Appeals to GSTAT (Section 112): A Guide to Filing & Monetary Limits

Appeals to GSTAT (Section 112)

This document outlines the key aspects of appeals to the Goods and Services Tax Appellate Tribunal (GSTAT) under Section 112 of the CGST Act. It covers the types of orders appealable, the parties eligible to file appeals, and the monetary limits prescribed for departmental appeals to manage litigation.

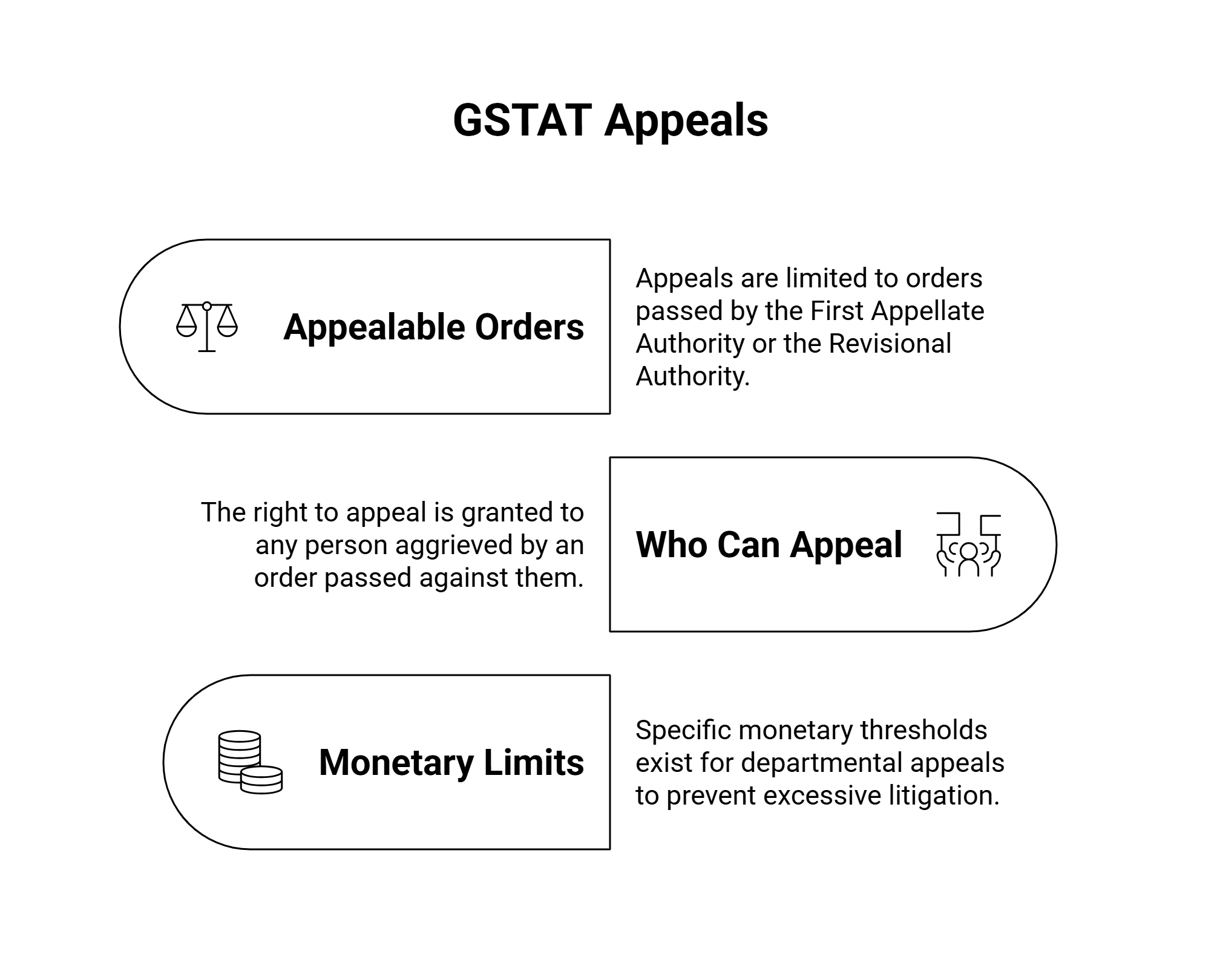

1. Appealable Orders

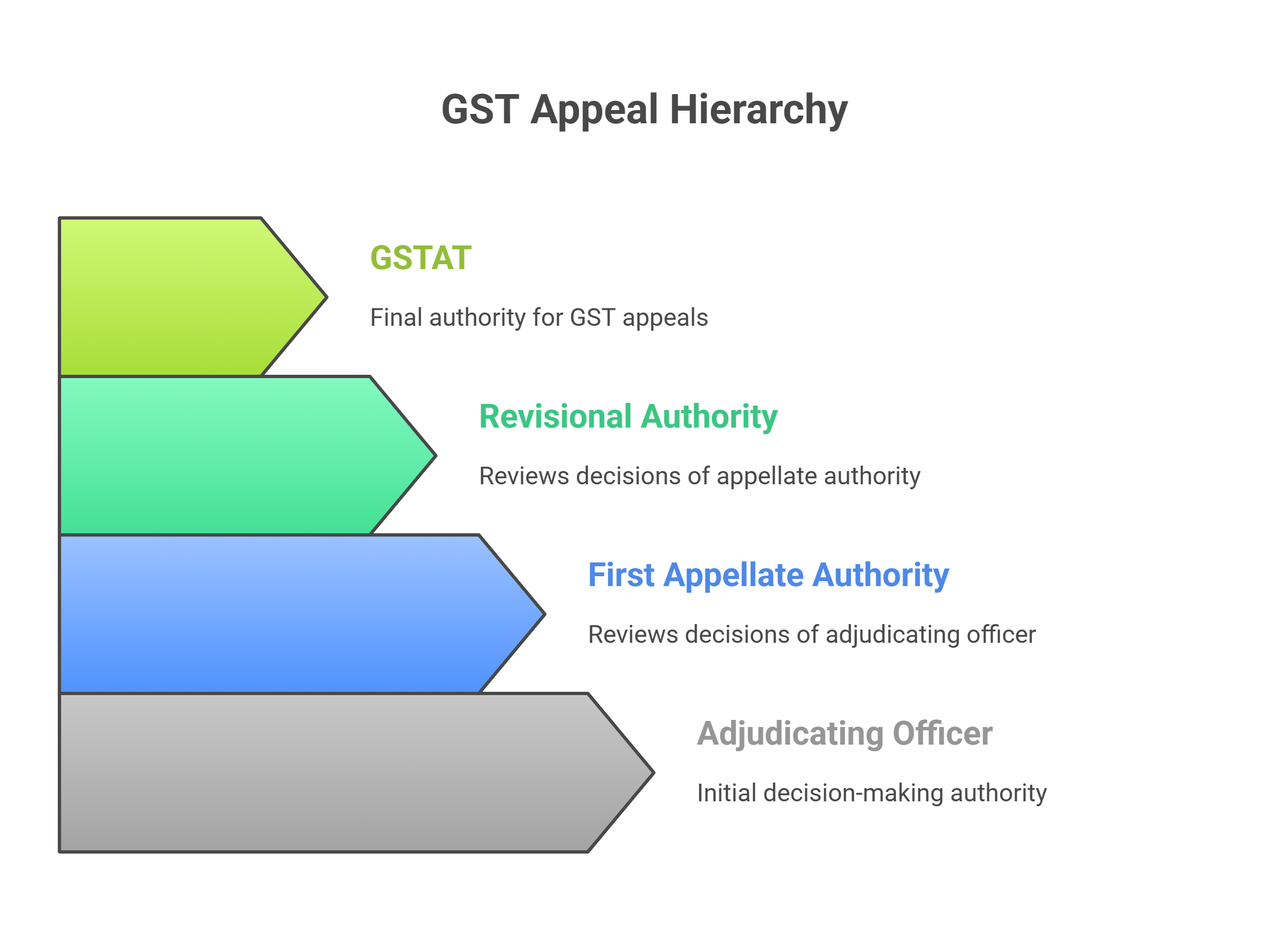

Appeals to the GSTAT are specifically limited to orders passed by the First Appellate Authority (under Section 107) or the Revisional Authority (under Section 108) of the CGST Act. This means that only decisions made at these two levels of adjudication can be challenged before the GSTAT. Orders passed by any other authority, such as the adjudicating officer, cannot be directly appealed to the GSTAT. The route for challenging those orders is to first appeal to the First Appellate Authority.

2. Who Can Appeal?

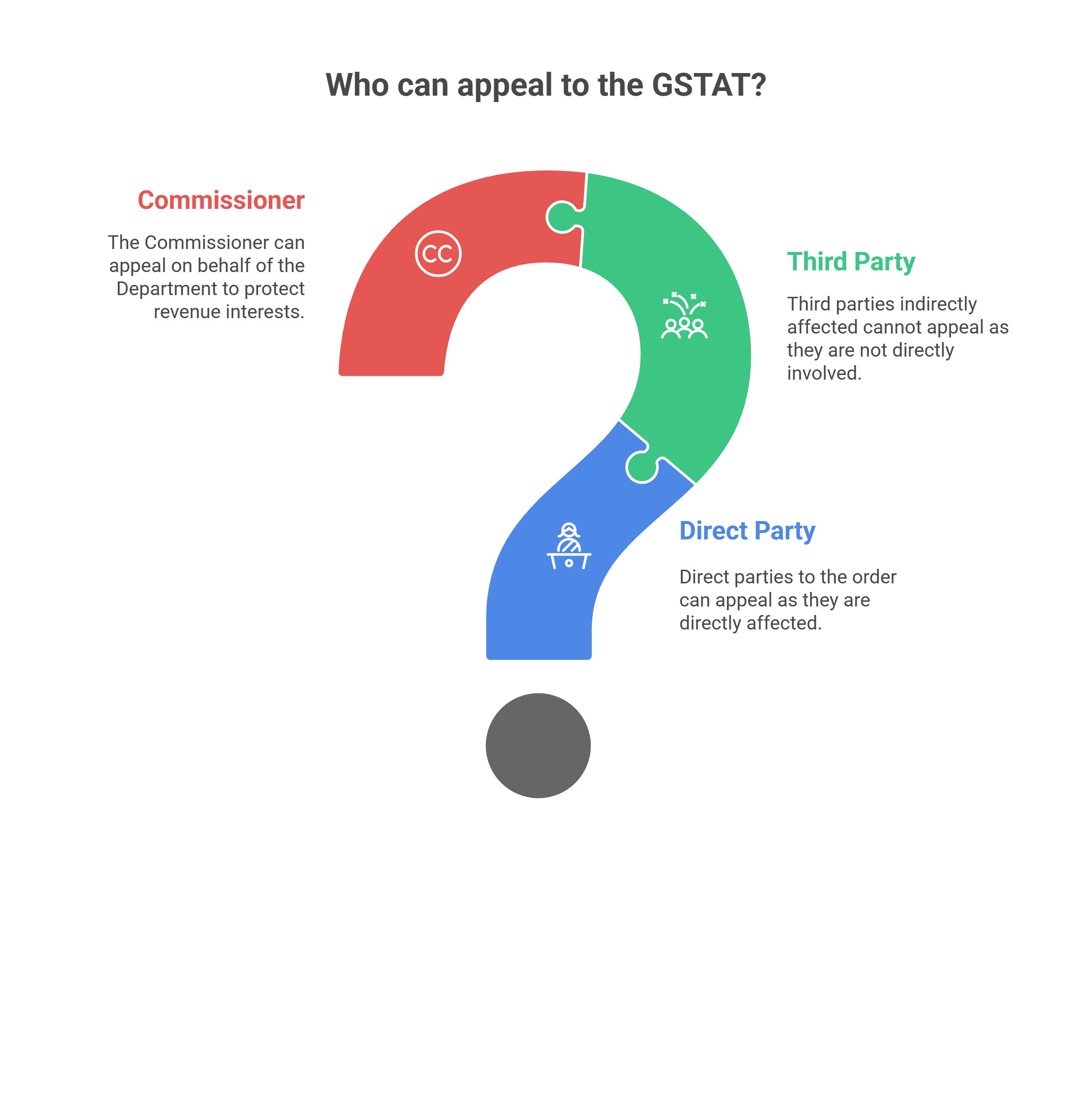

The right to appeal to the GSTAT is granted to "any person aggrieved by an order passed against him." This is a narrower scope compared to the provisions for first appeals. The phrase "aggrieved by an order passed against him" indicates that only the direct parties to the order can file an appeal. This means that third parties who may be indirectly affected by the order, but were not directly involved in the proceedings, generally cannot appeal to the GSTAT.

However, it's important to note that the Commissioner (representing the Department) also has the right to appeal to the GSTAT under Section 112(3) of the CGST Act. This provision allows the Department to challenge orders that are adverse to its interests, ensuring that the revenue's position is adequately represented before the appellate tribunal.

3. Monetary Limits for Departmental Appeals

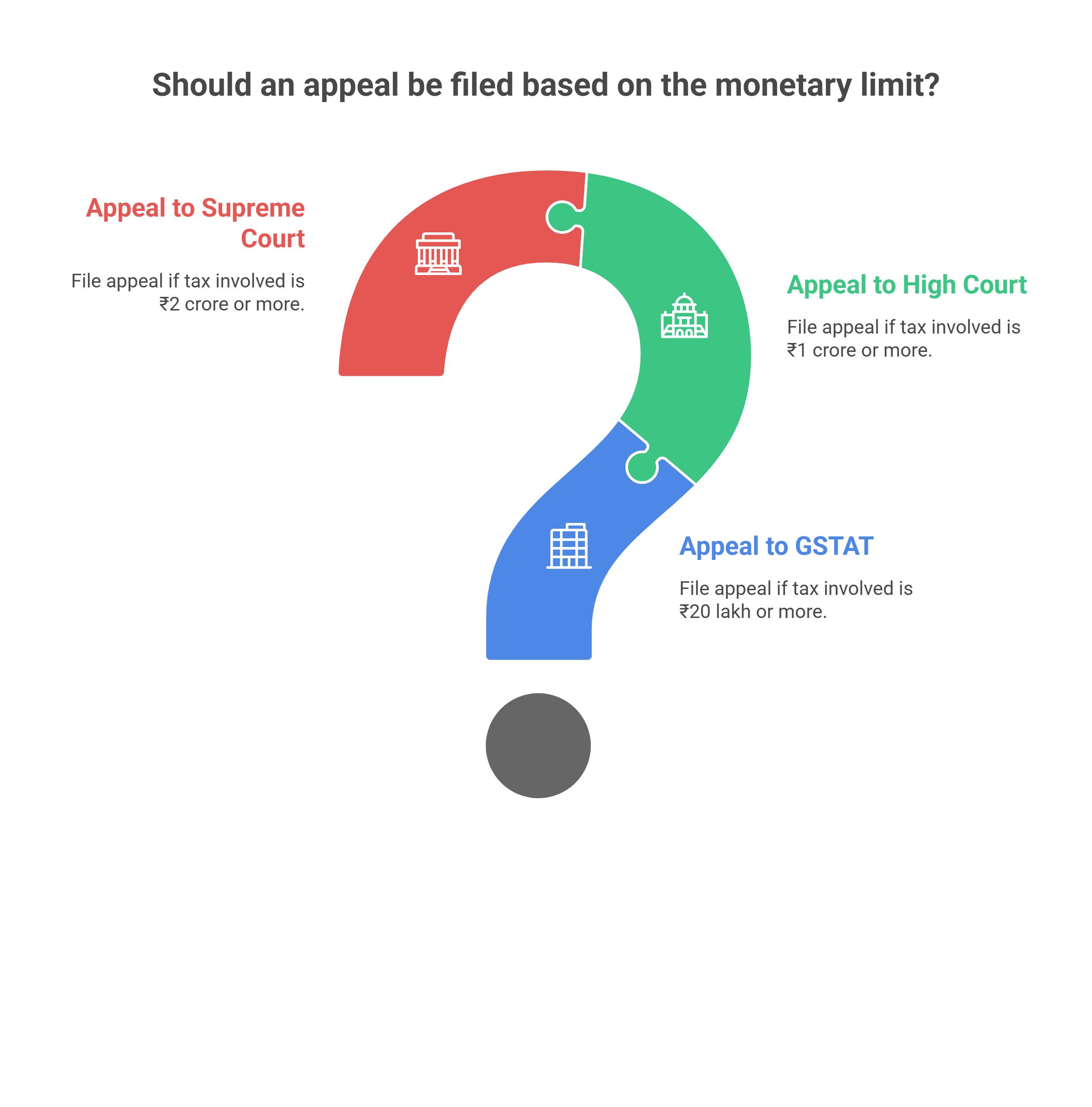

To prevent excessive litigation and focus resources on high-value cases, the GST Council has recommended specific monetary thresholds for departmental appeals. These thresholds are designed to discourage the Department from filing appeals in cases where the tax involved is below a certain amount. The current monetary limits are as follows:

-

Appeals to GSTAT: ₹20 lakh

-

Appeals to High Courts: ₹1 crore

-

Appeals to the Supreme Court: ₹2 crore

These limits mean that the Department should generally not file an appeal if the amount of tax, interest, penalty, etc., involved is less than ₹20 lakh for GSTAT, ₹1 crore for High Courts, and ₹2 crore for the Supreme Court.

If a decision is made not to file an appeal because the amount involved is below the prescribed monetary limit, the reasons for not filing the appeal must be recorded in writing. This record must then be communicated to the GSTAT or the relevant Court. This ensures transparency and accountability in the Department's decision-making process regarding appeals.

Conclusion

In summary, appeals to the GSTAT are governed by specific rules regarding the types of orders that can be appealed, the parties who can file appeals, and the monetary limits for departmental appeals. These provisions are designed to ensure that the appellate process is fair, efficient, and focused on cases of significant value and importance.

Free GST Invoice Generator | Check Invoice Number Online India | E Bill Software | Dry Fruits GST Rate | Maintenance Charges GST

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified