GSTN Advisory Effective January 2026: What CFOs and Finance Heads Must Know for Cash Flow & Compliance

GSTN ADVISORY EFFECTIVE JANUARY 2026

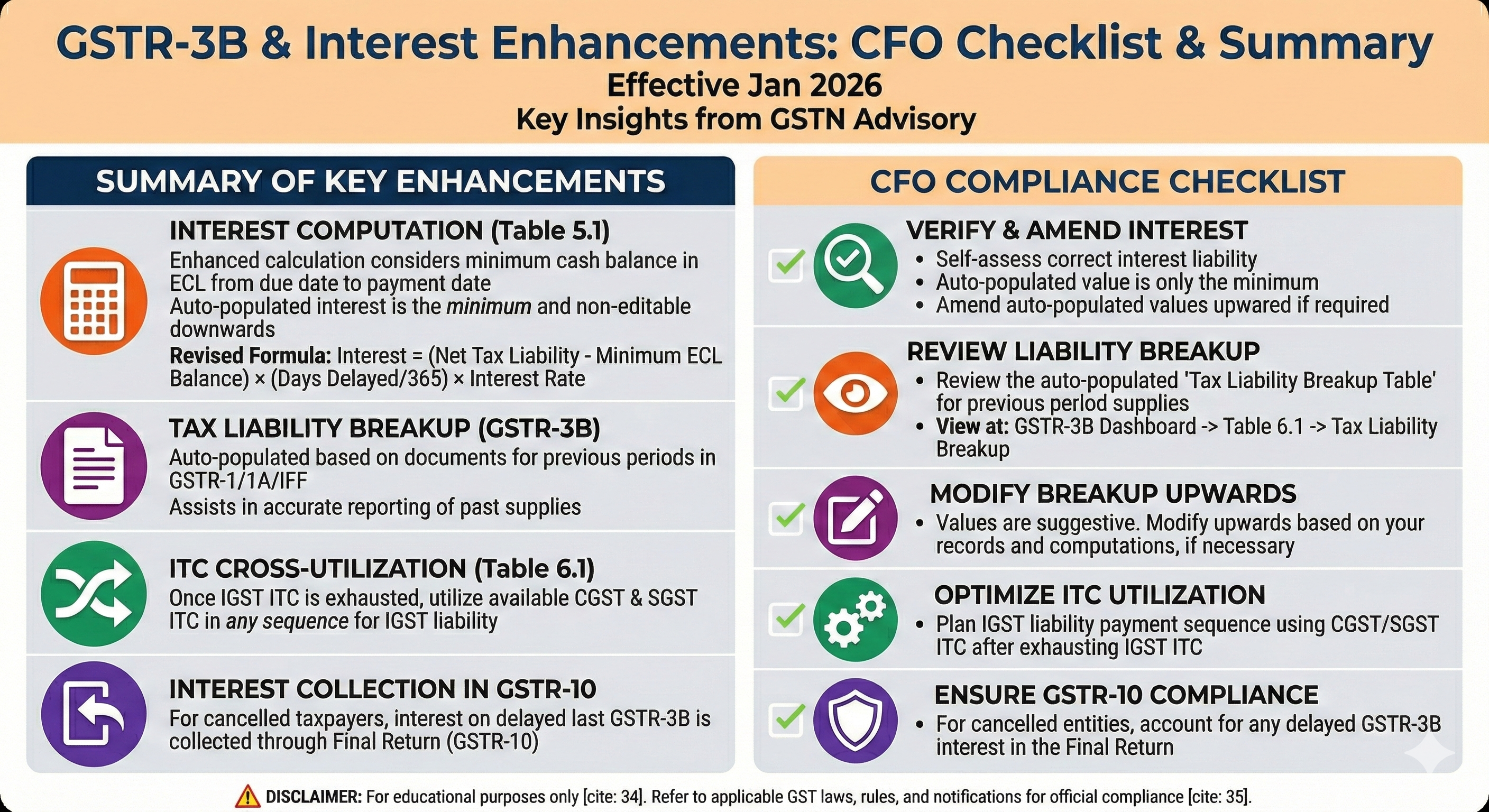

The GST Network (GSTN) has issued an important advisory introducing multiple system-level enhancements in GSTR-3B, effective from the January-2026 tax period onwards. These changes primarily impact interest computation, ITC utilisation, reporting of past-period liabilities, and closure of cancelled registrations.

While technical in nature, these changes have direct implications for cash flow planning, compliance certainty, and risk management for businesses.

This article explains the changes in simple terms and guides CFOs and Directors Finance on how to align their teams and processes.

1. INTEREST CALCULATION – A CASH FLOW FRIENDLY SHIFT

WHAT HAS CHANGED

Earlier, interest on delayed GSTR-3B filings was often computed without fully recognising cash already available in the Electronic Cash Ledger (ECL) during the delay period.

From January-2026, GSTN will compute interest by giving benefit of the minimum cash balance available in ECL from the due date till the date of tax payment (offset).

In simple terms:

Interest will apply only on the net unpaid portion, not on amounts already deposited but not yet offset.

WHY THIS MATTERS FOR CFOs

-

Businesses that deposit cash in advance but file returns late will now see lower interest outgo.

-

This aligns system computation with commercial reality and Section 50 proviso.

-

It rewards better treasury discipline even when operational delays occur.

CFO ACTION POINT

Ensure teams deposit cash early, even if final return filing is delayed. This can now directly reduce interest cost.

2. SYSTEM-COMPUTED INTEREST – MINIMUM PAYABLE, NOT NEGOTIABLE

WHAT HAS CHANGED

Interest auto-populated in Table 5.1 of GSTR-3B will:

-

Be non-editable downward

-

Represent the minimum interest payable

Taxpayers may increase it if required based on self-assessment, but cannot reduce it.

POSITIVE IMPACT

-

Eliminates ambiguity and inconsistent interpretations.

-

Reduces future disputes on “short-paid interest”.

-

Provides CFOs clarity on minimum statutory exposure at filing stage.

NEW OPERATIONAL RISK

-

Finance teams must review system-computed interest carefully.

-

Errors in underlying data (net liability or cash ledger balance) can flow into interest computation.

CFO ACTION POINT

Add a mandatory interest validation step before final GSTR-3B submission.

3. AUTO-POPULATION OF PAST-PERIOD TAX LIABILITY – BETTER TRACEABILITY

WHAT HAS CHANGED

GSTN will now auto-populate the Tax Liability Breakup Table in GSTR-3B for:

-

Supplies of earlier tax periods

-

Reported now in GSTR-1 / IFF

-

Where tax is paid in the current GSTR-3B

This is based on invoice/document date, not return period.

WHY THIS HELPS INDUSTRY

-

Improves period-wise accuracy of tax reporting.

-

Reduces manual disclosures and classification errors.

-

Strengthens internal audit and statutory reconciliation.

WHERE IT APPEARS

Login → GSTR-3B → Table 6.1 (Payment of Tax) → Tax Liability Breakup

CFO ACTION POINT

Ensure invoice dates in GSTR-1 align with actual transaction periods. Document discipline becomes critical.

4. ITC UTILISATION FLEXIBILITY – IMPROVED WORKING CAPITAL MANAGEMENT

WHAT HAS CHANGED

Once IGST ITC is fully exhausted, the system will allow payment of IGST liability using:

-

CGST ITC

-

SGST ITC

in any sequence.

BENEFIT TO CFOs

-

Removes system-imposed rigidity.

-

Reduces forced cash payments.

-

Improves working capital optimisation, especially for multi-state operations.

CFO ACTION POINT

Revisit internal ITC utilisation strategies and cash forecasting models.

5. CANCELLED REGISTRATIONS – CLEANER EXIT MECHANISM

WHAT HAS CHANGED

For cancelled registrations:

-

If the last applicable GSTR-3B is filed late,

-

Interest will now be levied and collected through GSTR-10 (Final Return).

WHY THIS IS GOOD GOVERNANCE

-

Ensures clean closure of GST liabilities.

-

Reduces legacy exposure post cancellation.

-

Brings certainty to business restructuring, mergers, or shutdowns.

CFO ACTION POINT

Plan adequate cash provisioning at the time of final return filing.

OVERALL TAKEAWAY FOR CFOs AND FINANCE LEADERS

This advisory signals a clear direction:

-

Greater system-driven compliance

-

Reduced interpretational disputes

-

Better alignment with cash flow realities

-

Enhanced data-driven risk management by GST authorities

For industry, these changes are largely positive, provided internal teams are aligned early.

FINAL CFO CHECKLIST

-

Encourage early cash deposits to reduce interest exposure

-

Strengthen invoice-date discipline

-

Add interest validation controls in GSTR-3B process

-

Update ITC utilisation SOPs

-

Budget for interest at exit stage (GSTR-10)

Powers of GST Officers | DRC-01 | GST Audit Procedure | GST ADT-01 | Penalty for Non GST Registration | GST Inspector Power

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified