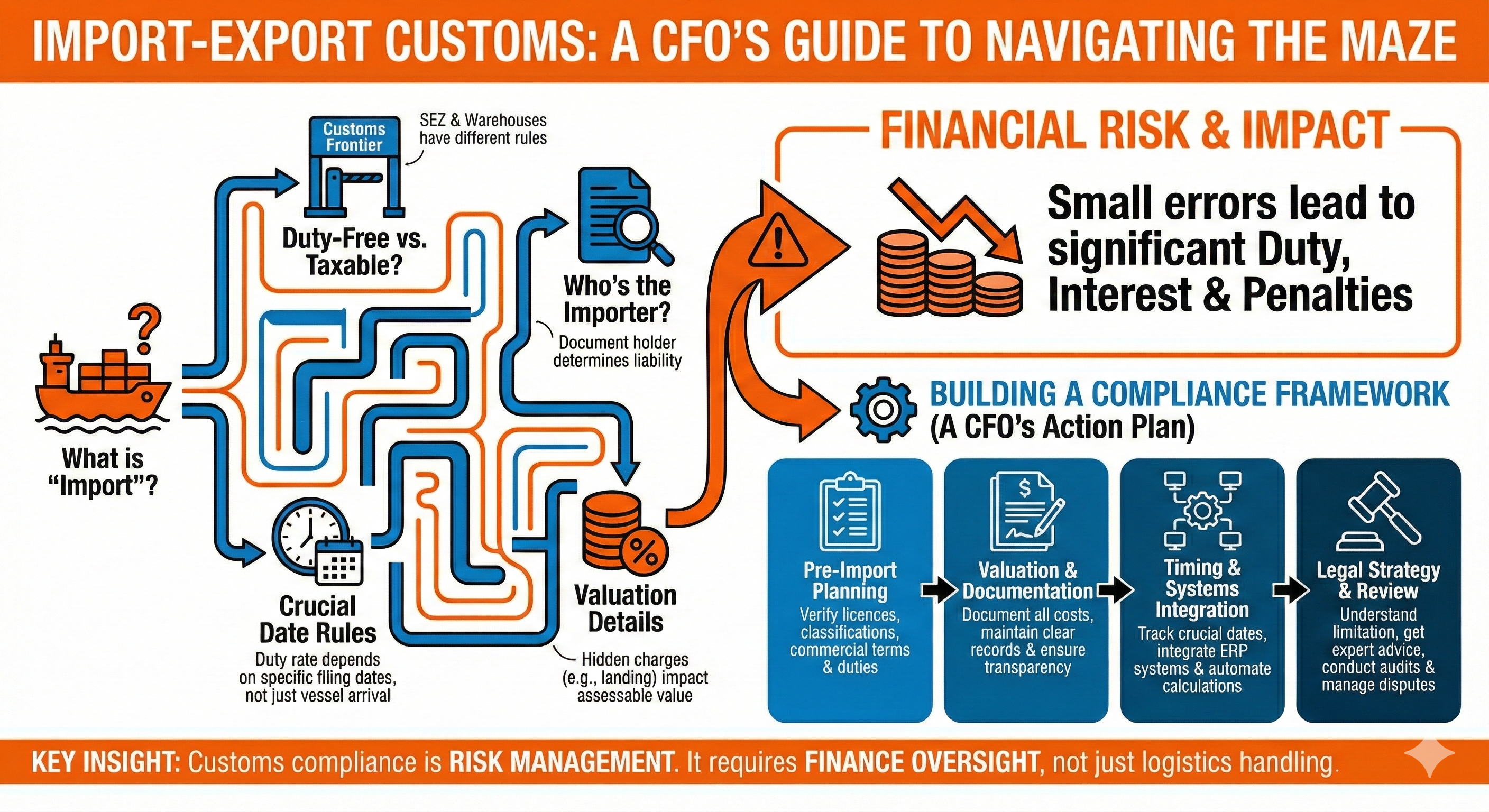

Why This Matters More Than You Think

Here's a scenario that plays out in finance departments across India: Your procurement team imports machinery, files the bill of entry, and thinks the job is done. Three years later, a show cause notice arrives demanding additional duty plus interest and penalties. The trigger? The customs department discovered that certain landing charges should have been added to the assessable value—a detail buried in commercial terms that nobody flagged.

If this sounds familiar, you're not alone. Customs law in India operates through a maze of definitions, timings, and technicalities that can trip up even experienced finance teams. The difference between "when goods enter territorial waters" and "when the bill of entry is filed" might seem academic, but it can determine whether you pay duty at 10% or 15%. That difference, multiplied across your annual imports, becomes material very quickly.

This article walks through the key judicial principles that govern import and export operations. We'll look at landmark cases that have shaped how customs law actually works—not just what the statute books say—and then build a practical compliance framework you can adapt for your organisation.

What "Import" Actually Means (It's Not What You'd Expect)

You'd think "import" simply means bringing goods into India. And legally, that's exactly what Section 2(23) of the Customs Act says: bringing goods into India from a place outside India. But decades of litigation have shown this definition hides more than it reveals.

Consider the K.R. Ahmed Shah case decided by the Madras High Court (reported in 1981 (8) ELT 153). A passenger arrived with baggage, made a complete declaration under Section 77, and then requested under Section 80 that the goods be detained for re-export. The court held this wasn't really an "import" at all—because import involves not just physical entry but also the intention to bring goods into the mass of goods within India. The passenger's request for re-export demonstrated the absence of this intent.

Now look at Shri Ramlinga Mills Private Ltd. vs Assistant Collector of Customs (Kerala High Court, 1983 (12) ELT 65). Here's what happened: a vessel carrying goods meant for Cochin stopped at Bombay as an intermediate port. The customs department tried to treat this as an import at Bombay. The Kerala High Court firmly rejected this approach, holding that mere entry into territorial waters or berthing at an intermediate port doesn't constitute import vis-à-vis the actual importers at the final destination. Import is destination-specific.

But the Madras High Court added another layer in Md. Ibrahim vs Secretary, Ministry of Finance (2000 (123) ELT 239). A passenger was found with diamonds hidden in his watch strap. His defence? These were personal items for constant wearing. The court wasn't persuaded. Articles brought from outside India constitute import regardless of whether they're for personal use. The nature of use doesn't change the character of importation.

What do these cases tell us? Import is a composite concept. It's about physical entry, yes. But it's also about intention, destination, and completion at a specific location. The practical takeaway: you can't simply track when your vessel enters Indian waters and assume you know when import occurred. The legal fiction is more nuanced than that.

The Curious Case of the Customs Frontier

Here's where things get really interesting. When exactly do goods cross the "customs frontier" of India? This isn't just an academic question—it determines tax liability, availability of exemptions, and even which tax regime applies.

The Supreme Court's decision in Hotel Ashoka vs Asst. Commissioner of Commercial Tax (2012 (276) ELT 433) fundamentally changed how we think about this. Hotel Ashoka operated duty-free shops at international airports, sourcing goods from bonded warehouses. The state tax authorities wanted to levy sales tax on these transactions. The Supreme Court said no—and here's why.

Goods kept in bonded warehouses haven't crossed the customs frontier. They're deemed to be outside India for customs purposes. When duty-free shops sell these goods to international passengers, the sale occurs before importation into India. Therefore, it's a transaction in the course of import, exempt from sales tax under Section 5 of the Central Sales Tax Act and Article 286 of the Constitution.

The Vasu Clothing case from the Madhya Pradesh High Court (2018 (19) GSTL J73) took this principle further into the GST era. Duty-free shops argued they shouldn't pay GST because they operate beyond the customs frontier. The court issued notice asking the Board to clarify whether refunds of accumulated input credit should be available to these shops. As of this writing, that clarification remains relevant for anyone operating in this space.

But here's where it gets tricky. The Bombay High Court in Radhasons International vs Commissioner of Sales Tax (2023 (7) Centax 550) distinguished between customs "barriers" and customs "frontiers" for Central Sales Tax purposes. Goods in bonded warehouses were held to have crossed the customs frontier under CST law, even though they hadn't crossed customs barriers under the Customs Act.

Think about what this dual characterisation means for your operations. You might be maintaining a bonded warehouse, thinking goods are "outside India" for all purposes. They are—for customs duty. But for other taxes, particularly CST and potentially GST, the treatment differs. You need a separate analysis for each tax statute. There's no single, definitive answer to "Are these goods in India or not?"

Who's the Importer? (It Matters More Than You Think)

The question "who is the importer?" sounds straightforward until you're three years into litigation about it. The legal answer determines who bears duty liability, who can claim refunds, who gets penalized for violations—everything.

JB Trading Corporation vs Union of India (Madras High Court, 1990 (45) ELT 9) established a critical principle: between the date of importation and clearance for home consumption, whoever holds themselves out to be the importer is the importer. This case involved a situation where the original importer firm was found to be fictitious and the licence allegedly obtained by fraud. Another party tried to substitute itself as the importer after importation was complete. The court said no—you can't change horses midstream like this.

The Gipoint Development case from the Madras High Court (1995 (80) ELT 55) added a documentary dimension. When customs authorities seized import documents from a bank, the court held that the bank became the "owner" of the goods, not the foreign supplier. The principle: whoever holds the documents is the owner for customs purposes.

This became even more explicit in Sun Export Corporation vs Board of Trustees (Supreme Court, 1997 (96) ELT 3). The case involved endorsement of a bill of lading. The Supreme Court held that such endorsement transfers all rights from the original consignee to the endorsee. For customs purposes, the endorsee becomes the consignee and is obligated to clear the goods.

The practical implication? Your documentation determines your liability. If you're engaging in high-sea sales, make sure the endorsements happen before the vessel arrives. If you're financing imports through banks, understand that the bank holding the documents might be treated as the importer. And if you're using a front company that later proves fictitious, don't assume you can simply step in and take over—the courts won't let you cherry-pick when to be the importer.

Valuation: The Devil in the Details

Custom valuation might seem like a technical exercise, but I've seen companies face million-rupee demands because nobody properly analysed what should be included in assessable value.

Garden Silk Mills Ltd. vs Union of India (Supreme Court, 1999 (113) ELT 358) remains the leading case on landing charges. The principle is actually quite logical once you understand it: landing charges imposed after discharge from the vessel but before clearance must be included in the assessable value—unless the seller or their agent is already obligated to bear these charges as part of the CIF value.

Let me give you a practical example. Your contract says CIF Mumbai. The seller pays for cost, insurance, and freight to Mumbai. The vessel arrives, goods are discharged. Now there are landing charges—stevedoring, handling, etc. Do you add these to the CIF value for customs purposes? Yes, you do—because these charges are imposed on you, the importer, after discharge. The seller's CIF obligation ended when the goods reached the vessel's side at the destination port.

But if your contract specifically states "CIF Mumbai including landing charges" and the seller actually bears these costs, then you don't add them again. The key is documenting who actually bears the obligation.

The Supreme Court's decision in Udyani Ship Breakers Ltd. (2006 (195) ELT 3) addressed another common scenario. A ship was imported for breaking and later sold to a domestic purchaser at a reduced price. The purchaser argued that the lower domestic sale price should determine customs value. The Supreme Court disagreed. The transaction value is what was paid during international trade—the price paid when the letter of credit was opened and money remitted to the foreign seller. What you do with the goods after import doesn't retroactively change their import value.

The lesson here: maintain clear documentation of your commercial terms. Know exactly what's included in FOB, CIF, or whatever Incoterm you're using. Separately identify every cost element. And don't assume that subsequent events (like resale at a lower price) will somehow benefit your customs valuation.

Timing Is Everything: The Crucial Date Rules

If there's one area where CFOs consistently get surprised, it's the rules about which date determines the applicable duty rate. You'd think it's when the goods arrive. It's not.

Union of India vs Apar Pvt Ltd. (Supreme Court, 1999 (112) ELT 3) settled this issue definitively. The crucial date is determined by Section 15(1) of the Customs Act:

For goods cleared for home consumption: the date you file the bill of entry under Section 46, or the date when entry inwards is granted to the vessel—whichever is later.

For goods removed from a bonded warehouse: the date of actual removal from the warehouse.

Notably, the date when the vessel entered territorial waters is irrelevant. This is counter-intuitive but critical to understand.

Sundaram Textiles vs ACC (Imports) (Madras High Court, 1989 (44) ELT 464) involved viscose staple fibre yarn that was wholly exempt from customs duty under notifications valid until 31st December 1978. New notifications were issued on 5th January 1979 with different rates. The question: were the goods unloaded on 4th January or 5th January? That one day determined whether the old exemptions applied. The court held that the relevant date is the date of unloading for purposes of applying the exemption notifications.

Now consider Amber Woollen Mills (Supreme Court, 1998 (102) ELT 518). Goods arrived at Bombay port on 10th February 1987 and were transhipped to Delhi ICD, arriving there on 8th and 11th March. The bills of entry for home consumption were filed at Delhi on 26th February. Which date governs duty rates? The Supreme Court held: 26th February—the date of filing the bill of entry—because entry inwards had already been granted to the vessel at Bombay.

There's also Kattar Enterprises (Supreme Court, 1997 (94) ELT 454), which addressed a warehousing-to-home-consumption conversion. The importer initially filed a warehousing bill of entry on 9th October 1986, then requested it be converted to a home consumption bill of entry. This conversion happened on 23rd October. The Supreme Court held that the duty rate as on 23rd October applied—the date when the bill was re-noted as home consumption.

Here's the strategic insight: you have some control over timing through when you file your bills of entry. If duty rates are about to change, expedite or delay your filing accordingly. But don't cut it too close—if entry inwards to the vessel happens later than your bill filing, that later date prevails.

For ocean-going vessels being broken up, the Supreme Court in Jalyan Udyog (1993 (68) ELT 9) held that the date of breaking determines applicable rates and valuation. So the timing rules vary by type of import.

The Countervailing Duty Puzzle

Additional Customs Duty—or CVD—is meant to ensure imported goods bear the same excise duty burden as domestically manufactured goods. But the case law around CVD has created a framework that's more complex than the basic concept suggests.

Hyderabad Industries Ltd. vs Union of India (Supreme Court, 1999 (108) ELT 321) is mandatory reading. The court clarified that basic customs duty is charged under Section 12 of the Customs Act read with the Customs Tariff Act. But CVD has a different charging provision: Section 3 of the Customs Tariff Act. These are separate, independent statutes.

Here's the key principle: the phrase "if produced or manufactured in India" in Section 3(1) doesn't mean the article must actually be produced in India right now. If an imported article is something that has been manufactured or produced (i.e., it's a manufactured article), then it must be presumed that such articles can likewise be manufactured in India. The test is capability of manufacture, not actual current manufacture.

However—and this is the flip side—if an article cannot be subjected to excise levy because it's not the kind of thing that gets produced or manufactured, then no CVD can be levied on importing similar articles.

Delhi Cloth & General Mills (Supreme Court, 1996 (87) ELT 339) involved tyre cord grade woodpulp imported from the USA. The importer argued this specific grade wasn't produced in India and wasn't covered by any specific excise entry. The Supreme Court disagreed. Even the residuary entry (erstwhile Tariff Item 68) in the excise tariff covers a class of goods. CVD was properly leviable.

Vareli Weaves P. Ltd. (Supreme Court, 1996 (83) ELT 255) established another important principle: CVD must be levied on goods in the stage in which they are imported. What you do with them after import is irrelevant. The case involved Partially Oriented Yarn (POY). POY in the imported stage was exempt from excise duty. The customs department tried to argue that after POY is texturized, the resulting product attracts duty, so CVD should apply. The Supreme Court rejected this—you levy CVD based on the import stage, not subsequent processing.

Thermax Private Limited (Supreme Court, 1992 (61) ELT 352) gave importers some relief on the procedural side. Refrigeration equipment was imported for use in factories. The users held L-6 licences/CT-2 certificates for concessional rates. The department argued that importers couldn't benefit from these concessions because certain Chapter X procedural requirements weren't followed. The Supreme Court endorsed the Board's practical view: if the substantive condition (intended use) is satisfied, benefits shouldn't be denied merely for procedural non-compliance.

But don't get too comfortable with that principle. The Madras High Court in HLG Trading (2016 (331) ELT 561) clarified that while circulars can provide clarifications, they cannot override statutory notifications. A notification issued under statutory powers cannot be whittled down by a Board circular. So while substantive compliance might save you from procedural defects, you can't rely on circulars that contradict notification terms.

The practical approach to CVD: first, determine the exact form and stage in which you're importing. Second, check whether that same form and stage would attract excise duty if manufactured domestically. Third, identify applicable exemptions and ensure you can meet their substantive conditions. Fourth, get procedural compliance right where possible, but document substantive compliance meticulously.

Special Economic Zones: A Different World

SEZ operations create a unique customs environment that deserves separate attention. The Gujarat High Court's decision in Adani Power Limited vs Union of India (2015 (330) E.L.T. 883) fundamentally clarified how customs law applies to SEZ.

The court held that Section 30 of the SEZ Act operates independently from Section 12 of the Customs Act—they work in different fields. Section 12 of the Customs Act applies to SEZ only for the initial import of goods from outside India into the SEZ. At that point of entry into territorial waters from outside India, no customs duty is payable because of the exemption under Section 26 of the SEZ Act. Once goods enter the SEZ, the Customs Act is exhausted—it has no further role to play.

When goods move from SEZ to Domestic Tariff Area (DTA), Section 30 of the SEZ Act governs, not the Customs Act. Section 51 of the SEZ Act is an overriding provision that makes this clear.

The implication: you cannot use Customs Act principles to determine duty when goods move from SEZ to DTA. Parliament cannot levy customs duty on SEZ-to-DTA movement because that would be ultra vires Entry 83 of List I of the Seventh Schedule read with Section 12 of the Customs Act.

For CFOs managing SEZ operations, this creates a clear demarcation. Track your imports into SEZ from outside India—that's where Customs Act applies, though duty is exempt. Track your movements from SEZ to DTA—that's where SEZ Act provisions govern. Don't confuse the two regimes.

Warehousing: When Does the Barrier Actually Get Crossed?

The Supreme Court in Kiran Spinning Mills vs Collector of Customs ((2000) 10 SCC 228) addressed acrylic polyester fibre that was imported between April 1977 and September 1978, placed in a bonded warehouse, and removed after 4th October 1978. An additional duty ordinance had been promulgated on 3rd October 1978. Was the duty payable?

Yes, said the Supreme Court. The taxable event occurs when the customs barrier is crossed—not when goods land in India or enter territorial waters. For goods in a warehouse, the customs barrier is crossed when they're taken out of customs control and brought into the mass of goods in the country. This happened after the ordinance came into force, so the additional duty was properly demandable.

Shewbuxrai Onkarmall (Calcutta High Court, 1981 (8) ELT 298) reinforced this with a practical observation: a literal interpretation of "imported into India" would create absurdity. Goods might be brought by ship and re-exported without clearance. Aircraft might land with goods in transit. These situations don't constitute completed imports. Therefore, "imported into India" doesn't merely mean goods crossed into territorial waters.

For goods in bonded warehouses, duty liability crystallises when you actually remove them for home consumption. This creates planning opportunities. If duty rates are about to decrease, delay your ex-bond clearance. If rates are rising, expedite. But remember the flipside from Radhasons International—while goods in your bonded warehouse haven't crossed customs barriers for duty purposes, they may have crossed customs frontiers for other tax purposes like CST.

When Goods Go Missing: Pilferage and Loss

The treatment of goods that disappear before clearance has generated significant litigation, and the principles matter because they determine whether you pay duty on goods you never actually received.

BEML Ltd. vs Collector of Customs, Madras (2001 (129) ELT 580) established the framework. Pilferage is specifically dealt with under Section 13 of the Customs Act. Where goods are pilfered after unloading but before clearance for home consumption or warehousing, the importer has no liability for payment of duty.

The court emphasized that Section 13 must be interpreted harmoniously with Section 23. Loss by reasons other than pilferage, and goods that are destroyed (not pilfered) are dealt with under Section 23. Pilferage gets its own treatment under Section 13.

Interestingly, the 1983 amendment to Section 23 that explicitly excluded pilferage was held to be merely clarificatory. Even before the amendment, the proper interpretation was that pilferage claims go under Section 13.

But there's a significant limitation from Udyani Ship Breakers (2006 (195) ELT 3): if you don't make your remission claim under Section 22 before the Assessing Authority, you can't get remission later. The domestic purchaser in that case bought a ship after import and then tried to claim remission for damage during beaching. The Supreme Court said no—the claim should have been made by the original importer to the Assessing Authority at the right time.

Board of Trustees for Port of Bombay (2009 (241) ELT 513) created a special category for statutory custodians. Where goods were pilfered while in the Port Trust's possession as custodian, the Bombay High Court held the Port Trust wasn't liable. The "person" referred to in Section 45(1) who can be liable for duty on pilfered goods must be someone approved by the Commissioner with warehouses under Sections 9 and 10. Port Trusts possess goods under the Port Trusts Act and are statutory bodies controlled by the government—they're not approved persons and can't be notified as such.

Practical guidance: if you discover pilferage, report it immediately to customs under Section 13. Document everything—get survey reports, file police complaints, maintain photographic evidence. For damaged goods, file your remission claim under Section 22 before the Assessing Authority, not after assessment is complete. And if you're a private importer, don't assume you get the same protection as Port Trusts or other government-controlled entities.

Limitation: Your Shield Against Extended Demands

Understanding limitation periods is crucial for estimating contingent liability exposure. The normal limitation period for raising duty demands is one year from the relevant date. But the proviso to Section 28(1) allows five years in cases involving fraud or collusion or willful misstatement or suppression of facts.

Aban Loyd Chiles Offshore Ltd. (Supreme Court, 2006 (200) E.L.T. 370) tightened the conditions for invoking extended limitation. The case involved contractors carrying out drilling at offshore rigs on behalf of ONGC. Show cause notices were issued beyond the normal period for ship stores removed to the rigs.

The Supreme Court held that the extended period is invocable only where duty payment escaped "by reason of" collusion, willful misstatement, or suppression of facts. The word "willful" preceding "misstatement or suppression" clearly indicates the requirement of intent to evade duty.

Critically, the Department had full knowledge of the contractors' activities because customs officers escorted the stores. The show cause notice didn't specifically allege which omission or commission under the proviso to Section 28(1) the appellants had committed. Without being put to notice of the specific ground, the appellants couldn't meet the Department's case. Extended period was not invocable.

Compare this to Section 11A of the Central Excise Act, which explicitly mentions "fraud" and "intent to evade payment of duty." These specific words are missing from Section 28 of the Customs Act. But the court read in the requirement of willfulness from the word "wilful" modifying both misstatement and suppression.

The practical lesson: maintain complete transparency in your dealings with customs authorities. Document everything. Where officers are aware of your activities and you're operating in full view of the Department, subsequent demands invoking extended limitation become much harder to sustain. But don't assume that honest mistakes automatically protect you—willfulness can be inferred from the circumstances. The test is whether you deliberately suppressed facts or made statements knowing them to be false.

For provisioning contingent liabilities, I'd suggest: for demands within normal limitation where facts were fully disclosed, use a lower probability factor. For extended limitation demands where the Department had full knowledge, also use a lower factor. But where you know facts weren't disclosed, or statements were questionable, be conservative in your provisioning.

Smuggled Goods: The Exemption That Wasn't

Can smuggled goods claim exemption benefits meant for imports? The Supreme Court answered this question definitively in M. Ambalal and Co. vs Commissioner of Customs (2010 (260) ELT 487).

Diamonds were imported without a licence. The importer sought exemption under a notification. The Supreme Court held that smuggled goods cannot be considered as "imported goods" for purposes of exemption notifications. The benefit of exemption is admissible only for goods that are imported—meaning lawfully imported under valid licences where required.

The logic is straightforward: exemption notifications contain conditions. Those conditions must be fulfilled. When goods are imported without a required licence, the notification's condition isn't met. Import must be lawful. Goods not imported under a valid licence, whose import is prohibited by law, cannot be treated as lawfully imported goods. Benefits meant for imported goods cannot be extended to smuggled goods—that would contradict the exemption's purpose.

The practical implication: ensure every import complies with applicable licensing requirements. Don't think you can import without a licence and then claim exemptions meant for properly imported goods. Non-compliance disqualifies you from exemptions, quite apart from penalties and confiscation.

This also means your procurement teams need to verify licence availability before placing orders. And your compliance function should audit licence utilizations against actual imports quarterly, not annually.

Building Your Compliance Framework: A Practical Checklist

Based on these judicial principles, here's how to structure your import-export compliance. I've organised this as a series of processes rather than just a list—because compliance is about systems, not checklists.

Pre-Import Planning

Before you even place the purchase order, several things need verification. Is the product licensable? If yes, do you have valid licences with sufficient quota? What's the correct tariff classification? Have you analysed the commercial terms to understand which costs are the seller's obligation versus yours?

This isn't just a procurement exercise. Finance needs to be involved because valuation starts with commercial terms. If your contract says "CIF including landing charges" but doesn't specify who actually bears those charges contractually, you'll face disputes later.

Create a template that your procurement team must complete for every import order. Fields should include: HS classification, applicable duty rates, exemption notifications being claimed, licence number and available quota, commercial Incoterms with specific clarification on landing charges, freight, and insurance.

If the product attracts CVD, document whether similar goods manufactured domestically would attract excise duty. If you're claiming concessional rates based on end-use, start gathering evidence of intended use before the goods arrive—don't wait for the assessment to begin.

Determining Who's the Importer

This sounds basic but gets complicated when you have group structures, intermediary holding companies, high-sea sales, or bank financing.

Make an explicit decision: which legal entity in your group is the importer of record? Document this in writing. If you're doing high-sea sales and bills of lading will be endorsed, ensure the endorsement happens before vessel arrival. Get the timing right—the Sun Export Corporation case showed that endorsement transfers all consignee rights.

Where letters of credit are involved, understand the bank's documentary control. The Gipoint Development case showed that whoever holds the documents is treated as the owner. If you want to be the importer, ensure documents come to you, not your bank, at the relevant time.

Maintain a register of authorized signatories for bills of entry. Make sure these people understand they're legally representing the company as the importer.

Valuation Controls

Create a standard operating procedure for determining transaction value. Start with the invoice value. Then separately add: freight (if not included), insurance (if not included), landing charges (unless seller bears them contractually), royalties or license fees related to the goods (if any).

Document who bears each cost element. If your contract says CIF, get clarity: does this include landing charges or not? Don't assume—verify and document.

For related party transactions, maintain transfer pricing documentation contemporaneously. You don't want to be arguing about arm's length pricing three years later.

If goods arrive damaged, photograph them before and after unloading. Get third-party survey reports. File your remission claim under Section 22 immediately to the Assessing Authority—don't wait.

Managing the Crucial Date

Develop a tracking system that monitors: vessel arrival date, entry inwards date, bill of entry filing date, and actual clearance date. These four dates serve different purposes, and you need all of them.

The duty rate that applies is usually determined by the bill of entry filing date (or entry inwards date if later). So you have some control through timing your filing. If a beneficial exemption is about to expire, file before it lapses. If duty rates are about to decrease, consider whether delaying filing makes sense.

For warehoused goods, track the ex-bond clearance date separately. That's when duty crystallises for warehoused goods, not when they originally arrived.

If you're importing at multiple ports with transhipment, remember Amber Woollen Mills: the entry inwards at the first port can determine the relevant date even if the bill of entry is filed at the final destination.

Warehousing and SEZ Management

If you operate bonded warehouses, maintain separate inventory tracking for goods not yet cleared for home consumption. These goods are legally outside India for customs purposes (though not necessarily for other taxes—remember Radhasons International).

Track removal dates meticulously because that's when duty liability arises. You could warehouse goods in April 2023 at 10% rates, but if you clear them in April 2024 at 15% rates, you pay 15%.

For SEZ units, understand the regime switch. Imports from outside India into SEZ are governed by Customs Act and get duty exemption. But movements from SEZ to DTA are governed by SEZ Act provisions, not Customs Act. Maintain clear demarcation in your systems between processing and non-processing areas.

CVD Planning and Documentation

Identify upfront whether your imports attract CVD. The test: if similar goods were manufactured in India, would they attract excise duty? If yes, CVD applies.

Determine the stage at which you're importing. Don't let subsequent processing muddy the analysis—Vareli Weaves established that CVD is based on import stage, not what you do afterward.

If you're claiming concessional CVD rates for specific end-use, start gathering supporting documentation before import. Yes, Thermax said procedural compliance isn't fatal if substantive conditions are met. But why take chances? Get your L-6 licence or CT-2 certificate before importing, not after.

Where the Board issues circulars interpreting CVD exemptions, read them but remember HLG Trading: circulars can't override notifications. If there's a conflict, the notification prevails.

Loss and Damage Protocols

Create an immediate response protocol for pilferage or damage. Within 24 hours: file a report with customs authorities under Section 13 (for pilferage) or Section 22 (for damage), file a police complaint for pilferage, engage a third-party surveyor, photograph everything, document the quantity and value of missing/damaged goods.

Remember that BEML established: for pilferage, you have no duty liability if you report under Section 13 properly. But Udyani Ship Breakers showed that you must make remission claims to the Assessing Authority at the right time—you can't claim remission after assessment.

Train your logistics team to recognize the difference between pilferage (theft), damage (deterioration or destruction), and shortage (less quantity received). Each has different legal treatment.

Limitation and Record Management

Here's a reality: show cause notices can arrive three, four, even five years after import. Your ability to defend depends entirely on records you maintain.

Create a document retention policy: all import documents for a minimum of six years (one year normal limitation plus five years maximum extended limitation). This includes: commercial invoice, bill of lading/airway bill, packing list, bill of entry, assessment order, evidence of duty payment, correspondence with customs, licence/certificate copies, contracts showing commercial terms.

More important than just retaining documents: organize them. When a show cause notice arrives, you need to retrieve the complete file within days, not weeks.

For potential extended limitation cases, document the Department's knowledge. If customs officers inspected the goods, get their signatures. If you disclosed facts in correspondence, keep copies. Aban Loyd Chiles showed that where the Department had full knowledge, extended limitation failed.

Maintain a litigation tracker: all show cause notices received, amounts demanded, grounds of demand, limitation period applicable, probability assessment for provisioning, appeal status if any.

Licence Compliance System

Create a licence register showing: licence number, issuing authority, validity period, permitted quantity, utilized quantity, balance available, approaching expiry dates.

Set up automatic alerts 90 days before expiry. This gives you time to apply for extensions or fresh licences without disrupting procurement.

Conduct quarterly reconciliations: actual imports versus licence utiliztions. M. Ambalal established that smuggled goods (including imports without proper licences) cannot claim exemption benefits. So licence compliance isn't just about avoiding penalties—it's about preserving your exemption claims.

Where restricted or prohibited goods are involved, maintain evidence of DGFT approvals before placing orders.

Organisational Structure

Designate a Customs Compliance Officer at a senior level. This shouldn't be delegated to someone in logistics or procurement without financial oversight. The CCO should report directly to you or to a senior finance leader.

The CCO's role: quarterly compliance reviews, coordination with customs consultants, training for procurement and logistics teams, serving as a single point of contact for customs matters, managing litigation and show cause notices, and maintaining the compliance documentation system.

Conduct an annual compliance audit using external customs consultants. Internal teams develop blind spots. External review helps catch issues before the Department does.

Implement maker-checker controls for bill of entry filing. The person preparing the bill of entry shouldn't be the same person reviewing and filing it.

Technology Integration

If you're still managing customs compliance through spreadsheets and email, you're taking unnecessary risk. Integrate your systems.

Your ERP should link: purchase orders (with HS classification and licence requirements), logistics (vessel tracking, bill of entry filing dates), finance (duty payments, valuation calculations), inventory (warehoused versus cleared goods).

Automate assessable value calculation. The system should pull invoice value, add freight if not included, add insurance if not included, add landing charges unless contractually the seller's obligation, add any other includable costs. This eliminates calculation errors.

Create alerts for: upcoming licence expiries, duty rate changes that affect pending imports, assessment orders not received within expected time, discrepancies between assessment and self-assessment.

Maintain a digital repository with version control. When commercial terms change or amendments happen, you should be able to retrieve the contract version that was current at the time of import.

Legal Strategy and Litigation Management

Despite best efforts, litigation happens. Create a litigation budget separate from operational budgets. Customs disputes can be expensive.

Understand the appellate hierarchy: Commissioner (Appeals) → Customs, Excise and Service Tax Appellate Tribunal (CESTAT) → High Court → Supreme Court. At each level, assess whether further appeal makes financial sense.

Develop relationships with specialized customs lawyers. This isn't work for general corporate counsel. Customs law is technical and precedent-heavy.

When taking aggressive interpretative positions on classification or valuation, get external legal opinions. If litigation follows, the opinion demonstrates good faith and helps defend against allegations of willful suppression.

Evaluate settlement schemes when they're announced (like Sabka Vishwas). Sometimes settling and moving on makes more sense than years of litigation.

For provisioning: use probability-weighted estimates. Don't just list maximum exposure—assess likelihood. Factor in: strength of legal position, precedents, Department's knowledge of facts, whether extended limitation applies, appeal success rates at Tribunal and High Courts.

Continuous Improvement

Customs law is dynamic. Notifications change monthly. Circulars get issued. Court decisions create new precedents. Your compliance framework must have update mechanisms built in.

Subscribe to reliable customs updates (not just free newsletters—invest in quality services). Have someone on your team responsible for monitoring changes.

Participate in industry forums where customs issues are discussed. Other CFOs facing similar issues are valuable sources of practical knowledge.

Conduct quarterly training for everyone who touches imports: procurement, logistics, finance, even legal. A 30-minute update session every quarter keeps everyone current.

After any significant dispute or show cause notice, conduct a post-mortem. What went wrong? What controls failed? What can be improved? Update your procedures accordingly.

Final Thoughts

Import-export compliance isn't glamorous work. It doesn't drive revenue. It won't get you promoted. But getting it wrong can destroy value spectacularly. A single show cause notice demanding duty, interest, and penalties can wipe out margins on years of imports.

The case law we've reviewed shows that customs law operates through precise technical definitions and exact timing mechanisms. The difference between "when the vessel arrived" and "when the bill of entry was filed" determines which duty rate applies. Whether landing charges were the seller's contractual obligation determines if you add them to assessable value. Whether you reported pilferage under Section 13 or Section 23 determines if you pay duty on stolen goods.

These distinctions might seem pedantic, but they're not academic—they're financial. And they're your responsibility as CFO.

The compliance framework outlined above isn't meant to be exhaustive. Every organization needs to adapt it to their specific business model, import volumes, product complexity, and risk appetite. A company importing ten containers annually needs different controls than one clearing fifty containers daily.

But certain principles are universal: document everything, maintain transparency with customs authorities, understand that timing matters, know who your importer is, get valuation right from commercial terms, and don't assume smuggled goods can claim exemptions.

One final observation: I've noticed that organizations that treat customs compliance as a procurement or logistics function tend to face more problems than those that treat it as a finance and legal function. Procurement optimizes for price and delivery. Finance optimizes for total cost including duties, penalties, and litigation risk. Those are different objectives.

As CFO, make sure you're actively involved in customs strategy—not just reacting when show cause notices arrive. The cases we've reviewed were all disputes that reached courts. Imagine how many similar issues got resolved (or didn't get detected) without litigation. Your goal is to be in the "didn't get detected because we were compliant" category, not the "resolved without litigation through settlement" or "we're on our way to the Supreme Court" categories.

Customs compliance is risk management. Treat it accordingly.

Disclaimer: This article reflects personal views of the author based on review of judicial pronouncements and is not legal advice. Organizations should consult qualified customs lawyers and consultants for specific guidance.

Icegate Port Code List | Need of GST in India | Powers of GST Officers | GST Audit Procedure | GST Audit Procedure | GST penalty under section 74

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified