The GST Evolution: Real Estate ITC Reversals and Apportionment

The real estate sector presents unique complexities under GST, especially in the apportionment and reversal of Input Tax Credit (ITC). A structural shift occurred with effect from 1 April 2019, commonly known as GST 2.0 for real estate. This change fundamentally altered how developers compute and claim Input Tax Credit (ITC) on construction services, which plays a crucial role in GST compliance.

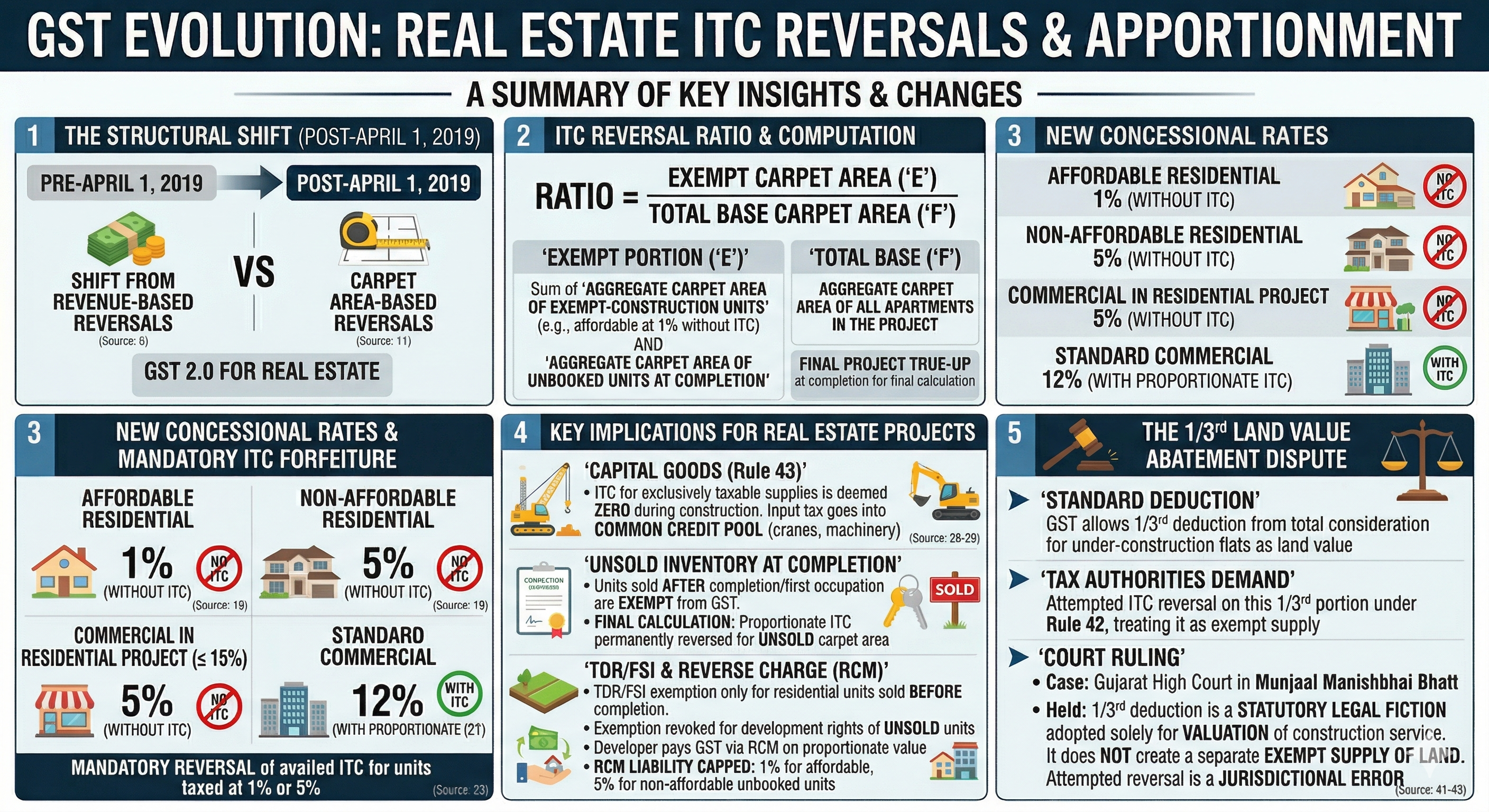

The Shift from Revenue to Carpet Area for Reversals

Prior to 1 April 2019, ITC reversals for common credits relied on the proportion of exempt revenue. This approach created a structural flaw. Developers incurred heavy common construction expenses in the initial phases when no exempt revenue existed. They claimed full ITC at that stage. Exempt revenue from units sold after the issuance of the completion certificate arose later, when construction expenses were minimal. Developers thus retained disproportionate credits.

The amended Rule 42 and Rule 43 of the CGST Rules corrected this anomaly. For a detailed breakdown, refer to Rule 42 and Rule 43 ITC reversal mechanism.

For the purpose of calculation:

- The exempt portion ('E') comprises the aggregate carpet area of apartments whose construction is exempt from tax, plus the carpet area of apartments that remain unbooked (unsold) at the time of issuance of the completion certificate or first occupation, whichever is earlier.

- The total base ('F') is the aggregate carpet area of all apartments in the project.

New Concessional Rates and Mandatory ITC Forfeiture

New projects commencing on or after 1 April 2019 are subject to mandatory concessional tax rates. These rates expressly deny the benefit of ITC.

- Sale of affordable residential apartments attracts tax at 1% without ITC.

- Sale of non-affordable residential apartments attracts tax at 5% without ITC.

- Sale of commercial units in a Residential Real Estate Project (where the commercial area does not exceed 15% of the total area) attracts tax at 5% without ITC. In contrast, commercial units in standard real estate projects are taxed at 12% with proportionate ITC.

Developers are not entitled to ITC on units taxed at 1% or 5%. They must reverse the ITC availed from the project's inception to the extent it relates to construction services for such units.

Treatment of Capital Goods and Final Project True-Up

Rule 43 of the CGST Rules applies a specific legal fiction to capital goods used in real estate projects. During the construction phase, the ITC intended for exclusively taxable supplies is deemed to be zero. Capital goods, such as cranes and machinery, serve the entire project. Their entire input tax is therefore routed into the common credit pool.

Real estate projects mandate a final re-calculation (final true-up) in the tax period when the completion certificate is issued or first occupation occurs. Developers reconcile the provisional monthly reversals made over the project life against the final carpet area ratio of units that actually remained unsold. Any shortfall in reversals must be paid along with interest from 1 April of the succeeding financial year. Any excess reversal can be reclaimed as credit.

Transfer of Development Rights (TDR) and Joint Development Agreements (JDA)

Under Joint Development Agreements (JDAs), the transfer of Development Rights (TDR), Floor Space Index (FSI), or long-term lease rights by the landowner to the developer is exempt from GST, subject to prescribed conditions. This exemption applies when these rights are used for the construction of residential apartments. The apartments must be sold before the completion of the project. This treatment aligns with TDR under GST in real estate.

The exemption stands revoked for development rights attributable to commercial premises or residential flats that remain unsold on the date of project completion. In such cases, the developer becomes liable to pay GST under the GST under the Reverse Charge Mechanism (RCM) on the proportionate value of those rights.

The 1/3rd Land Value Abatement Dispute

When a developer sells an under-construction flat, the GST framework permits a standard 1/3rd deduction from the total consideration towards the value of land. Tax authorities have at times demanded reversal of ITC under Rule 42 on this 1/3rd portion, treating it as an exempt supply.

This interpretation remains controversial. The Gujarat High Court in Munjaal Manishbhai Bhatt held that the 1/3rd deduction constitutes a statutory legal fiction adopted solely for valuation of the taxable construction service. It does not create a separate exempt supply of land. Consequently, any attempt by the department to trigger ITC reversal under Rule 42 on the land abatement amounts to a jurisdictional error.

The GST Input Tax Credit Reversal Ratio for Real Estate

Under the amended Rule 42 and Rule 43 of the CGST Rules, developers compute the ITC reversal ratio for a real estate project as the exempt carpet area ('E') divided by the total carpet area ('F') of the project.

Determination of the E/F Ratio Components

- Total Base ('F'): Aggregate carpet area of all apartments in the entire project.

- Exempt Portion ('E'): Aggregate carpet area of (i) apartments whose construction is explicitly exempt from tax (such as affordable housing units taxed at 1% without ITC), plus (ii) apartments that are not inherently exempt but remain unbooked (unsold) and are identified to be sold after the issuance of the completion certificate or first occupation.

Important Considerations for the Computation

Carpet area is defined as per RERA guidelines adopted under GST law. It means the net usable floor area of an apartment. It includes the area covered by internal partition walls but excludes external walls, service shafts, exclusive balconies, verandahs and exclusive open terrace areas.

Reversals during the construction phase remain provisional. In the tax period when the completion certificate is issued or first occupation occurs, a final project-wise calculation is mandatory. The numerator 'E' must then include the aggregate carpet area of all apartments not booked by the date of completion. Any shortfall in ITC reversal requires payment with interest. Any excess reversal can be reclaimed as credit.

The GST Implications of Unsold Residential Inventory

Units sold after the issuance of the Completion Certificate (CC) or first occupation, whichever is earlier, qualify as non-taxable or exempt supplies under GST. No output tax is payable on such sales. Developers are therefore not entitled to retain ITC on the expenses incurred in constructing these units.

ITC Reversal Based on Carpet Area

All credits relating to the project are treated as common credits during construction. In the tax period of issuance of the CC or first occupation, the developer performs a final calculation. The aggregate carpet area of all apartments that remain unbooked by that date is added to the exempt portion ('E') in the E/F ratio. The ITC proportionate to this unsold carpet area is permanently reversed.

Reverse Charge on Development Rights (TDR/FSI)

Where the project utilises Transfer of Development Rights (TDR), Floor Space Index (FSI) or a long-term lease, the standard GST exemption on such rights applies only to units sold before project completion. For units remaining unsold on the date of completion, the developer is liable to pay GST on the proportionate value of the TDR/FSI under the Reverse Charge Mechanism (RCM).

Capping the RCM Liability

To avoid excessive tax burden, the RCM liability on development rights attributable to unsold flats is capped. The maximum tax payable is 1% of the value of the unbooked affordable residential apartments and 5% of the value of the unbooked non-affordable residential apartments.

itc reversal rule 42 & 43 | rule 42 of cgst/sgst rules | gst on tdr under rcm | gst set off rules | input tax credit | gst on apartment maintenance charges

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified