GST Refund for Unregistered Persons: A Guide to Cancelled Services

GST Refunds for Unregistered Persons: Cancelled Service Contracts

Section 54 of the Central Goods and Services Tax (CGST) Act outlines the legal and procedural aspects for claiming refunds of various amounts, including any excess tax, interest, or other amounts paid. An "unregistered person" is generally understood as an individual or entity not registered under section 25 of the Act and does not possess a Unique Identity Number (UIN).

Refunds for Unregistered Persons in Case of Cancelled Service Contracts

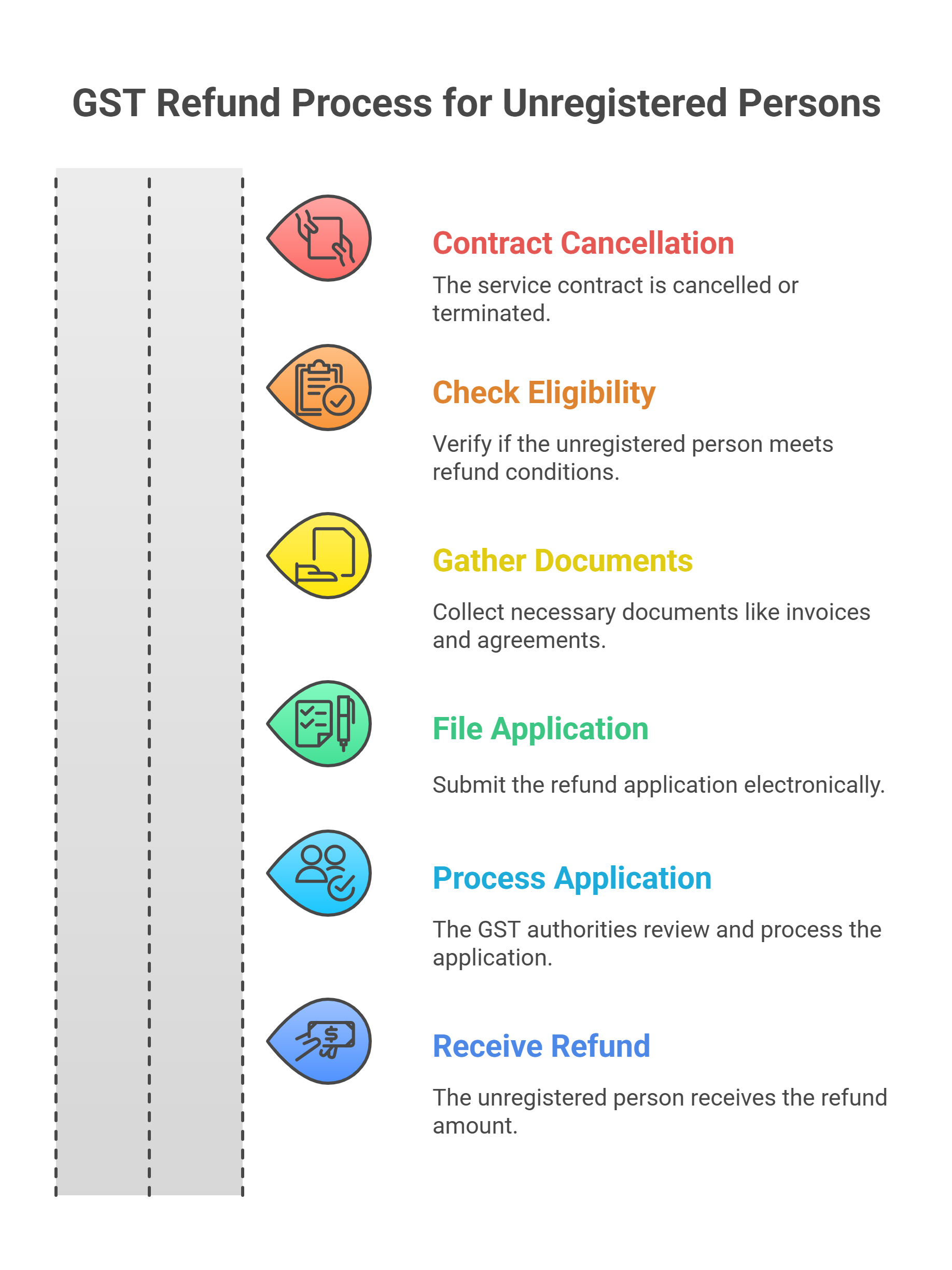

The Goods and Services Tax (GST) law specifically provides for refunds to unregistered persons in certain circumstances, particularly when a service contract has been cancelled or terminated.

Eligibility and Conditions:

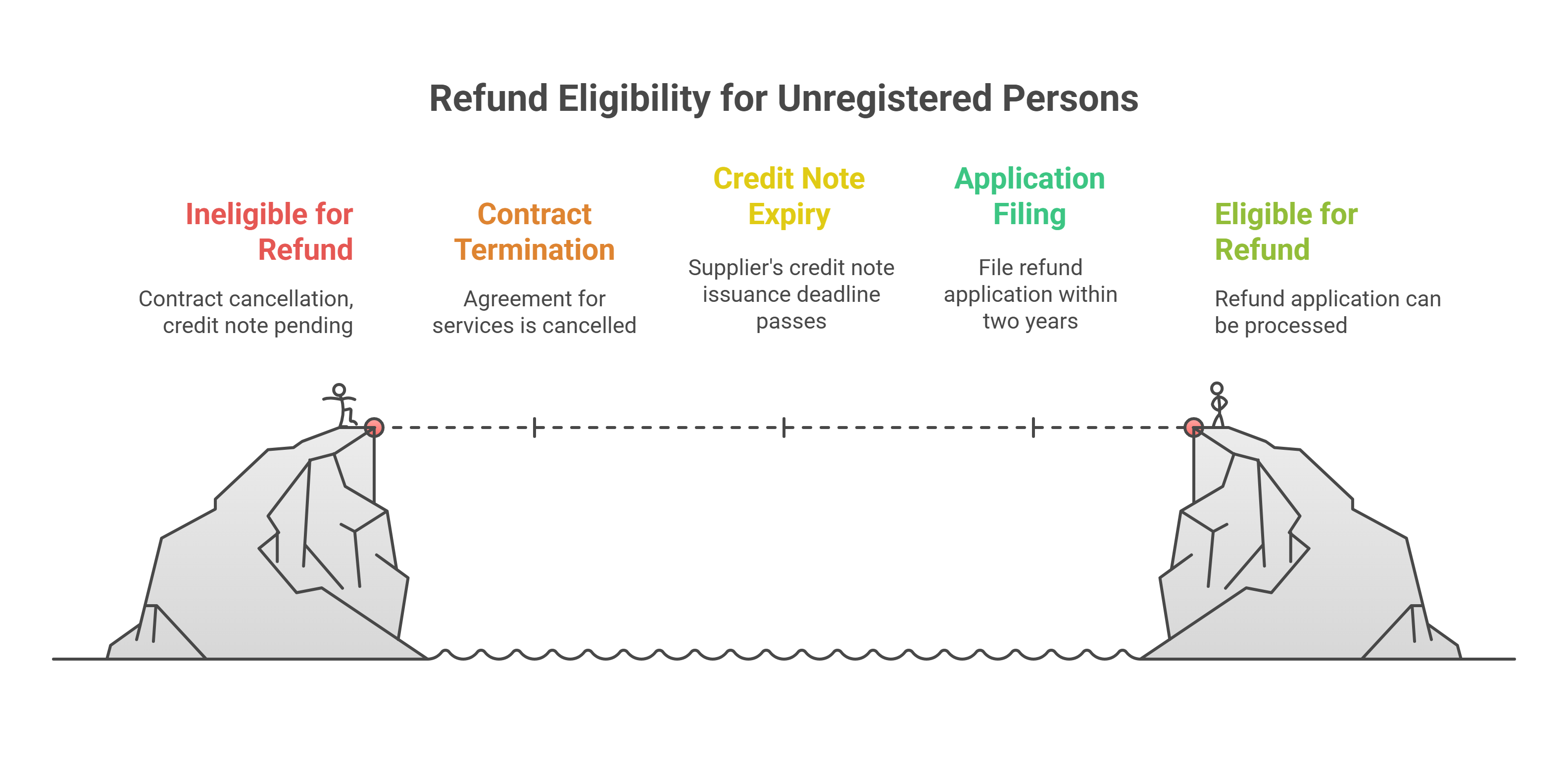

• Circumstances for Refund: This provision is applicable to unregistered persons who have entered into an agreement or contract for the supply of services, and that agreement or contract has subsequently been cancelled or terminated. Specific scenarios include the construction of flats/buildings and long-term insurance policies with upfront premium payments that are terminated.

• Supplier's Credit Note Expiry: An unregistered person can only apply for such a refund if the time limit for the supplier to issue a credit note under section 34 has expired.

• Relevant Date for Application: For the purpose of determining the two-year time limit for filing the refund application, the date of issuance of the letter of cancellation or termination of the contract/agreement by the supplier will be considered as the date of receipt of the services by the applicant.

Procedure for Filing:

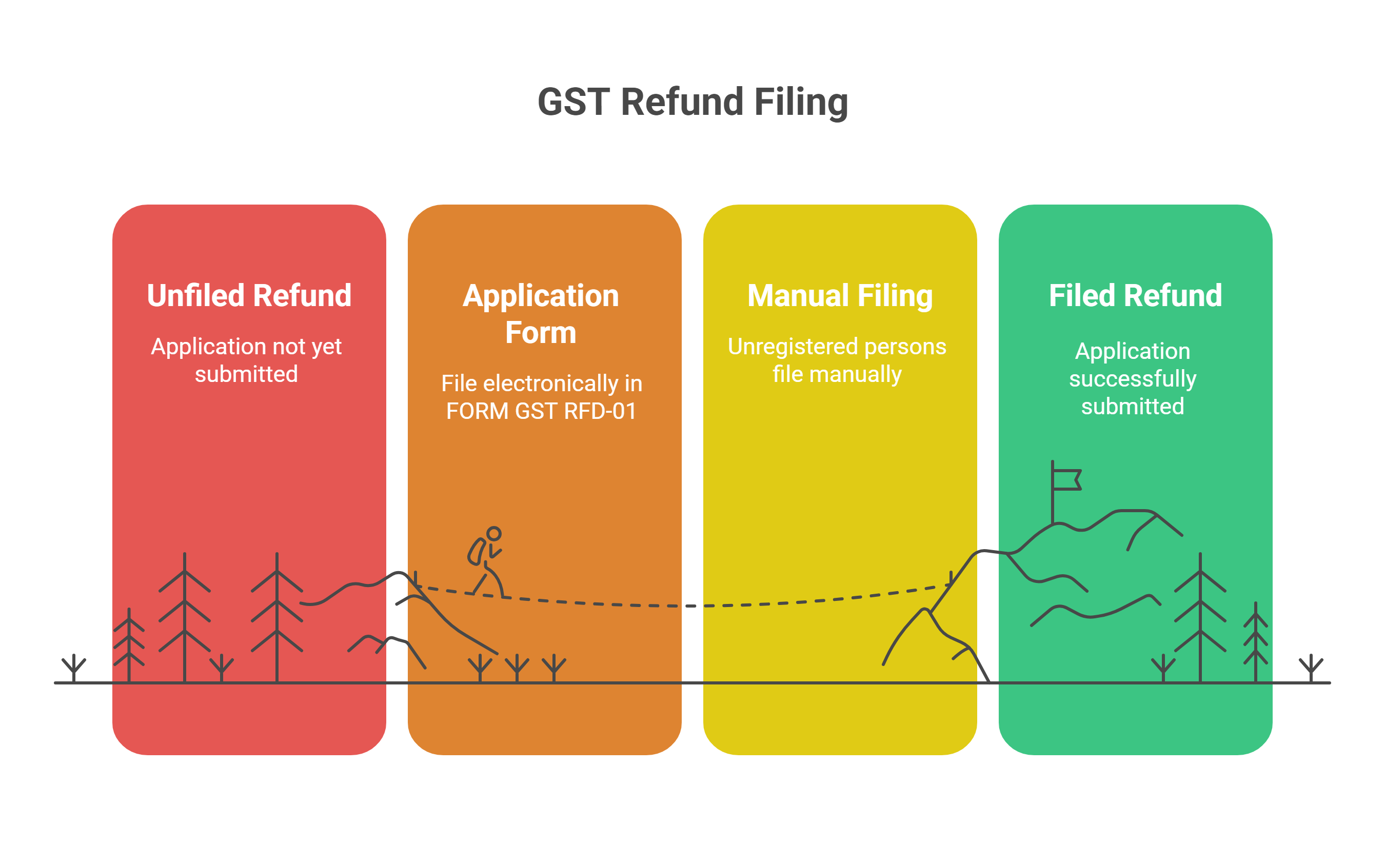

• Application Form: The refund application must be filed electronically in FORM GST RFD-01.

• Manual Filing: As per Circular No. 188/20/2022-GST, a manual filing and processing mechanism is prescribed for unregistered persons in these specific scenarios.

Documentary Evidence Required (Annexure 1 in FORM GST RFD-01):

When an unregistered person claims a refund due to a cancelled or terminated service contract, the application must be accompanied by the following documentary evidence:

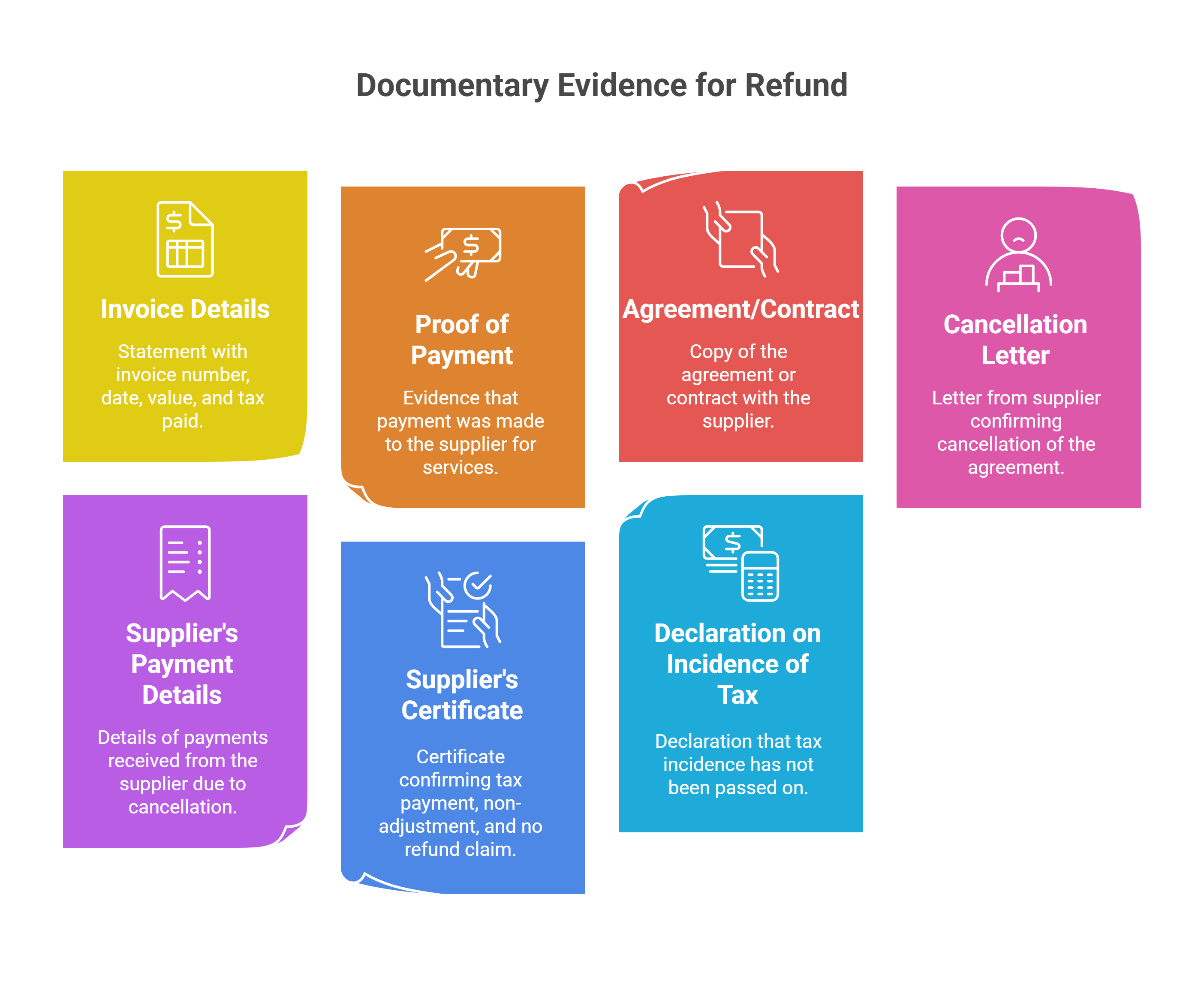

• Invoice Details: A statement containing details of invoices, including their number, date, value, and tax paid.

• Proof of Payment: Proof that the payment for the services was made to the supplier.

• Agreement/Contract: A copy of the agreement or registered agreement or contract entered into with the supplier for the supply of service.

• Cancellation/Termination Letter: The letter issued by the supplier confirming the cancellation or termination of the agreement or contract for supply of service.

• Supplier's Payment Details: Details of any payment received from the supplier against the cancellation or termination of such agreement, along with proof thereof.

• Supplier's Certificate (FORM GST RFD-01, clause (kb)): A crucial certificate issued by the supplier to confirm the following:

◦ The supplier has paid tax in respect of the invoices on which the refund is being claimed by the applicant.

◦ The supplier has not adjusted the tax amount involved in these invoices against their tax liability by issuing a credit note.

◦ The supplier has not claimed and will not claim a refund of the amount of tax involved in respect of these invoices.

• Declaration on Incidence of Tax (FORM GST RFD-01, clause (l)): A declaration to the effect that the incidence of tax, interest, or any other amount claimed as refund has not been passed on to any other person is generally required. However, this declaration is not needed if the amount of refund claimed does not exceed two lakh rupees, or in cases where the refund is claimed by an unregistered person who has borne the incidence of tax.

General Time Limit for Refunds (Section 54)

Any person claiming a refund under Section 54 must typically make an application before the expiry of two years from the relevant date. However, for refunds of excess balance in the electronic cash ledger, this two-year time limit is not applicable.

What documents are needed by the Unregistered Person to claim Refund?

For an unregistered person claiming GST refunds due to cancelled service contracts, specific documentary evidence must accompany the refund application in FORM GST RFD-01.

These documents are prescribed in Annexure 1 of FORM GST RFD-01 and include:

• A statement containing details of invoices, including their number, date, value, and the tax paid.

• Proof of making payment to the supplier for the services.

• A copy of the agreement or registered agreement or contract entered into with the supplier for the supply of service.

• The letter issued by the supplier for cancellation or termination of the agreement or contract for the supply of service.

• Details of any payment received from the supplier against the cancellation or termination of such agreement, along with proof thereof.

• A certificate issued by the supplier (in terms of FORM GST RFD-01, clause (kb)) affirming the following:

◦ The supplier has paid tax in respect of the invoices on which the refund is being claimed by the applicant.

◦ The supplier has not adjusted the tax amount involved in these invoices against their tax liability by issuing a credit note.

◦ The supplier has not claimed and will not claim a refund of the amount of tax involved in respect of these invoices.

• A declaration to the effect that the incidence of tax, interest, or any other amount claimed as refund has not been passed on to any other person (FORM GST RFD-01, clause (l)). However, this declaration is not required if the refund is claimed by an unregistered person who has borne the incidence of tax.

It is important to note that an unregistered person can only apply for such a refund if the time limit for the supplier to issue a credit note under section 34 has expired. For these cases, the "relevant date" for determining the two-year time limit for filing the refund application is considered to be the date of issuance of the letter of cancellation or termination of the contract/agreement by the supplier. While Rule 97A, which allowed manual filing and processing of refunds, is not relevant in the present online ecosystem, unregistered persons are specifically enabled for filing refund applications in these scenarios.

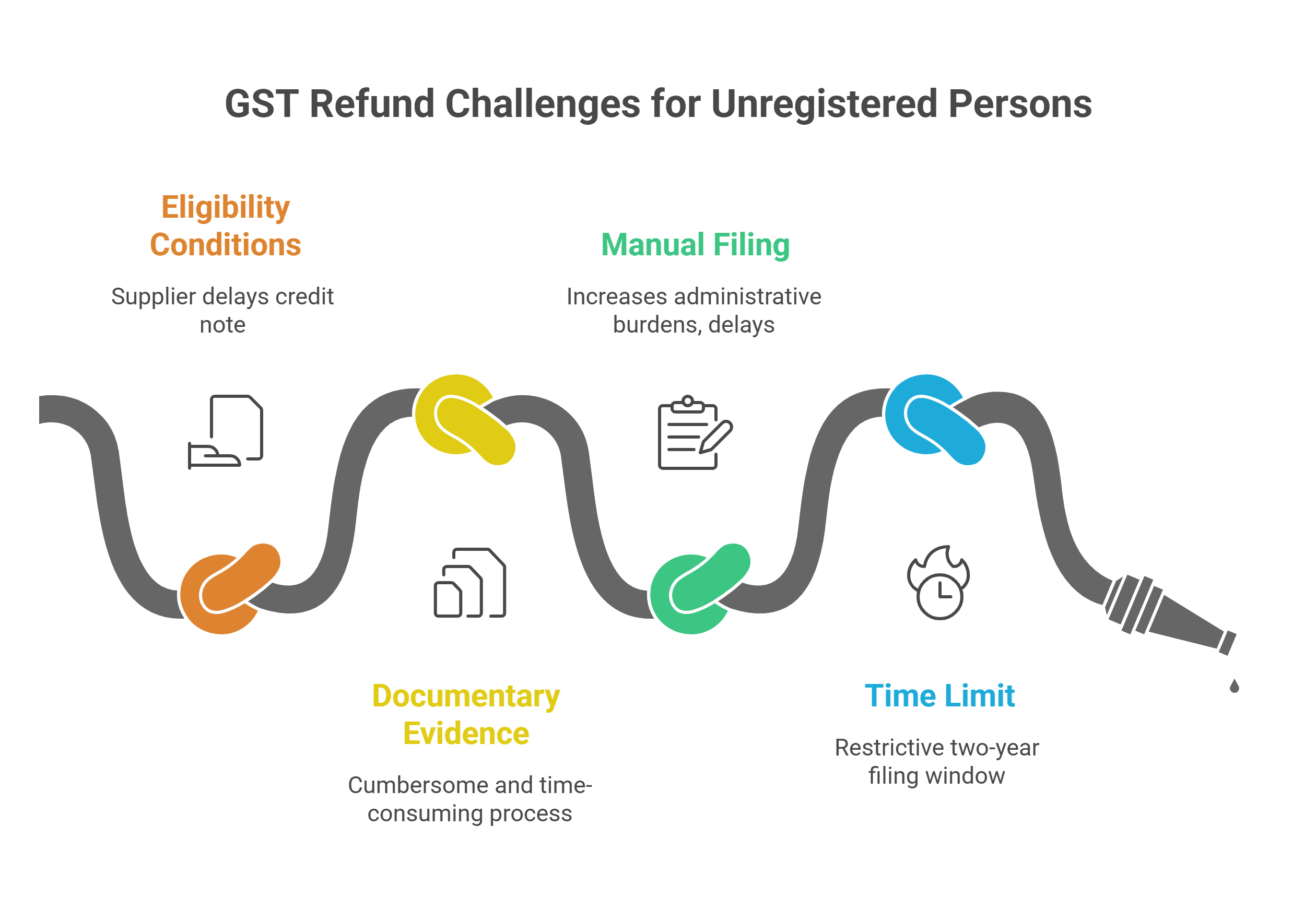

What are the main challenges faced in Refund?

The main challenges faced in the GST refund process for unregistered persons, particularly in cases of cancelled or terminated service contracts, include:

-

Eligibility and Conditions: An Unregistered person must meet specific conditions to be eligible for refunds, such as the expiry of the supplier's credit note issuance period. This can be a challenge if the supplier delays or fails to issue the necessary credit note.

-

Documentary Evidence: The requirement to provide extensive documentary evidence, including invoice details, proof of payment, agreement/contract copies, cancellation/termination letters, and supplier's certificates, can be cumbersome and time-consuming.

-

Manual Filing: Although the application must be filed electronically using FORM GST RFD-01, there are scenarios where manual filing is prescribed. This can lead to additional administrative burdens and potential delays.

-

Time Limit for Refunds: The two-year time limit for filing the refund application from the relevant date can be restrictive. Unregistered persons need to be vigilant about deadlines to avoid missing the opportunity to claim refunds.

Conclusion:

In conclusion, the GST refund process for unregistered persons, particularly in cases of cancelled or terminated service contracts, is well-defined under Section 54 of the CGST Act. Unregistered persons can claim refunds if specific conditions are met, such as the expiry of the supplier's credit note issuance period and the submission of necessary documentary evidence. The application must be filed electronically using FORM GST RFD-01, with manual filing allowed in certain scenarios. The process ensures that the tax incidence is not passed on to another person, and the refund claim is made within the stipulated two-year time limit. This structured approach aims to provide clarity and fairness in the refund process for unregistered persons.

GST Software | Eway Bill Api | Powers of Revisional Authority Under GST | Kaju GST Rate | Maintenance GST Rate

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified