1. Introduction

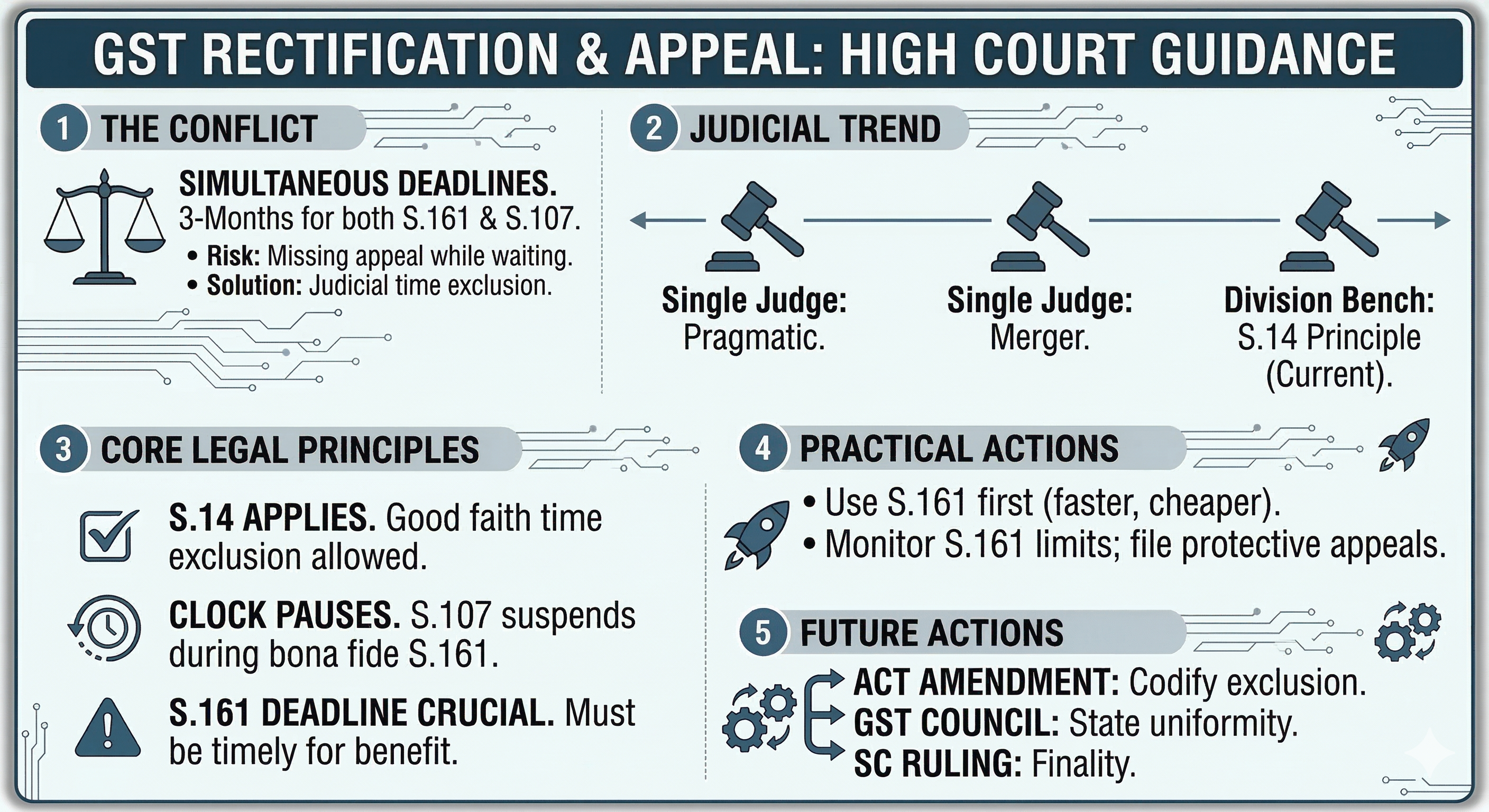

A recurring and practically significant question in GST litigation is whether the time spent by an assessee in pursuing a rectification application under Section 161 of the CGST/SGST Act should be excluded while computing the limitation period for filing a first appeal under Section 107. The statutory scheme creates a tension: the same three-month window governs both the right to seek rectification and the right to appeal. An assessee who bona fide files a rectification application first—hoping for a simpler resolution—often finds that by the time the rectification is rejected, the appeal period has already lapsed.

This article analyses four recent High Court decisions that have addressed this issue, culminating in a Division Bench ruling of the Allahabad High Court that has substantially settled the legal position. The judgments are: Prakash Medical Stores v. Union of India (2026) 38 Centax 190 (All.); Vyas Traders v. Additional Commissioner (2026) 39 Centax 325 (All.); M/s. SPK and Co. v. State Tax Officer (2024) 25 Centax 410 (Mad.); and Tvl. SKL Exports v. Deputy Commissioner W.P. Nos. 6825, 6828 & 6829 of 2024 (Mad.).

2. The Core Legal Issue

Section 107(1) of the CGST Act prescribes a three-month limitation period for filing a first appeal, extendable by only one further month under Section 107(4) upon showing sufficient cause. Section 161 independently permits rectification of errors apparent on the face of the record within three months of the order. Both limitation periods start running simultaneously from the date of the original order.

The difficulty arises because the CGST Act contains no express provision for excluding the period spent on rectification from the appeal limitation. Unlike the Limitation Act, 1963, which applies to court proceedings, the CGST Act governs proceedings before quasi-judicial authorities, and the general provisions of the Limitation Act (including Section 5 for condonation and Section 14 for exclusion of time) do not apply in terms. The Supreme Court in Commissioner v. Hongo India (P.) Ltd. and Glaxo Smith Kline Consumer Health Care Ltd. had already settled that Section 5 of the Limitation Act is impliedly excluded by the self-contained condonation scheme in pari materia statutes. The live question was whether Section 14’s underlying principle—as distinct from its literal text—could still be invoked.

3. The Judicial Response: A Case-by-Case Analysis

3.1 Tvl. SKL Exports (Madras HC, March 2024)

This was among the earliest cases to confront the issue under GST. The assessments against SKL Exports were framed in September–October 2023. The assessee filed rectification petitions, which were rejected on 29 January 2024. Appeals were then filed, but were dismissed as time-barred since they fell 21 to 24 days beyond the condonable period. Justice Senthilkumar Ramamoorthy took a pragmatic approach: noting that the assessee had already deposited 10% of the disputed tax and that a further sum of over Rs. 1.26 crore had been appropriated from its bank account, the Court quashed the appellate orders and directed the appellate authority to hear the appeals on merits without going into limitation. While the order did not engage in a detailed doctrinal analysis, it signalled judicial discomfort with the practical injustice caused by the limitation trap.

3.2 M/s. SPK and Co. (Madras HC, November 2024)

Justice K. Kumaresh Babu of the Madras High Court addressed the issue more directly. The original assessment was passed on 7 August 2024 and the rectification application was rejected on 12 November 2024. The assessee apprehended that the appellate authority would compute limitation from the original assessment date, rendering any appeal time-barred.

The Court introduced the concept of merger: when a rectification application is filed under Section 161, the order of rectification (whether it grants or rejects the application) merges into the original order. Therefore, the limitation for challenging the original assessment should start from the date of the rectification order, not from the date of the original assessment. This approach effectively sidestepped the Section 14 debate by recharacterising the starting point of limitation itself.

3.3 Prakash Medical Stores (Allahabad HC, Division Bench, December 2025)

This is the most doctrinally significant of the four judgments. A Division Bench of Justices Saumitra Dayal Singh and Vivek Saran undertook an exhaustive analysis of the Supreme Court’s jurisprudence on the interplay between special limitation statutes and the Limitation Act.

Key Facts: The ex-parte adjudication order under Section 73 was dated 23 April 2024, creating a demand of approximately Rs. 16.46 lakh (tax, interest, and penalty). The assessee filed a rectification application under Section 161 on 23 May 2024 (one month and one day after the order). This was rejected on 22 October 2024. The appeal under Section 107 was filed on 29 November 2024—within one month and eight days of the rectification rejection, but well beyond four months of the original order.

The Court’s Reasoning: The Division Bench drew a critical distinction between Section 5 and Section 14 of the Limitation Act. While Section 5 (condonation of delay) is impliedly excluded by the self-contained scheme of Section 107(1) read with 107(4), the underlying principle of Section 14 (exclusion of time spent in bona fide proceedings before a wrong forum or forum unable to entertain the matter) is not excluded. The Court relied squarely on the Supreme Court’s ruling in M.P. Steel Corporation v. CCE (2015), which held that Section 14’s principle applies even to quasi-judicial proceedings under special statutes and must be interpreted extremely liberally because it furthers the cause of justice.

The Core Holding: The filing of a rectification application under Section 161, if made within the prescribed time and pursued bona fide, puts the limitation for filing an appeal under Section 107 in abeyance from the date of filing till the date of disposal of the rectification application. The only exception is where the rectification application itself is filed beyond the limitation prescribed under Section 161. On the facts, since the appeal was filed within two months and nine days of the original order (after excluding the rectification period), it was within the three-month limitation.

3.4 Vyas Traders (Allahabad HC, February 2026)

Justice Vikas Budhwar applied the Prakash Medical Stores ratio to two consolidated writ petitions involving distinct factual scenarios.

Leading Petition (Writ Tax No. 1054/2025): Vyas Traders received a Section 73 order on 22 April 2024 imposing a demand of approximately Rs. 50.76 lakh. It filed a rectification application on 7 May 2024, which was rejected on 18 September 2024. The appeal filed on 28 September 2024 was rejected as time-barred on 27 October 2024. Following Prakash Medical Stores, the Court held the appeal was within limitation after excluding the rectification period.

Connected Petition (Writ Tax No. 2897/2025): This involved an interception and seizure case where a penalty of Rs. 48.58 lakh was imposed under Section 129 via Form GST MOV-09. The assessee had initially challenged the penalty by way of a writ petition, which was dismissed as withdrawn with liberty to file an appeal. The appeal filed thereafter was rejected as time-barred. The Court applied Section 14 of the Limitation Act to exclude the period spent in the writ proceedings, holding that the assessee was prosecuting its remedy bona fide before a wrong forum.

4. Synthesis: The Emerging Legal Framework

| Judgment | Court / Bench | Legal Basis | Outcome |

| SKL Exports (Mar 2024) | Madras HC, Single Judge | Pragmatic / equitable (no detailed doctrinal reasoning) | Appeals restored on merits |

| SPK and Co. (Nov 2024) | Madras HC, Single Judge | Merger doctrine: rectification order merges into original; limitation runs from rectification date | Limitation starts from rectification rejection date |

| Prakash Medical Stores (Dec 2025) | Allahabad HC, Division Bench | Underlying principle of S.14 Limitation Act; limitation in abeyance during rectification pendency | Rectification period excluded; appeal within time |

| Vyas Traders (Feb 2026) | Allahabad HC, Single Judge | Follows Prakash Medical Stores; also applies S.14 to writ proceedings before wrong forum | Both appeals restored on merits |

Three propositions can now be distilled from these decisions:

First, while Section 5 of the Limitation Act is impliedly excluded by the self-contained condonation framework of Section 107(4), the underlying principle of Section 14 is not excluded. The two provisions serve fundamentally different purposes: Section 5 extends time, while Section 14 excludes time spent in bona fide proceedings, leaving the original limitation period intact.

Second, when an assessee files a rectification application under Section 161 within time and pursues it bona fide, the appeal limitation under Section 107 is placed in abeyance for the duration of the rectification proceedings. This means the assessee gets the full benefit of the remaining limitation period after the rectification application is disposed of.

Third, the benefit does not arise if the rectification application itself was filed beyond the period prescribed under Section 161. The principle rewards diligence, not delay.

5. Practical Implications for Assessees and Practitioners

The immediate practical consequence of this jurisprudence is that assessees who receive adverse orders under Sections 73, 74, or 129 of the CGST Act are no longer forced into an either-or choice between rectification and appeal. They can pursue rectification first—which is often a faster, less expensive remedy—without sacrificing their right to appeal if rectification fails.

However, practitioners must exercise caution. The protection is available only if the rectification application is filed within the limitation prescribed under Section 161 (three months from the order, with an outer limit of six months for disposal by the authority). If the rectification application is itself time-barred, the principle of Section 14 will not rescue the appeal. Furthermore, while the Allahabad Division Bench has laid down the law with considerable authority, the position is not yet settled by the Supreme Court, and appellate authorities in other states may initially resist applying it. Assessees should therefore continue to file protective appeals within time wherever possible, or at minimum preserve a clear record of the rectification filing date and its bona fide nature.

6. The Way Forward

The current judicial consensus points strongly in favour of assessee protection, but the legal landscape would benefit from further clarity on three fronts.

Legislative Amendment: The cleanest solution would be a proviso to Section 107 expressly providing that the period during which a rectification application under Section 161 remains pending shall be excluded from the computation of the limitation period for appeal. This would eliminate litigation on the point entirely and align the statutory text with judicial interpretation.

GST Council Recommendation: Pending legislative amendment, the GST Council could issue a clarificatory circular directing appellate authorities to exclude the rectification period while computing appeal limitation. This would ensure uniform application across states and reduce the need for High Court intervention in individual cases.

Supreme Court Adjudication: If the Revenue challenges any of these High Court rulings, a Supreme Court pronouncement would settle the position conclusively. Given the unanimity among the High Courts that have considered the issue, an affirmation seems likely, though the Court may also refine the doctrinal basis—choosing between the Madras High Court’s merger theory and the Allahabad High Court’s Section 14 abeyance principle.

7. Conclusion

The judgments in SKL Exports, SPK and Co., Prakash Medical Stores, and Vyas Traders represent a welcome and principled intervention by the High Courts to remedy a structural gap in the GST statute. The law now clearly recognises that an assessee who diligently pursues rectification before filing an appeal should not be penalised by the efflux of time during the rectification proceedings. The underlying principle of Section 14 of the Limitation Act—that the law assists the vigilant, not the indolent—has been given full effect in the GST context. Until the legislature acts to codify this position, these judgments provide a robust shield for assessees navigating the limitation minefield under the CGST Act.

Need of GST in India | Powers of GST Officers | GST Audit Procedure | GST Audit Procedure | GST penalty under section 74

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified