The GST Gauntlet: 3 Surprising Times the Burden of Proof Is on You

Introduction: The Hidden Legal Hurdle in Your GST Filings

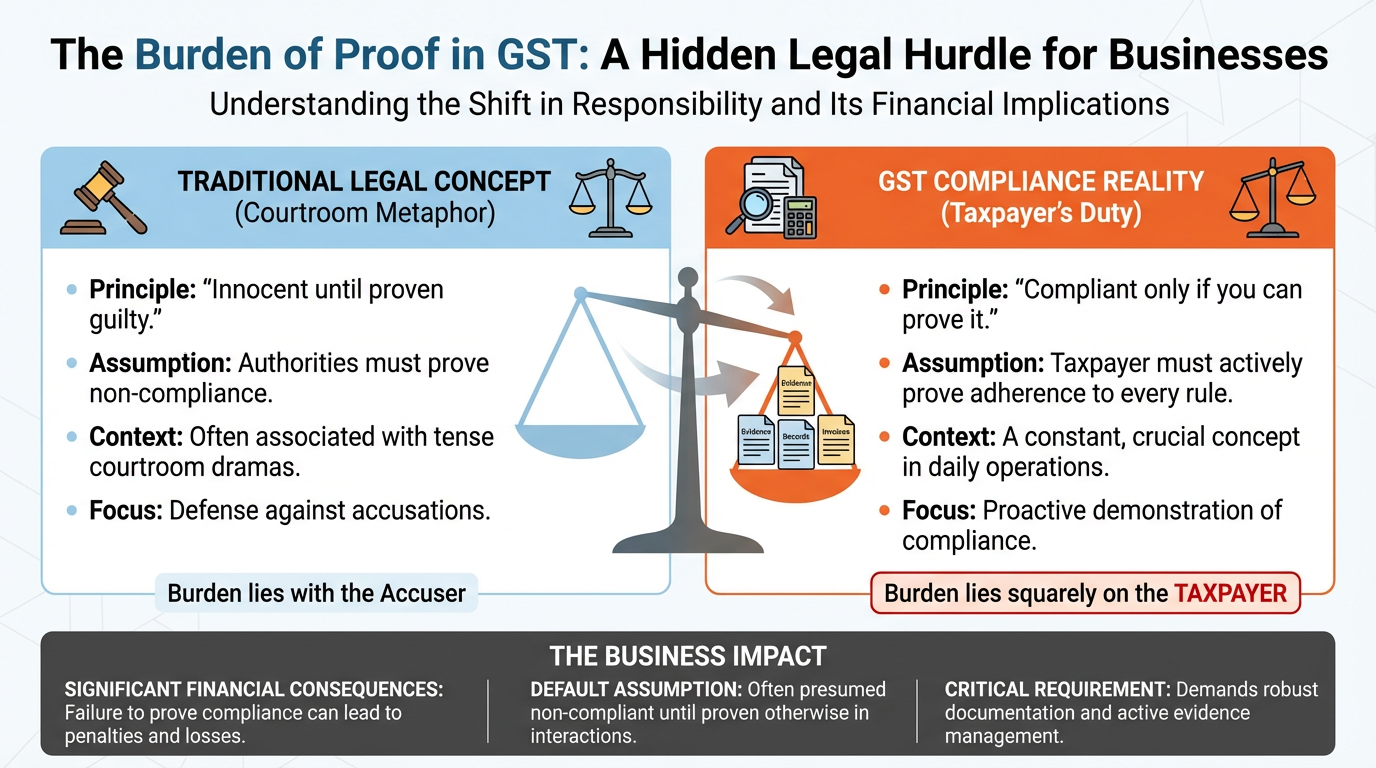

The phrase "burden of proof" might bring to mind tense courtroom dramas, but it's a crucial and constant concept in the world of Goods and Services Tax (GST) that falls directly on the taxpayer. It represents a hidden legal hurdle that every business owner must understand. In many interactions with tax authorities, the default assumption is not that they must prove you are non-compliant, but that you must actively prove you have followed every rule. In the world of GST, the principle is not 'innocent until proven guilty,' but rather 'compliant only if you can prove it.' This shift in responsibility can have significant financial consequences.

Here, we uncover three critical areas where this reversed burden of proof can create significant financial risk—and where proactive compliance can save your business.

.png)

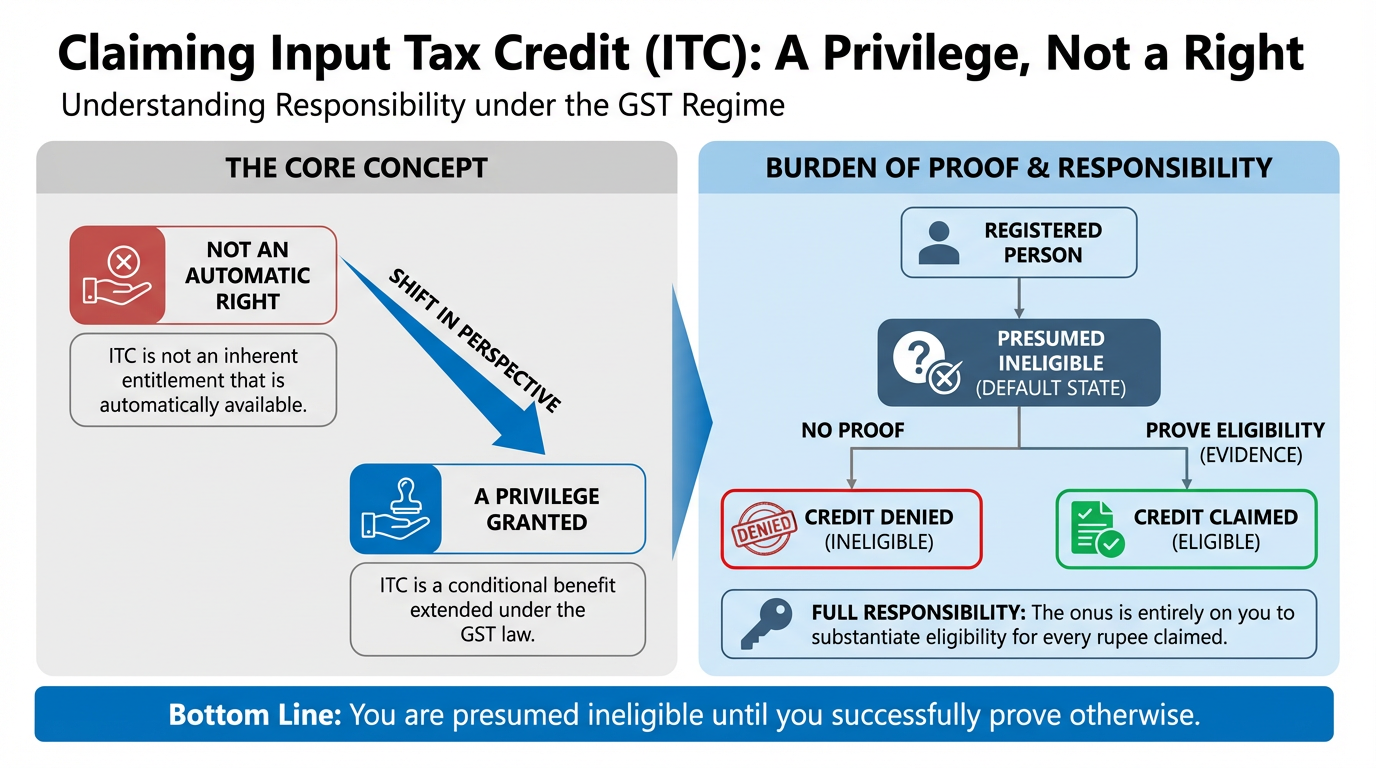

1. That Input Tax Credit You Claimed? You Have to Prove You Deserve It.

Claiming Input Tax Credit (ITC) is a privilege granted under the GST regime, not an automatic right. The law places the full responsibility on the registered person to prove their eligibility for every rupee of credit claimed. Simply put, you are presumed ineligible until you can prove otherwise.

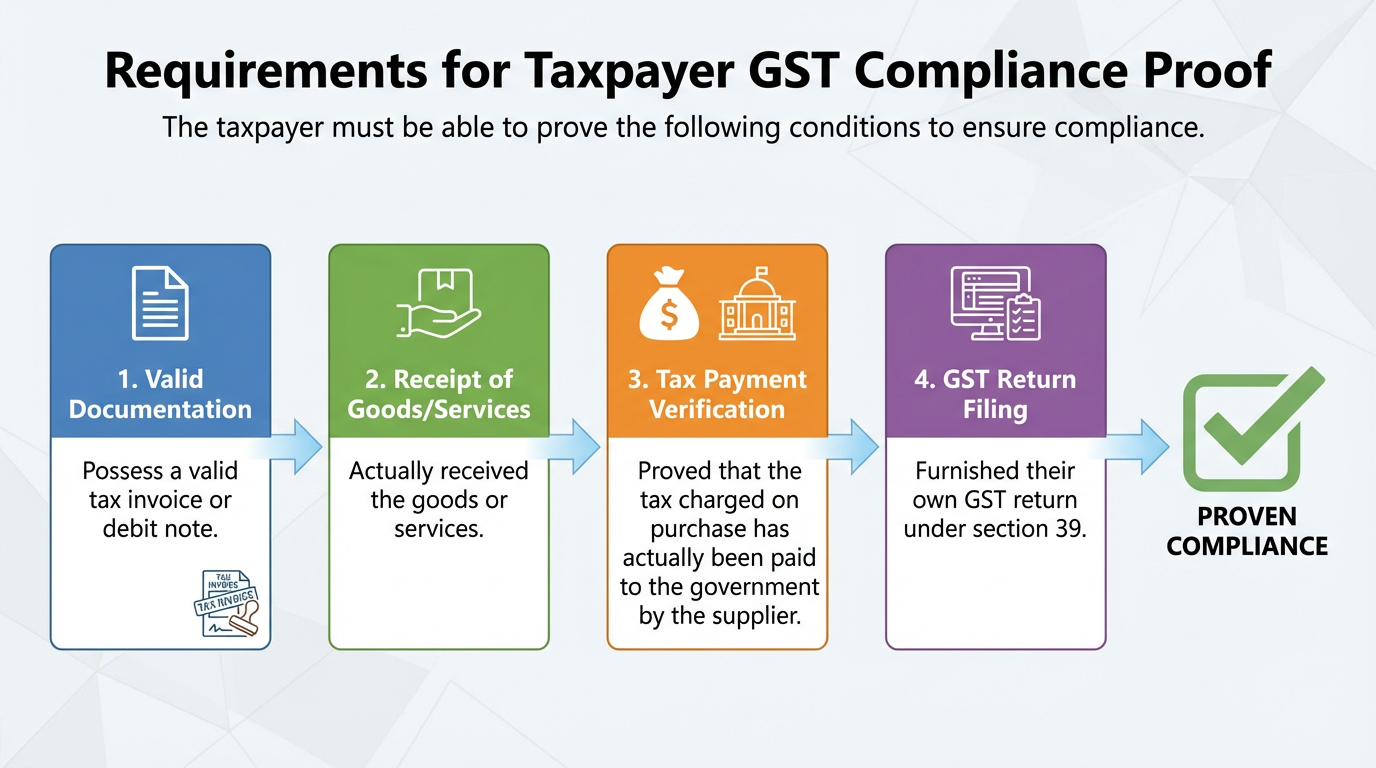

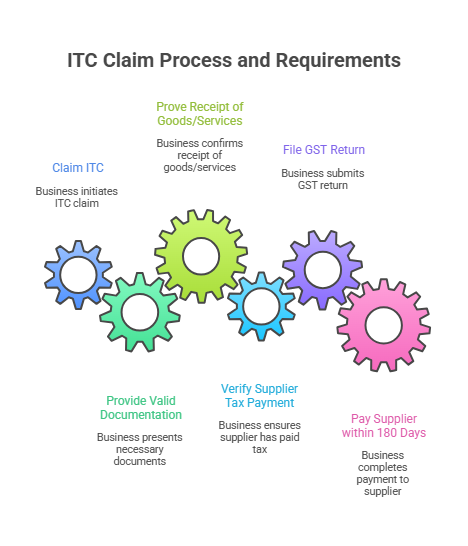

To successfully claim ITC, a business must possess valid documentation and demonstrate that all conditions under Section 16 of the CGST Act have been meticulously met.

The taxpayer must be able to prove they have:

• A valid tax invoice or debit note.

• Actually received the goods or services.

• Proved that the tax charged on your purchase has actually been paid to the government by the supplier.

• Furnished their own GST return under section 39.

That third condition is a notorious business pain point. Proving your supplier has actually remitted the tax to the government is exceptionally difficult and puts your business entirely at the mercy of their compliance. A default by your vendor can directly lead to the denial of your ITC, making robust vendor-vetting and diligent follow-up processes essential risk management tools.

One of the most counter-intuitive rules is the requirement to pay your supplier within 180 days (second proviso to Section 16(2), operationalised by Rule 37). If your business fails to make payment for an invoice within this period, the burden is on you to reverse the ITC you already claimed. This means paying the credit back to the government, along with interest. This provision effectively makes the government a stakeholder in your business's accounts payable cycle, creating a direct tax consequence for delayed supplier payments and underscoring the necessity of diligent record-keeping.

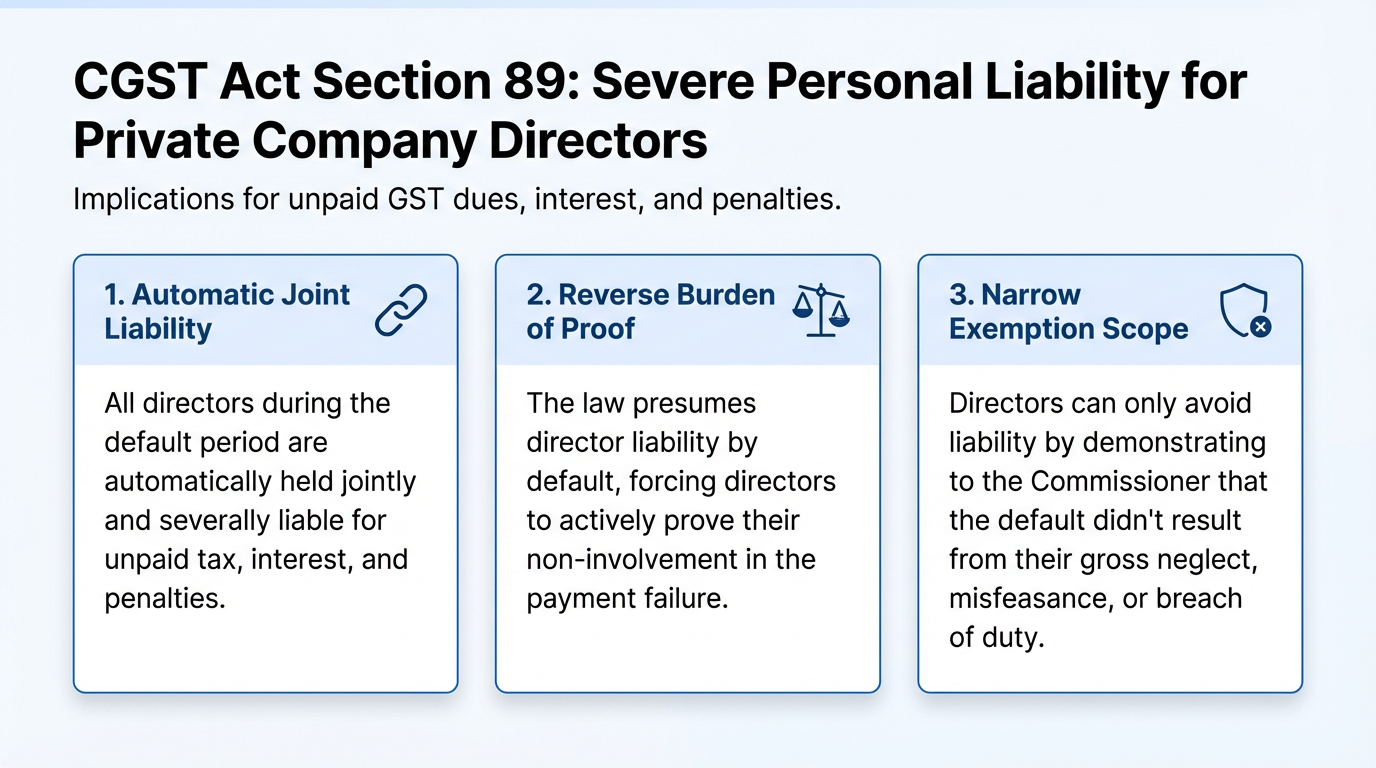

2. As a Director, You're Liable by Default—Unless You Can Prove Your Innocence.

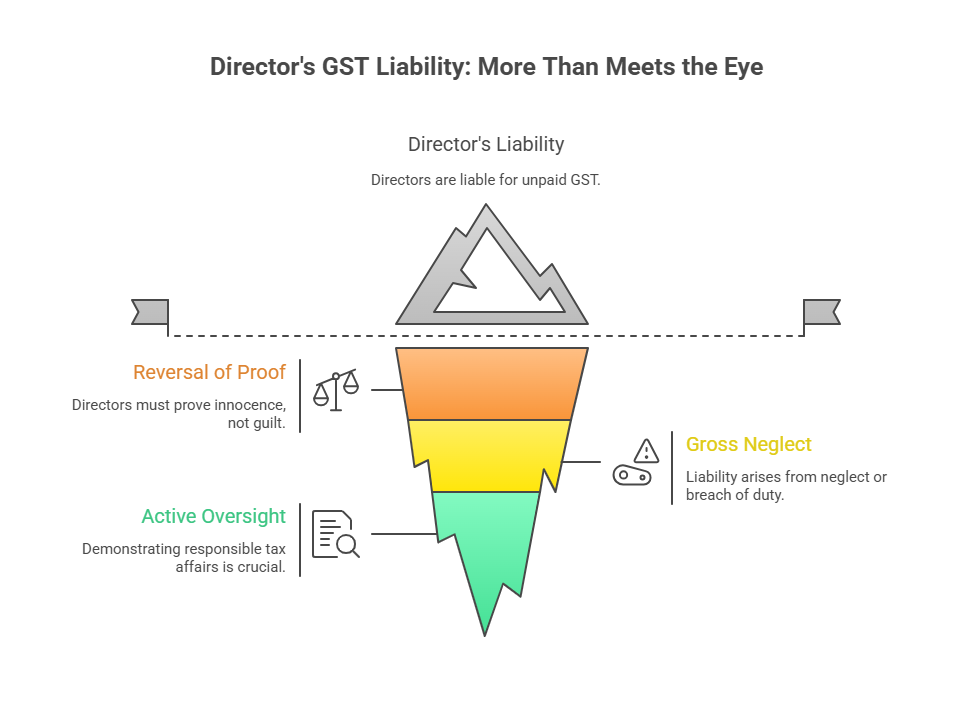

For leaders of private companies, Section 89 of the CGST Act contains a shocking and often overlooked provision. It states that when a private company fails to pay its GST dues, every person who was a director during that period is "jointly and severally" liable for the company's unpaid tax, interest, or penalty.

The most critical aspect of this rule is the complete reversal of the burden of proof. The law presumes every director is personally liable by default. The only way for a director to escape this significant financial risk is to actively prove to the Commissioner that the company's failure to pay was not a result of their own "gross neglect, misfeasance or breach of duty".

This is a powerful legal position for the tax authorities. In a dispute over unpaid taxes, a director does not have to be proven guilty; they are tasked with proving themselves innocent. It highlights a profound personal risk for company leaders and places a premium on demonstrating active and responsible oversight of the company's tax affairs.

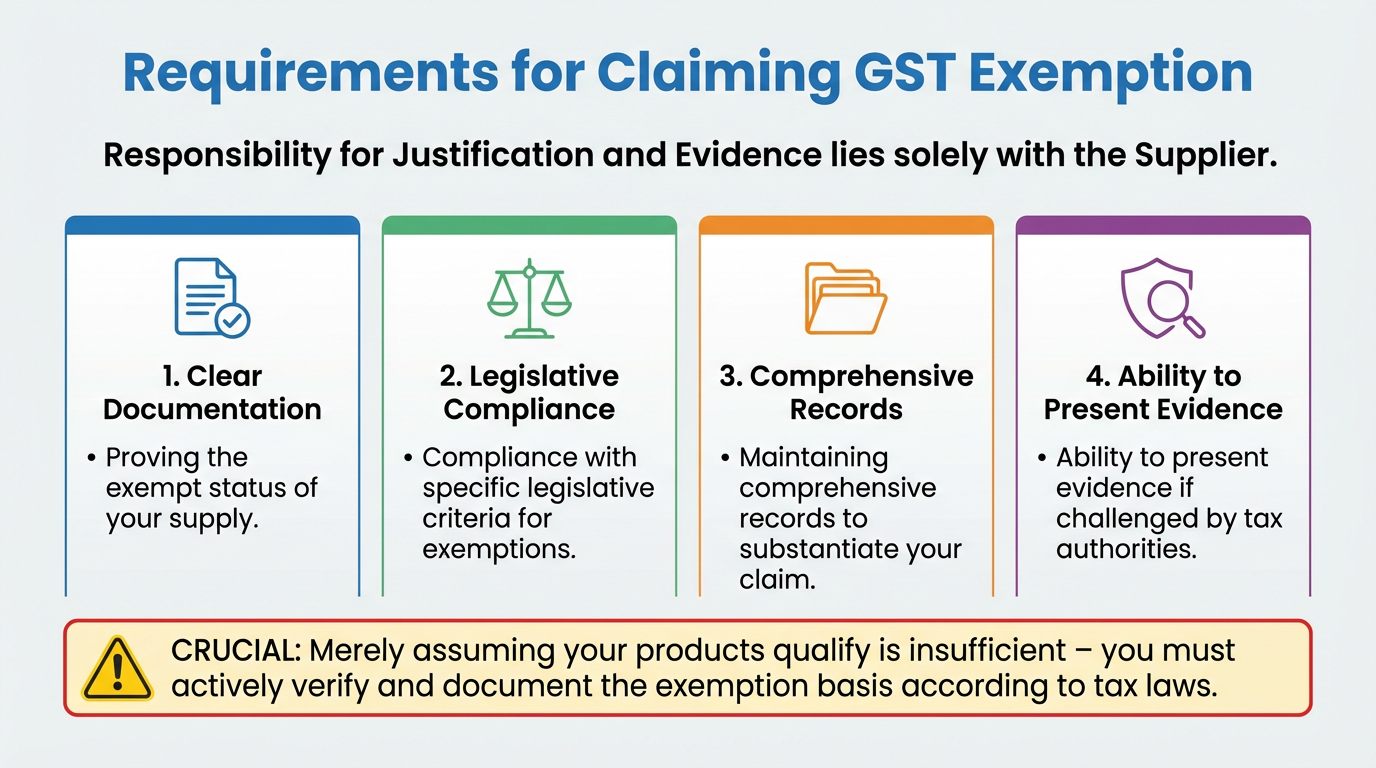

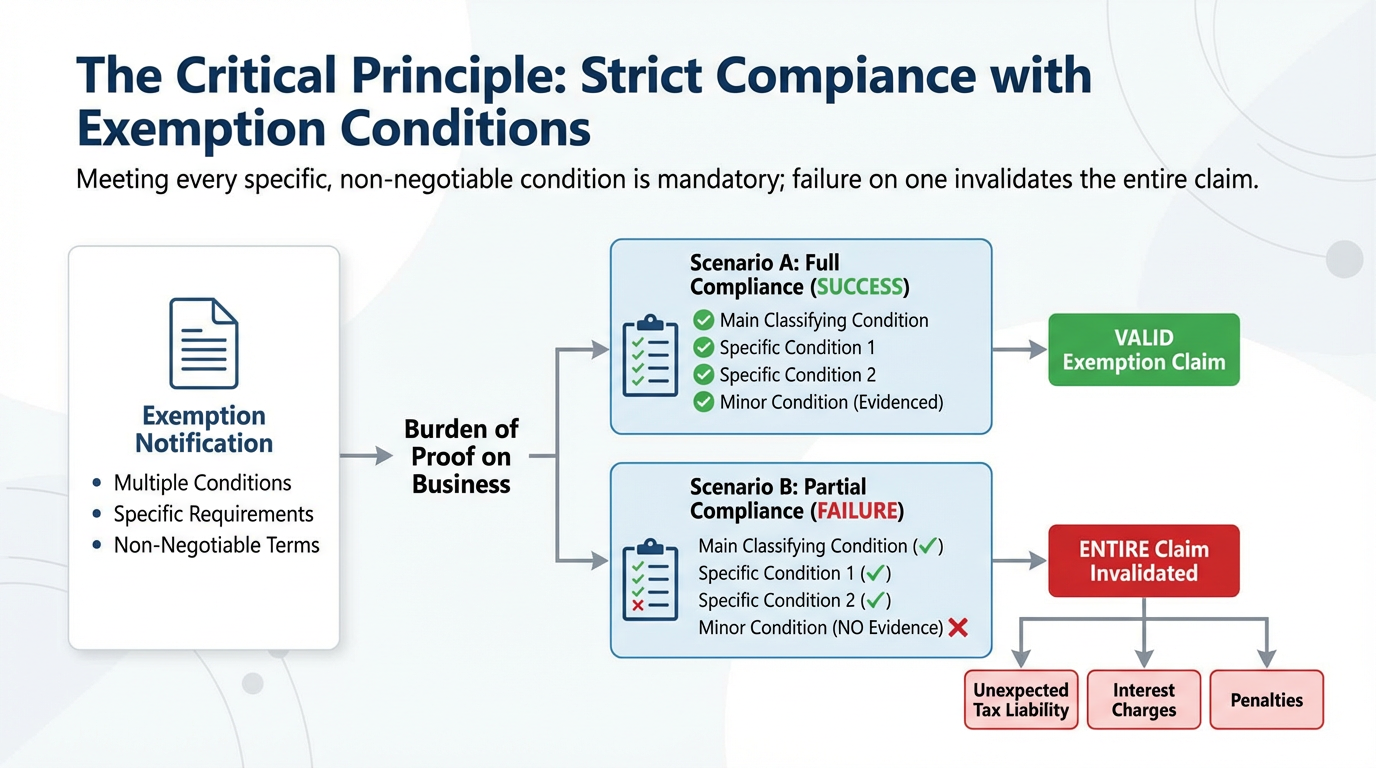

3. Want to Claim an Exemption? The Onus Is on You to Justify It.

Operating under the belief that your goods or services are exempt from GST is not a sufficient defence if challenged by tax authorities. The burden of proving that a supply qualifies for an exemption rests entirely on the taxpayer who makes that claim.

If your claim is questioned, your business must be prepared to provide clear and convincing evidence that it meets every single condition required for that specific exemption. This principle is fundamental to tax administration, as exemptions are considered a deviation from the standard rule of taxation. The source text puts it plainly:

Note: Applicability of exemption is a burden of taxpayer to demonstrate eligibility to any exemption and satisfaction of all conditions attendant to such classification.

This principle is critical because exemption notifications often contain multiple, specific, and non-negotiable conditions. The burden is on the business to prove it has met every single one, not just the main classifying condition. Failure to provide evidence for even one minor condition can invalidate the entire exemption claim, leading to unexpected tax liability, interest, and penalties.

Conclusion: Are Your Records Ready for the Challenge?

From claiming credits and justifying exemptions to the personal liabilities of directors, a central theme emerges in the GST framework: the taxpayer must be constantly prepared to prove their compliance. The system is not built on the principle of "innocent until proven guilty," but rather on "compliant if you can prove it." This reality demands a proactive and meticulous approach to tax management. Are your records and processes truly ready to stand up to that challenge?

GST Anti Evasion Department Powers | Powers of GST Officers | DRC-01 | Statement of Facts and Grounds of Appeal Format GST | Valuation Rules Under GST

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified