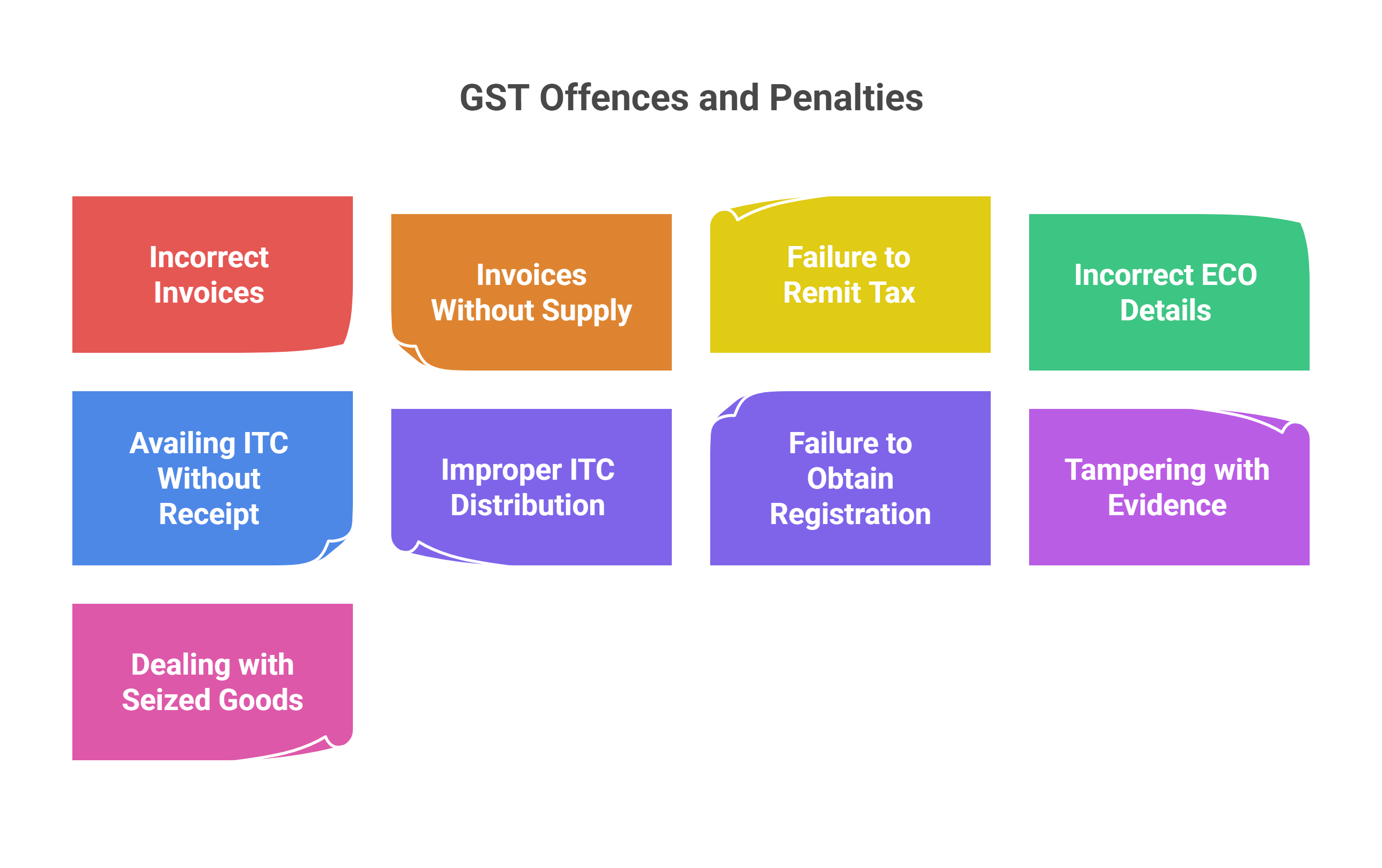

Section 122(1): Penalties for Specific GST Offences

This document outlines the penalties prescribed under Section 122(1) of the Goods and Services Tax (GST) Act for committing any of the 21 specified offences. The penalty for each offence is a fine of ten thousand rupees or an amount equivalent to the tax involved, whichever is higher. This document details some of the key offences covered under this section.

Section 122(1) of the GST Act prescribes penalties for a range of offences. The penalty is set at ten thousand rupees or the amount of tax evaded/involved, whichever is higher. Here are some of the key offences covered under this section:

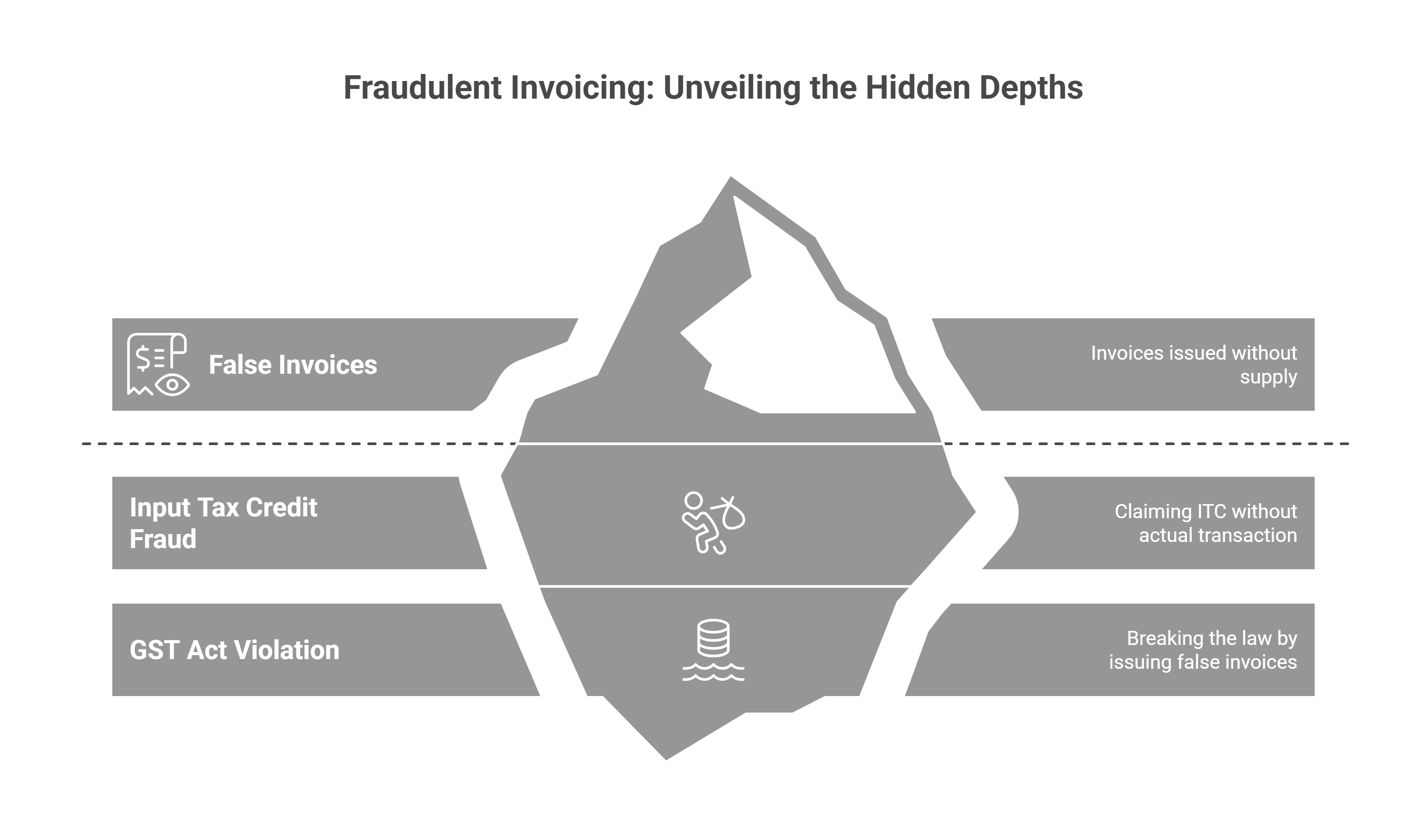

1. Issuing Incorrect or False Invoices:

-

Offence: Supplying goods or services without issuing a proper invoice, or issuing an incorrect or false invoice related to the supply.

-

Implication: This aims to prevent tax evasion by ensuring accurate record-keeping of transactions.

-

References: [152(i), 164(a), 165]

2. Issuing Invoices Without Actual Supply:

-

Offence: Issuing any invoice or bill without actually supplying the goods or services, in violation of the GST Act or its rules.

-

Implication: This targets fraudulent activities where invoices are generated to claim input tax credit (ITC) without any underlying transaction.

-

References: [152(ii), 169]

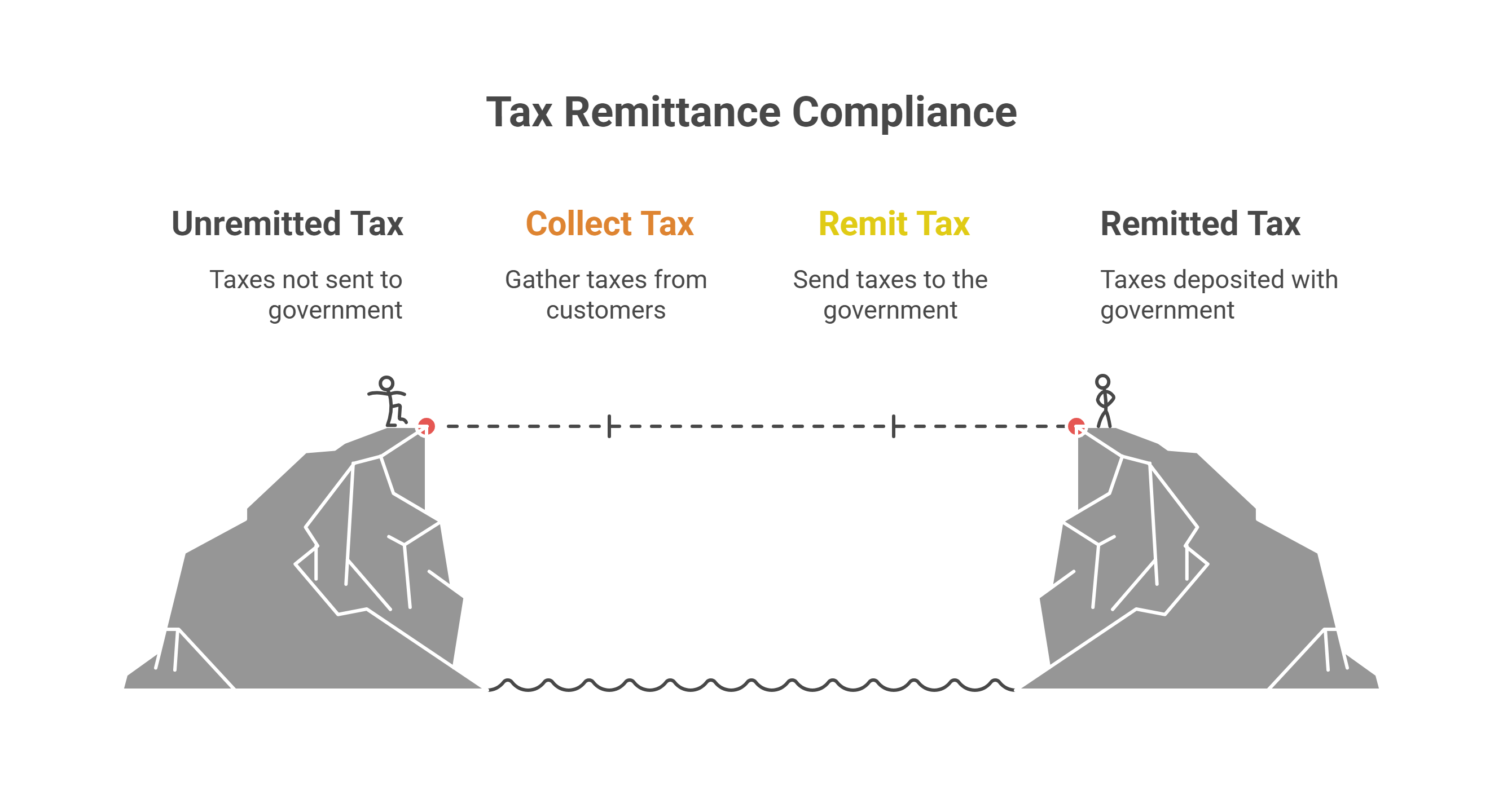

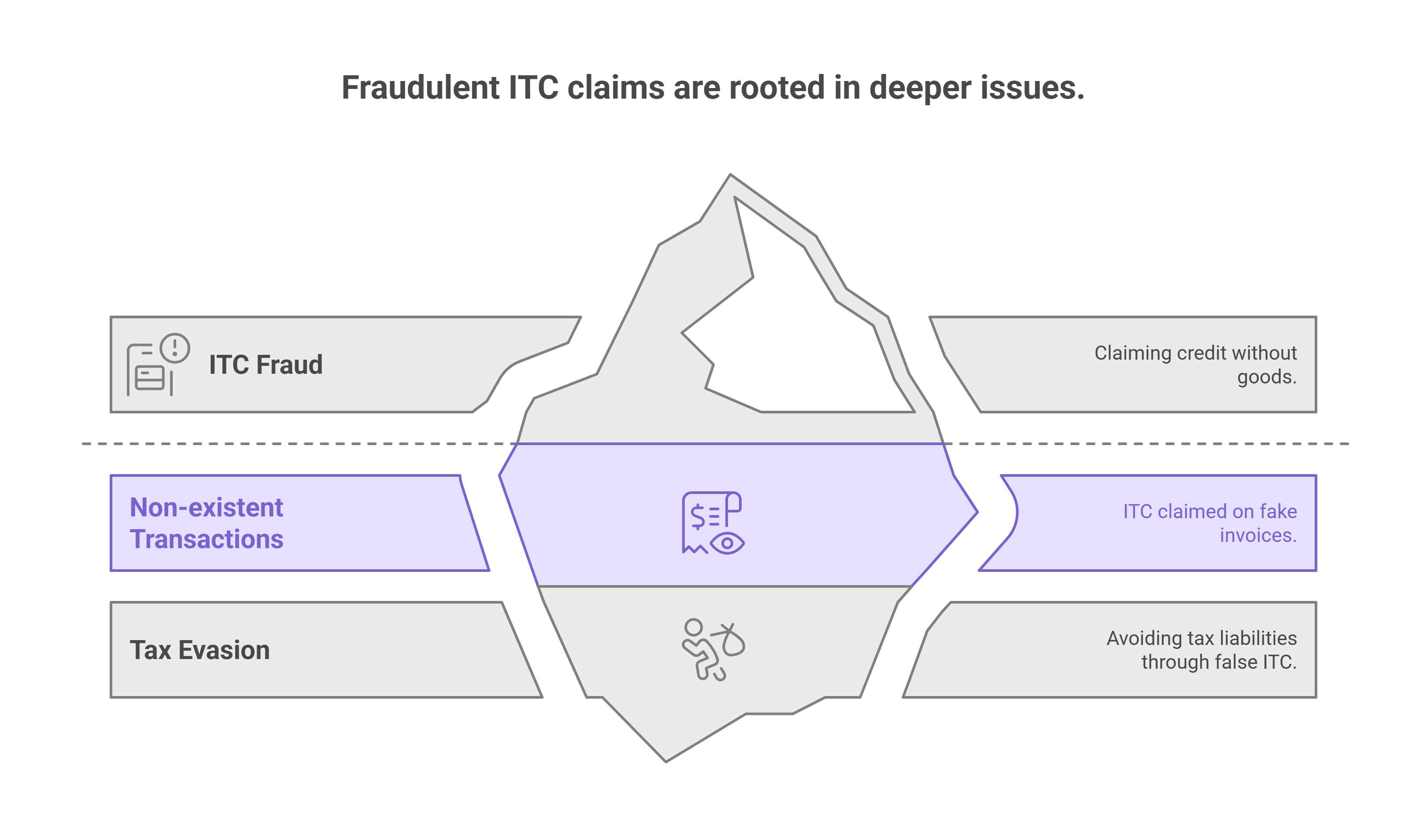

3. Failure to Remit Collected Tax:

-

Offence: Collecting any amount as tax but failing to remit it to the Government within three months from the due date.

-

Implication: This ensures that taxes collected from customers are promptly deposited with the government.

-

References: [194(iii), 494(iii)]

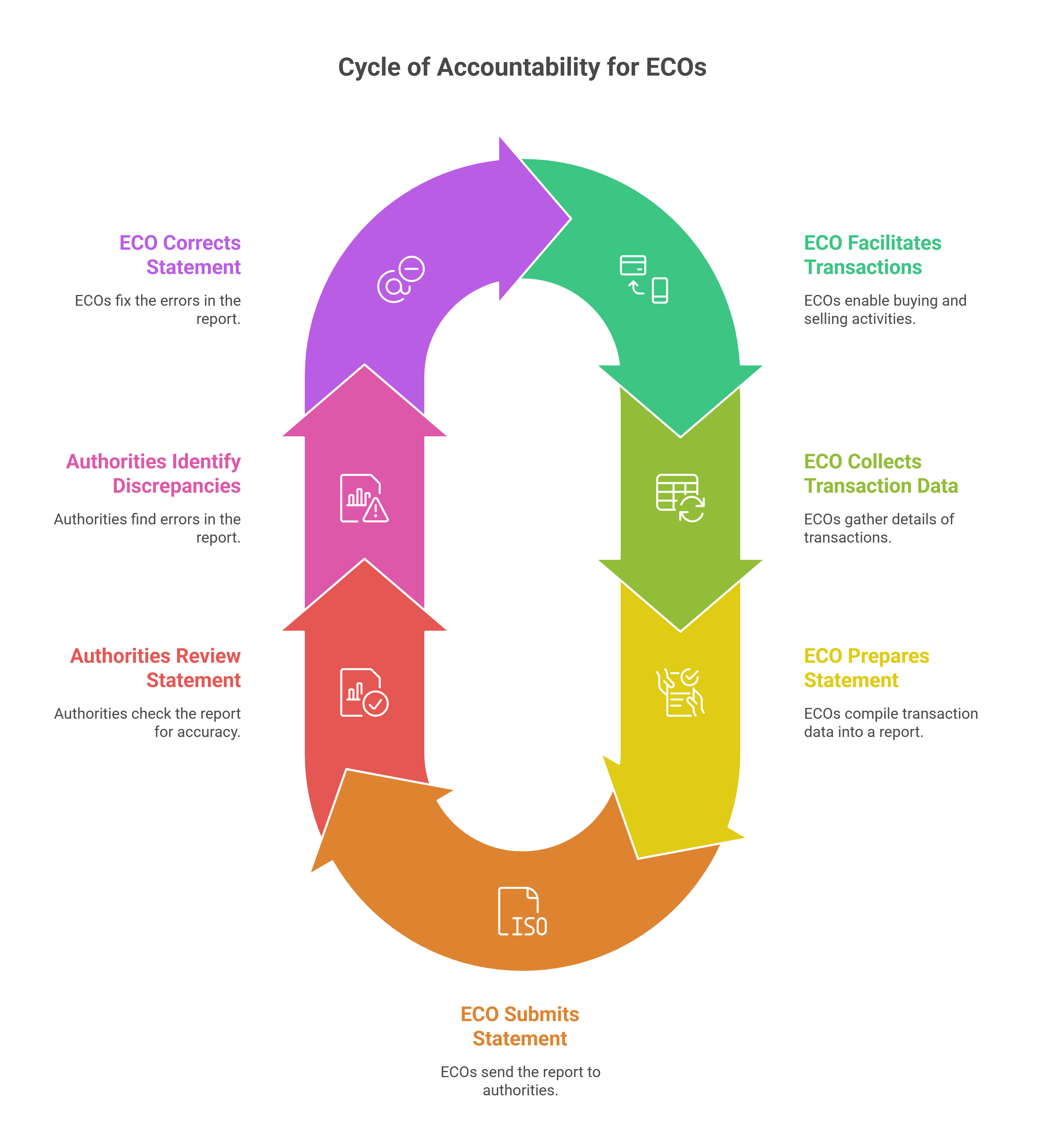

4. Incorrect Details by Electronic Commerce Operators (ECOs):

-

Offence: Failing to furnish correct details in the statement required under Section 52(4) by an Electronic Commerce Operator (ECO).

-

Implication: This holds ECOs accountable for accurate reporting of transactions facilitated through their platforms.

-

References: [153(iii), 160(c)]

5. Availing Input Tax Credit (ITC) Without Actual Receipt:

-

Offence: Taking or utilizing input tax credit (ITC) without actually receiving the goods or services.

-

Implication: This prevents fraudulent claims of ITC based on transactions that did not occur.

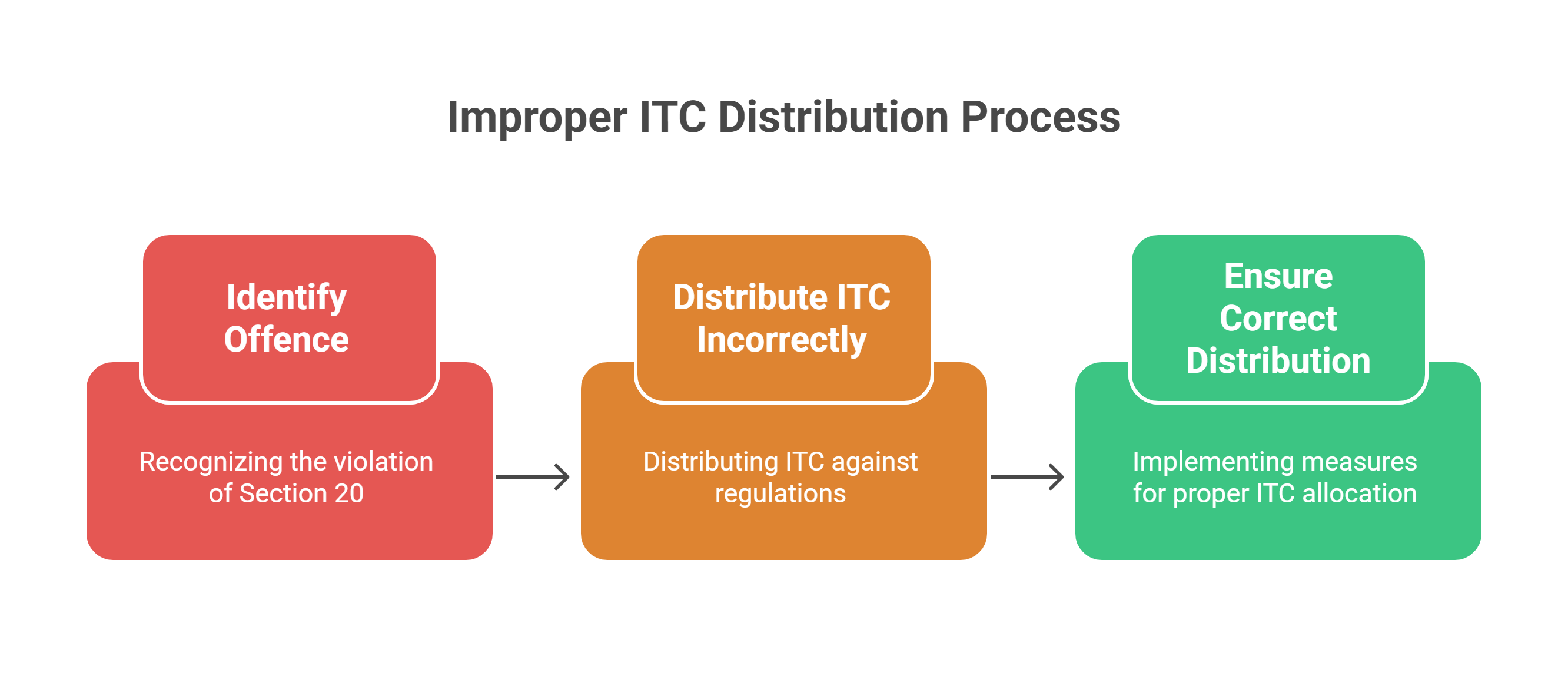

6. Improper Distribution of ITC:

-

Offence: Taking or distributing ITC in contravention of Section 20 of the CGST Act.

-

Implication: This ensures that ITC is distributed correctly among distinct persons as per the regulations.

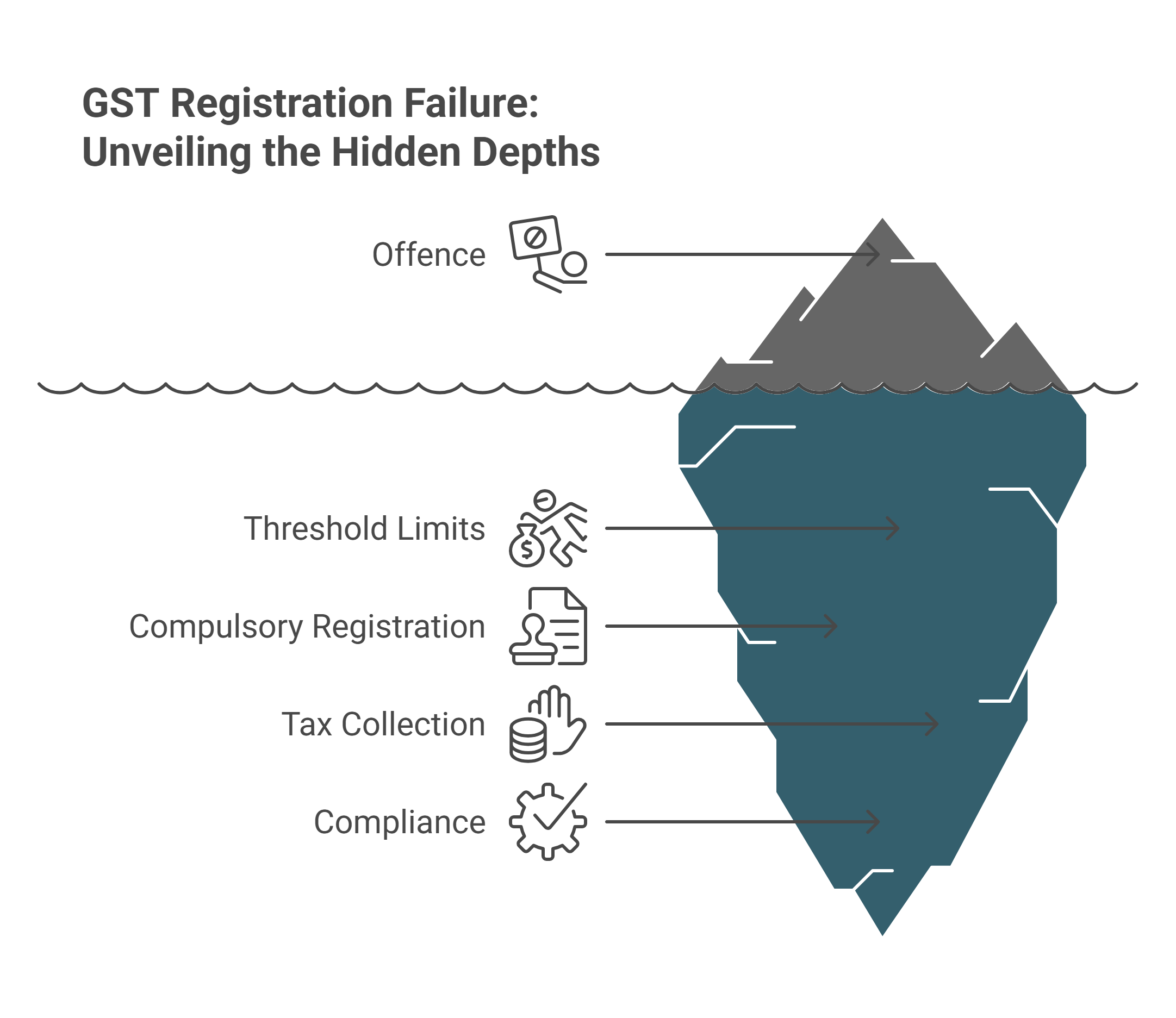

7. Failure to Obtain Registration:

-

Offence: Failing to obtain GST registration when required, such as exceeding the threshold limits or being subject to compulsory registration under Section 24.

-

Implication: This ensures that all eligible businesses are registered under GST to facilitate tax collection and compliance.

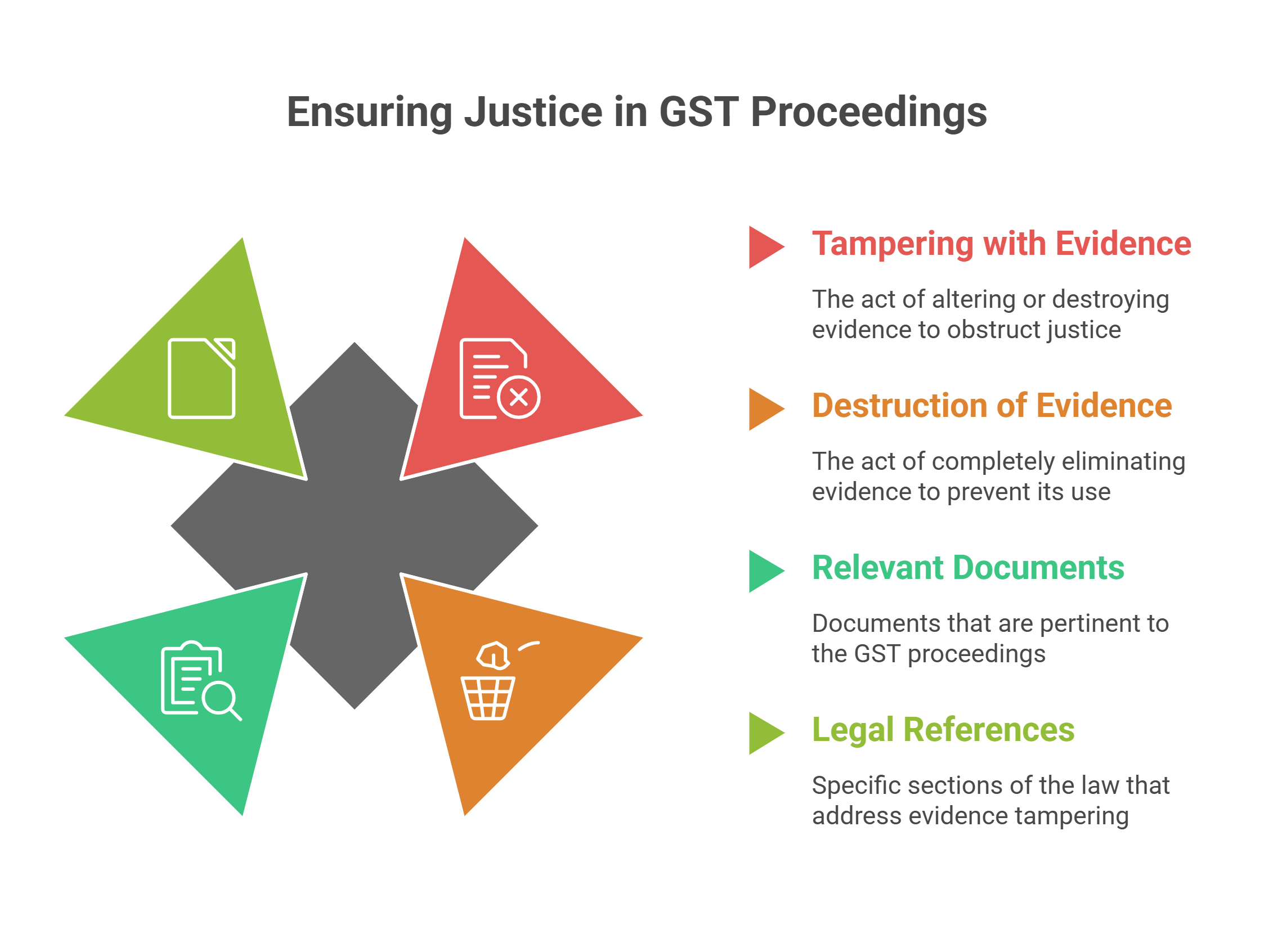

8. Tampering with Evidence:

-

Offence: Tampering with, or destroying, any material evidence or document relevant to GST proceedings.

-

Implication: This prevents obstruction of justice and ensures that all relevant information is available for investigation and assessment.

-

References: [195(xx), 495(xx)]

9. Dealing with Detained/Seized Goods:

-

Offence: Disposing of or tampering with any goods that have been detained, seized, or attached under the GST Act.

-

Implication: This protects the integrity of legal proceedings and ensures that goods under official custody are not misappropriated.

-

References: [195(xxi), 495(xxi)]

In summary, Section 122(1) aims to deter various forms of tax evasion, fraud, and non-compliance under the GST regime by imposing significant penalties on offenders. The penalties are designed to be proportionate to the severity of the offence, ensuring that businesses adhere to the provisions of the GST Act and its rules.

GST Filing Software | Eway Bill Apis | Power of Officer Under GST | GST On Dry Fruits | GST On Society Maintenance

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified