Distinctions Between Section 70 Summons and Personal Hearings under GST

The distinction between a Summons under Section 70 and a Personal Hearing (specifically under Section 75(4)) lies primarily in their purpose, the stage of proceedings at which they occur, the rights of the individual involved, and the legal consequences of non-compliance.

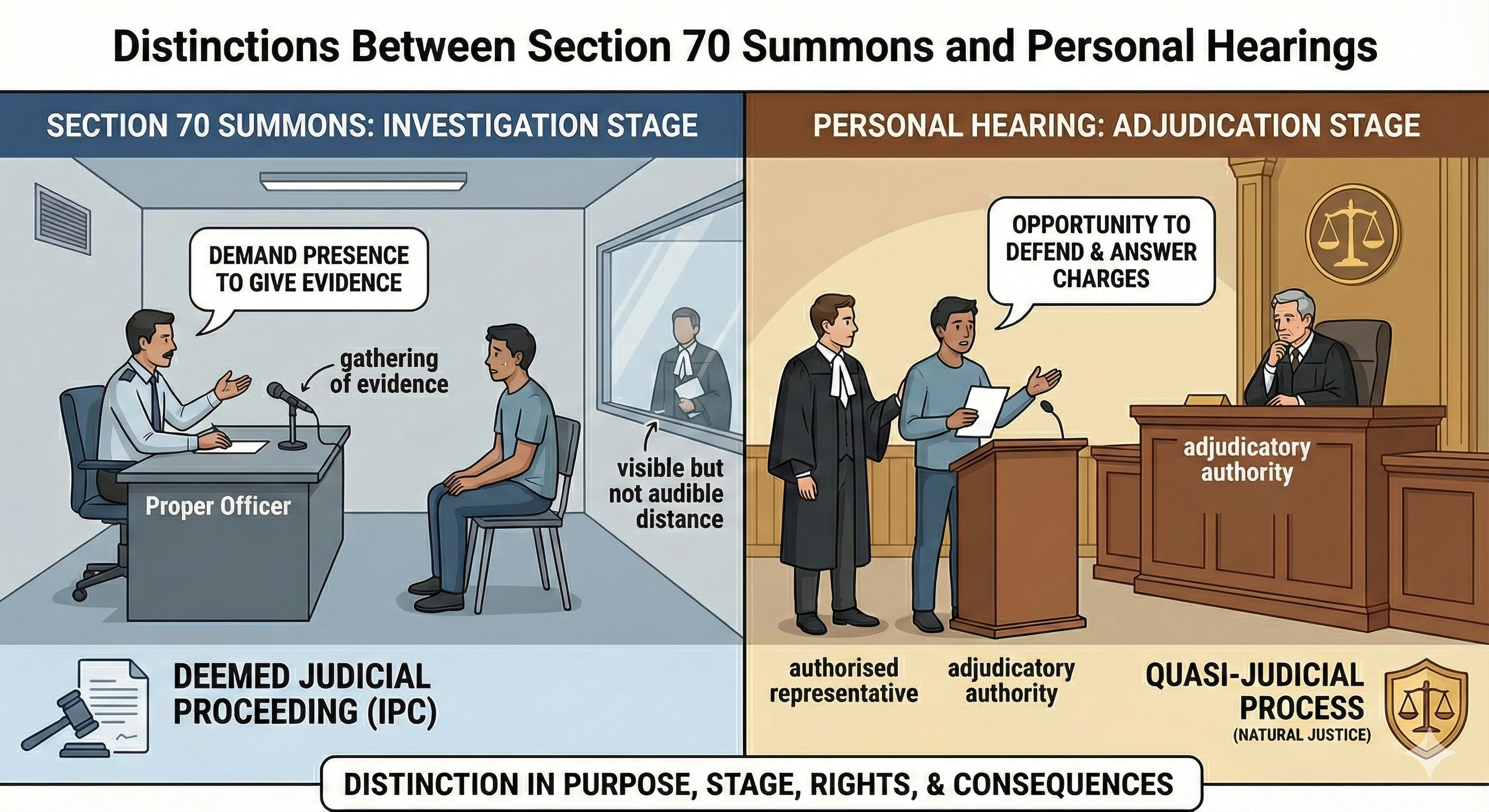

1. Fundamental Purpose and Stage

• Section 70 Summons (Investigation/Inquiry Stage):

◦ Purpose: The primary purpose of a summons is to gather evidence. The Proper Officer has the power to summon any person whose attendance is considered necessary either to give evidence or to produce a document or any other thing in any inquiry.

◦ Nature: It is an investigative tool used to obtain information or record statements to find out about tax evasion. The term "summon" essentially means to "demand the presence of" or "call upon a person to appear".

• Personal Hearing (Adjudication Stage):

◦ Purpose: The purpose of a personal hearing is to provide the taxpayer a reasonable opportunity to defend themselves and answer charges before a demand is confirmed or a penalty is imposed. It enables the adjudicatory authority to observe the witness's demeanour and resolve doubts during arguments.

◦ Nature: It is a facet of the Principles of Natural Justice (Audi Alteram Partem), ensuring no one is adjudged guilty without being heard.

2. Legal Status of the Proceedings

• Summons: Every inquiry pursuant to a summons under Section 70 is deemed to be a "judicial proceeding" within the meaning of Section 193 and Section 228 of the Indian Penal Code. This means giving false evidence is a punishable offence.

• Personal Hearing: This is part of the "Quasi-Judicial" adjudication process. While similar to judicial proceedings, they deal with facts and decisions based on law (e.g., assessing tax liability).

3. Statutory Mandate and Rights

• Summons:

◦ Attendance: The person summoned is bound to attend (unless there is a lawful excuse) and state the truth.

◦ Right to Lawyer: A person called for interrogation under summons generally has no right to have a lawyer present during questioning, as they are not equivalent to an accused in a criminal case. However, courts have permitted advocates to remain present at a "visible but not audible distance" during recording of statements to prevent coercion,,.

◦ Right of Silence: It is not mandatory for a person to make a statement appearing for the summons; one has a right of silence.

• Personal Hearing:

◦ Mandatory Provision: Under Section 75(4), granting an opportunity of hearing is mandatory where a request is received in writing OR where any adverse decision is contemplated against the person.

◦ Consequence of Denial: An order passed without providing a personal hearing, especially when an adverse decision is taken, is invalid and liable to be set aside by courts.

◦ Representation: The taxpayer can be represented by an authorised representative (e.g., CA, Advocate, Employee).

4. Adjournments and Non-Compliance

• Summons:

◦ Non-Compliance: Failure to attend can lead to prosecution under Section 174 of the IPC (non-attendance in obedience to an order from a public servant) or a penalty of up to ₹25,000 under Section 122(3)(d),.

◦ Repeated Summons: If a person does not join investigations, generally three summons are issued at reasonable intervals before filing a complaint with the Magistrate.

• Personal Hearing:

◦ Adjournments: The law restricts adjournments explicitly. No adjournment shall be granted more than three times to a party during the hearing of an appeal or adjudication.

◦ Non-Compliance: If the taxpayer fails to attend the personal hearing or file a reply, the officer may proceed to pass an ex-parte order (though courts have often frowned upon ex-parte orders passed in haste),.

Summary Comparison Table

| Feature | Section 70 Summons | Personal Hearing (Sec 75(4)) |

| Stage | Investigation / Inquiry | Adjudication / Defense |

| Legal Status | Deemed "Judicial Proceeding" | "Quasi-Judicial Proceeding" |

| Primary Goal | Gather evidence / Record Statement | Defend against allegations / SCN |

| Legal Counsel | Generally restricted (visible distance only) | Allowed (Authorized Representative) |

| Adjournments | Multiple allowed (guideline suggests 3) | Max 3 times to a party, |

| Non-compliance | Prosecution (IPC 174) / Penalty | Ex-parte Adjudication Order |

Analogy: A Section 70 Summon is like being called to the police station to answer questions about a crime where you might be a witness or suspect (evidence collection). A Personal Hearing is like standing before a judge or a disciplinary committee to defend yourself before they decide your punishment (adjudication).

Powers of GST officers | GST anti evasion department powers | ADT-01 GST | DRC-01 format | Need for GST in India

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified