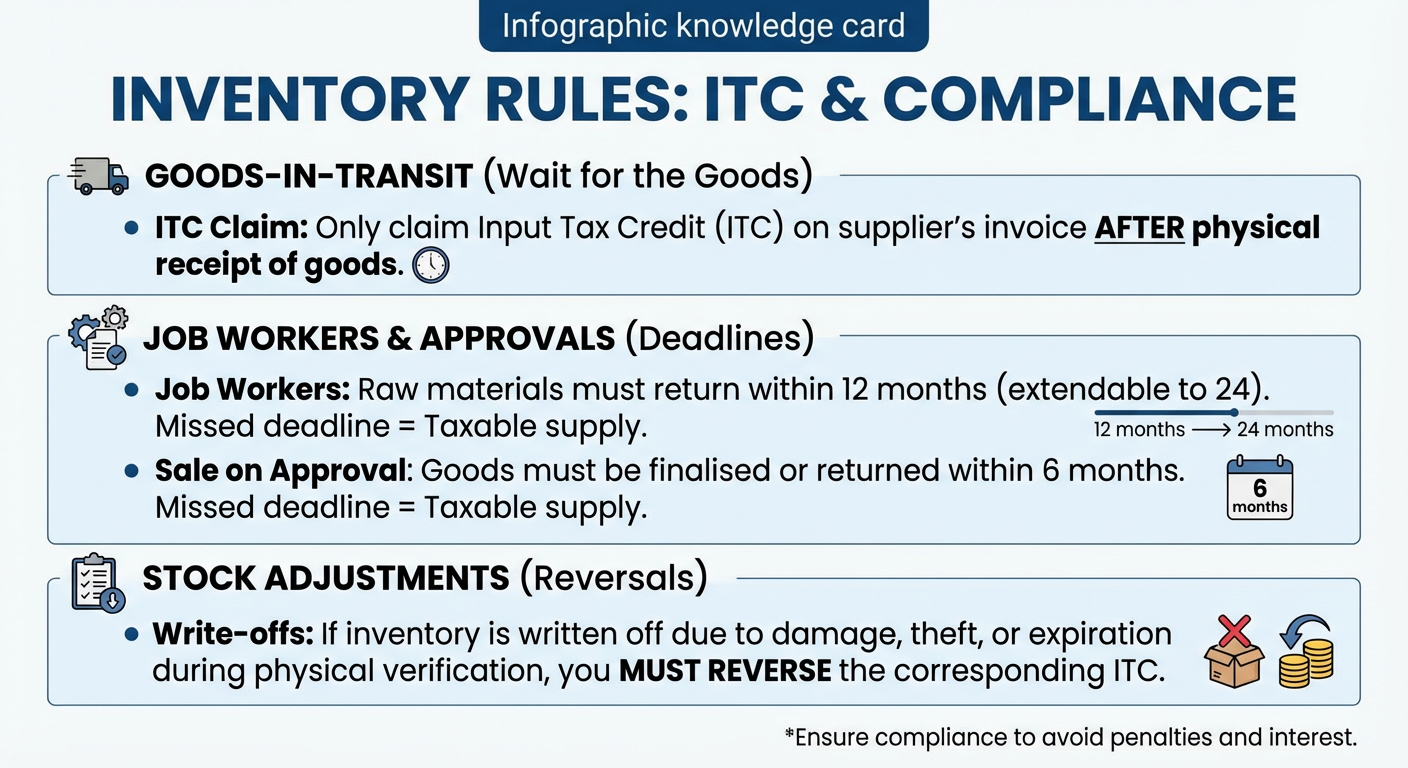

- Wait for the Goods: For goods-in-transit, you can only claim ITC on the supplier's invoice once you physically receive the goods.

- Job Workers & Approvals: Raw materials sent to a job worker must return within 12 months (extendable to 24). Goods sent on "sale on approval basis" must be finalised or returned within 6 months. If you miss these deadlines, they become taxable supplies.

- Stock Adjustments: If you write off inventory due to damage, theft, or expiration during your physical verification, you must reverse the corresponding ITC.

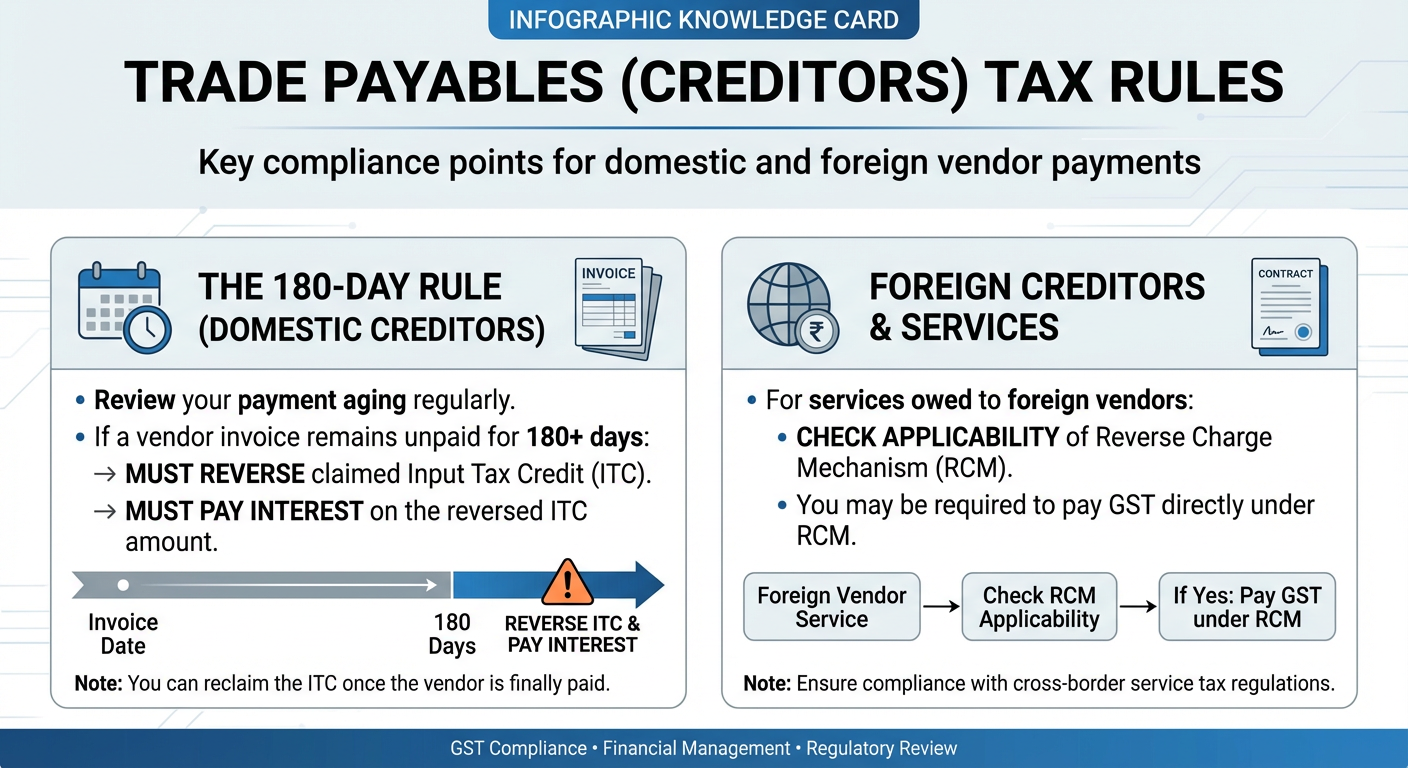

3. Trade Payables (Creditors)

- The 180-Day Rule: For domestic creditors, review your payment aging. If you have not paid a vendor within 180 days from the date of their invoice, you must reverse the ITC you claimed and pay interest on it. You can reclaim it once you finally pay them.

- Foreign Creditors: If you owe foreign vendors for services, check if you need to pay GST under the Reverse Charge Mechanism (RCM).

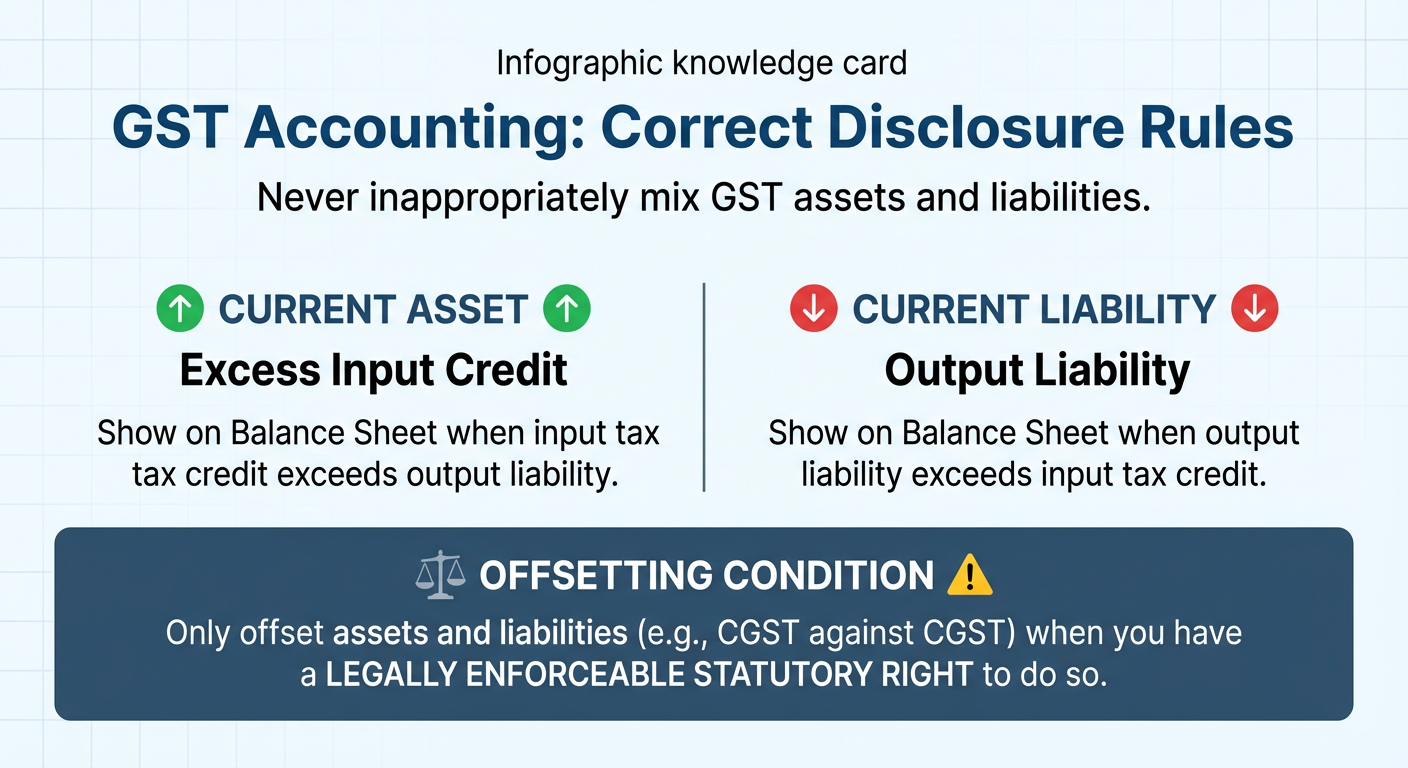

4. Correct Disclosures

Never inappropriately mix your GST assets and liabilities. The excess of your input credit should be shown as a current asset, and your output liability as a current liability. Only offset them (e.g., CGST against CGST) when you have a legally enforceable statutory right to do so.

C: Perfecting the Profit & Loss Statement

Your P&L is the engine of your business. Let us fine-tune it.

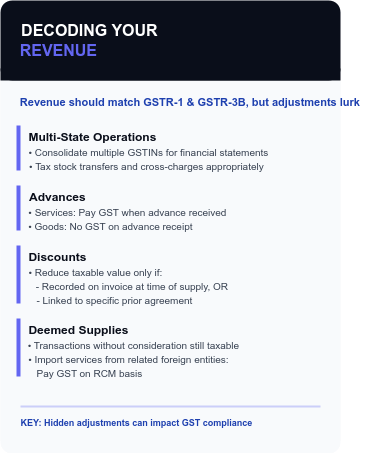

1. Decoding Your Revenue

Your booked revenue should ideally match GSTR-1 and GSTR-3B, but hidden adjustments often lurk here.

- Multi-State Operations: If you have multiple GST registrations (GSTINs), you must consolidate them for your financial statements. Ensure stock transfers or "cross-charges" (like a Head Office providing HR/accounting support to a branch) are taxed appropriately, as these are considered supplies under GST.

- Advances: Did you receive an advance for services to be rendered in the future? If so, you must discharge GST on the date you receive the advance. (Advances for goods are not taxed upon receipt.)

- Discounts: You can only reduce discounts from your taxable value if they are recorded on the invoice at the time of supply, or if they are linked to a specific prior agreement. If you give a discount after the supply without a prior agreement, you cannot reduce your GST liability.

- Deemed Supplies: Be hyper-aware of transactions without consideration. If you import services from a related foreign entity (like your parent company) for business purposes without paying them, it is still a supply and you must pay GST on an RCM basis.

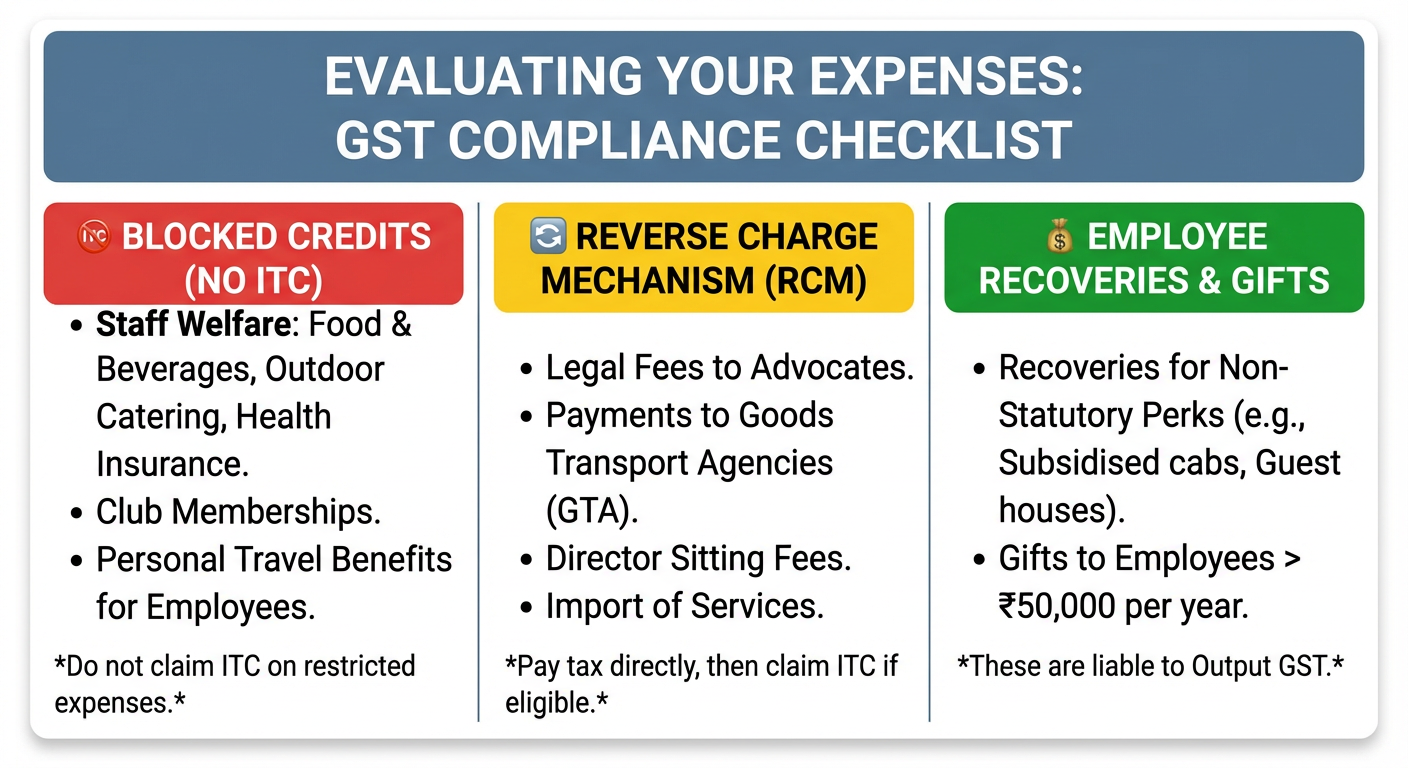

2. Evaluating Your Expenses

To protect your bottom line, ensure you aren't claiming ITC on restricted expenses and that you are paying tax on RCM items.

- Beware the Blocked Credits: Do not claim ITC on staff welfare expenses like food and beverages, outdoor catering, or health insurance. Club memberships and personal travel benefits for employees are also strictly blocked.

- Reverse Charge Mechanism (RCM): You are responsible for paying the tax yourself on certain expenses. Look out for legal fees paid to advocates, payments to Goods Transport Agencies (GTA), director sitting fees, and import of services. Ensure the liability is calculated, paid, and appropriately claimed as ITC if eligible.

- Employee Recoveries: If you recover money from employees for non-statutory perks (like subsidised cabs or guest houses), this is liable to GST. Also, gifts to employees exceeding Rs. 50,000 per year are subject to tax.

D: Acing Your Statutory and Tax Audits

By keeping your books clean throughout the year, you make the final audit a breeze.

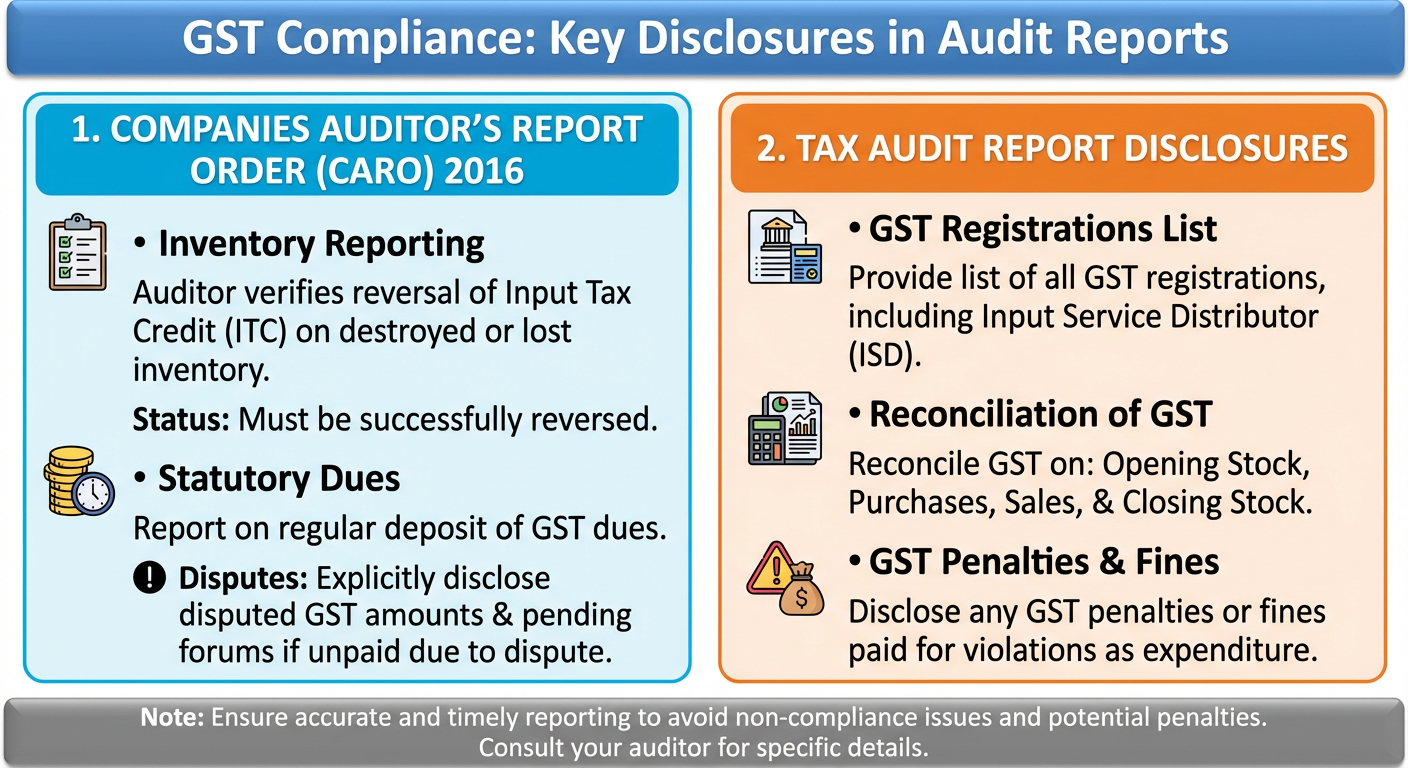

1. Companies Auditor's Report Order (CARO) 2016

- Inventory Reporting: Your auditor will check if ITC on destroyed or lost inventory has been successfully reversed.

- Statutory Dues: You must report whether you are regularly depositing your GST. If you have not paid GST because of a dispute, you must explicitly disclose the disputed amount and the forum where the dispute is pending.

2. Tax Audit Report Disclosures

Your tax audit report requires specific GST disclosures:

- List all your GST registrations, including Input Service Distributor (ISD) registrations.

- Provide a reconciliation of GST on opening stock, purchases, sales, and closing stock.

- Ensure any GST penalties or fines paid for violating the law are disclosed as expenditure.

By systematically addressing each of these headings, you enable yourself to conclude your financial year precisely, confidently, and in complete adherence to legal requirements.

itc reversal rule 42 & 43 | rule 42 of cgst/sgst rules | gst on tdr under rcm | gst set off rules | input tax credit | gst on apartment maintenance charges

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified