GST Compliance Challenges in the New "Demerit" 40% Slab Sectors

Executive Summary

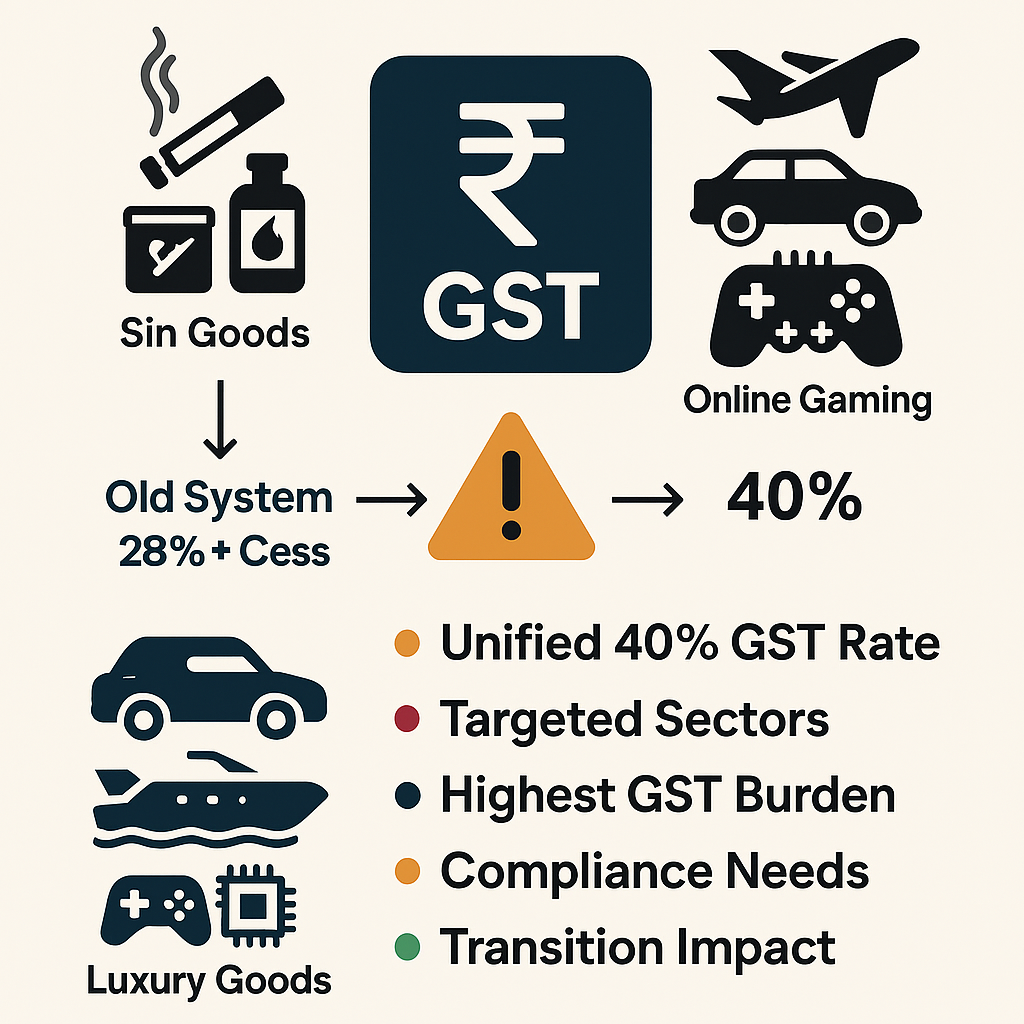

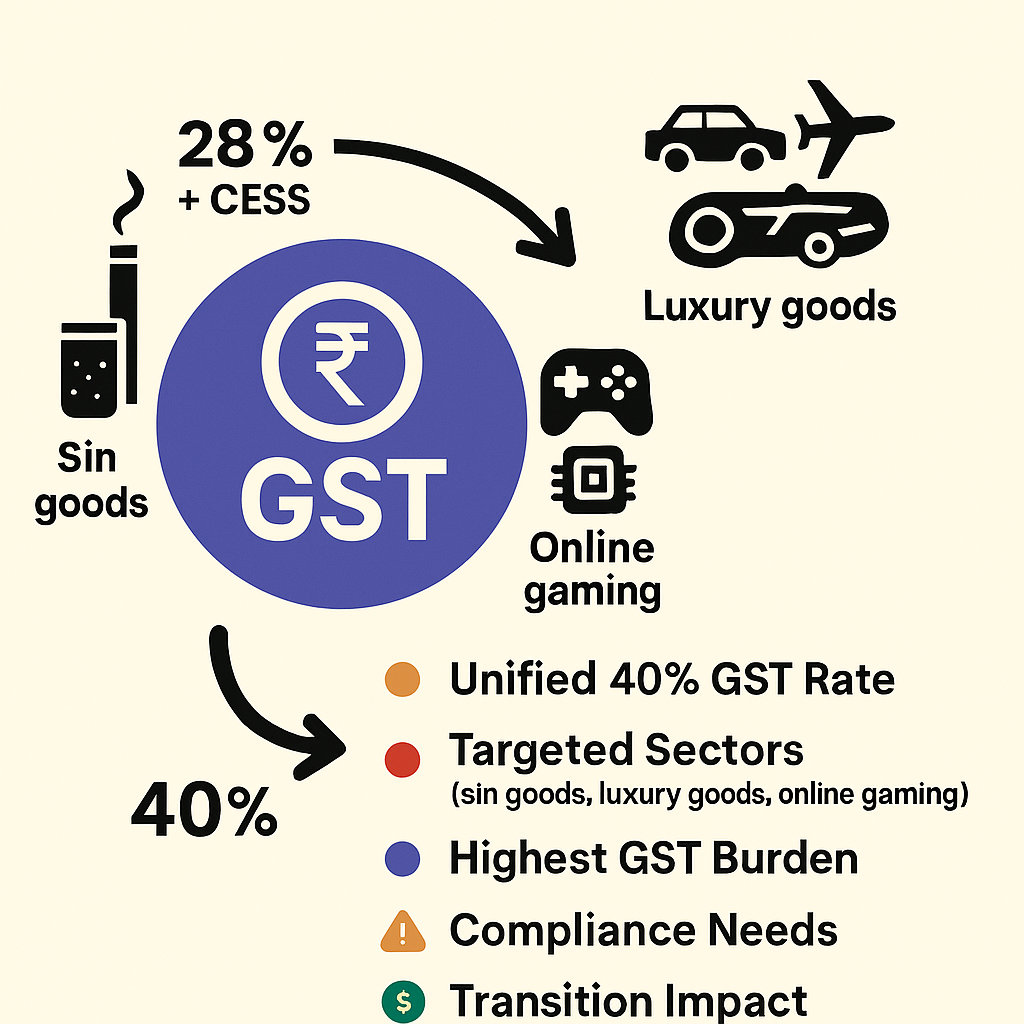

India's GST 2.0 reform, effective September 22, 2025, has fundamentally reshaped the indirect tax landscape by introducing a new 40% "demerit" slab for luxury and sin goods. This comprehensive restructuring replaces the previous complex system of 28% GST plus compensation cess with a unified 40% rate, creating unprecedented compliance and financial planning challenges for businesses operating in these high-impact sectors.

The new framework targets three primary categories: traditional sin goods (tobacco, pan masala, aerated beverages), luxury vehicles and vessels (cars above 1200cc petrol/1500cc diesel, motorcycles exceeding 350cc, yachts, private aircraft), and the emerging online gaming sector. These businesses now face the highest GST burden in India's tax system, requiring sophisticated compliance strategies and careful financial restructuring.

The New 40% Demerit Slab: Scope and Coverage

Sin Goods Classification

The 40% slab encompasses traditional "sin goods" - products deemed harmful to health or society. Key items include tobacco products, pan masala, gutkha, carbonated beverages, caffeinated drinks, and aerated waters. The government's policy rationale centres on discouraging consumption while generating substantial revenue for public welfare initiatives.

Unlike the previous regime, where these items attracted 28% GST plus varying compensation cess rates, the new structure provides clarity through a single 40% rate. However, tobacco products continue under the existing 28% plus cess structure temporarily, transitioning to the 40% slab only after outstanding compensation loans to states are cleared.

Luxury Vehicles and Premium Goods

The luxury segment is undergoing substantial restructuring in accordance with the new slab. Motor vehicles equipped with petrol engines exceeding 1,200cc or diesel engines above 1,500cc are now subject to a 40% rate. Additionally, high-end motorcycles exceeding 350cc, yachts, private aircraft, and weapons such as revolvers and pistols are encompassed within this category.

Interestingly, this represents a net tax reduction for many luxury vehicles previously subject to a 28% GST plus a 15-22% compensation cess, bringing the total effective rate down from 45-50% to the new 40% level. This change aims to boost the luxury automotive segment while maintaining substantial revenue generation.

Online Gaming and Digital Services

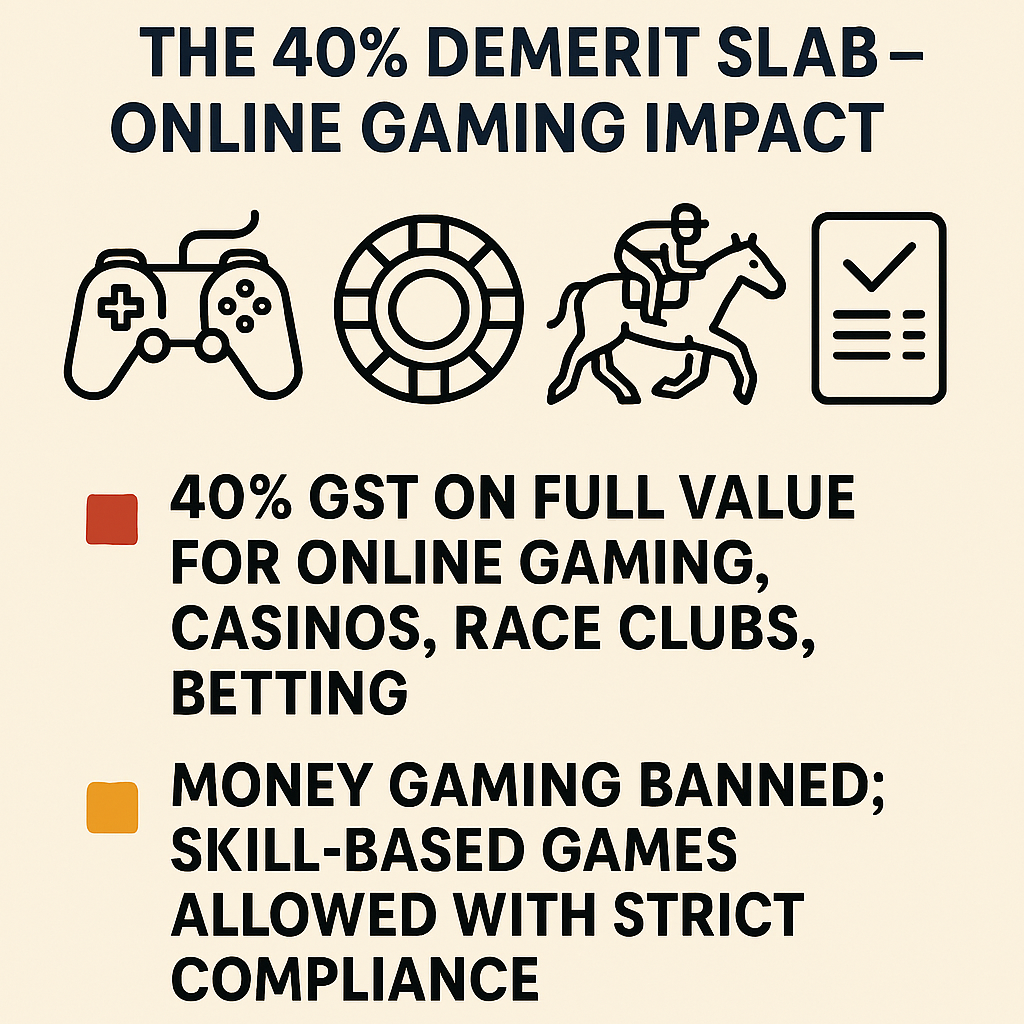

The online gaming sector represents perhaps the most complex compliance challenge within the 40% slab. Gaming platforms, casinos, race clubs, and betting services now attract the unified 40% rate on the full face value of transactions. This includes online gaming deposits, casino chip purchases, and all actionable claims related to gambling and betting.

The sector faces additional regulatory complexity through the Promotion and Regulation of Online Gaming Act, 2025, which banned online money gaming from August 22, 2025, while allowing skill-based games to continue under specific compliance frameworks.

Compliance Challenges and Strategic Responses

Input Tax Credit Complications

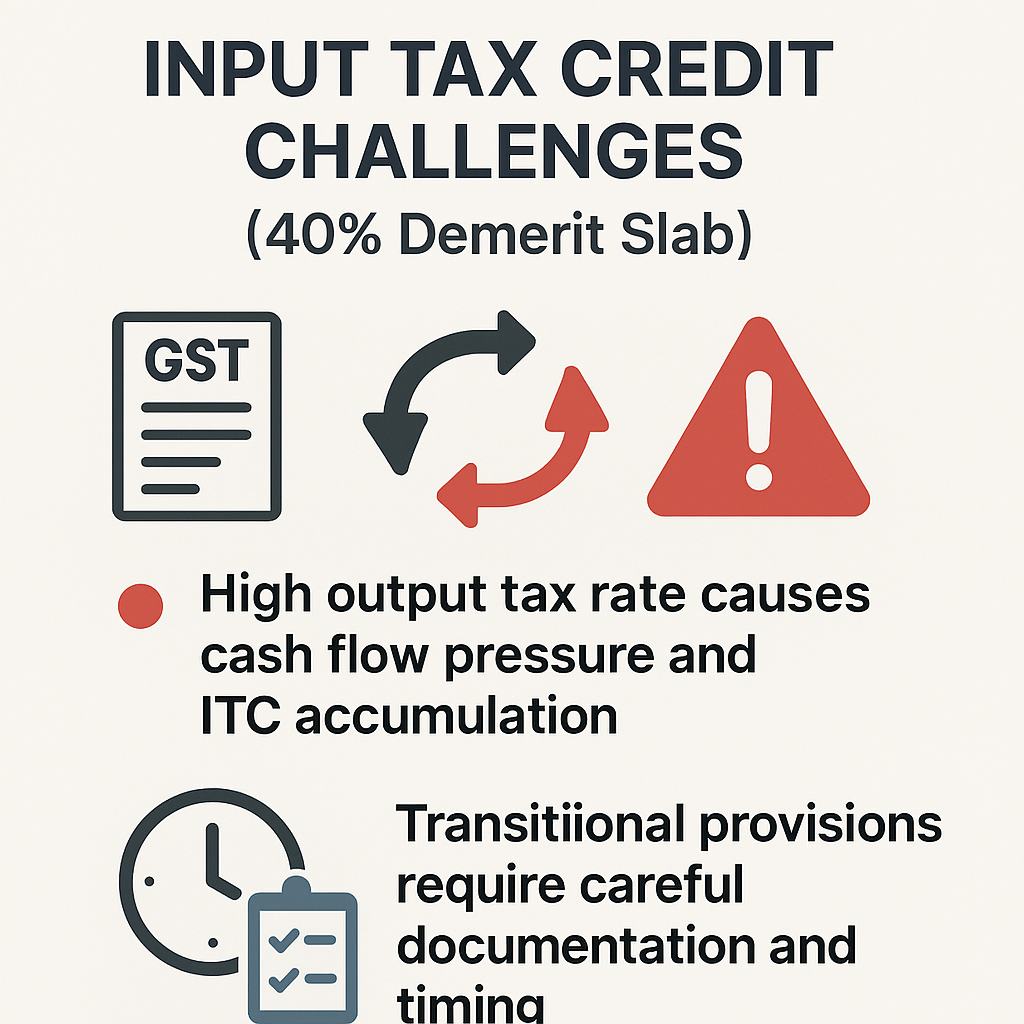

Businesses in the 40% slab face unique challenges with Input Tax Credit (ITC). While they can claim ITC on inputs used in business operations, the high output tax rate creates cash flow pressures when input suppliers operate under lower GST slabs. This inverted duty structure can lead to the accumulation of credits, requiring sophisticated working capital management.

The elimination of compensation cess simplifies ITC calculations, as businesses no longer need to segregate cess components from regular GST. However, transitional provisions for existing stock and pending transactions create temporary compliance burdens requiring careful documentation and rate application based on supply timing.

Registration and Compliance Requirements

Gaming platforms face particularly stringent registration requirements. Online money gaming suppliers must obtain a single registration under the Simplified Registration Scheme of the IGST Act. Foreign gaming platforms serving Indian customers are required to obtain a GST registration, with non-compliance potentially leading to the blocking of the platform.

The regulatory framework empowers the Directorate General of GST Intelligence as the appropriate authority under the Information Technology Act to block unregistered platforms. This enforcement mechanism creates significant compliance risks for international operators entering the Indian market.

Cash Flow Management Strategies

The 40% tax rate poses substantial working capital challenges, particularly for businesses operating on an accrual-based GST system. Companies must pay GST on invoice issuance rather than payment receipt, often creating gaps of 40-90 days between tax payment and revenue realisation.

Luxury goods manufacturers report that nearly 3% of annual revenue can be tied up in GST on unpaid invoices. This necessitates sophisticated cash flow forecasting, credit line arrangements, and pricing strategies that account for extended payment cycles.

Anti-Profiteering Considerations

While the National Anti-Profiteering Authority ceased accepting new complaints from April 1, 2025, businesses remain obligated to pass rate benefits to consumers. The GST 2.0 transition creates reverse anti-profiteering scenarios where luxury goods with reduced effective rates (due to cess elimination) must reflect appropriate price reductions.

Industry leaders emphasise that competitive market forces, rather than regulatory mechanisms, now drive benefit pass-through. However, businesses must maintain detailed justifications for their pricing to demonstrate compliance with fair pricing principles.

Financial Planning and Business Restructuring

Pricing Strategy Adjustments

Companies in the 40% slab require comprehensive pricing strategy overhauls. The unified rate structure simplifies calculation while creating substantial end-consumer price impacts. Luxury automotive dealers report implementing dynamic pricing models that account for inventory transition periods and rate application timing.

Gaming platforms face particular challenges as the 28% rate applies to full deposit values rather than just platform commissions, fundamentally altering revenue models. Many operators report shifting to higher-margin, skill-based offerings to maintain profitability under the new tax structure.

Supply Chain Optimisation

The new rate structure incentivises supply chain restructuring to optimise ITC utilisation and minimise cash flow impact. Luxury goods importers are exploring duty optimisation strategies that balance customs duties with GST implications under the 40% domestic rate.

Some businesses are implementing vendor financing programs to manage the cash flow impact of accrual-based tax payments, while others are renegotiating payment terms with suppliers to align with tax payment obligations.

Technology and Automation Solutions

The complexity of the 40% slab necessitates a robust technology infrastructure. Businesses are implementing automated GST calculation systems that can handle rate transitions, stock valuations, and ITC optimisation across multiple supply chains.

Gaming platforms, in particular, require sophisticated systems to track transaction types, apply appropriate rates, and maintain compliance with both GST and gaming regulations. Many are adopting blockchain-based solutions to ensure transparent transaction recording and regulatory compliance.

Sector-Specific Challenges and Opportunities

Tobacco and Traditional Sin Goods

The tobacco sector is facing a complex transition period, with continued application of the compensation cess alongside eventual migration to the 40% slab. Industry players are implementing dual-track compliance systems to handle both current cess obligations and future applications of the 40% rate.

The uncertainty surrounding transition timing creates inventory management challenges, as companies must balance stock levels against potential rate changes while maintaining a stable market supply. Many are adopting just-in-time inventory strategies to minimise tax rate transition risks.

Luxury Automotive Sector

Despite the net tax reduction for many luxury vehicles, the automotive sector faces implementation challenges around classification and rate application. Vehicles with specifications near the 1200cc/1500cc thresholds require careful documentation to ensure the correct rate is applied.

Dealers are implementing enhanced documentation systems to support rate classifications and maintain compliance with evolving regulatory interpretations. The sector also benefits from simplified compliance through the elimination of cess, thereby reducing administrative burdens.

Online Gaming and Digital Entertainment

The gaming sector's regulatory environment continues evolving, with a distinction between skill-based and chance-based games creating ongoing compliance complexity. Operators must maintain detailed game analysis and classification documentation to support rate applications.

The sector faces additional challenges from state-level gaming regulations that may conflict with GST requirements. Industry associations are working with regulatory authorities to establish clear compliance frameworks that address both tax and gaming law obligations.

Risk Management and Compliance Best Practices

Audit and Documentation Requirements

The 40% slab attracts enhanced audit scrutiny due to its substantial revenue implications. Businesses must maintain comprehensive documentation supporting rate classifications, ITC claims, and pricing decisions. This includes detailed transaction records, classification analyses, and justifications for rate applications.

Gaming operators face particular audit risks due to the complex nature of their transactions and regulatory overlap between GST and gaming laws. Many are implementing third-party audit mechanisms to ensure ongoing compliance and identify potential issues before regulatory review.

Legal and Regulatory Monitoring

The evolving regulatory landscape requires continuous monitoring of GST Council decisions, tribunal rulings, and sector-specific guidance. Businesses are establishing dedicated compliance teams to track regulatory changes and assess their operational impact.

The GST Appellate Tribunal's jurisdiction over anti-profiteering cases creates new legal precedents that businesses must monitor and incorporate into their compliance strategies. Regular legal review of pricing and compliance practices has become essential for risk management.

Conclusion and Strategic Recommendations

The 40% demerit slab marks a significant shift in India's indirect tax landscape, presenting both challenges and opportunities for affected businesses. Success in this environment requires sophisticated compliance strategies that address the unique characteristics of each sector while maintaining operational efficiency and competitive positioning.

Key recommendations include implementing strong tech infrastructure for rate management and compliance, developing cash flow systems for high taxes, establishing clear pricing strategies to balance compliance and competitiveness, and maintaining documentation and audit readiness to support rate classifications and compliance.

Businesses that proactively address these challenges while leveraging the simplified compliance framework will be best positioned to thrive under the new GST 2.0 regime. The elimination of multiple cess components and creation of a unified rate structure, despite the high 40% level, ultimately provides greater predictability and operational clarity for long-term planning and growth.

The success of GST 2.0's demerit slab depends on businesses adapting their operations, systems, and strategies to the high-rate environment while maintaining competitiveness and compliance. Those who succeed will gain advantages in India's simplified but intensified tax landscape.

Valuation Rules Under GST | GST Audit Checklist | GST Audit Process | Matching Reversal and Reclaim of ITC | GST KYC Update

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified