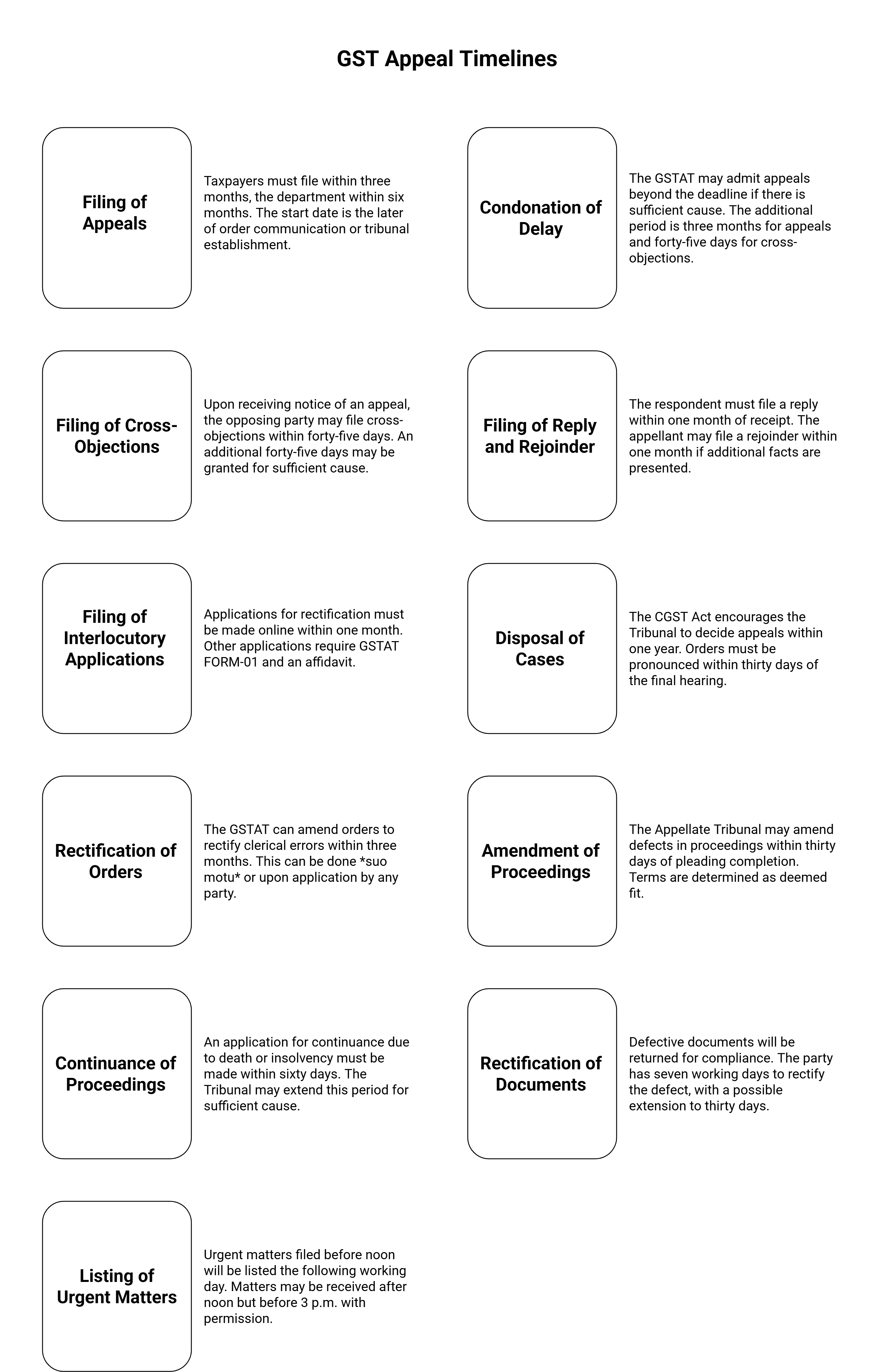

GST Appeal Timelines

The Goods and Services Tax Appellate Tribunal (GSTAT) (Procedure) Rules, 2025, along with the Central Goods and Services Tax (CGST) Act, 2017, outline various timelines for the filing of appeals, replies, rejoinders, and other applications, aiming to streamline the GST dispute resolution process.

• Filing of Appeals (Institution of Appeals - Chapter III):

◦ For Taxpayers: An appeal to the GSTAT must generally be filed within three months from the date the order is communicated to the person preferring the appeal.

◦ For the Department: The Commissioner (or an authorised officer) may apply to the GSTAT within six months from the date the order has been passed for determination of specified points.

◦ Start Date of Limitation Period: The three-month/six-month period for filing appeals shall be considered to start from the later of (A) the date of communication of the order, or (B) the date on which the President or the State President of the Appellate Tribunal, after its constitution, enters office. This provision addresses cases where the Tribunal was not yet functional.

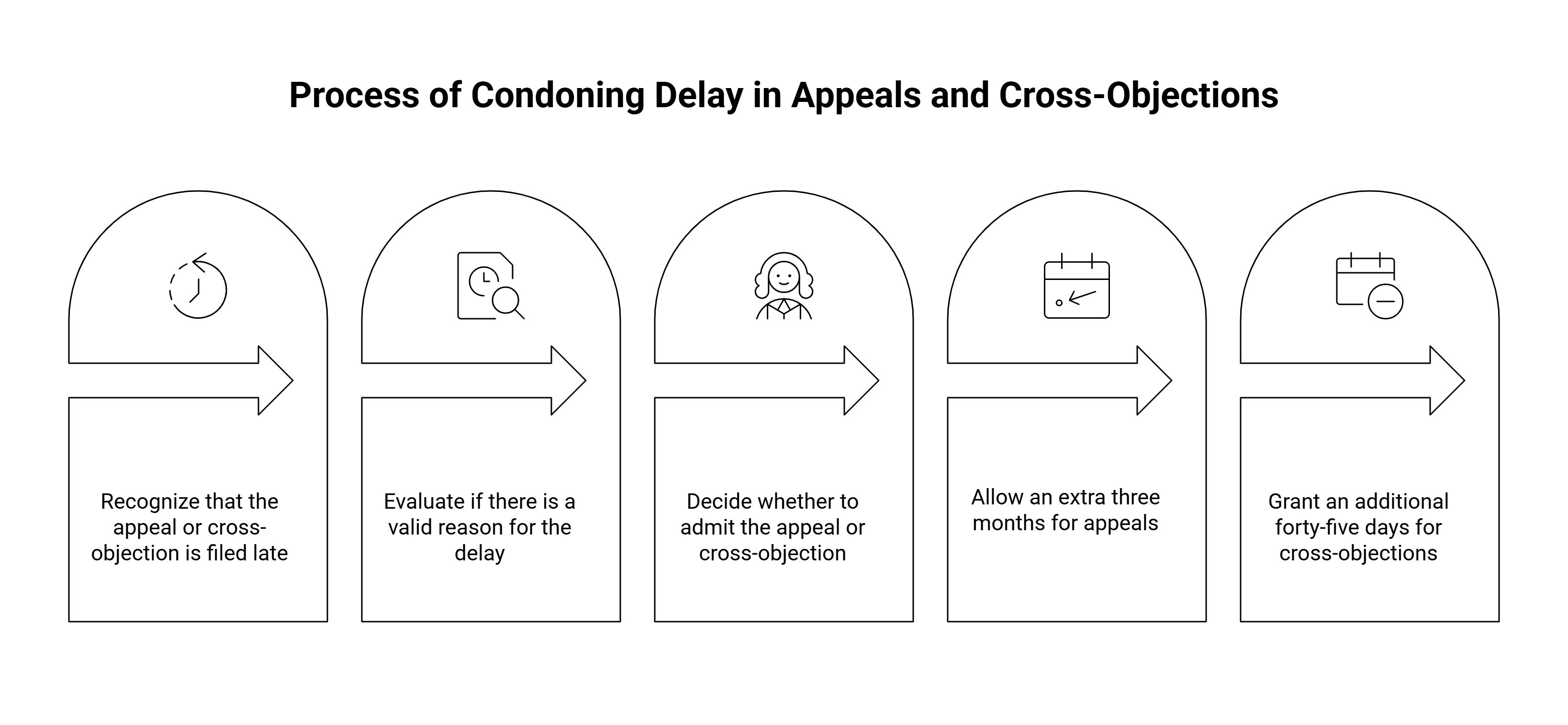

• Condonation of Delay:

◦ The GSTAT may admit an appeal or permit the filing of a memorandum of cross-objections beyond the initial prescribed period if it is satisfied that there was sufficient cause for not presenting it within that period. For appeals, this additional period is three months, and for cross-objections, it is forty-five days.

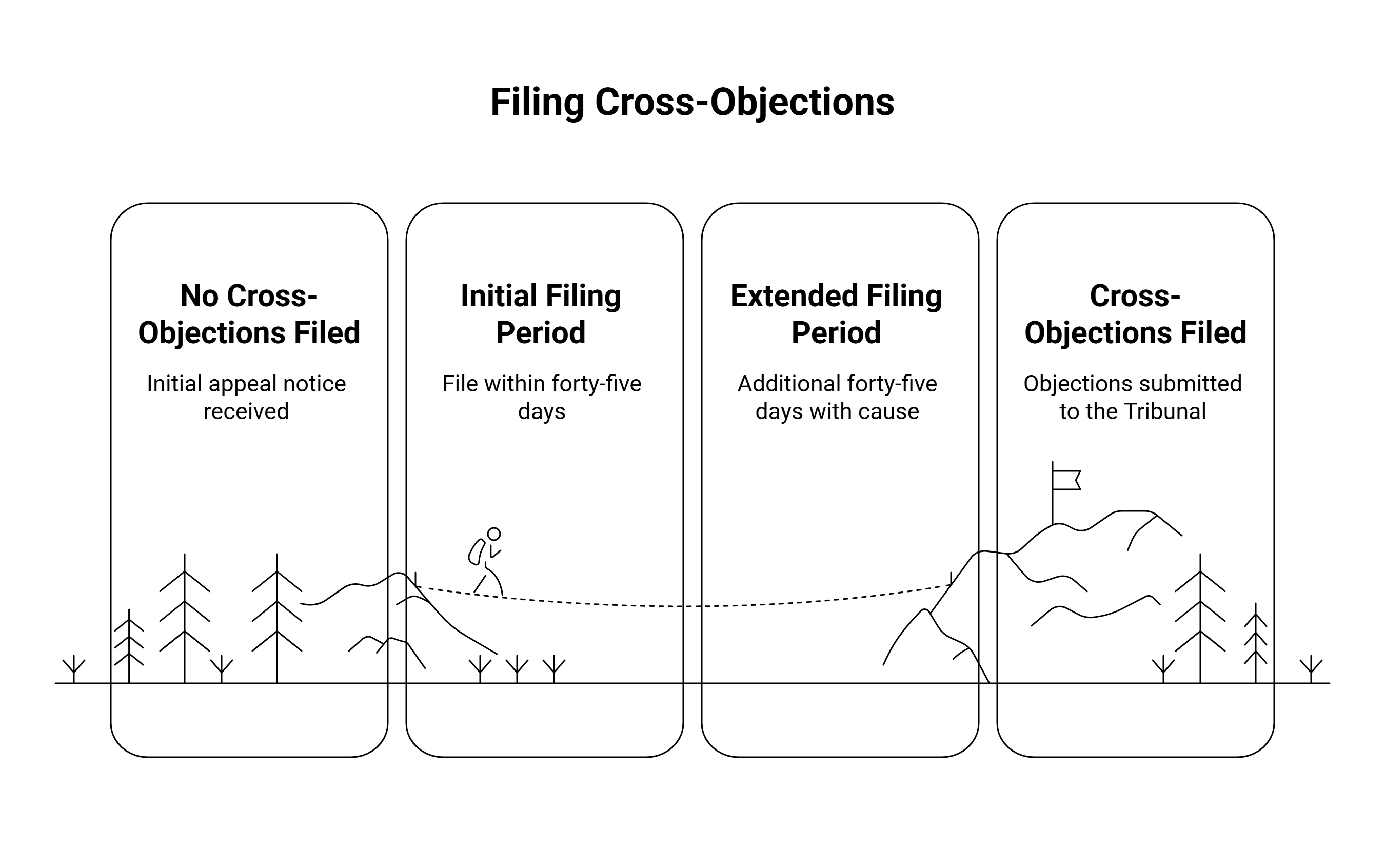

• Filing of Cross-Objections:

◦ Upon receiving notice that an appeal has been preferred, the party against whom the appeal has been preferred may file a memorandum of cross-objections within forty-five days of the receipt of notice.

◦ The Tribunal may permit the filing of cross-objections within an additional forty-five days after the expiry of the initial period if sufficient cause is shown.

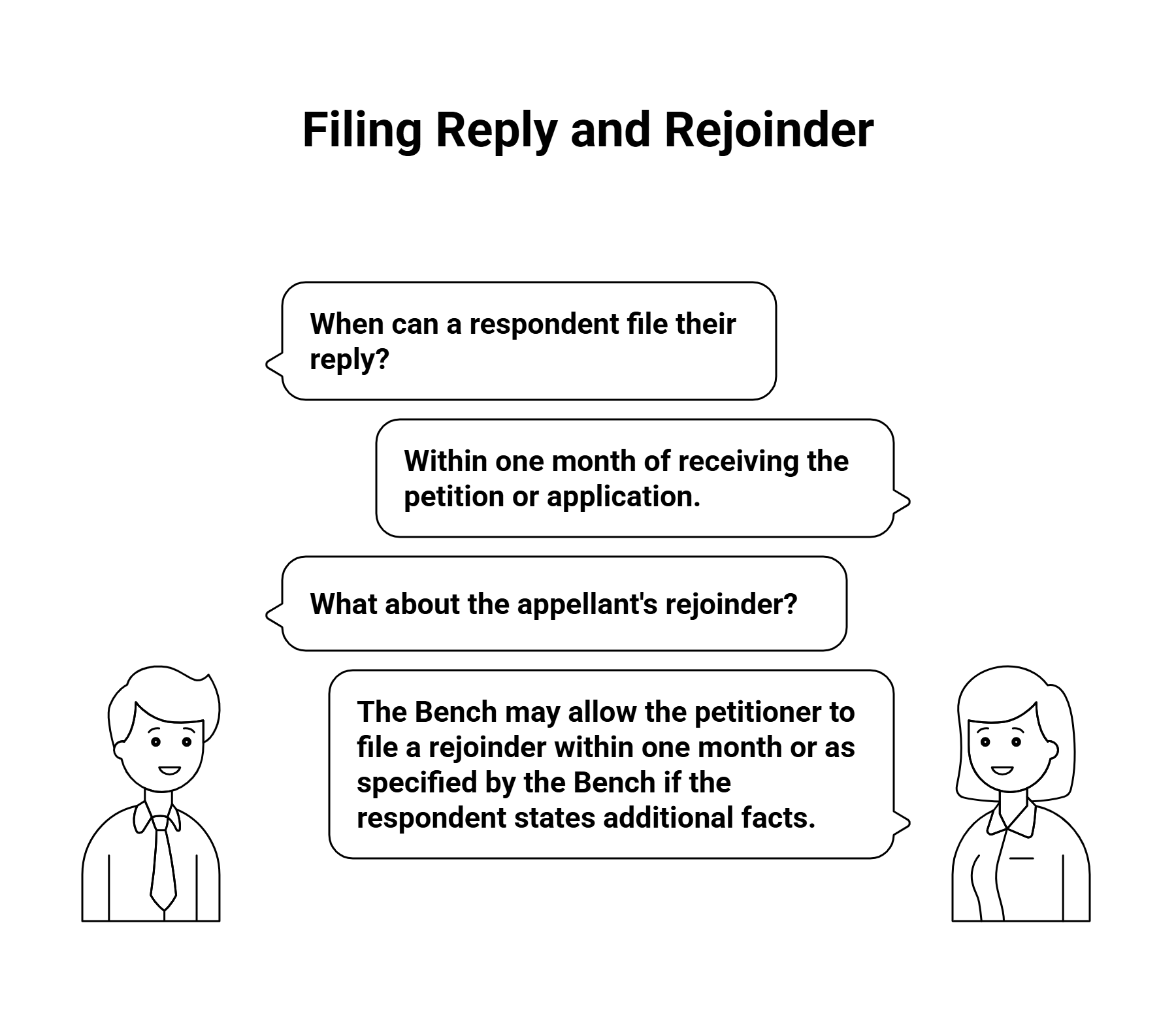

• Filing of Reply and Rejoinder (Chapter III):

◦ Respondent's Reply: Each respondent may file their reply to the petition or application and copies of documents with the Registrar within one month of receipt. A copy of the reply must be forthwith served on the applicant by the respondent.

◦ Appellant's Rejoinder: If the respondent states additional facts, the Bench may allow the petitioner to file a rejoinder within one month or within such time as specified or extended by the Bench, with an advance copy served upon the respondent.

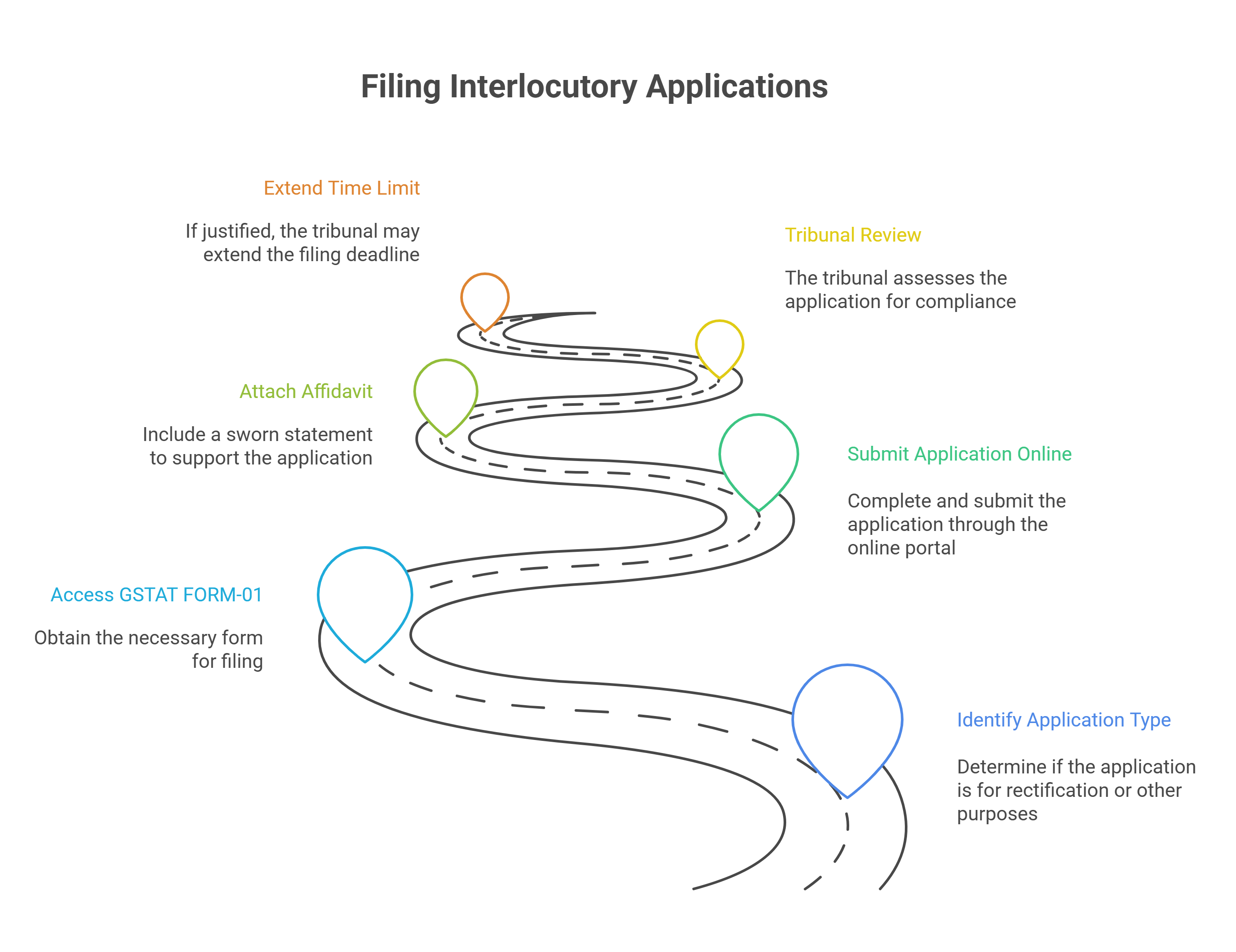

• Filing of Interlocutory Applications:

◦ An application for rectification of an order must be made online (using GSTAT FORM-01) within one month from the date of the final order.

◦ Other interlocutory applications, such as for stay, condonation of delay (as above), or early hearing, must use GSTAT FORM-01 and be supported by an affidavit.

◦ The Appellate Tribunal has the power to extend any time limit fixed by the rules or by its own order, even if the application for extension is made after the original period has expired, if the justice of the case requires it.

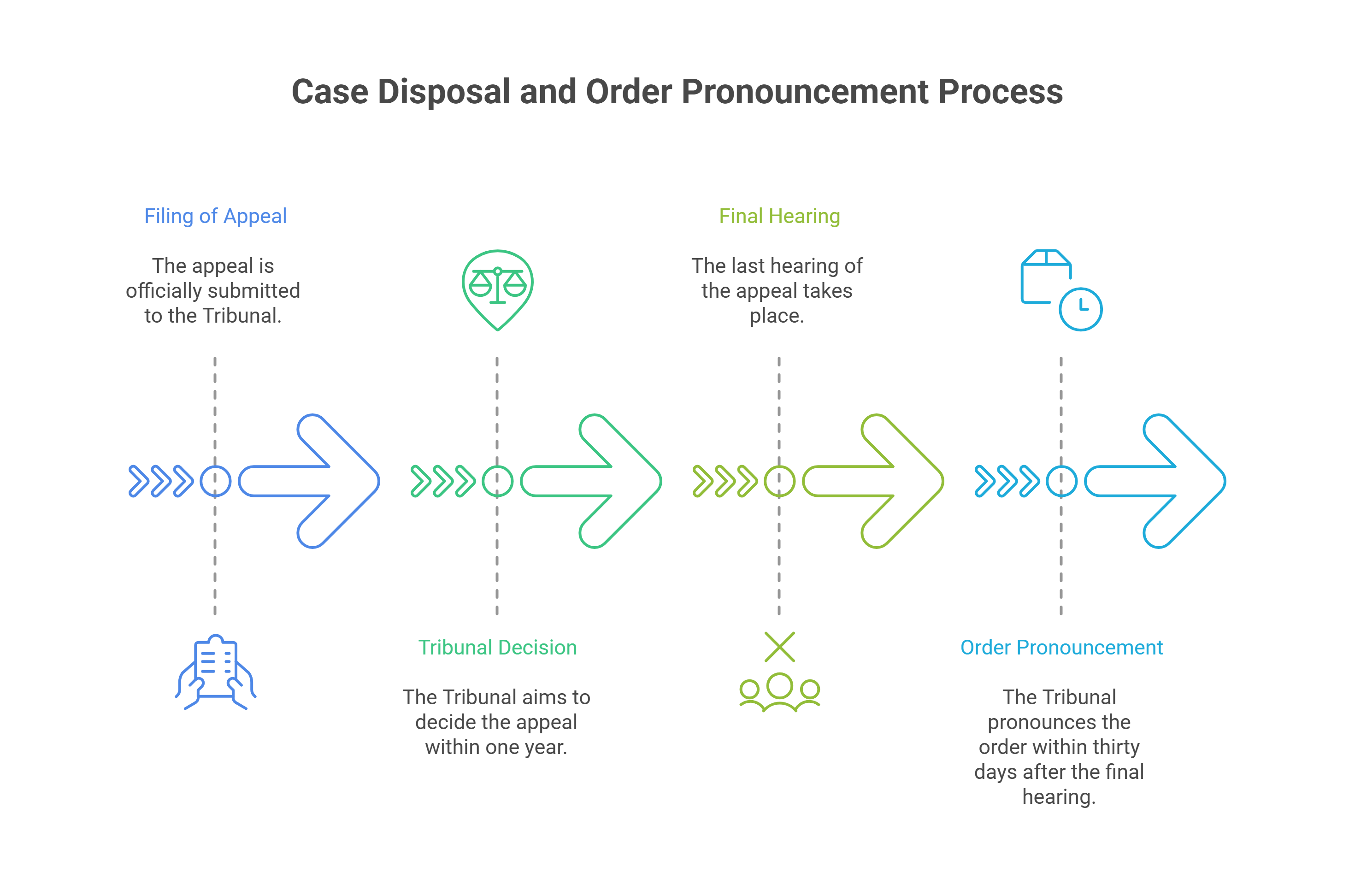

• Disposal of Cases and Pronouncement of Orders (Chapter XIII):

◦ The CGST Act encourages the Tribunal to decide appeals, as far as possible, within one year from the date of filing.

◦ The Appellate Tribunal shall make and pronounce an order either at once or as soon as practicable, but not later than thirty days from the final hearing, excluding vacations or holidays.

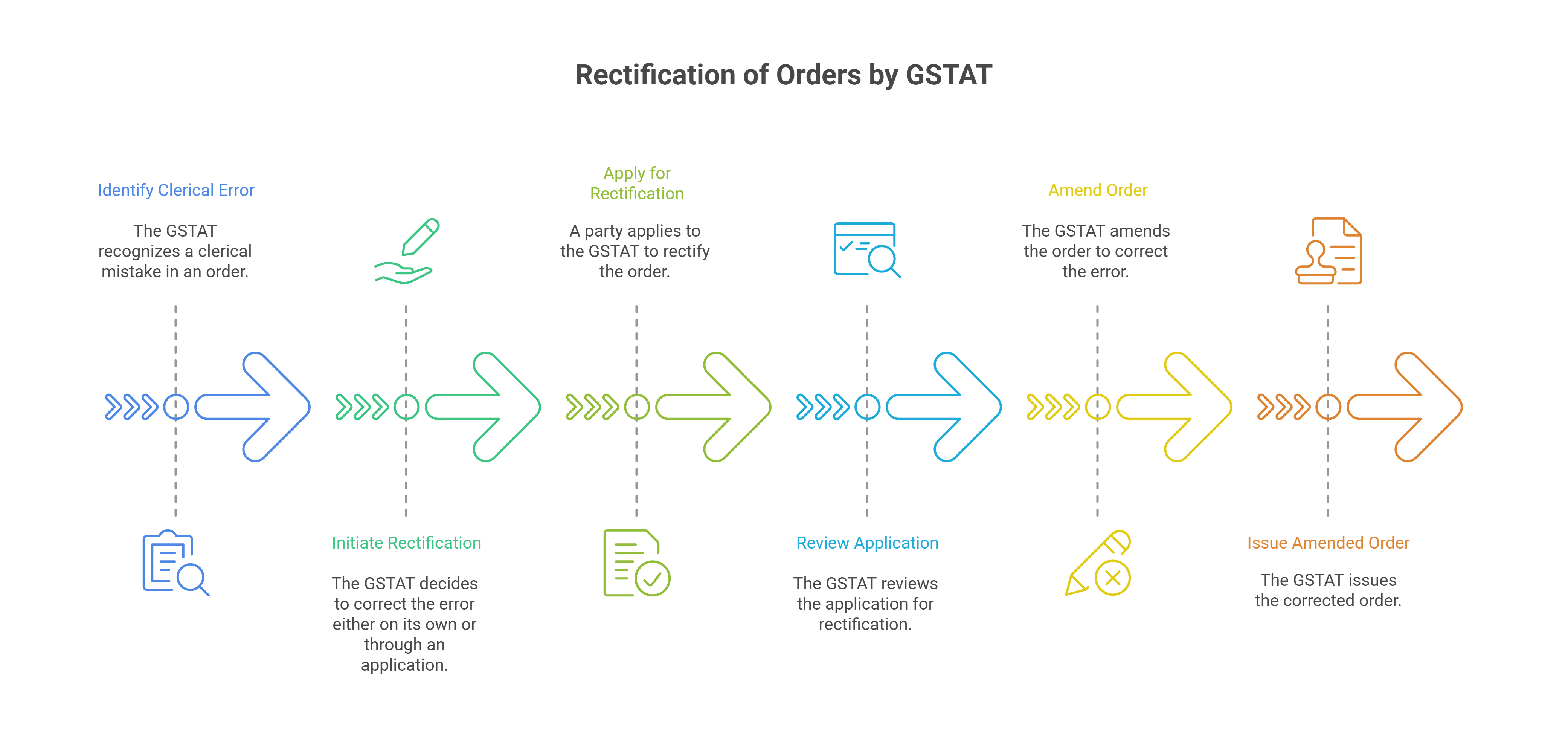

• Rectification of Orders by the Tribunal:

◦ The GSTAT can amend its own orders to rectify any clerical mistakes or errors apparent on the face of the record. This can be done suo motu or upon application by any party, within three months from the date of the original order.

• General Power to Amend Proceedings:

◦ The Appellate Tribunal may amend any defect or error in any proceeding before it within a period of thirty days from the date of completion of pleadings, on such terms as it deems fit.

• Continuance of Proceedings (Death or Insolvency of a Party):

◦ An application for the continuance of proceedings in case of death, insolvency, or winding up of a party must be made within sixty days of the occurrence of the event. The Appellate Tribunal may extend this 60-day period if it is satisfied that the applicant was prevented by sufficient cause.

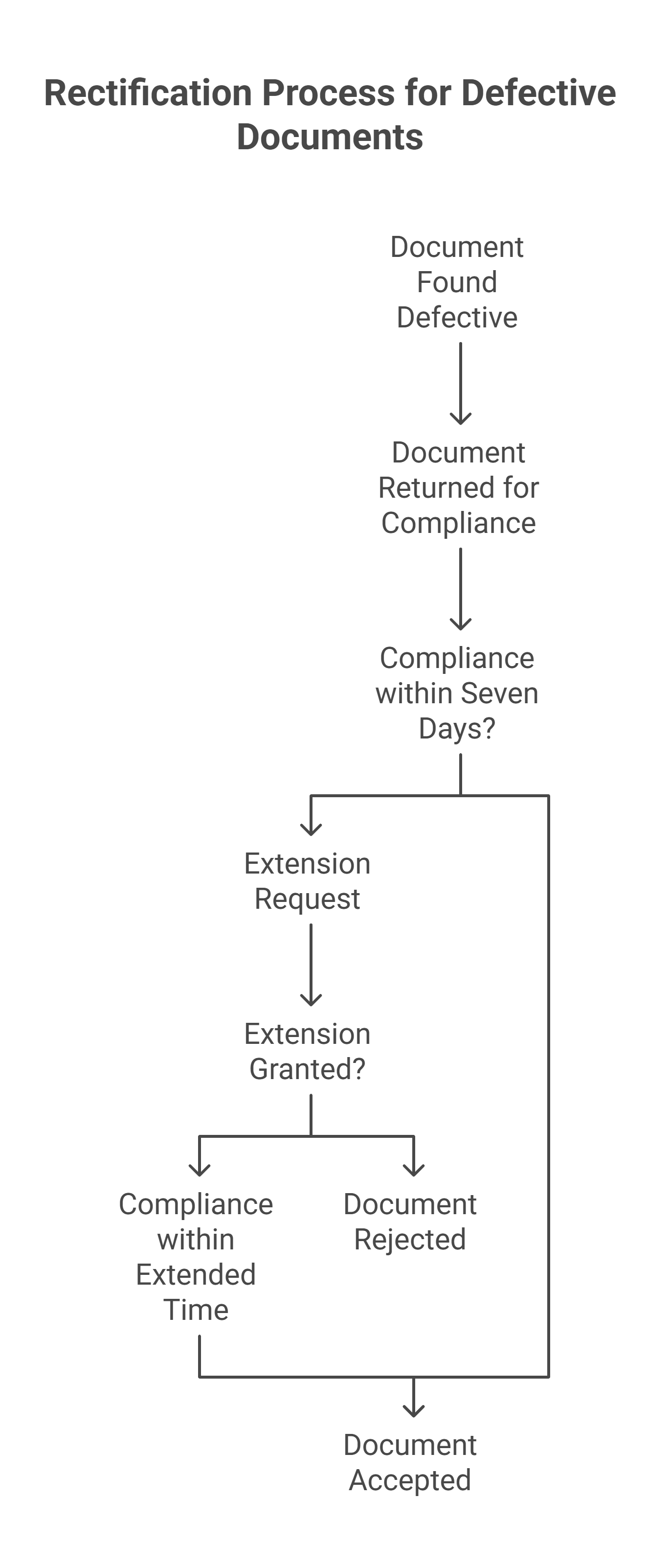

• Rectification of Defective Documents (Scrutiny):

◦ If an appeal, application, or other document is found defective upon scrutiny, it shall be returned for compliance. The party has seven working days from the date of return to rectify the defect. The Registrar may extend this time for compliance, in any case not exceeding thirty days from the date of filing.

• Listing of Urgent Matters (Cause List - Chapter IV):

◦ Any urgent matter filed before 12:00 noon shall be listed before the Appellate Tribunal on the following working day, provided it is complete in all respects.

◦ In exceptional cases, matters may be received after 12:00 noon but before 3:00 p.m. for listing on the following day, with the specific permission of the Appellate Tribunal or President.

The Goods and Services Tax Appellate Tribunal (GSTAT) (Procedure) Rules, 2025, along with the Central Goods and Services Tax (CGST) Act, 2017, outline various timelines for the filing of appeals, replies, rejoinders, and other applications, aiming to streamline the GST dispute resolution process.

• Filing of Appeals (Institution of Appeals - Chapter III):

◦ For Taxpayers: An appeal to the GSTAT must generally be filed within three months from the date the order is communicated to the person preferring the appeal.

◦ For the Department: The Commissioner (or an authorised officer) may apply to the GSTAT within six months from the date the order has been passed for determination of specified points.

◦ Start Date of Limitation Period: The three-month/six-month period for filing appeals shall be considered to start from the later of (A) the date of communication of the order, or (B) the date on which the President or the State President of the Appellate Tribunal, after its constitution, enters office. This provision addresses cases where the Tribunal was not yet functional.

• Condonation of Delay:

◦ The GSTAT may admit an appeal or permit the filing of a memorandum of cross-objections beyond the initial prescribed period if it is satisfied that there was sufficient cause for not presenting it within that period. For appeals, this additional period is three months, and for cross-objections, it is forty-five days.

• Filing of Cross-Objections:

◦ Upon receiving notice that an appeal has been preferred, the party against whom the appeal has been preferred may file a memorandum of cross-objections within forty-five days of the receipt of notice.

◦ The Tribunal may permit the filing of cross-objections within an additional forty-five days after the expiry of the initial period if sufficient cause is shown.

• Filing of Reply and Rejoinder (Chapter III):

◦ Respondent's Reply: Each respondent may file their reply to the petition or application and copies of documents with the Registrar within one month of receipt. A copy of the reply must be forthwith served on the applicant by the respondent.

◦ Appellant's Rejoinder: If the respondent states additional facts, the Bench may allow the petitioner to file a rejoinder within one month or within such time as specified or extended by the Bench, with an advance copy served upon the respondent.

• Filing of Interlocutory Applications:

◦ An application for rectification of an order must be made online (using GSTAT FORM-01) within one month from the date of the final order.

◦ Other interlocutory applications, such as for stay, condonation of delay (as above), or early hearing, must use GSTAT FORM-01 and be supported by an affidavit.

◦ The Appellate Tribunal has the power to extend any time limit fixed by the rules or by its own order, even if the application for extension is made after the original period has expired, if the justice of the case requires it.

• Disposal of Cases and Pronouncement of Orders (Chapter XIII):

◦ The CGST Act encourages the Tribunal to decide appeals, as far as possible, within one year from the date of filing.

◦ The Appellate Tribunal shall make and pronounce an order either at once or as soon as practicable, but not later than thirty days from the final hearing, excluding vacations or holidays.

• Rectification of Orders by the Tribunal:

◦ The GSTAT can amend its own orders to rectify any clerical mistakes or errors apparent on the face of the record. This can be done suo motu or upon application by any party, within three months from the date of the original order.

• General Power to Amend Proceedings:

◦ The Appellate Tribunal may amend any defect or error in any proceeding before it within a period of thirty days from the date of completion of pleadings, on such terms as it deems fit.

• Continuance of Proceedings (Death or Insolvency of a Party):

◦ An application for the continuance of proceedings in case of death, insolvency, or winding up of a party must be made within sixty days of the occurrence of the event. The Appellate Tribunal may extend this 60-day period if it is satisfied that the applicant was prevented by sufficient cause.

• Rectification of Defective Documents (Scrutiny):

◦ If an appeal, application, or other document is found defective upon scrutiny, it shall be returned for compliance. The party has seven working days from the date of return to rectify the defect. The Registrar may extend this time for compliance, in any case not exceeding thirty days from the date of filing.

• Listing of Urgent Matters (Cause List - Chapter IV):

◦ Any urgent matter filed before 12:00 noon shall be listed before the Appellate Tribunal on the following working day, provided it is complete in all respects.

◦ In exceptional cases, matters may be received after 12:00 noon but before 3:00 p.m. for listing on the following day, with the specific permission of the Appellate Tribunal or President.

GST Bill Online | Check Invoice Number Online | E Invoicing Software | Dry Fruits Hsn Code | GST Maintenance Charges

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified