GST Rules: Registration, Invoices, Returns & ITC | Operational Aspects

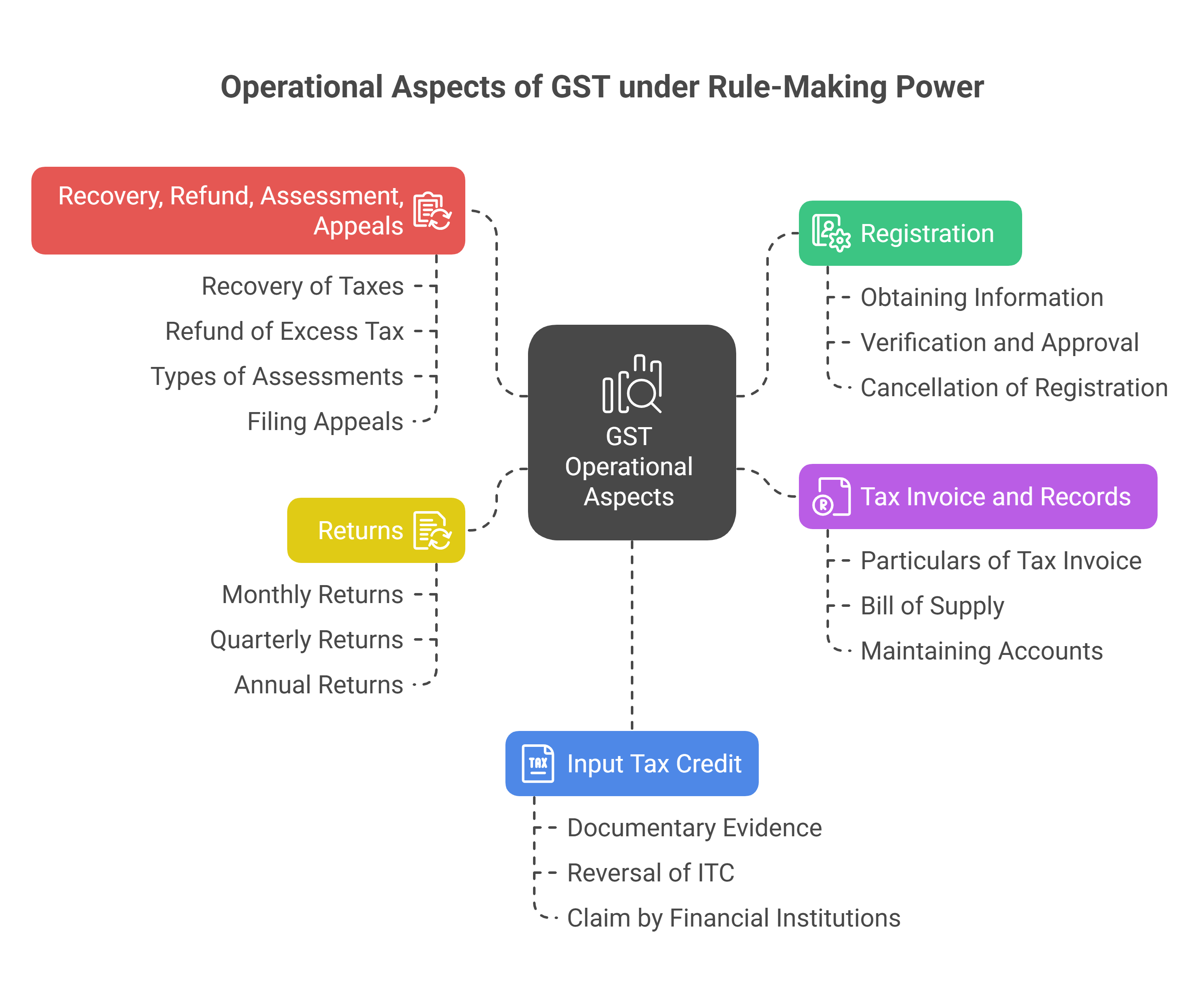

This document outlines the operational aspects of Goods and Services Tax (GST) that are governed by rule-making power. These aspects include registration, tax invoices and records, returns, input tax credit, and procedures related to recovery, refund, assessment, and appeals. The rules provide detailed procedures and guidelines for the effective implementation of the GST law.

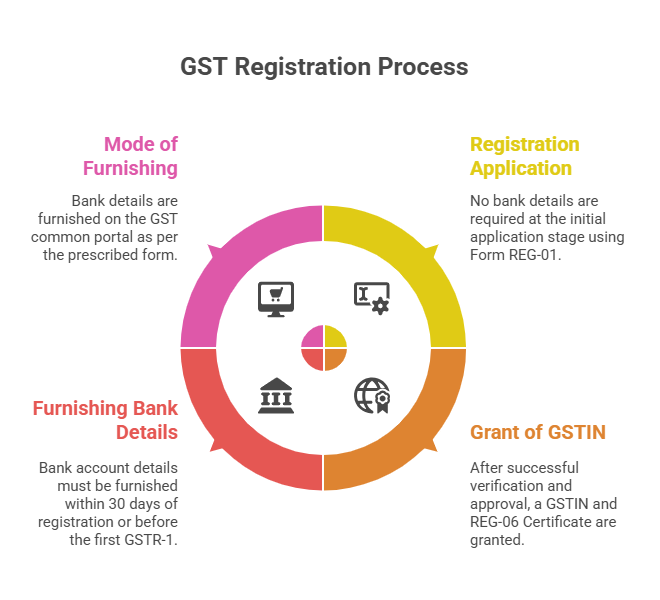

Registration (Rules 1–27)

The registration process under GST is governed by Rules 1 to 27. These rules specify the procedures for obtaining registration, the documents required, and the conditions for cancellation or suspension of registration.

-

Rule 1: Deals with the manner of obtaining information and documents for processing the application for registration.

-

Rule 8: Specifies the procedure for verification of application and approval.

-

Rule 9: Provides for the issue of registration certificate.

-

Rule 10: Outlines the procedure for amendment of registration.

-

Rule 12: Covers the grant of registration to persons required to deduct tax at source or collect tax at source.

-

Rule 17: Deals with cancellation of registration.

-

Rule 26: Addresses the physical verification of business premises in certain cases.

These rules ensure that only eligible businesses are registered under GST, and they provide a framework for maintaining an accurate and up-to-date registry of taxpayers.

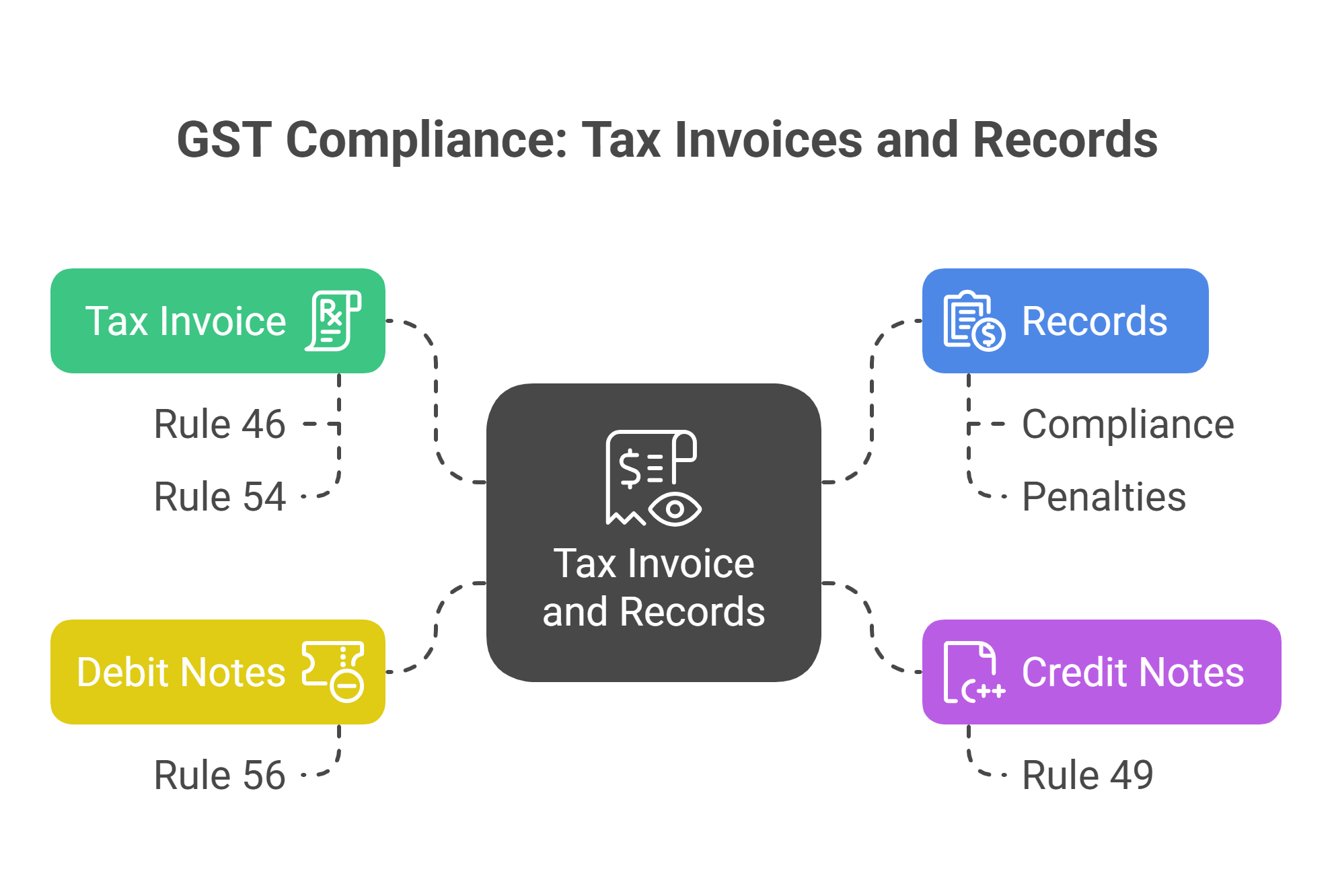

Tax Invoice and Records (Rules 46–56)

Rules 46 to 56 prescribe the requirements for issuing tax invoices, credit notes, debit notes, and maintaining records. These rules are crucial for ensuring transparency and accountability in GST transactions.

-

Rule 46: Specifies the particulars of a tax invoice.

-

Rule 49: Deals with the bill of supply.

-

Rule 54: Covers the tax invoice in case of supply of services.

-

Rule 56: Prescribes the manner of maintaining accounts and records.

Compliance with these rules is essential for claiming input tax credit and for avoiding penalties for non-compliance.

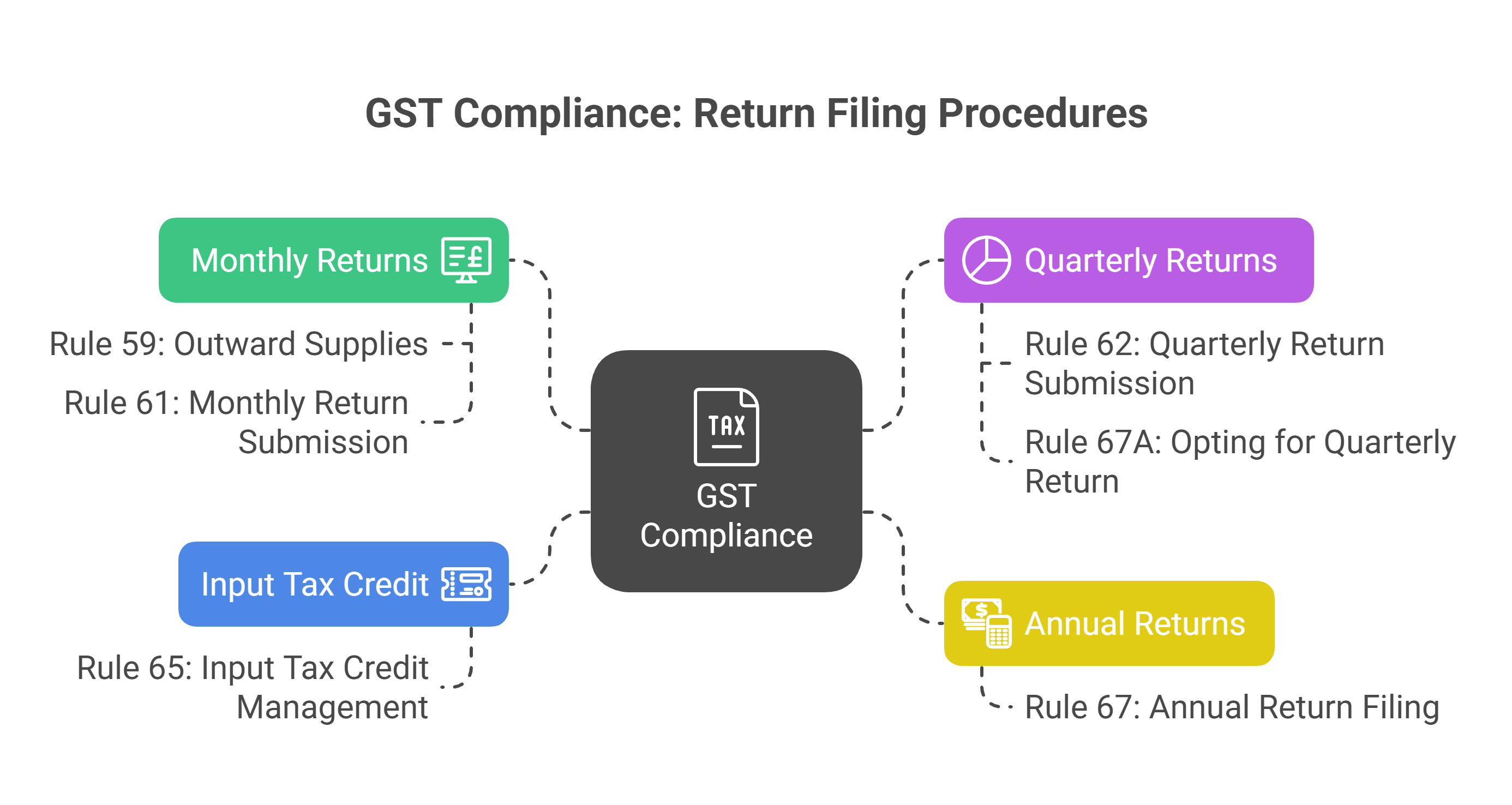

Returns (Rules 59–67A)

The filing of returns is a critical aspect of GST compliance. Rules 59 to 67A outline the procedures for filing various types of returns, including monthly, quarterly, and annual returns.

-

Rule 59: Specifies the form and manner of furnishing details of outward supplies.

-

Rule 61: Deals with the form and manner of submission of monthly return.

-

Rule 62: Covers the form and manner of submission of quarterly return.

-

Rule 65: Addresses the matching, reversal, and reclaim of input tax credit.

-

Rule 67: Provides for the procedure for filing annual return.

-

Rule 67A: Deals with the manner of opting for furnishing quarterly return.

These rules ensure that taxpayers accurately report their transactions and pay their taxes on time.

Input Tax Credit (Rules 36–45)

Input Tax Credit (ITC) is a fundamental feature of GST, allowing businesses to claim credit for the tax paid on their inputs. Rules 36 to 45 specify the conditions and procedures for availing ITC.

-

Rule 36: Specifies the documentary evidence required for claiming ITC.

-

Rule 37: Deals with the reversal of ITC in certain cases.

-

Rule 38: Covers the claim of credit by banking companies and financial institutions.

-

Rule 42: Prescribes the manner of determination of ITC in respect of inputs and input services and reversal thereof.

-

Rule 43: Deals with the manner of determination of ITC in respect of capital goods and reversal thereof.

These rules ensure that ITC is claimed legitimately and that there is no misuse of the credit mechanism.

Recovery, Refund, Assessment, Appeals, etc.

The GST rules also cover procedures related to recovery of taxes, refunds, assessment, and appeals. These rules provide a framework for resolving disputes and ensuring that taxpayers are treated fairly.

-

Recovery: The rules specify the procedures for recovering unpaid taxes, including attachment and sale of property.

-

Refund: The rules outline the conditions and procedures for claiming refunds of excess tax paid.

-

Assessment: The rules provide for various types of assessments, including self-assessment, provisional assessment, and scrutiny assessment.

-

Appeals: The rules specify the procedures for filing appeals against assessment orders and other decisions of tax authorities.

These rules ensure that the GST system is fair and transparent and that taxpayers have recourse to justice in case of disputes.

Conclusion

In conclusion, the rule-making power under GST is exercised to provide detailed procedures and guidelines for various operational aspects of the law. These rules are essential for the effective implementation of GST and for ensuring compliance by taxpayers.

GST Invoice Generator | Invoice Number Check | E Invoice Software | GST On Dry Fruits | GST On Maintenance Charges

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified