Navigating GST Disputes: The Role and Impact of the Goods and Services Tax Appellate Tribunal (GSTAT)

Goods and Services Tax Appellate Tribunal (GSTAT)

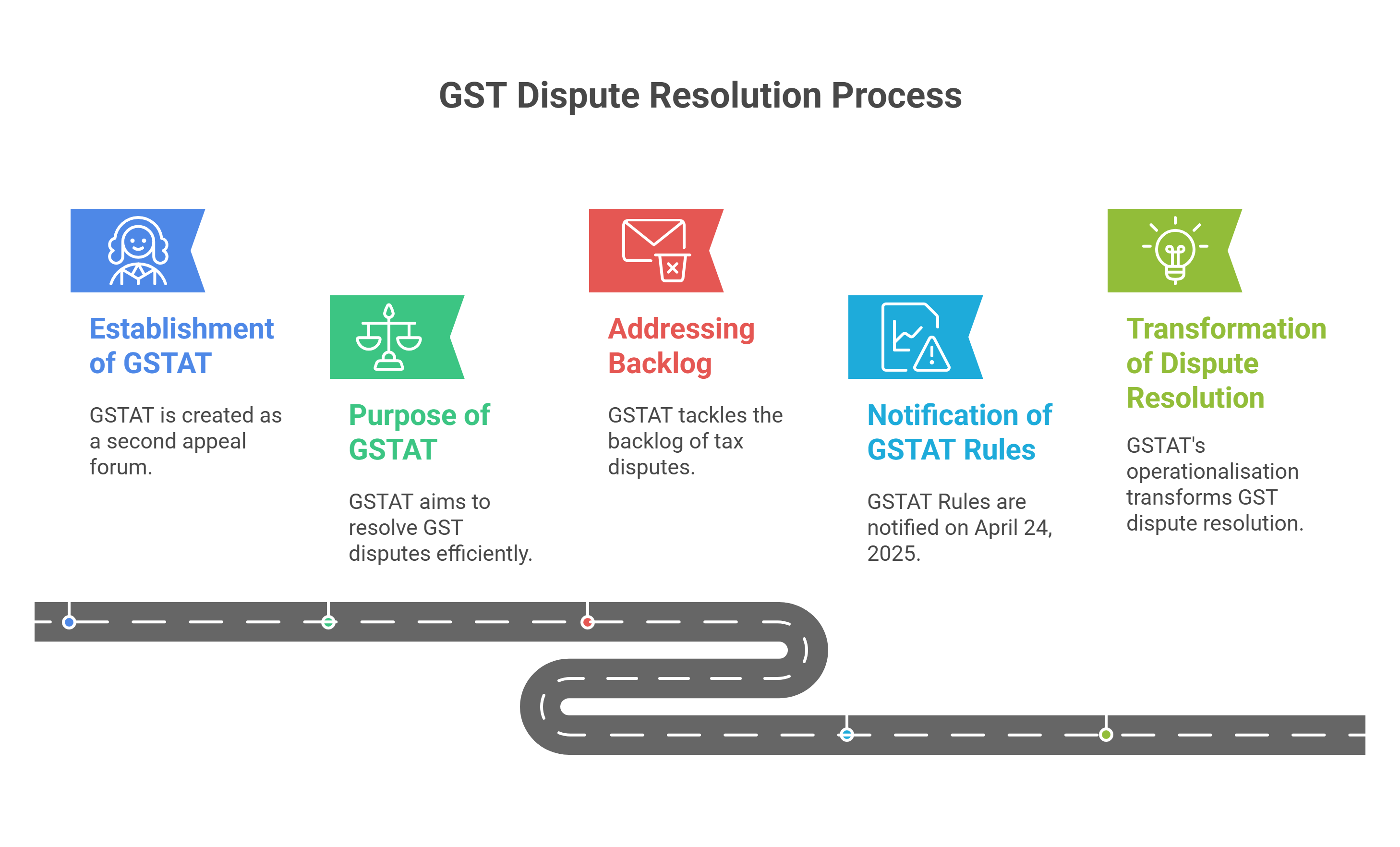

The Goods and Services Tax Appellate Tribunal (GSTAT) is established as a critical second forum for appeal within India's GST dispute resolution hierarchy. Its primary purpose is to provide a specialised, efficient, and uniform mechanism for resolving GST matters. This includes addressing the significant backlog of tax disputes that have burdened High Courts through writ petitions since the inception of GST in 2017.

The operationalisation of GSTAT, through the Goods and Services Tax Appellate Tribunal (Procedure) Rules, 2025 (GSTAT Rules), notified on 24 April 2025, represents a pivotal transformation for GST dispute resolution.

Reasons for GST Litigation Leading to GSTAT

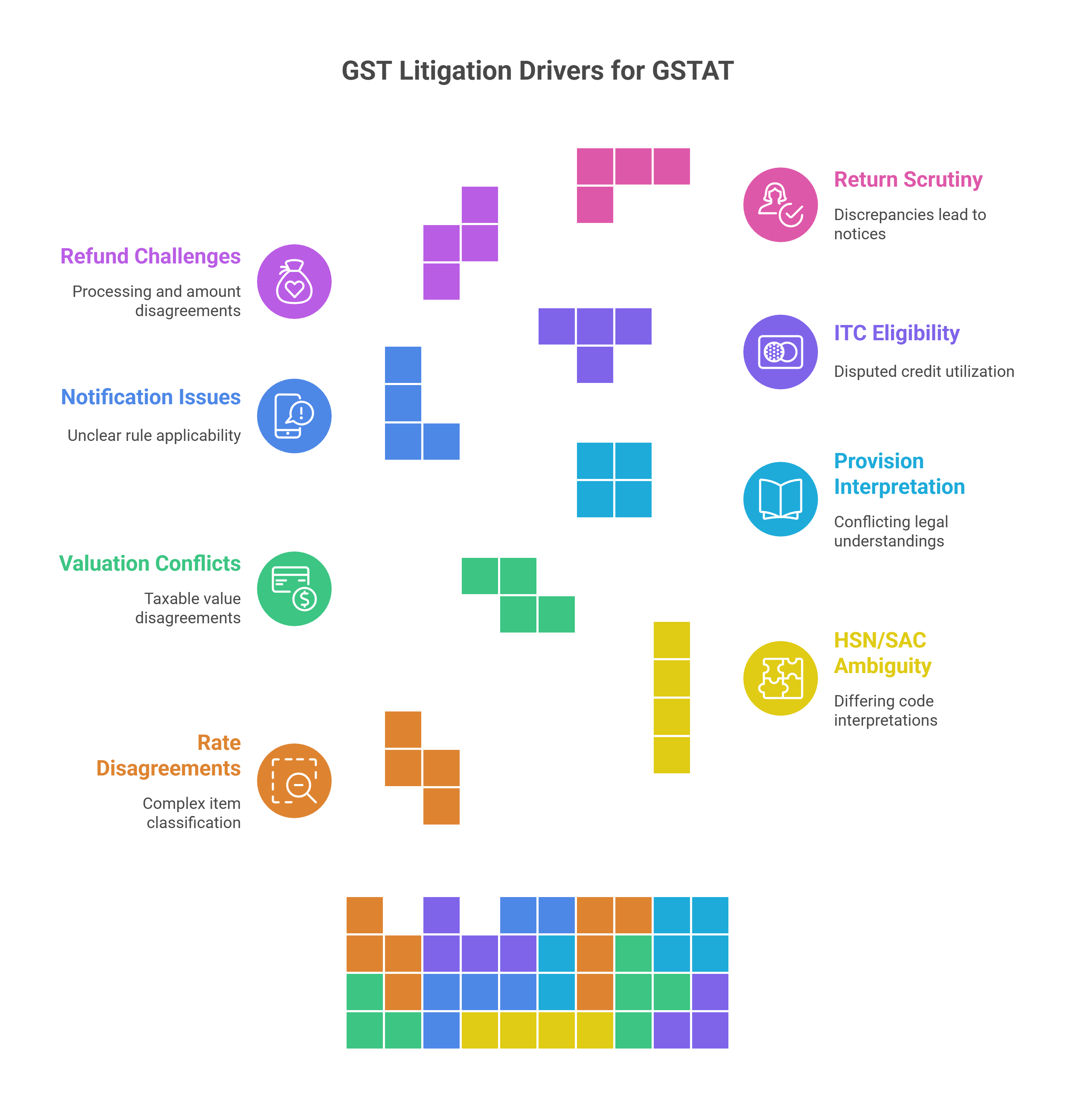

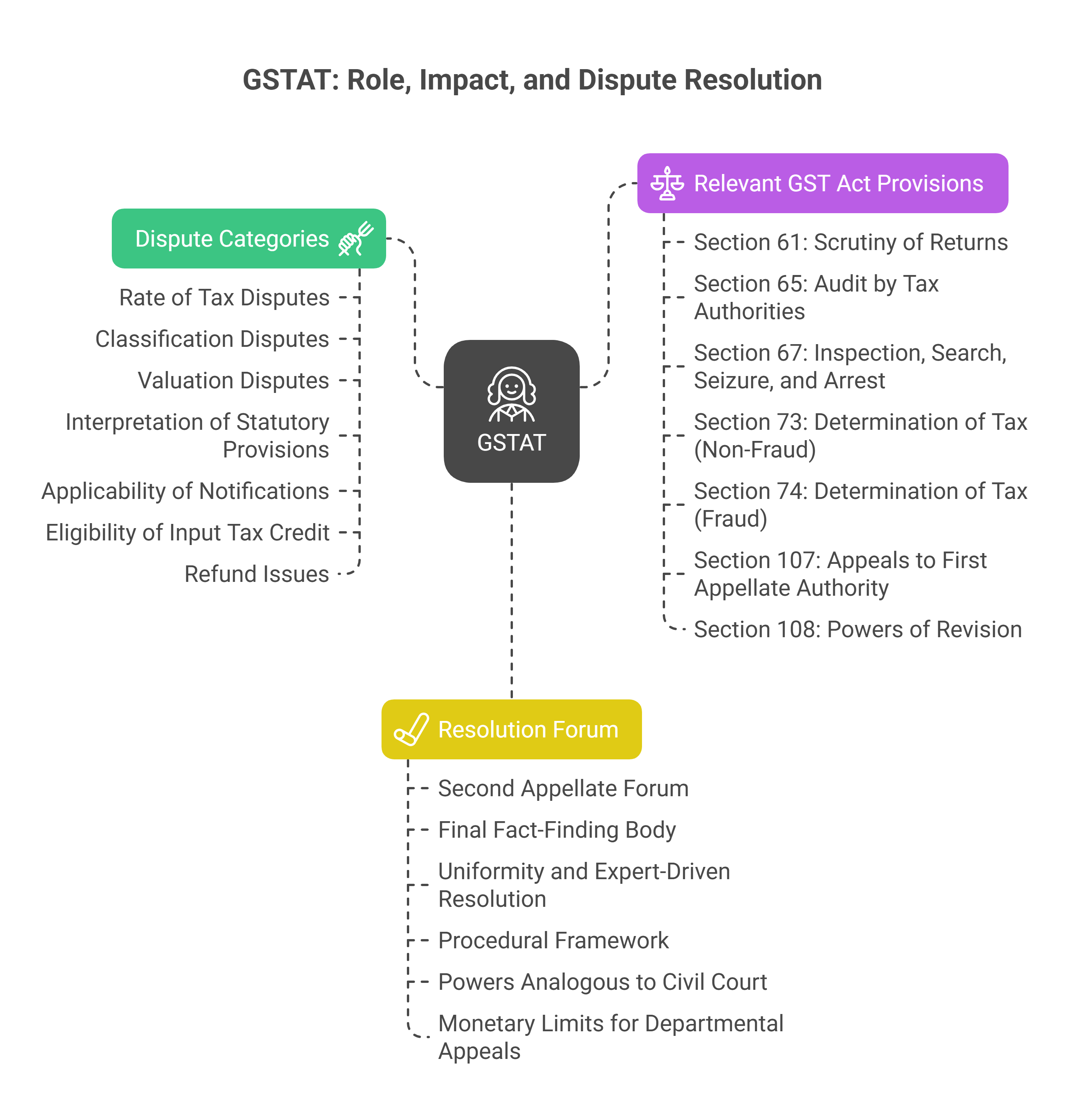

The sources identify several common categories of disputes that lead to litigation under the GST regime and are thus intended to be resolved by the GSTAT:

-

Rate of Tax Disputes Disagreements over the applicable GST rate for specific goods or services are a common cause of contention, often stemming from the complexity of classifying items under different schedules.

-

Classification (HSN/SAC) Disputes Determining the correct Harmonised System of Nomenclature (HSN) code for goods or the Service Accounting Code (SAC) for services is crucial, and ambiguities or differing interpretations can trigger litigation.

-

Valuation Disputes Disputes concerning the taxable value of goods or services, especially in related-party transactions or cases involving discounts and incentives, frequently lead to legal challenges.

-

Interpretation of Statutory Provisions The GST law is complex, and differing understandings of its various sections and rules between taxpayers and tax authorities often result in litigation.

-

Applicability of Notifications Disputes can arise regarding the applicability or interpretation of notifications issued by the government to clarify or amend GST rules and rates, including exemption notifications.

-

Eligibility of Input Tax Credit (ITC) Disputes While not explicitly listed as a standalone category, the sources broadly state that "every topic under GST can potentially become a subject of litigation". Therefore, disputes concerning eligibility, distribution (Input Services Distribution Disputes), or utilisation of ITC would fall within GSTAT's intended jurisdiction once they have been considered at the first appellate level. ITC is also explicitly mentioned in the context of anti-profiteering cases.

-

Refund Issues Disagreements or challenges concerning the eligibility, processing, or amount of GST refunds are explicitly mentioned as a reason for litigation. Monetary limits for departmental appeals for "erroneous refund" cases are also set for GSTAT, High Court, and Supreme Court.

Relevant GST Act Provisions Leading to Disputes Disputes often originate from actions or orders under various sections of the CGST Act, which then progress through the appellate hierarchy to the GSTAT:

-

Section 61: Scrutiny of Returns Discrepancies identified during the scrutiny of returns can lead to demand notices and subsequent litigation.

-

Section 65: Audit by Tax Authorities Findings from audits conducted by tax authorities can initiate disputes and litigation.

-

Section 66: Special Audit Directives for special audits by chartered or cost accountants can trigger disputes based on their findings.

-

Section 67: Inspection, Search, Seizure, and Arrest Enforcement actions under this section are explicitly identified as highly likely to lead to disputes.

-

Section 70: Summons The issuance of summons and subsequent proceedings can lay the groundwork for disputes.

-

Section 73: Determination of Tax (Non-Fraud) & Section 74: Determination of Tax (Fraud) These sections deal with the determination of tax liability, and orders issued under them (especially Section 74, involving fraud, wilful misstatement, or suppression) are direct instigators of disputes and penalties.

-

Section 76: Tax Collected but not Paid to Government Failure to remit collected tax to the government can lead to stringent actions and disputes under this section.

-

Section 78: Recovery Proceedings Initiation of recovery proceedings can become a point of dispute, particularly if the underlying tax demand is contested.

-

Section 107: Appeals to First Appellate Authority This section constitutes the first appellate authority. Orders passed by this authority are directly appealable to the GSTAT.

-

Section 108: Powers of Revision This section grants revisional powers to higher tax authorities. Orders passed by a revisional authority are also directly appealable to the GSTAT.

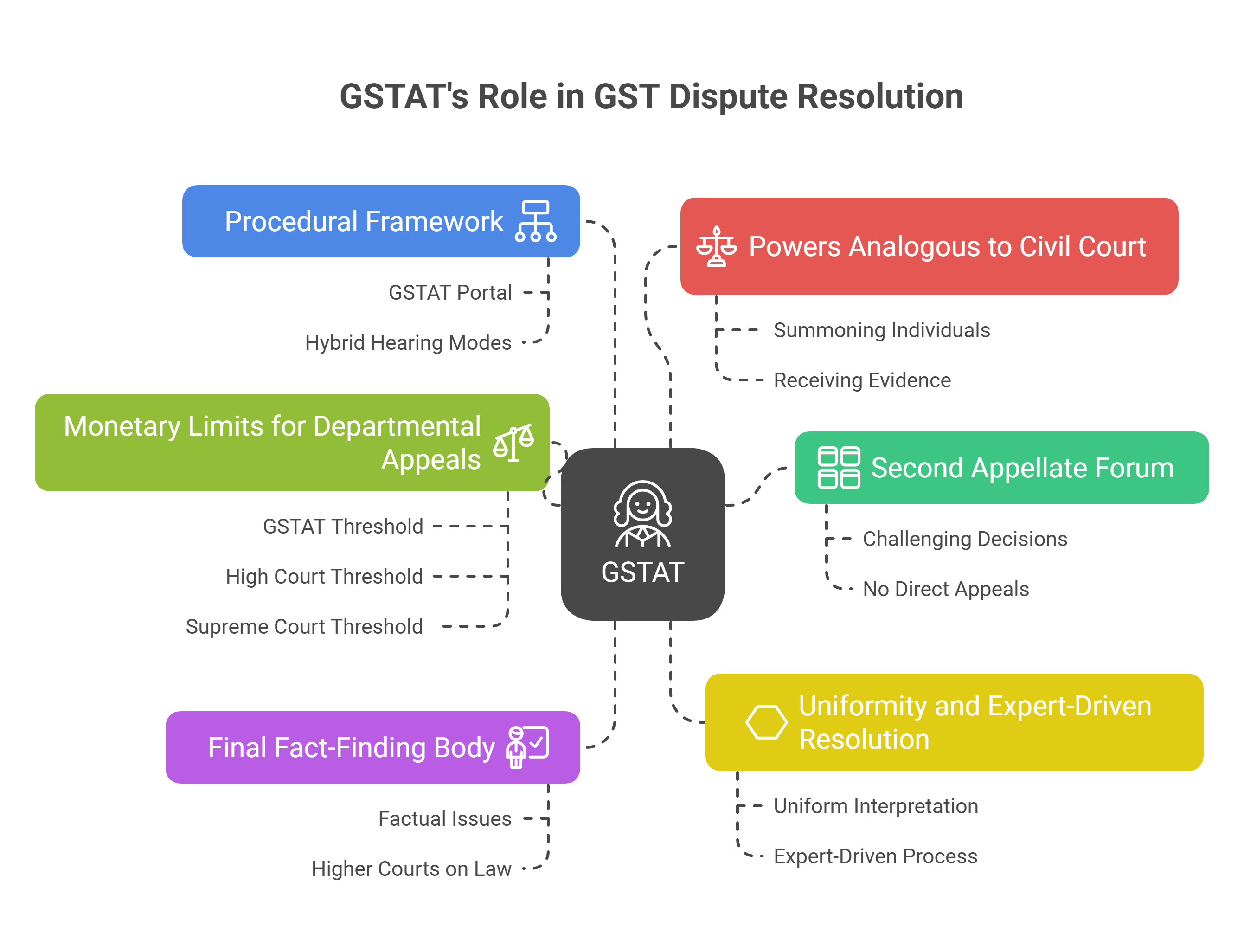

GSTAT as the Resolution Forum for these Disputes

The GSTAT is specifically designed to address these disputes:

-

Second Appellate Forum: It functions as the designated second forum for appeal under the GST laws, providing a structured pathway for challenging decisions of the first appellate or revisional authorities. Direct appeals against original adjudication orders (e.g., under Section 73/74) are explicitly not permitted at the GSTAT stage.

-

Final Fact-Finding Body: The GSTAT is envisioned as the final fact-finding body in the GST appeal process. This means that factual issues are generally settled at this stage, with higher courts focusing on substantial questions of law.

-

Uniformity and Expert-Driven Resolution: GSTAT is conceptualised as the first common forum for dispute resolution involving both the Centre and the States, aiming to foster uniformity in the interpretation and application of GST law across the country. Its specialised nature is intended to provide a quicker, more economical, and expert-driven resolution process compared to litigation in generalist courts. The Principal Bench also has exclusive jurisdiction over "place of supply" issues and "anti-profiteering matters" (Section 171(2)).

-

Procedural Framework: The GSTAT (Procedure) Rules, 2025, notified on 24 April 2025, provide a comprehensive procedural framework for the functioning of the Tribunal. These rules, structured into fifteen chapters and 124 provisions, govern the entire lifecycle of an appeal, including filing, hearings, and pronouncement of orders. Key innovations include mandatory e-filing through the GSTAT Portal and hybrid hearing modes.

-

Powers Analogous to Civil Court: The GSTAT is not strictly bound by the Civil Procedure Code (CPC) but is guided by principles of natural justice. However, it possesses powers similar to a civil court under CPC for specific functions like summoning individuals and documents, receiving evidence on affidavits, and issuing commissions.

-

Monetary Limits for Departmental Appeals: To curb excessive litigation, the GST Council recommended specific monetary thresholds for departmental appeals: ₹20 lakh for appeals to GSTAT, ₹1 crore for High Courts, and ₹2 crore for the Supreme Court.

Impact of GSTAT's Past Absence For over seven years since GST's inception in 2017, the absence of a functional GSTAT created a "critical lacuna" in the dispute resolution mechanism. This forced taxpayers to seek recourse against first appellate orders through writ petitions in High Courts, a remedy intended for a later stage, leading to a significant backlog of unresolved tax disputes and an "undue burden" on the High Courts.

Conclusion

The operational GSTAT, guided by its new procedural rules, is poised to become a cornerstone of India's GST dispute resolution landscape. It aims to efficiently resolve a wide array of disputes originating from various GST Act provisions and interpretations, thereby fostering uniformity, reducing litigation, and alleviating the burden on higher courts.

Need for GST In India | GST Invoice Serial Number Rules | Powers of GST Officers | Dry Fruits GST Rate | Maintenance Charges GST

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified