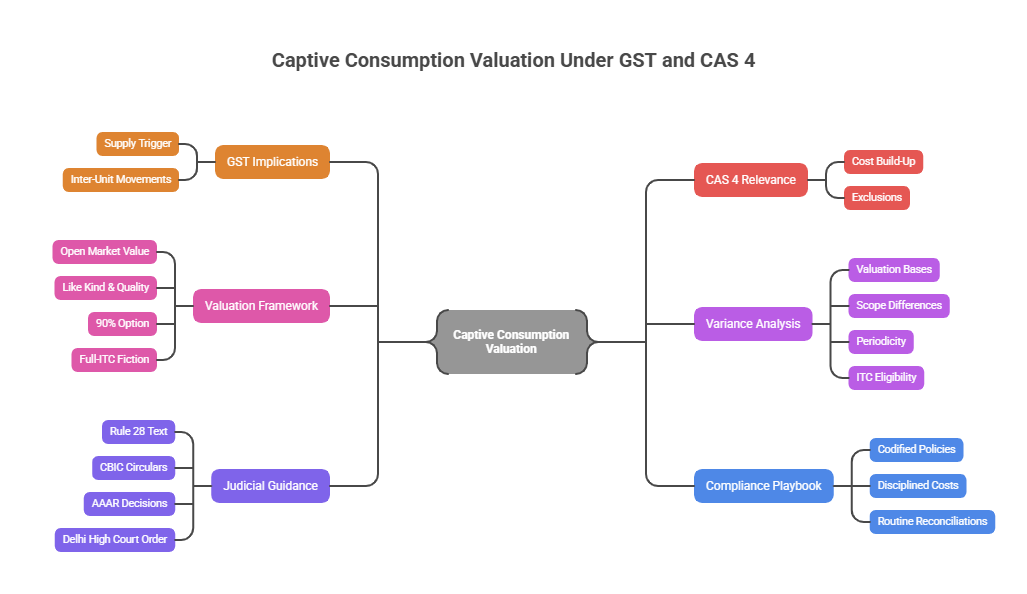

Executive Summary

"Captive consumption" (in cost/indirect-tax parlance) broadly refers to goods manufactured by one division/unit and consumed by another division/unit of the same organisation (or a related undertaking) for further manufacture or use. Under GST, the tax trigger is supply, not manufacture, and therefore pure intra-GSTIN captive consumption (intermediate goods consumed within the same registered person) typically does not create an outward supply event; however, inter-unit movements across GST registrations (distinct persons) are expressly deemed supplies even without consideration, which is where "captive consumption valuation" becomes live again for GST.

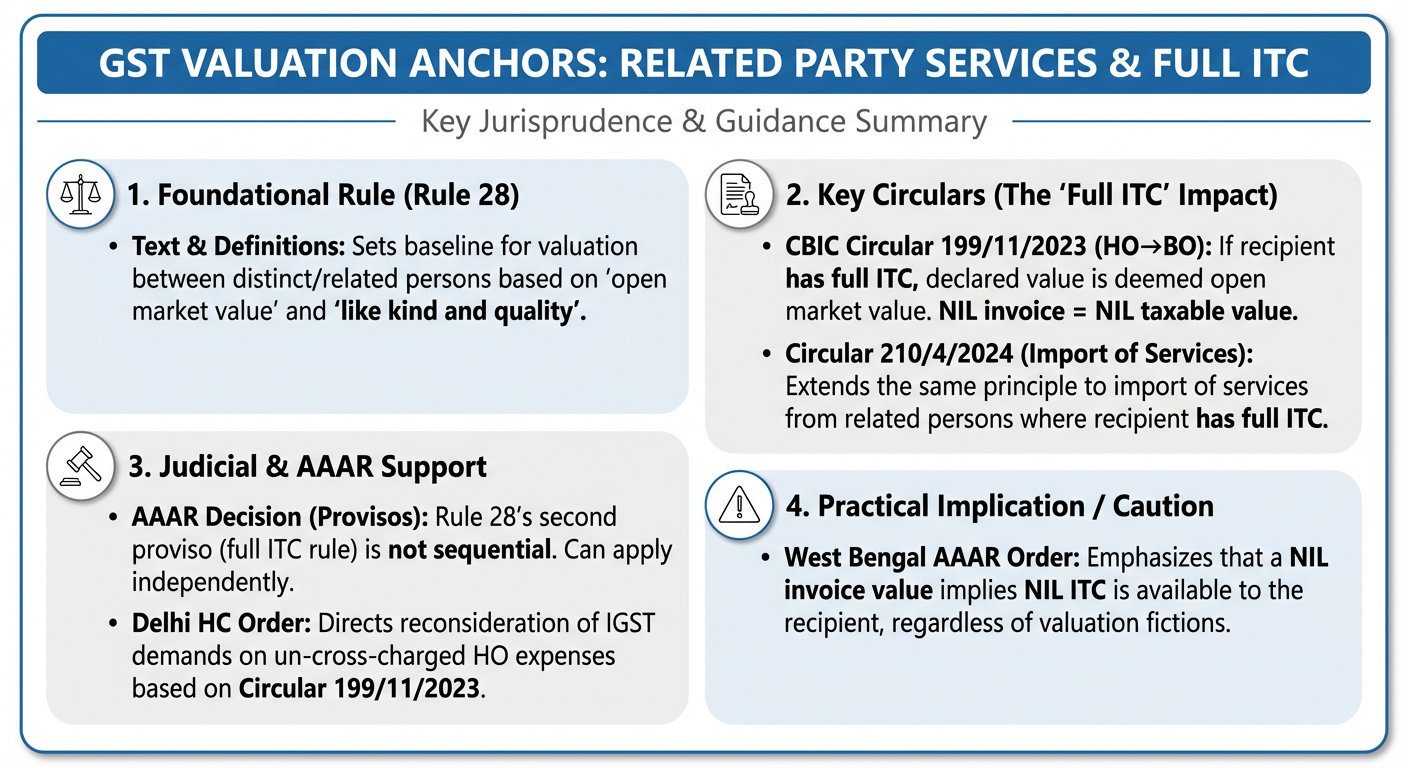

For goods or services supplied between "distinct persons" (multiple registrations under the same PAN across States/UTs, or separate establishments across States/UTs), valuation is governed by Section 15(4) read with Rule 28 of the CGST Rules (open market value → like kind & quality → Rule 30/31), with two strategically important provisos: a 90% option for onward "as such" supply, and a full-ITC deeming fiction where the invoice value is accepted as open market value.

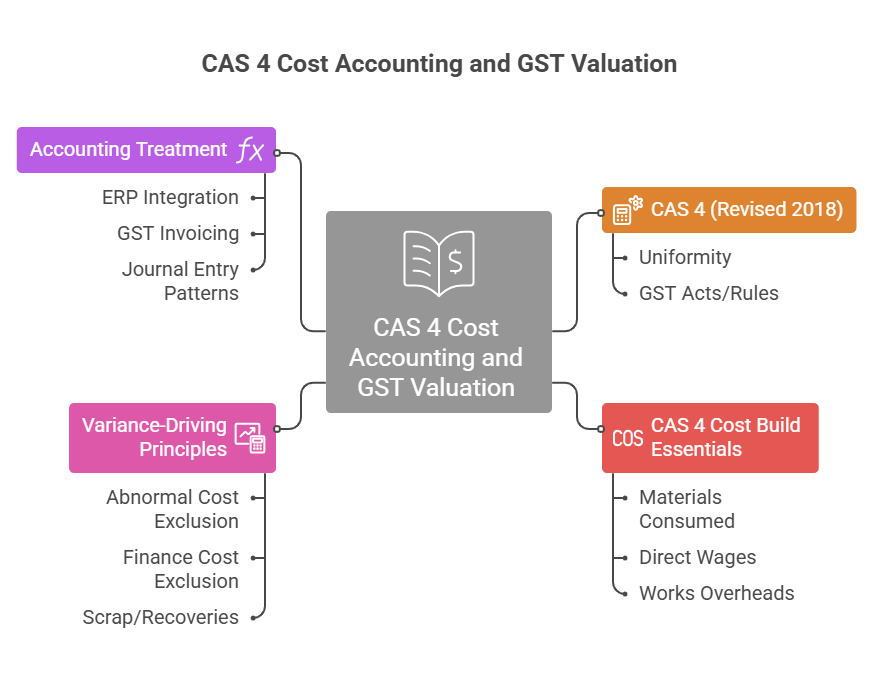

CAS 4 (Revised 2018) issued by The Institute of Cost Accountants of India explicitly notes that while "captive consumption" is no longer relevant for computing GST incidence, cost of production/manufacture remains relevant under GST where the value of supply is determined based on cost (e.g., Rule 30). CAS 4 also provides a structured cost build-up, exclusions (e.g., interest/finance costs, abnormal costs), and allocation principles that are directly usable as defensible "cost" support for Rule 30 valuations and for audit-ready reconciliations.

In practice, the largest variances between CAS 4 cost sheets and GST taxable values arise from: (i) different valuation bases (Rule 28 OMV vs invoice value deemed OMV vs 110% cost), (ii) scope differences in cost elements (production admin, R&D, QC, free supplies, scrap recoveries, subsidies), (iii) periodicity (annual CAS 4 vs transaction/month GST), and (iv) ITC eligibility differences at the recipient unit (which determines whether Rule 28's deeming fiction is available).

Key jurisprudence and guidance to anchor positions includes: (a) the Rule 28 text and its definitions of "open market value" and "like kind and quality", (b) CBIC Circular 199/11/2023 clarifying valuation of HO→BO services and the NIL-invoice/NIL-value implication when full ITC is available to the recipient, (c) Circular 210/4/2024 extending the same principle to import of services from related persons where full ITC is available, (d) an AAAR decision holding that Rule 28's provisos are not necessarily sequential and the second proviso can apply where the recipient is eligible for full ITC, (e) a West Bengal AAAR order emphasising that nil invoice value implies nil ITC, even if valuation fiction is relied upon, and (f) a Delhi High Court order directing reconsideration of IGST demand on un-cross-charged HO expenses in light of Circular 199/11/2023.

Finally, a CFO-grade solution focuses on codified valuation policies, disciplined cost builds (CAS 4 aligned), and routine variance reconciliations that anticipate analytics-driven scrutiny and audit selection.

Captive Consumption Under GST: Scope and When It Becomes a Supply

Under the legacy central excise regime, CAS 4 was operationalised because excise duty could apply on manufacture and captive clearances required a cost-based assessable value; the 2003 Board circular expressly linked captive consumption valuation under excise valuation rules to CAS 4 costing. Under GST, the charging provision levies tax on supplies (intra-State under CGST; inter-State under IGST), on value determined under Section 15.

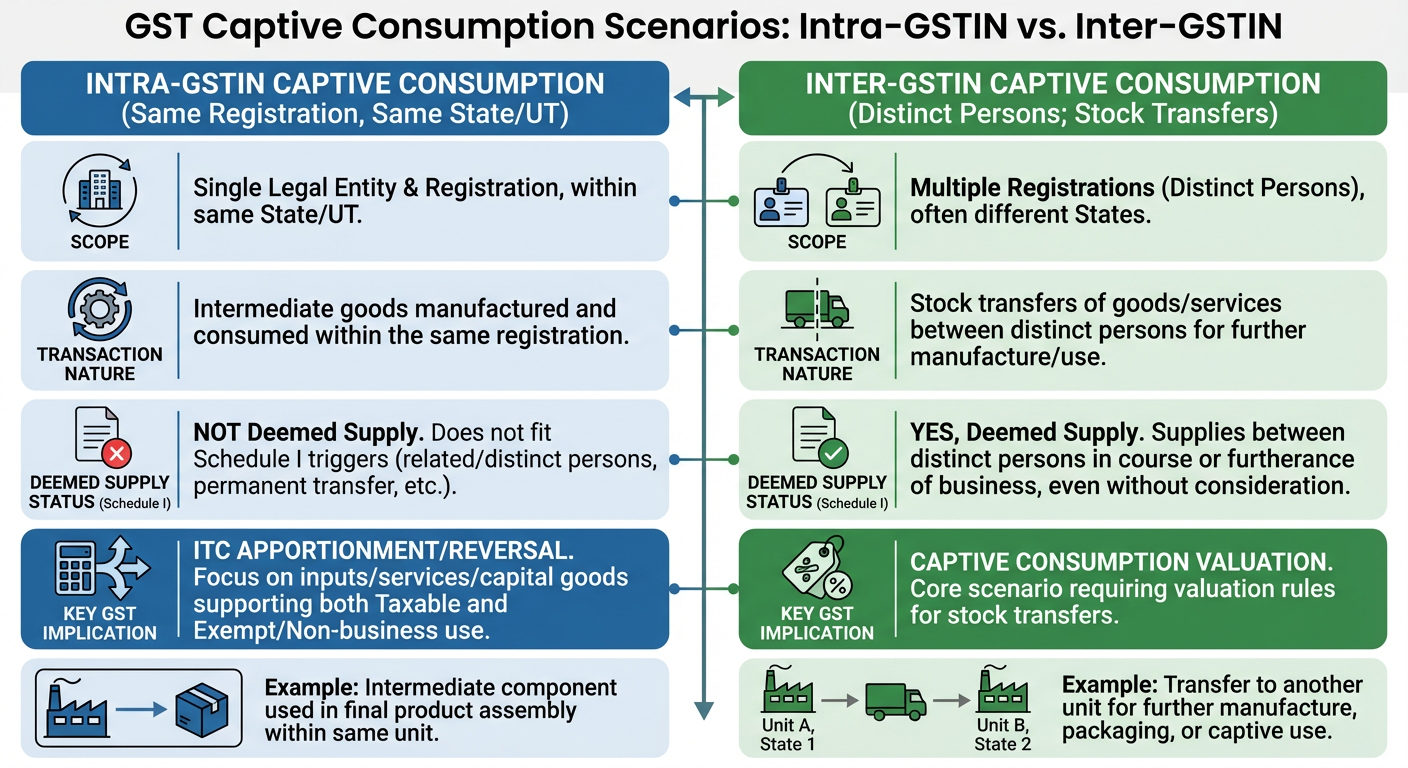

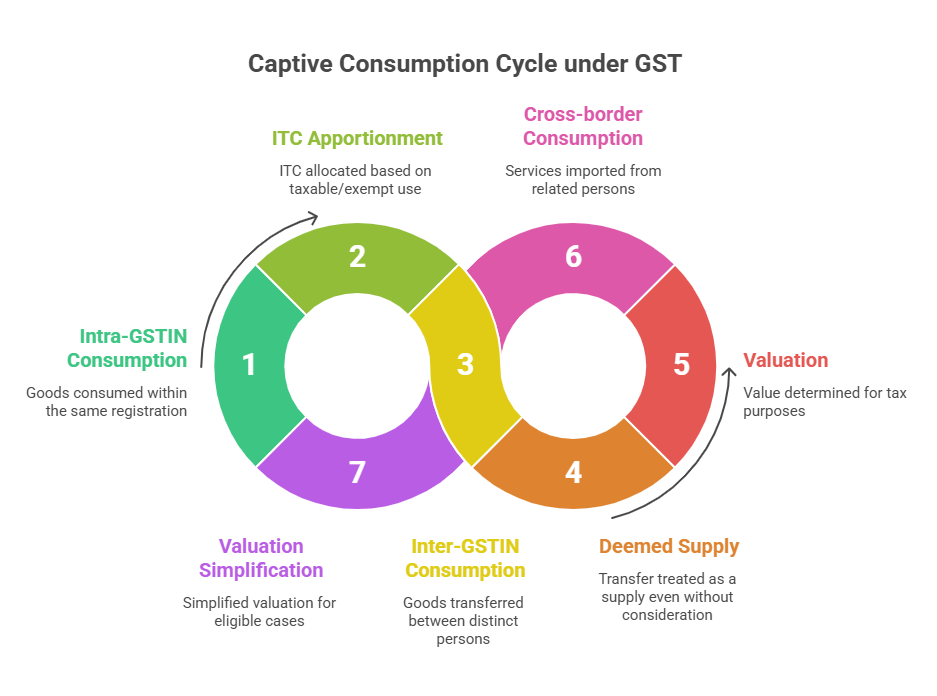

A practical "captive consumption" taxonomy for GST (industry-agnostic) is:

Intra-GSTIN Captive Consumption (Same Registration, Same State/UT)

Intermediate goods manufactured and consumed within the same registration do not fit the Schedule I deemed-supply triggers (which are framed around supplies between related/distinct persons, permanent transfer of business assets, principal-agent, or import of services). The more material GST implications are usually input tax credit (ITC) apportionment/reversal where inputs/input services/capital goods support both taxable and exempt/non-business use.

Inter-GSTIN Captive Consumption (Distinct Persons; Stock Transfers for Further Manufacture/Use)

If a legal entity holds more than one GST registration, each registration is treated as a distinct person for GST. Supplies of goods or services between distinct persons in the course or furtherance of business are deemed supplies even without consideration. This is the core GST "captive consumption valuation" scenario: a unit manufactures goods, transfers them to another unit (often in another State) for further manufacture, packaging, or captive use.

Cross-Border "Captive Consumption" of Services (Related Person Import of Services)

Import of services by a person from a related person or from any of its establishments outside India, in the course or furtherance of business, is a deemed supply even without consideration. Where valuation and ITC are fully available, the law/circulars create strong valuation simplifications (discussed below).

Industry-specific issues (not assumed in this report) can become relevant where there are regulated valuation constructs or special supply chains — e.g., captive power/steam transfers, petroleum-adjacent chains, multi-stage pharma manufacturing, toll/contract manufacturing, SEZ supplies, and financial services branch models — primarily because the recipient unit's ITC eligibility may be constrained or because open market comparables are difficult to establish.

Valuation Framework and Official Guidance: Rule 28, Rule 30, Invoicing, and Variance Analytics

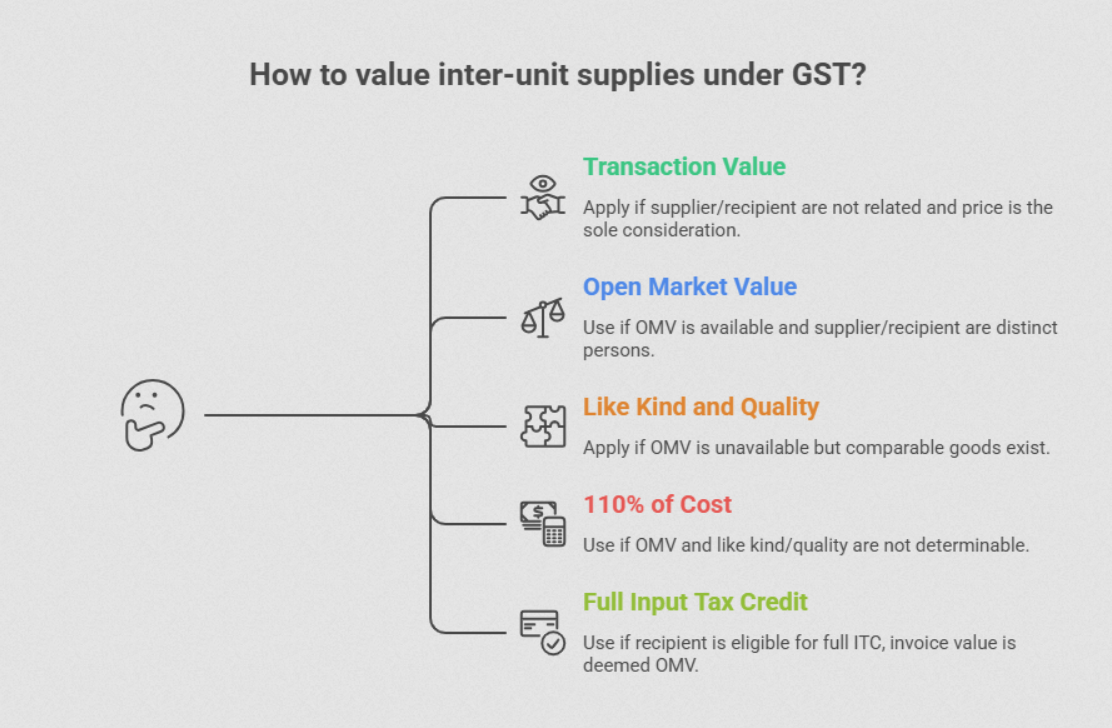

Section 15(1) (transaction value) applies where supplier/recipient are not related and price is the sole consideration. For distinct persons, valuation is generally driven by Section 15(4) (value cannot be determined under 15(1), apply prescribed manner) with Rule 28 as the primary mechanism.

Rule 28 — Statutory Valuation Ladder (Distinct/Related Persons)

Step 1 — Open Market Value (OMV)

Apply open market value (defined ex-GST taxes).

Step 2 — Like Kind & Quality

If OMV unavailable: like kind and quality (comparability factors: characteristics, quantity, reputation, etc.).

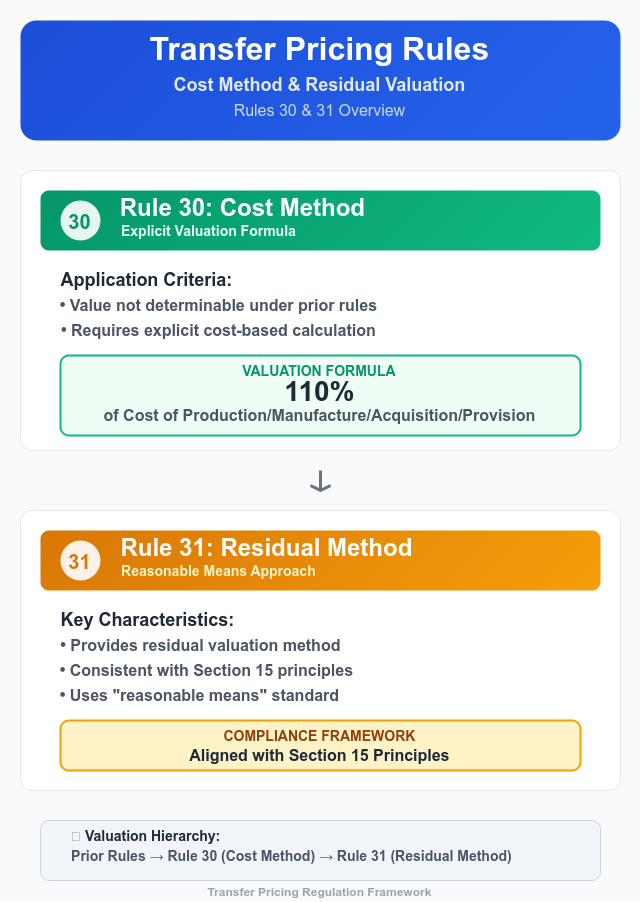

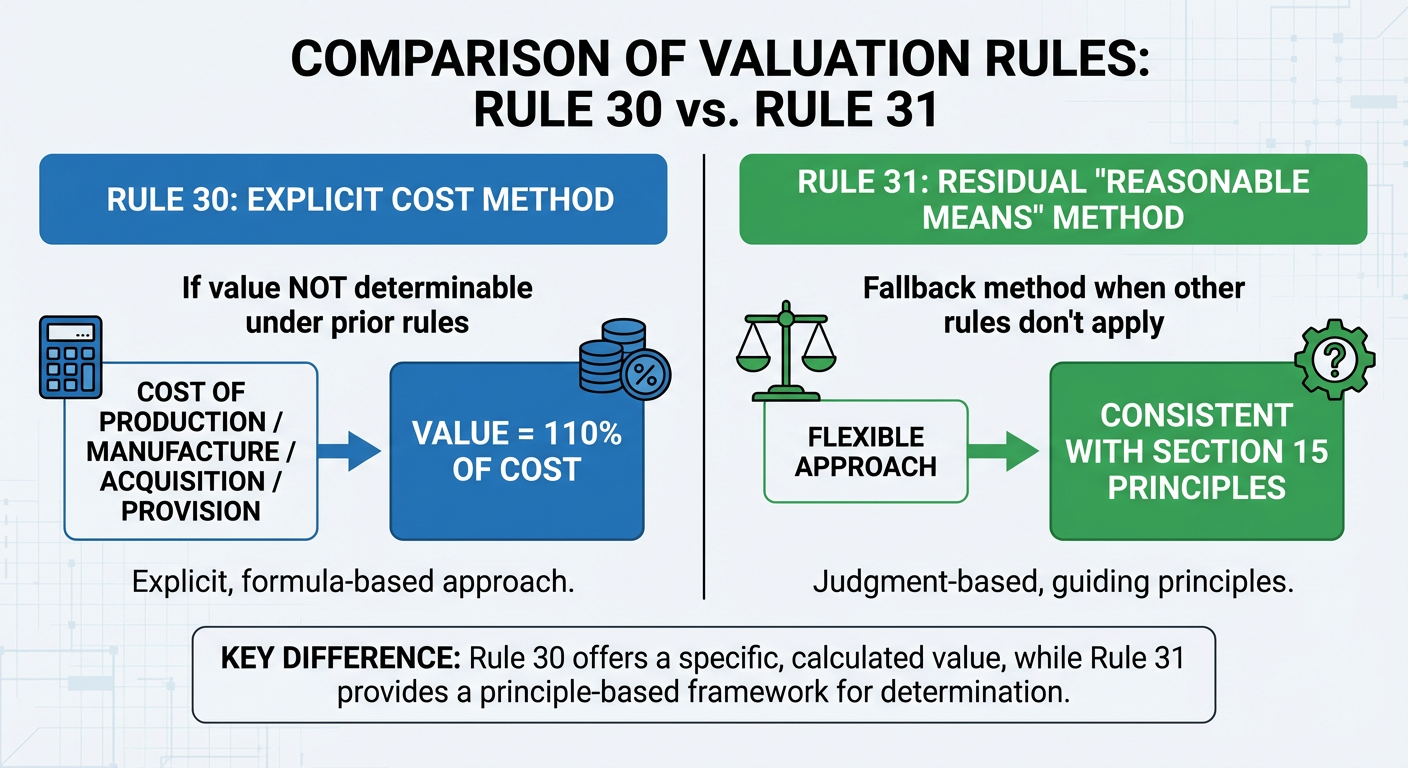

Step 3 — Rule 30 / Rule 31

If still not determinable: apply Rule 30 (110% of cost), failing which Rule 31 (reasonable means).

Two Key Provisos

90% Option: Where goods are intended for further supply "as such" by the recipient, the supplier may value at 90% of the price charged by the recipient to its customer (not related).

Full-ITC Deeming Fiction: Where the recipient is eligible for full input tax credit, the value declared in the invoice is deemed to be OMV.

Rule 30's cost method: If value not determinable under prior rules, value is 110% of the cost of production/manufacture/acquisition/provision. Rule 31 provides a residual "reasonable means" method consistent with Section 15 principles.

CBIC / GST Council Circulars That Materially Affect Inter-Unit Valuation Positions

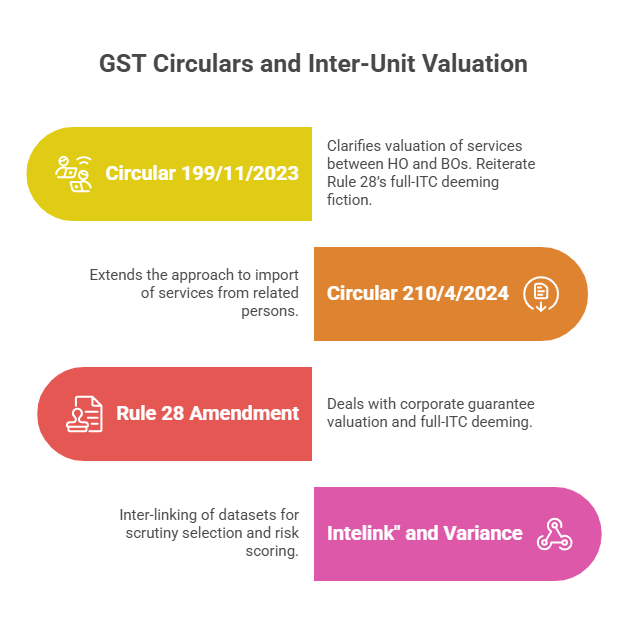

Circular 199/11/2023 (Dated 17 July 2023)

Clarifies valuation of services between HO and BOs (distinct persons). It reiterates Rule 28's full-ITC deeming fiction and clarifies that when full ITC is available to the recipient BO, the invoice value is deemed OMV irrespective of whether specific cost components (e.g., employee cost) are included; further, where no invoice is issued for particular internally generated services and full ITC exists, the value may be deemed Nil as OMV under the deeming fiction.

Circular 210/4/2024 (Dated 26 June 2024)

Extends the above approach to import of services from related persons where the Indian recipient is eligible to full ITC, anchoring the position that the Rule 28 second proviso principle applies in this import-of-services context as well.

Corporate Guarantee Valuation (Rule 28 Sub-rule (2))

Rule 28 has also been amended to deal with corporate guarantee valuation (sub-rule (2)) and a further proviso on full-ITC deeming in that sub-rule has been inserted via notification. While not "captive consumption" in the manufacturing sense, CFOs should treat this as part of the broader inter-unit/related-party valuation governance framework.

"Intelink" and Variance: Interpreting the Term in a GST Controls Context

The term "Intelink" is not commonly referenced in publicly available CBIC/GST Council/GSTN documentation for valuation of captive consumption. In practice, what CFOs see as "intel-linking" is often the inter-linking of datasets (invoice-level e-invoicing, e-way bill movement, GSTR-1 outward supplies, GSTR-3B liabilities, ITC availability, and entity master data) used for scrutiny selection, audit planning, and enforcement risk scoring. As compliance increasingly relies on interconnected data systems, enterprises managing high-volume inter-unit transactions adopt GST API integration to synchronise invoices, returns, and analytics efficiently. Official materials describe the expansion of analytics tooling and return scrutiny processes, and audit manuals emphasise structured compliance verification.

For valuation-sensitive inter-unit supplies, the practical implication is that persistent variances between your cost base (CAS 4 / costing records), your invoiced taxable values (Rule 28/30), and your outward supply/stock movement datasets can act as risk flags during scrutiny/audit selection and departmental queries — even where the net tax effect is revenue-neutral due to ITC.

CAS 4 Cost Accounting: Valuation Mechanics and Accounting Entries

What CAS 4 (Revised 2018) Is Doing in a GST World

CAS 4 was originally issued to bring uniformity in computing cost of production for goods meant for captive consumption under the Central Excise valuation rules, and a Board circular linked captive consumption valuation to CAS 4 costing. CAS 4 (Revised 2018) explicitly acknowledges GST and re-positions its objective toward consistent determination of cost of production/acquisition/supply of goods and provision of services "as required under the provisions of GST Acts/Rules."

This is operationally important because Rule 30 uses "cost of production/manufacture" but GST law does not define a detailed cost build; CAS 4 provides a defensible, standardised build that tax teams can present during audit/assessment, especially where OMV is not reliably determinable and Rule 30 becomes the fallback.

CAS 4 Cost Build Essentials That Matter for GST Valuation

CAS 4 defines cost of production/manufacturing to include materials consumed, direct wages/salaries, direct expenses, works overheads, quality control, R&D, packing, and administrative overheads relating to production, with WIP/FG adjustments and recoveries from scrap/wastage.

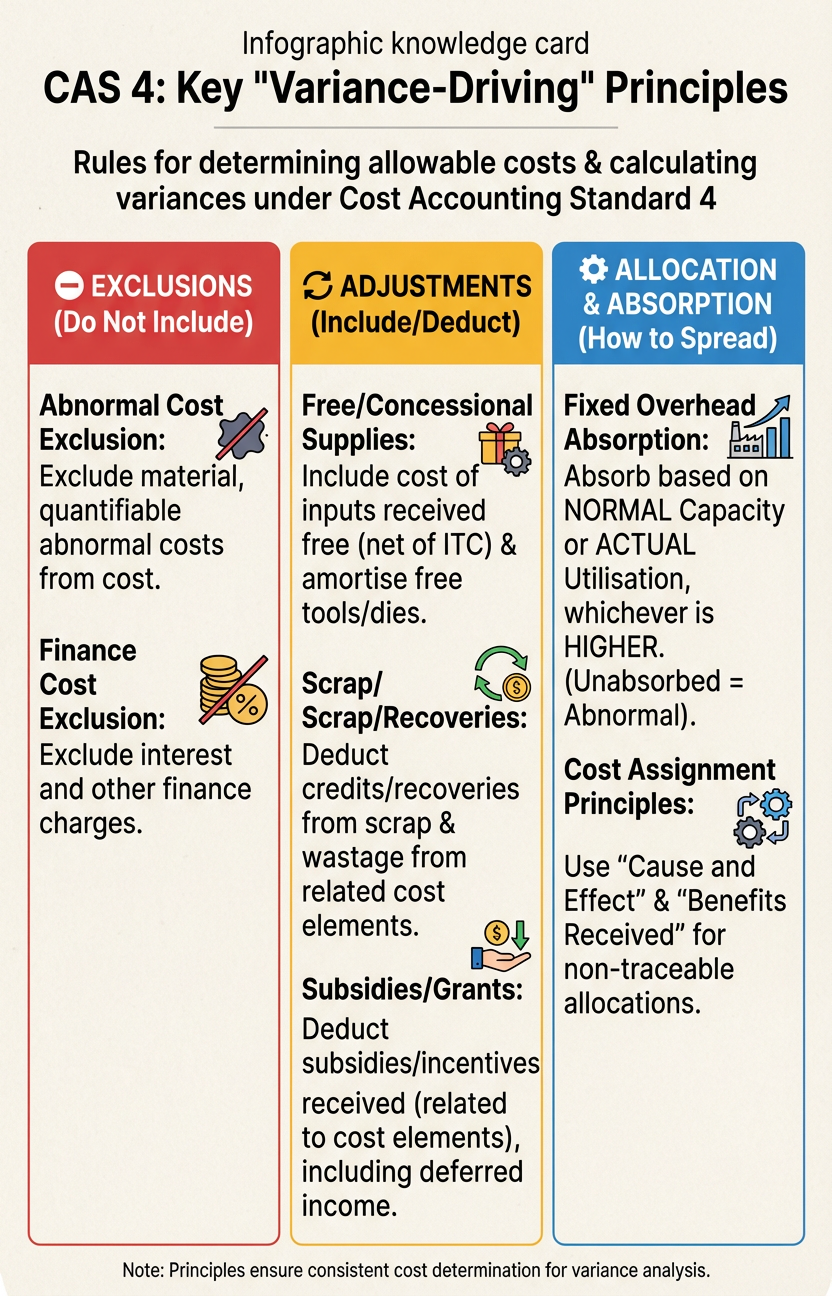

CAS 4 also establishes several "variance-driving" principles:

CAS 4 Variance-Driving Principles for GST

Abnormal Cost Exclusion

Material abnormal, quantifiable abnormal costs should not form part of cost.

Finance Cost Exclusion

Interest and other finance costs are excluded.

Free/Concessional Supplies

Include cost of inputs received free/concessional (net of ITC) and amortisation of free tools/dies/patterns etc.

Scrap/Recoveries

Deduct credits/recoveries relating to cost elements and recoveries from scrap/wastage.

Subsidies/Grants

Deduct subsidies/grants/incentives received (other than from the recipient) relating to cost elements, including deferred income treatment.

Capacity and Fixed Overhead Absorption

Fixed overheads (including QC/R&D/production admin) are to be absorbed based on normal capacity or actual capacity utilisation, whichever is higher; unabsorbed is treated as abnormal.

Cost Assignment Principles

"Cause and effect" and "benefits received" for allocations not directly traceable.

Accounting Treatment and Suggested Journal Entry Patterns for Inter-Unit Supplies

CAS 4 is a cost standard, not a financial reporting standard, so it does not prescribe GL entries. The CFO problem is the integration of (i) cost measurement (CAS 4), (ii) ERP valuation and inventory costing, and (iii) GST invoicing/returns that must reflect a taxable outward supply when distinct persons are involved.

| Scenario |

Dispatching Unit (Supplier GSTIN) |

Receiving Unit (Recipient GSTIN) |

GST Characterisation |

Valuation Anchor |

| Stock transfer of finished goods to depot/branch |

Dr Inter-unit receivable (incl. GST) / Cr Inter-unit sales (taxable value) / Cr Output IGST/CGST+SGST |

Dr Inventory (taxable value) / Dr ITC (IGST/CGST+SGST) / Cr Inter-unit payable |

Deemed supply between distinct persons even without consideration |

Rule 28 ladder; if full ITC, invoice value deemed OMV |

| Transfer of intermediate goods for further manufacture (different GSTIN) |

Similar to above; inventory classification as semi-finished / WIP as applicable |

Dr WIP/Raw material/Stores; Dr ITC; Cr payable |

Deemed supply between distinct persons |

Rule 28; if OMV not determinable, Rule 30 (110% of cost) |

| HO provides management/support services to branch (distinct GSTIN) |

Dr Inter-unit receivable / Cr Inter-unit service income / Cr Output IGST (if invoiced) |

Dr Expense/overhead / Dr ITC / Cr payable |

Supply of services between distinct persons (Schedule I logic), with valuation simplifications when full ITC exists |

Circular 199/11/2023 + Rule 28 second proviso; NIL invoice value may be deemed OMV when full ITC and no invoice raised |

| Import of services from overseas related party (RCM) |

Recipient in India: Dr Expense/asset; Dr ITC (if eligible); Cr RCM liability / Cr vendor |

N/A |

Deemed supply: import of services from related person even without consideration |

Circular 210/4/2024 + Rule 28 second proviso approach where full ITC exists |

Variance Analysis: CAS 4 vs GST Tax Base with Worked Examples

Why Variances Exist Conceptually

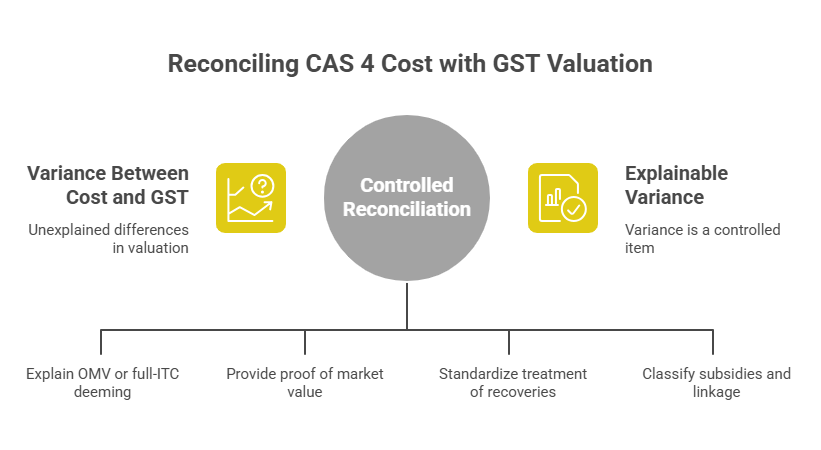

GST taxable value is a legal valuation construct, not necessarily the same as "cost" or "book value". Section 15 includes certain items in value (taxes other than GST if charged separately, incidental expenses, interest/late fee/penalty for delayed payment, subsidies directly linked to price) and excludes specific discounts under conditions. Where Section 15(1) transaction value is unavailable/invalid (as in distinct person supplies), Rule 28/30/31 valuation rules override, and CAS 4 becomes a supporting cost measurement basis primarily relevant when Rule 30 is applied or where cost is used as a defensible proxy.

Therefore, "variance" should be treated as a controlled reconciliation item rather than an "error" per se — provided it is explainable from Rule 28 choices/provisos, OMV evidence, ITC eligibility, and CAS 4 cost build principles.

Worked Example Set with Quantified Calculations

All examples assume an 18% GST rate for illustration only; rate classification is out of scope here.

Example A: Stock Transfer to Another State (Recipient Eligible for Full ITC) – Invoice Value Planning vs CAS 4 Cost

Facts

Finished goods cost of production per CAS 4 cost sheet = ₹1,000/unit (fully absorbed, net of eligible ITC in inputs). Supplier transfers 1,000 units from Plant GSTIN (State A) to Depot GSTIN (State B). Distinct persons apply. Recipient depot makes only taxable outward supplies (full ITC).

Two Legally Supportable Valuation Choices

Choice 1 — Rule 30 fallback (if OMV/like kind not determinable): Taxable value = 110% of cost = ₹1,100/unit; IGST = ₹198/unit; total IGST = ₹1,98,000.

Choice 2 — Rule 28 second proviso (full ITC): Invoice value = ₹900/unit (commercially motivated working-capital move); IGST = ₹162/unit; total IGST = ₹1,62,000. Invoice value is deemed OMV because recipient eligible for full ITC.

CFO Insight

Variance: CAS 4 cost (₹1,000) vs GST base (₹900 or ₹1,100) is not inherently non-compliant; it must be documented as a Rule 28 proviso choice (full ITC deemed OMV) or a Rule 30 fallback position. Choice (2) reduces IGST outflow/credit transfer to the receiver GSTIN; choice (1) increases ITC at the receiver. This becomes a cash-flow / ITC-pooling lever, but requires governance to avoid inconsistent pricing and audit discomfort.

Example B: Stock Transfer Where Recipient Is Not Eligible for Full ITC – OMV Becomes Binding

Facts

Same product is also sold by supplier to unrelated customers at ₹1,400/unit in the same time window, so an OMV is observable and defensible. Recipient unit makes exempt supplies/partially taxable supplies and cannot take full ITC.

Valuation Consequence

Rule 28 requires OMV if available; the full-ITC deeming fiction is not available. Taxable value = ₹1,400/unit; IGST = ₹252/unit. If recipient's eligible ITC ratio is, say, 60% (illustrative), then eligible ITC is ₹151.20/unit; balance ₹100.80/unit is reversed/blocked through Rule 42 mechanics (conceptually), increasing net cost at the recipient.

Variance Driver

CAS 4 cost (₹1,000) vs GST base (₹1,400) is explained by Rule 28 OMV priority and ITC eligibility constraints.

Example C: HO→BO Internal Services (Distinct Persons) – NIL Value Positions

Facts

HO incurs employee and overhead costs for shared management support. Recipient BO is eligible for full ITC. Rule 28 second proviso deems invoice value as OMV where full ITC exists. Circular 199/11/2023 clarifies that (i) invoice value is deemed OMV irrespective of whether certain cost components (like salary) are included, and (ii) if HO does not issue an invoice for particular internally generated services to a full-ITC BO, the value may be deemed Nil as OMV.

Position

If HO issues no cross-charge invoice, GST value could be treated as Nil (per the circular's clarification in the full-ITC scenario), which can create a large apparent "variance" versus CAS-style service cost allocations, even though the circular indicates this should be acceptable under the deeming fiction when full ITC exists.

CFO Risk Point

"Nil value" eliminates both output tax and the recipient's ITC; if the BO depends on ITC for cash-flow efficiency, the nil position may be counter-productive even if compliant. Circular 210/4/2024 extends the same principle to import of services from related persons where full ITC exists, reinforcing that "cost build vs invoice value" variance is not necessarily a compliance failure in full-ITC scenarios if properly documented.

Variance Matrix and Corrective Actions

| Variance Cause |

CAS 4 / Cost-Sheet Treatment |

GST Valuation / Reporting Impact |

Corrective Action & Evidence Pack |

| Rule 28 OMV vs cost |

CAS 4 is cost-based |

Rule 28 mandates OMV first when available |

Maintain OMV evidence: external sale invoices, comparable pricing, or valuation memo; document why OMV used |

| Rule 28 full-ITC deeming fiction used |

CAS 4 cost likely not equal invoice value |

Invoice value deemed OMV when recipient eligible for full ITC |

Maintain full-ITC eligibility evidence; board-approved inter-unit pricing policy |

| Rule 30 110% cost vs CAS 4 cost |

CAS 4 provides cost build |

GST base becomes 110% of cost |

Keep CAS 4 cost sheet and bridging schedule from cost sheet to "cost for Rule 30"; ensure consistent period and product mapping |

| Overhead absorption differences (capacity) |

Normal capacity vs actual (whichever higher); unabsorbed treated abnormal |

If ERP uses different absorption, GST cost base may diverge |

Align ERP standard cost logic to CAS 4, or maintain a reconciliation; document abnormal cost exclusions |

| Scrap / by-product recoveries |

Recoveries are deducted |

If not deducted in GST "cost", taxable value may be overstated |

Standardise recoveries treatment across costing and GST valuation memos; retain scrap sale records |

| Subsidies/grants effect |

Subsidies/grants deducted from relevant cost elements |

Section 15 includes certain price-linked subsidies in value (conceptual) |

Classify subsidy type and linkage; document treatment and whether Section 15(2)(e) is triggered; maintain subsidy agreements |

| Full-ITC but invoice raised at zero |

CAS 4 cost exists |

Output tax nil; recipient ITC nil |

Ensure business understands ITC consequence; West Bengal AAAR clarified no ITC when invoice value is zero |

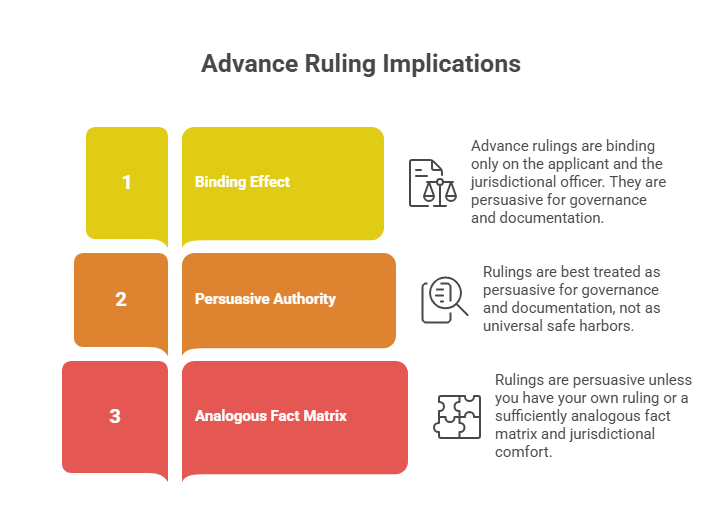

Judicial and Advance Ruling Landscape: Practical Implications

Advance rulings under GST (AAR/AAAR) are binding only on the applicant and the jurisdictional/concerned officer for that applicant (subject to change in law/facts), per Section 103. Therefore, rulings are best treated as persuasive for governance and documentation, not as universal safe harbours — unless you have your own ruling or a sufficiently analogous fact matrix and jurisdictional comfort.

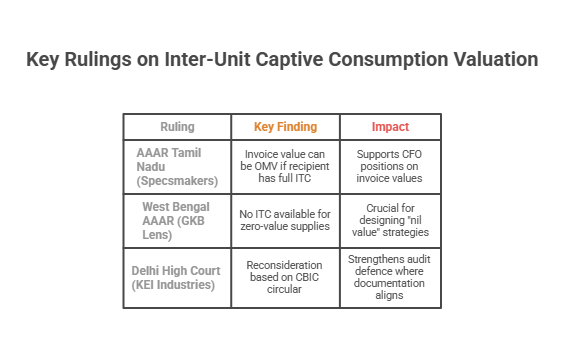

AAAR Tamil Nadu (Specsmakers Line of Reasoning)

Ruling

The appellate authority analysed Rule 28 and held that the two provisos (90% option and full-ITC invoice-value-as-OMV) cater to different situations and need not be applied only sequentially; where the recipient is eligible for full ITC, invoice value can be treated as OMV for valuation of inter-branch supplies.

CFO Implication

This supports CFO positions that invoice values may deviate from OMV/cost where the full-ITC deeming fiction is legitimately available — subject to evidence of full ITC eligibility.

West Bengal AAAR (GKB Lens Appeal)

Ruling

The appellate authority modified the ruling to clarify that no input tax credit would be available for supplies at zero value, i.e., if invoice value is zero, recipient ITC is zero.

CFO Implication

This is crucial in designing "nil value" strategies: they may reduce output tax, but they also eliminate ITC flow. Design carefully.

Delhi High Court (KEI Industries)

Ruling

In a writ challenging IGST demand on expenses not cross-charged to distinct persons, the court recorded reliance on Circular 199/11/2023 and directed reconsideration by the adjudicating authority in light of the circular. While fact-specific, it signals judicial receptiveness to the CBIC circular's full-ITC valuation logic (including the "nil value" deeming in appropriate circumstances).

CFO Implication

Strengthens audit defence where documentation aligns with Circular 199/11/2023. The most defensible posture is policy-driven consistency: explicitly classify the inter-unit transaction type, document Rule 28 method selection, and retain ITC eligibility evidence.

Compliance Playbook: Controls, Documentation, Roadmap, and Checklists

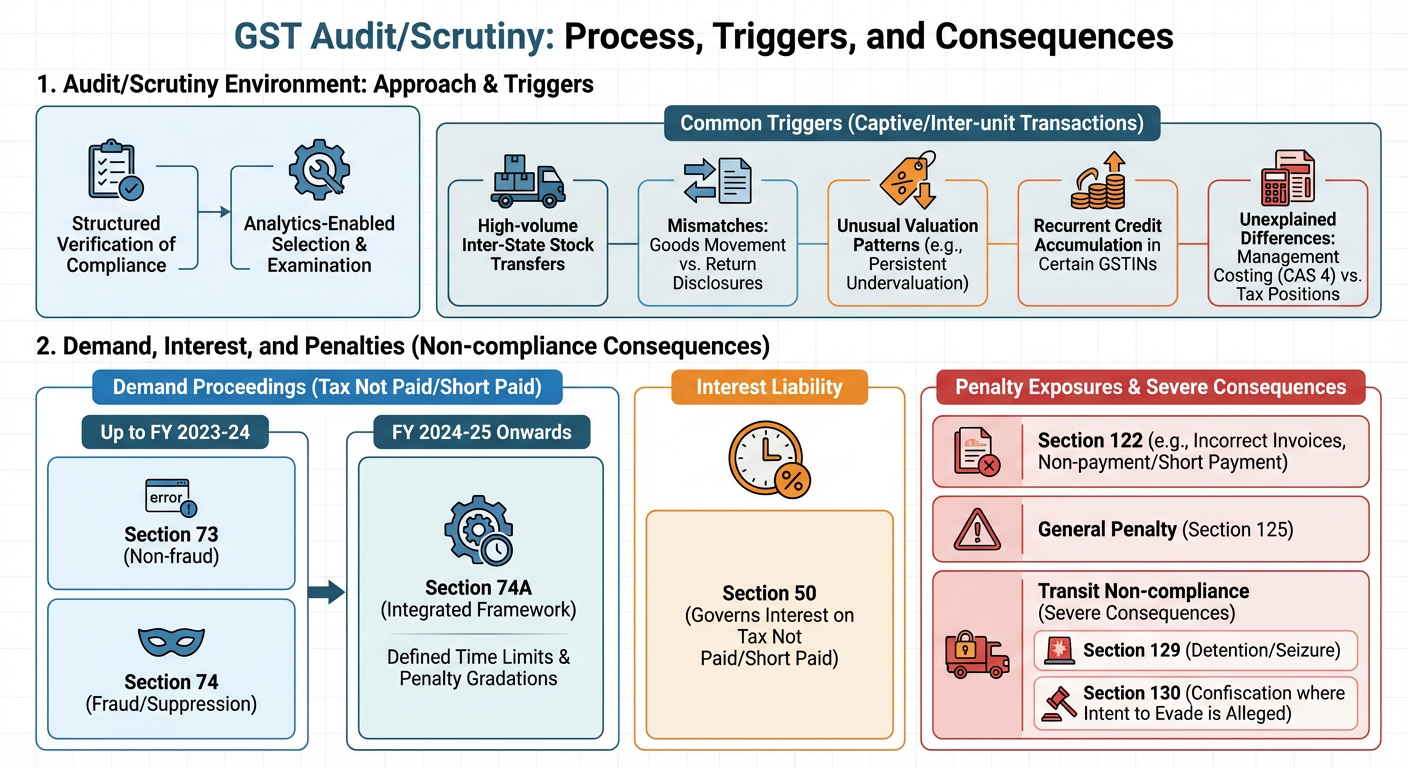

Compliance Risks, Audit Triggers, and Penalty Exposure

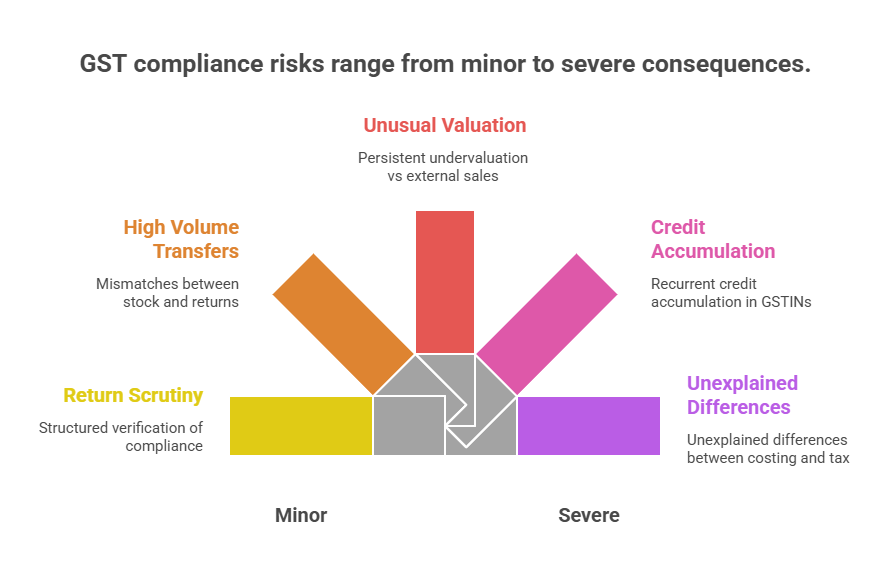

Common Audit Triggers for Inter-Unit Captive Supplies

- High-volume inter-State stock transfers

- Mismatches between goods movement and return disclosures

- Unusual valuation patterns (e.g., persistent undervaluation vs external sales)

- Recurrent credit accumulation in certain GSTINs

- Unexplained differences between management costing (CAS 4) and tax positions

Demand, Interest, and Penalty Exposure

Under GST, tax not paid/short paid can trigger demand proceedings under Section 73/74 for periods up to FY 2023-24 (non-fraud vs fraud/suppression) and under Section 74A for FY 2024-25 onwards (integrated framework with defined time limits and penalty gradations). Interest is governed by Section 50. Penalty exposures arise under Section 122 (e.g., incorrect invoices, non-payment/short payment), general penalty under Section 125, and potentially severe consequences for transit non-compliance (detention/seizure under Section 129; confiscation under Section 130 where intent to evade is alleged).

Practical Action Points and Documentation Checklist

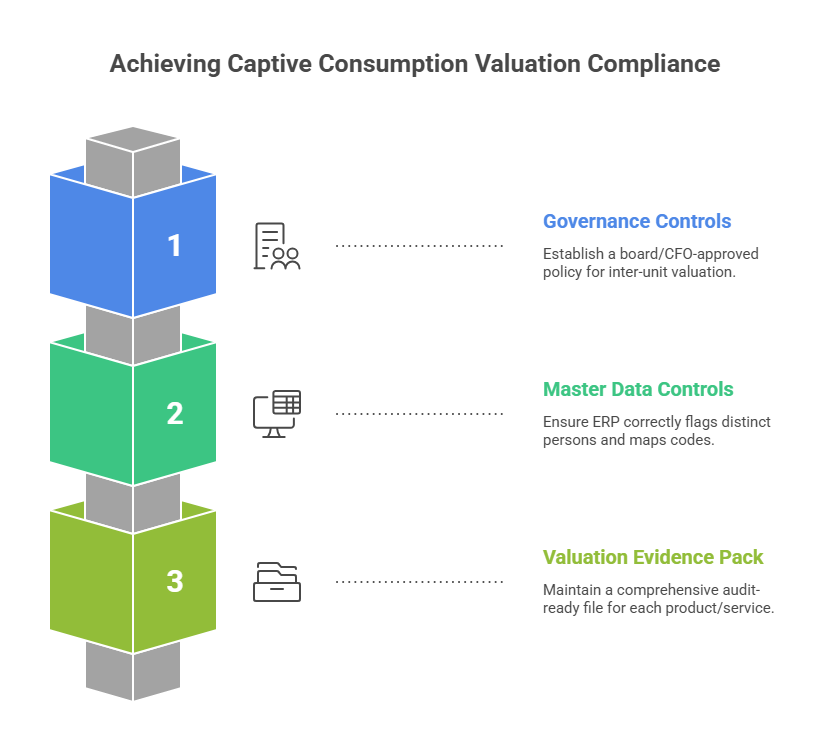

1. Governance Controls (Policy + Ownership)

A board/CFO-approved "Inter-Unit Supply & Valuation Policy" that maps each inter-unit flow to the correct Rule 28 method, sets decision criteria for OMV vs proviso usage, and defines frequency of price/cost updates (monthly/quarterly) with sign-offs.

2. Master Data Controls (The Silent Failure Point)

Ensure the ERP correctly flags distinct persons (multi-GSTIN structure), maps HSN/service codes, and tags recipient ITC eligibility status (full vs partial vs blocked) because the right to use Rule 28's second proviso is contingent on "eligible for full ITC".

3. Valuation Evidence Pack (Audit-Ready File)

Maintain, per product/service family and per period:

- Rule 28 valuation memo (method selected; why OMV exists/does not exist; why "like kind and quality" is/isn't applicable)

- OMV support: external sale invoices, price lists, comparable quotations, or market data where relevant

- Full-ITC support: recipient outward supply profile, ITC reversal computation evidence (Rule 42 logic) demonstrating "full" vs "partial"

- CAS 4 cost statements (where Rule 30 used) and bridging schedule from cost sheet to "cost for GST" (e.g., abnormal cost exclusions, recoveries, subsidies)

- Inter-unit invoice register (with link to e-invoice IRN where applicable) and goods movement evidence (e-way bill, delivery challans as applicable), with e-invoicing software helping ensure accurate invoicing and compliant IRN generation.

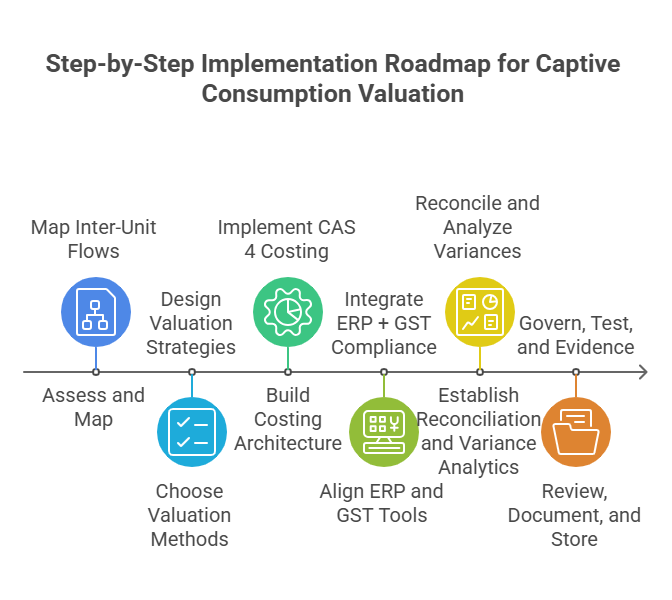

Step-by-Step Implementation Roadmap

Step 1 — Assess and Map

Map all inter-unit flows (goods, services, intangibles, cross-charges, imported services) and tag whether they are intra-GSTIN or between distinct persons (Section 25).

Step 2 — Design Valuation Strategies by Flow

For each flow, choose valuation method: OMV, like kind & quality, 90% option, full-ITC deeming (invoice value), or cost+10%. Record the rationale and when each method is permitted.

Step 3 — Build Costing Architecture (CAS 4 Aligned Where Cost Is Used)

Implement CAS 4 aligned cost build and allocation logic (normal capacity absorption, exclusions, recoveries, free supplies) and ensure it can generate "Rule 30 cost" packs on demand.

Step 4 — Integrate ERP + GST Compliance Tooling

Ensure invoice generation, tax determination, and postings align with Section 31 invoicing and Rule 28/30 valuation; ensure correct tax type (IGST vs CGST/SGST) based on place of supply constructs (inter-State where supplier and place of supply are in different States).

Step 5 — Establish Reconciliation and Variance Analytics

Implement a monthly reconciliation between:

- Inter-unit invoice taxable values (Rule 28/30)

- CAS 4 cost bases (where relevant)

- Inventory movement/value

- Outward supply reporting

This is the "variance dashboard" that prevents unpleasant scrutiny surprises.

Step 6 — Govern, Test, and Evidence

Run quarterly sample reviews, document exceptions, and refresh valuation memos; keep a litigation folder for circulars and rulings relevant to your chosen positions (e.g., Circular 199/11/2023, Circular 210/4/2024).

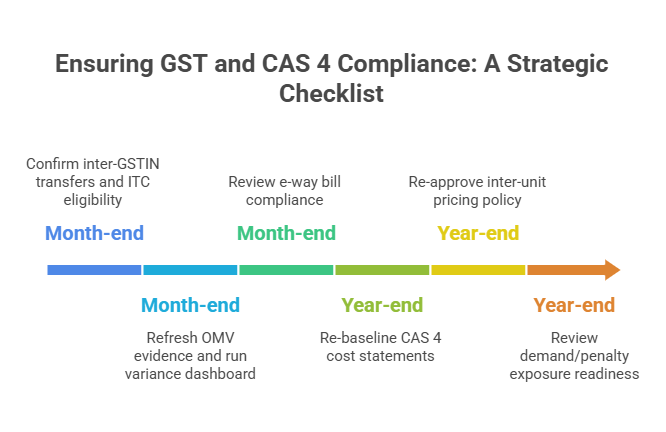

Month-End and Year-End Short Checklist

Month-End (Minimum Viable Controls)

- Confirm each inter-GSTIN stock/service transfer has a valid tax invoice and is reported consistently in outward supplies and tax payment.

- Verify recipient ITC eligibility status for flows using Rule 28 second proviso; document exceptions (partial ITC units).

- Refresh OMV evidence for high-value SKUs where OMV is used; flag price deviations beyond tolerance.

- Run variance dashboard: invoice value vs CAS 4 cost (where cost method used) and explain top deltas.

- Review e-way bill/document compliance for inter-State movements to reduce detention risk.

Year-End (Audit Defence and Policy Refresh)

- Re-baseline CAS 4 cost statements (period validity, allocations, abnormal cost treatment, recoveries).

- Re-approve inter-unit pricing policy and the "when OMV exists" decision logic; archive annual valuation memos.

- Review demand/penalty exposure readiness: ensure documentation folders are complete for valuation positions (Rule 28/30) and for full-ITC deeming positions (Circulars 199/11/2023 and 210/4/2024).

GST Registration Status Check | How to do GST Audit | E invoice Penalty Notification | DRC 01D | GST Penalty Under Section 74

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co