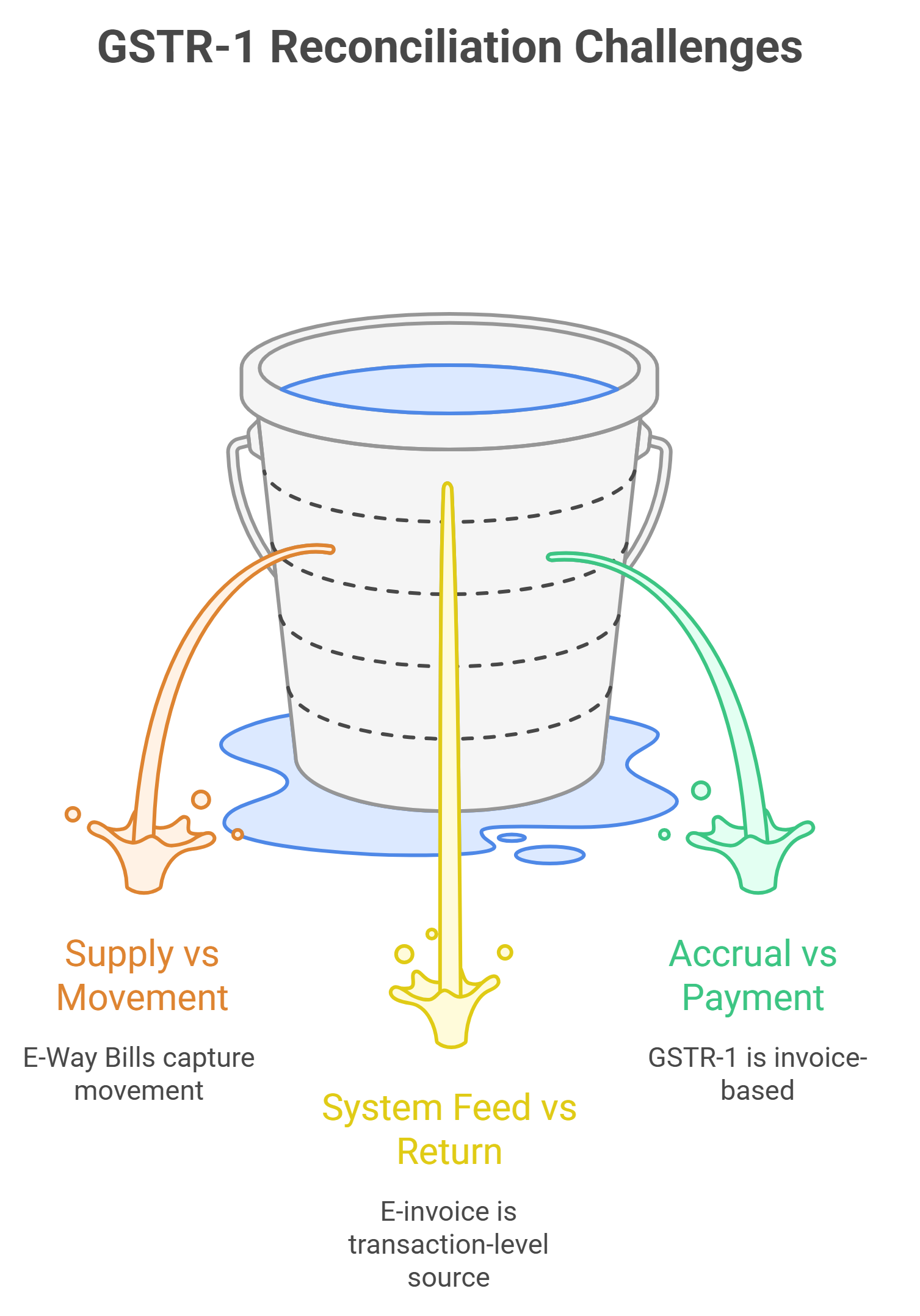

Why GSTR-1 Rarely Matches Other Reports (and How to Reconcile Without Panic)

Businesses keep receiving mismatch alerts GSTR-1 vs E-Way Bills, GSTR-1 vs E-Invoice, GSTR-1 vs TDS.

Most teams assume “mismatch = wrong filing”. That’s the mistake.

A mismatch is only a signal.

Your job is to classify the reason, then close it with evidence or action.

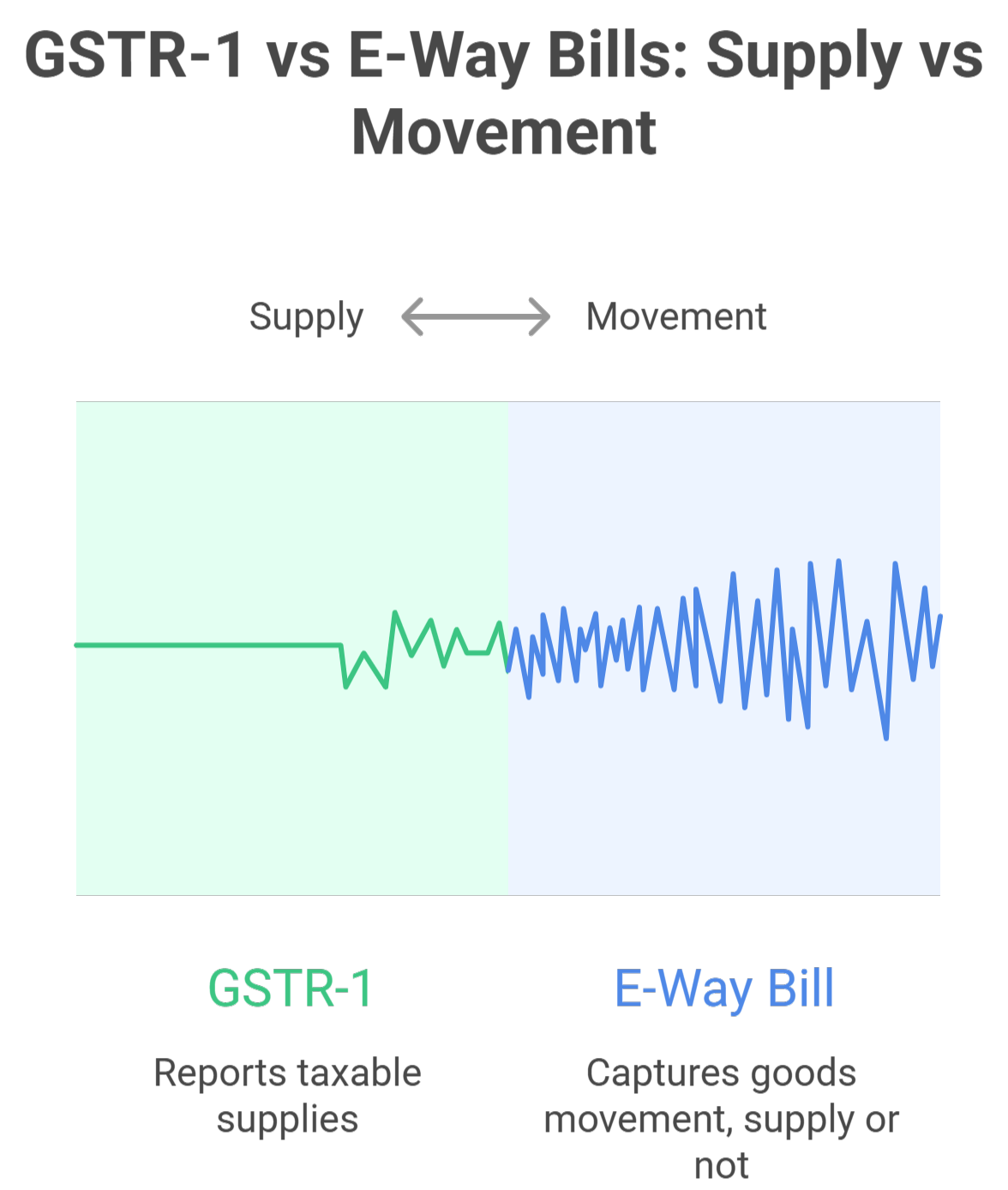

1) GSTR-1 vs E-Way Bills: “Supply” vs “Movement”

GSTR-1 reports supplies.

E-Way Bill captures movement of goods whether supply or not.

So the first truth is simple:

Many E-Way Bills will never appear in GSTR-1. That is normal.

Common reasons for differences

A. Non-supply movements (valid difference)

-

Job work movement (inputs / capital goods / moulds & dies)

-

Stock transfer / branch transfer on delivery challan

-

Goods sent for approval, exhibition, demo, testing, repair

-

Return movement (sales return / replacement)

-

Movement between principal and agent where supply may happen later

B. Timing differences

-

EWB on delivery challan now, invoice later (running account / consolidated billing)

-

Month-end dispatch, invoice raised next month

-

Multiple dispatches against one invoice (or one dispatch against multiple invoices)

C. Data errors

-

Wrong invoice number/date in EWB

-

Duplicate EWB

-

EWB generated but shipment cancelled / not executed

How to reconcile (guiding steps)

-

Don’t compare totals first. Compare documents.

-

Split mismatches into 3 buckets:

-

Non-supply (close with documents)

-

Timing (track to next month)

-

Error (cancel/correct or document)

-

-

For non-supply, keep a clean evidence set:

delivery challan + job work records + movement proof. -

For timing, maintain one tracker: “EWB raised, invoice pending”.

-

For errors, fix the source: wrong doc references must be corrected at dispatch level.

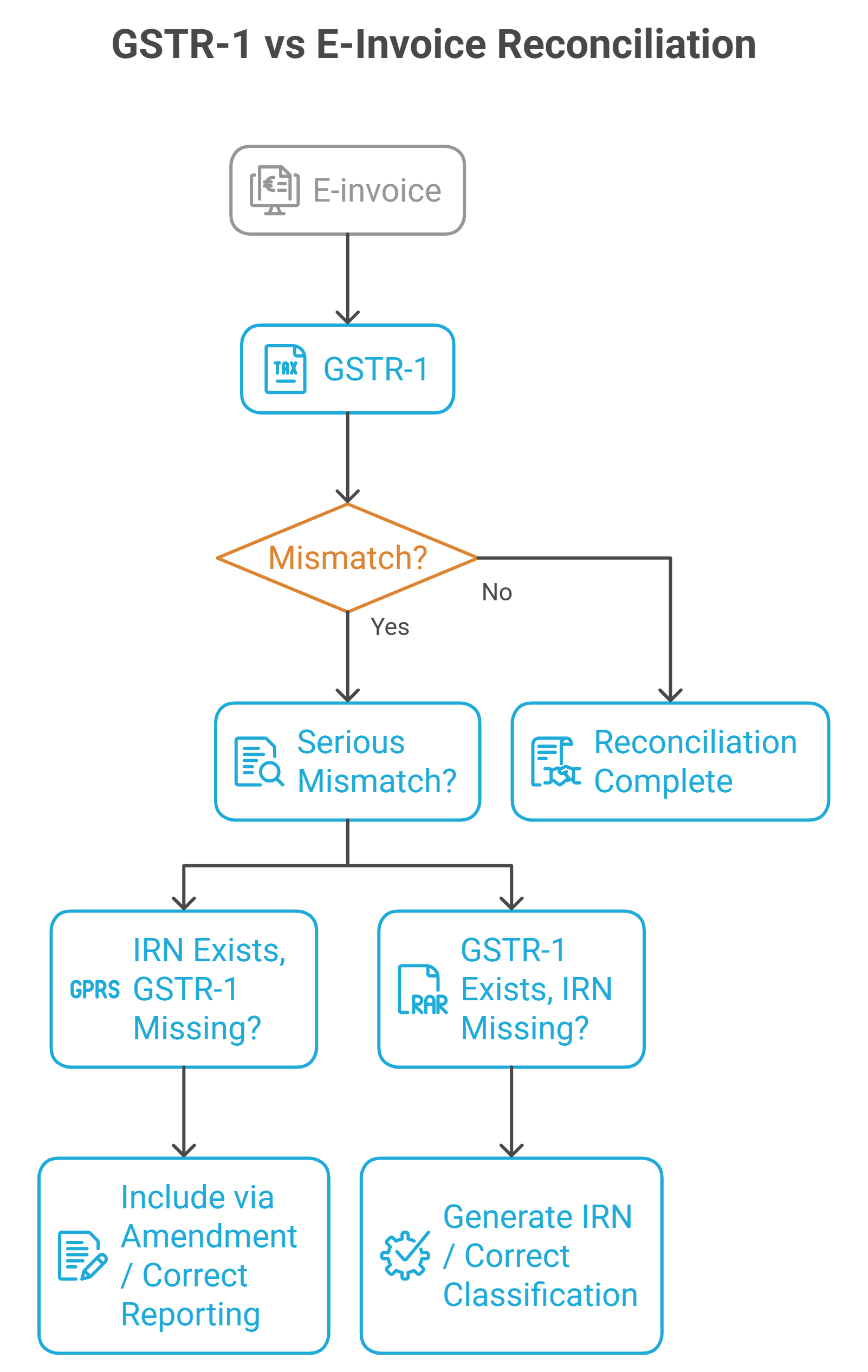

2) GSTR-1 vs E-Invoice: “System feed” vs “Return filed”

E-invoice is the transaction-level source (IRN).

GSTR-1 is the return compilation filed.

So mismatch here is serious only when it indicates:

-

IRN exists but is not reported in GSTR-1, or

-

GSTR-1 invoice exists, but IRN is missing where IRN was required.

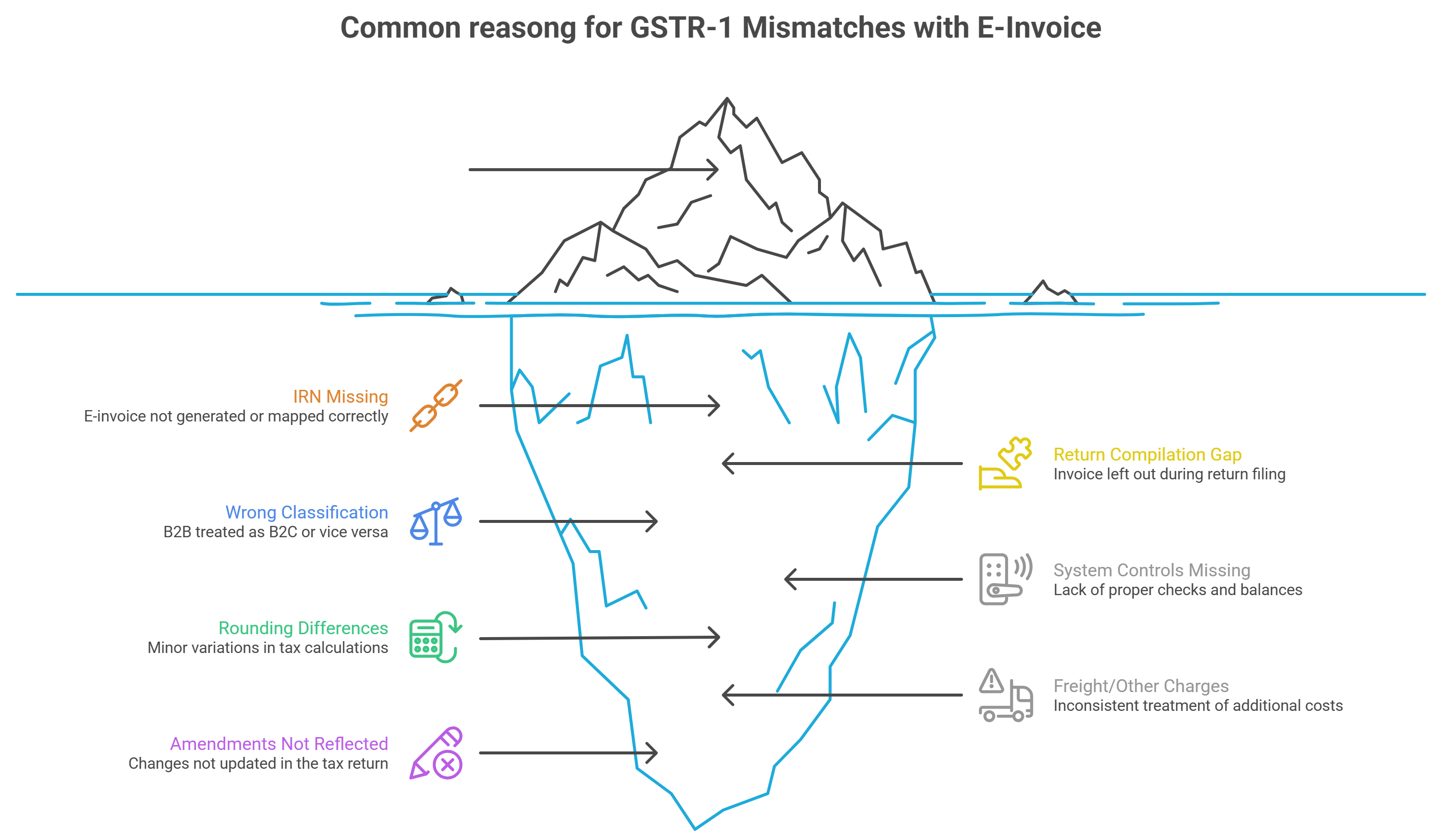

Common reasons for differences

A. IRN exists, GSTR-1 missing

-

Invoice cancelled in ERP but IRN not cancelled (or cancelled late)

-

Invoice falls in one period, but uploaded/reported in another

-

CN/DN generated but mapped wrongly

-

Return compilation gap (invoice left out)

B. GSTR-1 exists, IRN missing

-

IRN required but failed / not generated

-

Wrong classification (B2B treated as B2C or vice versa)

-

System/process controls missing

C. Value / tax mismatch

-

Rounding differences

-

Freight/other charges treated differently

-

Amendments not reflected correctly

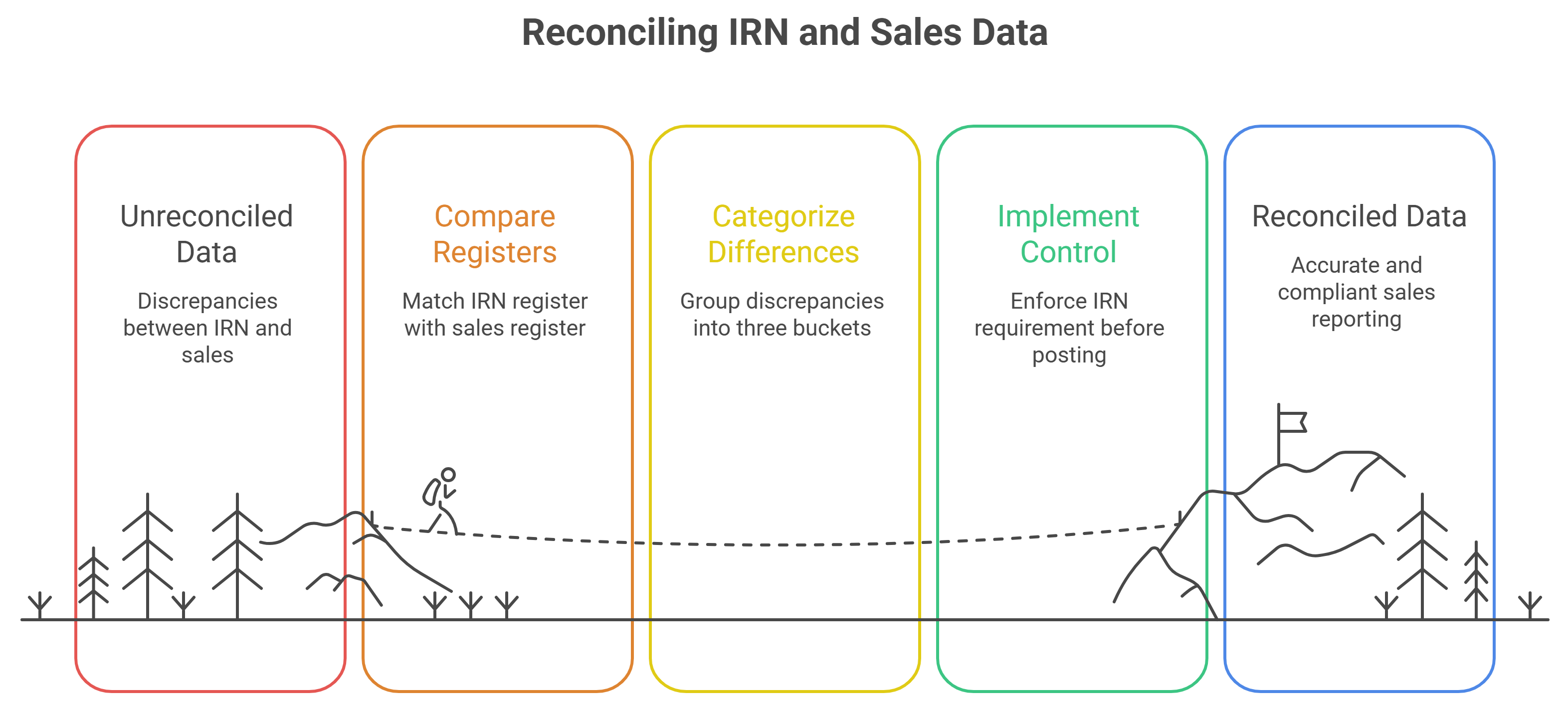

How to reconcile (guiding steps)

-

Start with IRN register vs sales register (not return PDF).

-

Create 3 buckets:

-

IRN present, return missing → include via amendment / correct reporting

-

Return present, IRN missing → treat as compliance gap (fix process)

-

Both present, values differ → correct master/tax computation mapping

-

-

Put one hard control going forward:

“If IRN required, invoice cannot be finally posted without IRN.”

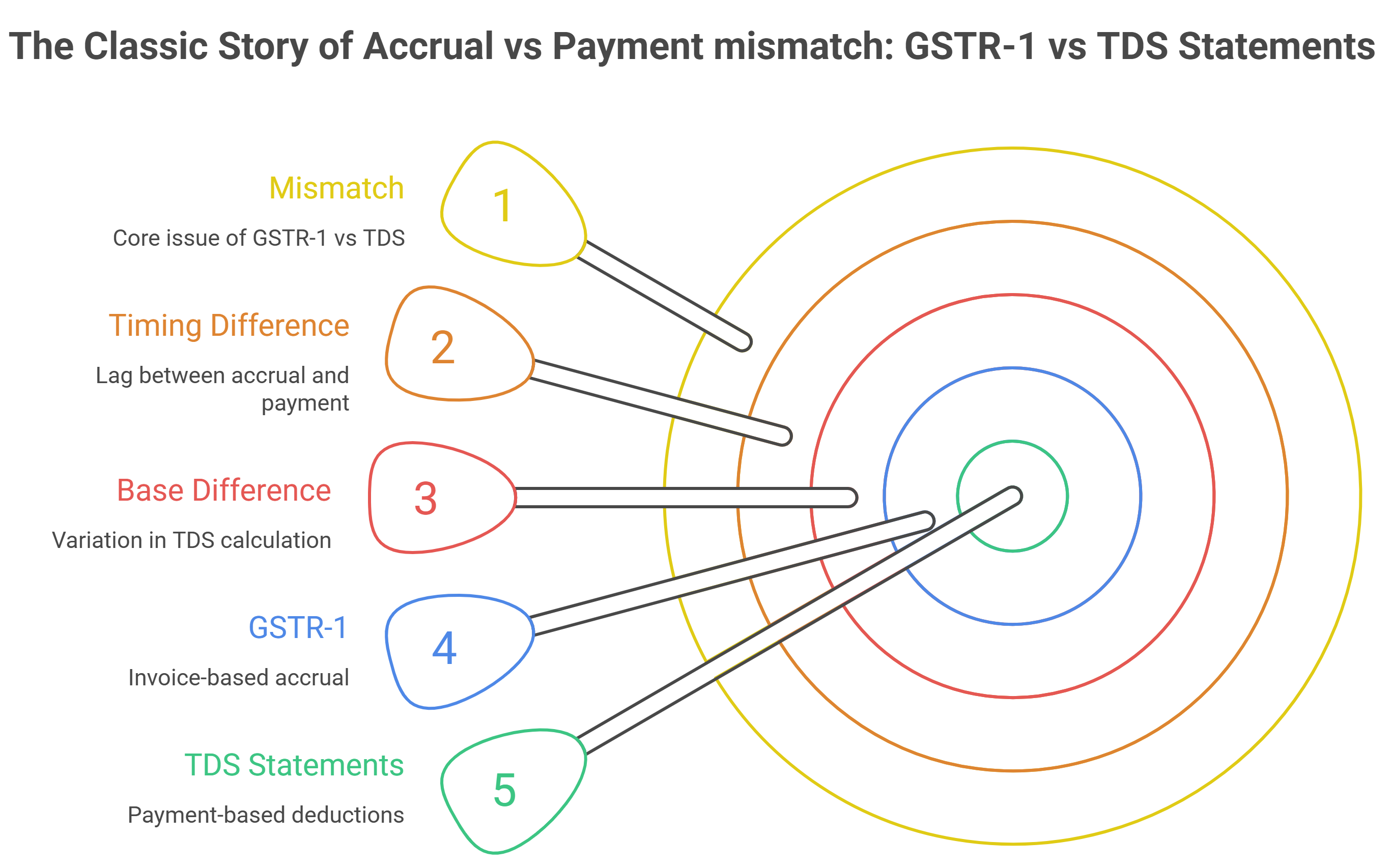

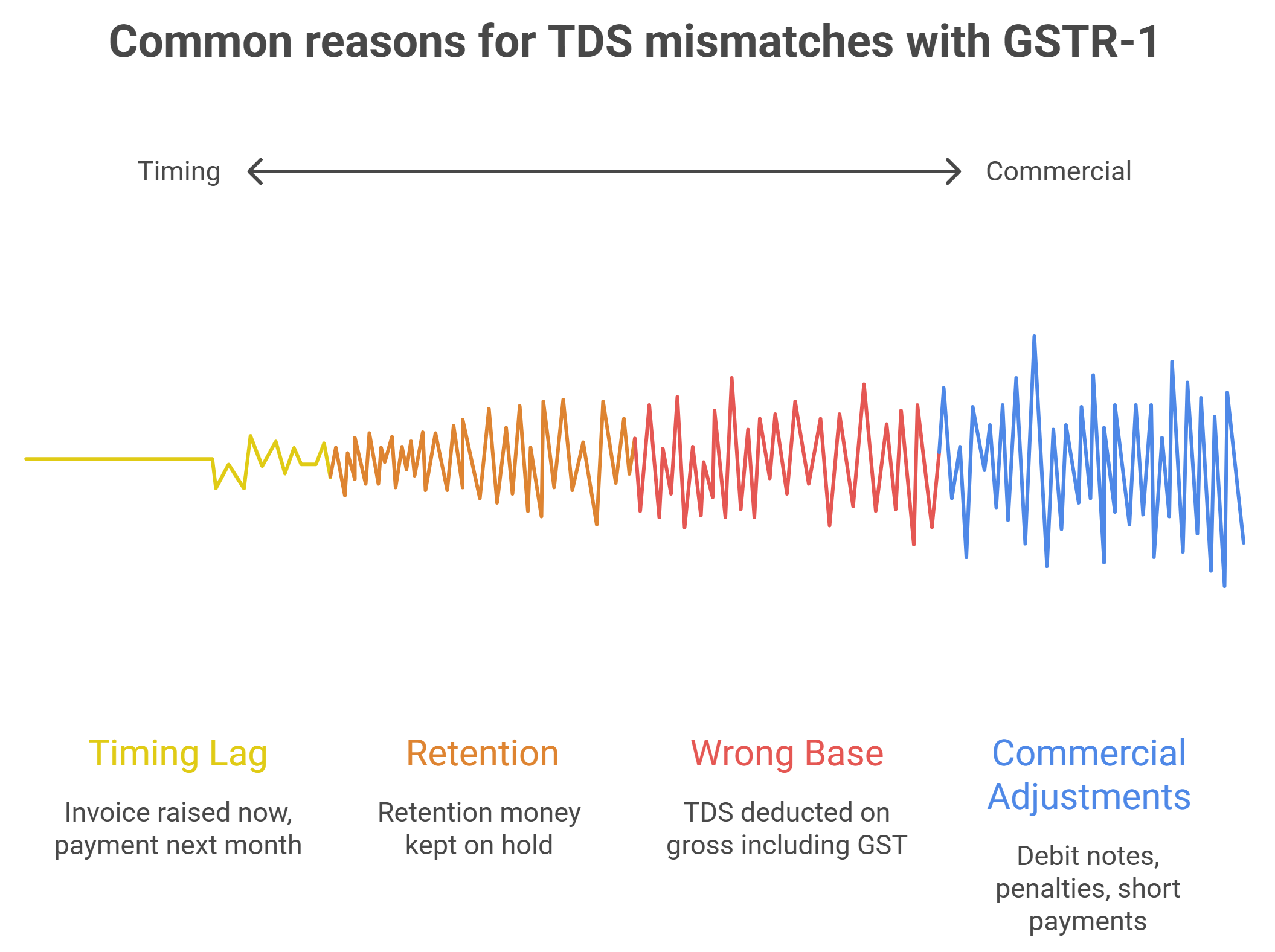

3) GSTR-1 vs TDS Statements: Accrual vs Payment

This mismatch is the most misunderstood.

GSTR-1 is invoice-based (accrual).

TDS is payment-based, and customers often compute it differently.

So mismatch is usually not a GST error.

It’s a timing + base difference.

Common reasons for differences

A. Timing lag

-

Invoice raised now, payment next month/quarter

-

Year-end invoices paid next FY

-

Advance received earlier, invoice raised later

B. Retention / milestone holdbacks

-

Retention money kept on hold in turnkey projects

-

Partial payment against full invoice

-

Performance guarantee adjustments

C. Wrong base for TDS

-

Some customers deduct TDS on gross including GST

-

Some on value excluding GST

-

Some deduct on total payment including reimbursables

D. Commercial adjustments

-

Debit notes, penalties, LD, short payments

-

Disputes settled later

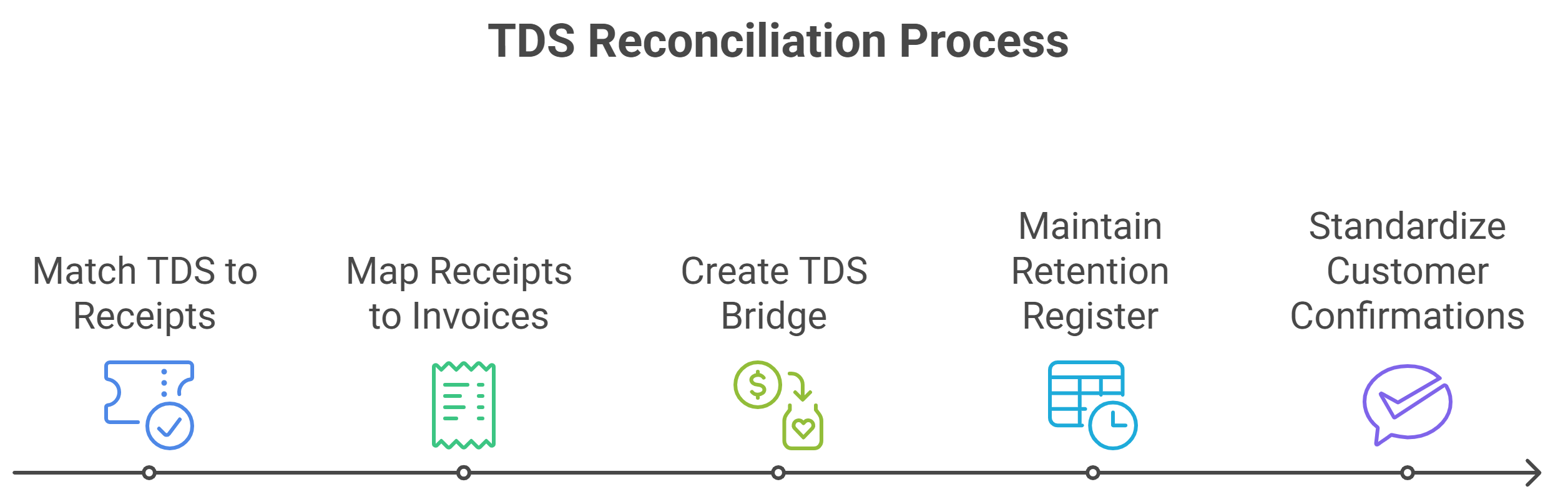

How to reconcile (guiding steps)

-

Match TDS to receipts first, not to invoices.

-

Then map receipts to the invoices settled by those receipts.

-

Create a customer-wise “TDS bridge”:

invoice value → receipt → TDS base → GST component → retention. -

For retention-heavy customers, maintain a retention register with expected release dates.

-

Standardise customer confirmations for large accounts:

“invoice list covered in this payment + base used for TDS”.

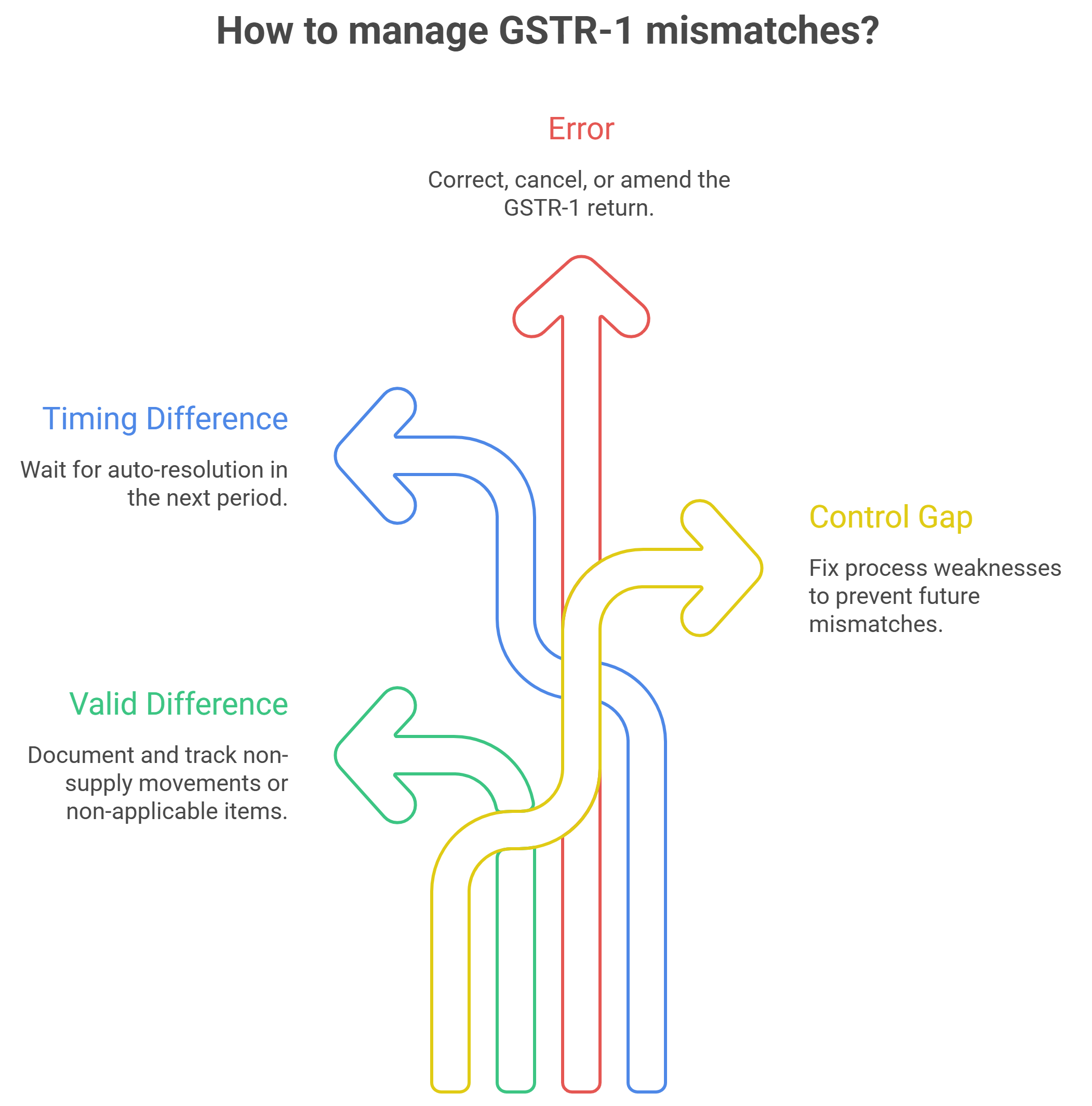

The One Rule That Makes Reconciliation Easy

A mismatch becomes manageable only after you label it as one of these:

-

Valid difference (non-supply movement / not applicable)

-

Timing difference (will auto-resolve next period)

-

Error (needs correction / cancellation / amendment)

-

Control gap (process weakness must be fixed to prevent repeats)

Once classified, the action becomes obvious:

-

Document it,

-

Track it, or

-

Correct it.

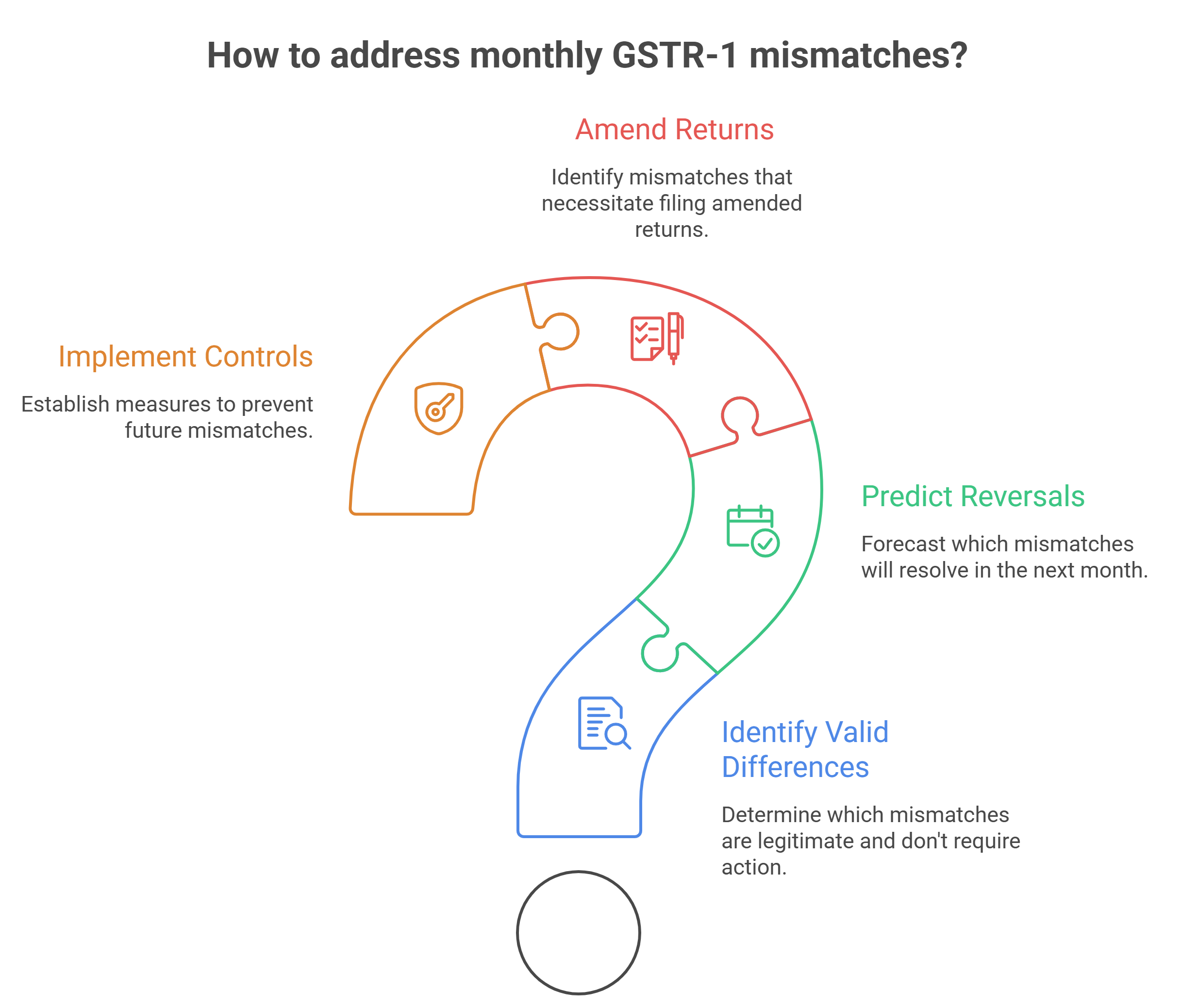

What CFOs Should Ask Their Team Every Month

Instead of “why doesn’t it match?”, ask:

-

What % differences are valid vs errors?

-

Which mismatches will reverse next month?

-

Which ones require return amendments?

-

What controls will stop the same mismatch next month?

Need of GST in India | Powers of GST Officers | GST Audit Procedure | GST Audit Procedure | GST penalty under section 74

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified