Can GST Refund be rejected when the LUT is filed after/post Exports?

No, a refund claim for zero-rated supplies (exports) cannot be rejected solely on the procedural ground that the Letter of Undertaking (LUT) was filed after the date of export. The requirement to furnish an LUT prior to export under Rule 96A of the CGST Rules, 2017, is considered a directory and not a mandatory provision. The CBIC has clarified via circulars that such procedural delays can be condoned, and the LUT can be accepted on an ex post facto basis. The substantive benefit of a refund cannot be denied for a curable procedural lapse.

Detailed Explanation

Under the GST framework, an exporter has two options for making zero-rated supplies:

1. Export goods or services on payment of IGST and subsequently claim a refund of the tax paid.

2. Export goods or services without payment of IGST by furnishing a Bond or a Letter of Undertaking (LUT).

The procedure for exporting without payment of IGST is governed by Section 16(3)(a) of the IGST Act, 2017, read with Rule 96A of the CGST Rules, 2017.

Legal Provision and Clarification

-

Rule 96A of the CGST Rules, 2017: This rule stipulates that an exporter is required to furnish a Bond or an LUT in Form GST RFD-11 to the jurisdictional Commissioner before making zero-rated supplies.

-

CBIC Circulars: The Central Board of Indirect Taxes and Customs (CBIC) has addressed situations where exporters make zero-rated supplies before furnishing the LUT.

-

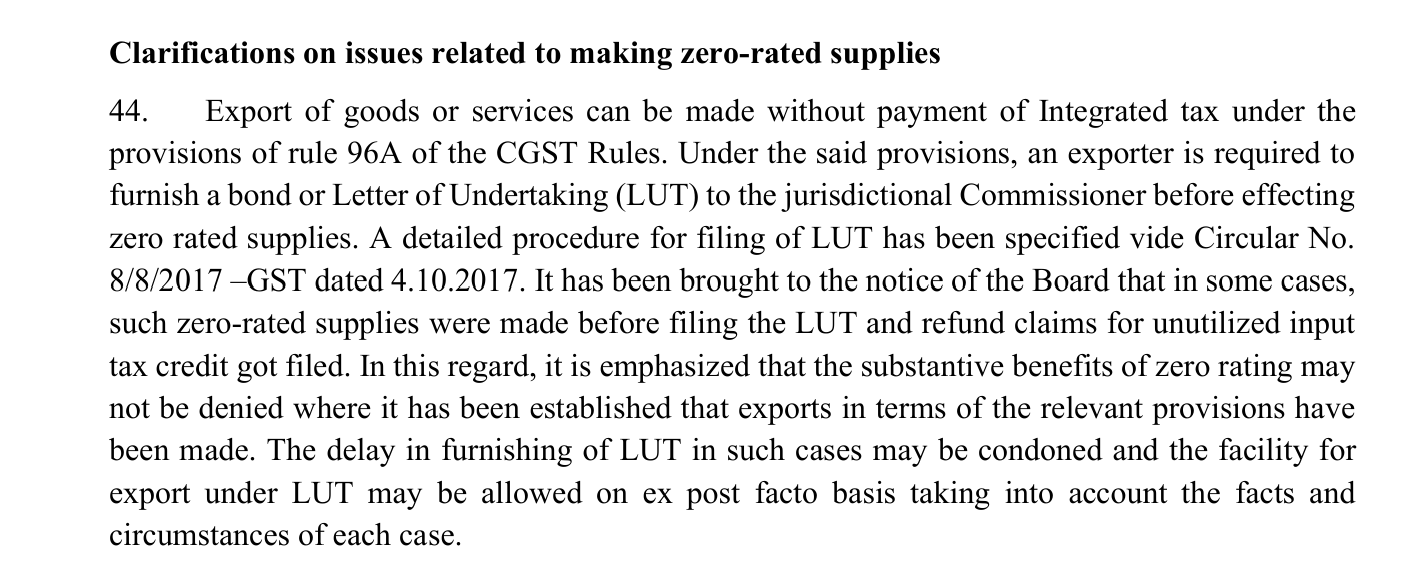

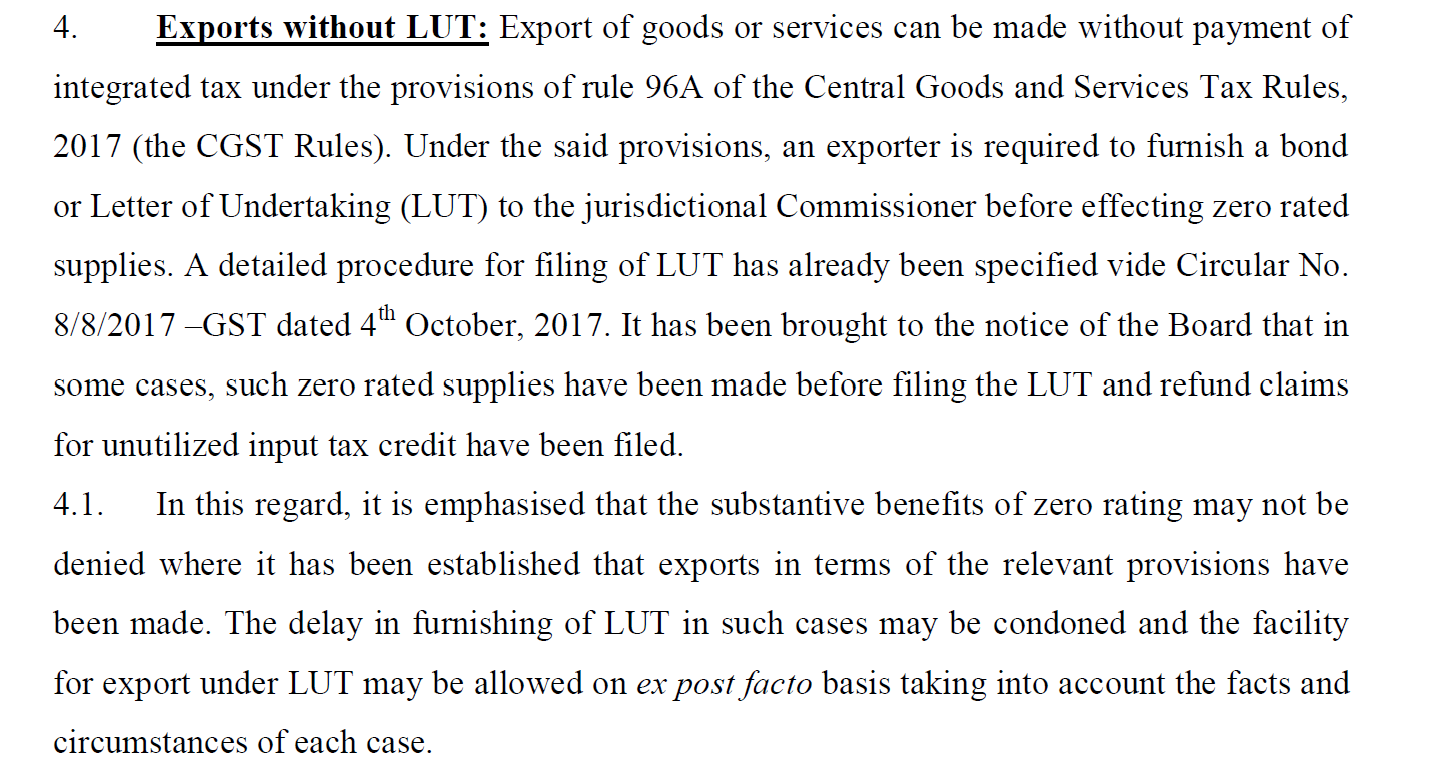

Circular No. 37/11/2018-GST dated 15.03.2018 and Circular No. 125/44/2019-GST dated 18.11.2019 emphasise that the substantive benefits of zero-rating should not be denied where it is established that exports have been made in accordance with the relevant provisions.

-

These circulars explicitly state that the delay in furnishing the LUT can be condoned, and the facility for export under LUT may be allowed on an ex post facto basis, considering the facts and circumstances of each case.

This administrative clarification establishes that the non-submission of an LUT before export is a curable procedural defect, not a fatal error that would extinguish the exporter's right to claim a refund of unutilized Input Tax Credit (ITC).

Relevant Judicial Pronouncement

The judiciary has affirmed this position, holding that procedural lapses should not override substantive entitlements.

M/S Prime Perfumery Works vs. Assistant Commissioner Of Central Tax (Karnataka High Court) Writ Petition No. 11076 of 2024 (T-RES) : 02-Dec-2025 :: (2026) 38 Centax 232 (Kar.)/2026 (106) G.S.T.L. 301 (Kar.)

-

Facts: The petitioner's refund claim for unutilized ITC on zero-rated supplies was rejected by the department. The sole reason for rejection was the failure to furnish the LUT in Form GST RFD-11 prior to the export of goods, as required under Rule 96A.

-

Issue: Whether a refund claim on zero-rated supplies can be rejected solely because the exporter failed to furnish the LUT before the export.

-

Observations of the Court:

-

The High Court heavily relied on Circular No. 37/11/2018-GST dated 15.03.2018, which provides for the condonation of delay and post-facto acceptance of the LUT.

-

The Court observed that the circular itself demonstrates that the non-submission of an LUT before export is not an incurable defect and does not extinguish the assessee's right to a refund.

-

It was held that the requirement is directory in nature, and the substantive benefit of a refund cannot be denied for a procedural delay, especially when a mechanism to cure the defect is provided by the tax administration itself.

-

The Court noted that the adjudicating authority had completely failed to consider this binding circular while rejecting the refund claim.

-

Ruling: The writ petition was allowed, and the refund rejection order was set aside. The matter was remitted back to the authority for fresh consideration, with a direction to consider the application in light of the Court's observations and the beneficial provisions of the circular allowing for ex post facto acceptance of the LUT.

Conclusion:

The late filing of LUT is not a fatal defect by itself, but the officer can still scrutinise whether:

-

the supply was genuinely zero-rated,

-

exports were completed,

-

invoices and shipping/banking evidence match,

-

refund computation is correct, and

-

there are no other statutory deficiencies. Circular No. 37/11/2018-GST (Mar. 15, 2018)

So, a GST refund should generally not be rejected solely because the LUT was filed after export. The better view, supported by CBIC, is that the LUT delay may be condoned and a refund considered on the merits if the export is otherwise established.

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified