Form 10-IA

Form 10IA of Income Tax Act, taxpayers can claim several deductions from their total income. Every deduction has specific criteria to be met. Deductions under section 80DD and 80U can be claimed if any medical expenditure has been incurred for the treatment of a differently-abled person. To claim deduction under either of the sections, the taxpayer has to obtain and submit a certificate in the prescribed manner as mentioned in Form 10IA for 80DD. In this article, we will discuss the elements below:

Who Should Submit Form 10-IA?

An Individual/Hindu Undivided Family claiming deduction u/s 80DD/80U should furnish a copy of the certificate issued by the medical authority in Form 10IA along with his/her/their Income Tax Return.

In Which Situation Can Form 10-IA be Furnished?

Form 10 IA has to be furnished when deduction u/s section 80DD/80U is claimed. These sections cover expenses incurred to treat a dependent person (or self) with a disability/severe disability subject to pre-defined conditions. The deduction is available only when the person has autism, cerebral palsy or multiple disabilities, and the same is certified by:

- A Neurologist having a degree of Doctor of Medicine (MD) in Neurology (in case of children, a Paediatric Neurologist having an equivalent degree); or

- A Civil Surgeon or Chief Medical Officer in a Government hospital.

Note: When the condition of disability is temporary and requires reassessment after a specified period, the certificate in Form no. 10-IA shall be valid for the period starting from the assessment year relevant to the previous year during which the certificate was issued and ending with the assessment year relevant to the previous year during which the Form 10 IA validity of the certificate expires.

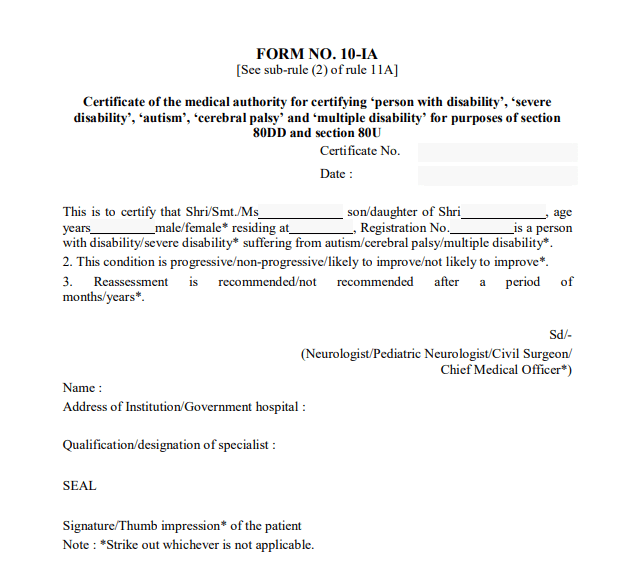

Format of Form 10-IA

The below image is sample of form no 10-1a word format:

This form can be downloaded here. The above image is Form 10-IA filled sample.To fill the form, you have to fill all the details required in the above form. If you don't know about what is registration number in form 10ia, so you should get the details regarding the same.

Points to Remember

- Under section 80DD/80U, a taxpayer can claim INR 75,000 as a flat deduction (for dependents/self with a disability). However, in case the taxpayer is supporting himself/herself/dependent with severe disability (80% disability), the quantum of the deduction is raised to INR 1,25,000.

- Deduction u/s 80DD is allowed for the expenses incurred for a dependant of the taxpayer and not for the taxpayer himself/herself.

- As per the Income Tax Rules, the definition of dependent person includes the spouse, children, parents, brothers and sisters of the taxpayer or members of the HUF.

Need of GST In Points | GST Invoice Series Rules | Powers of Revisional Authority Under GST | Kaju GST Rate | Maintenance GST Rate

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified