While Section 67 grants extensive powers, the GST framework incorporates several procedural safeguards and related provisions to ensure a balance between enforcement and taxpayer rights:

Reason to Believe: The exercise of powers under Section 67(1) and 67(2) is not arbitrary. It must be predicated on the officer’s “reason to believe,” which necessitates a basis in material facts or information indicating a contravention or evasion.

Access to Business Premises (Section 71): This section allows authorized officers (not below the rank of Joint Commissioner) to access business premises for inspection, scrutiny, verification, and checks. Such officers must present written authorization, and the person in charge is obligated to provide access to records. Non-compliance can result in a penalty of up to .

Production of Documents (Section 70): The proper officer has the authority to summon any person to provide evidence or produce documents relevant to an inquiry. This process mirrors that of a civil court under the Code of Civil Procedure, 1908, and inquiries under this section are considered judicial proceedings.

Officers to Assist Proper Officers (Section 72): To facilitate the implementation of the Act, various government officers, including those from Police, Railways, Customs, and State/Union Territory tax departments, are mandated to assist GST proper officers. The government may also empower other classes of officers to provide assistance.

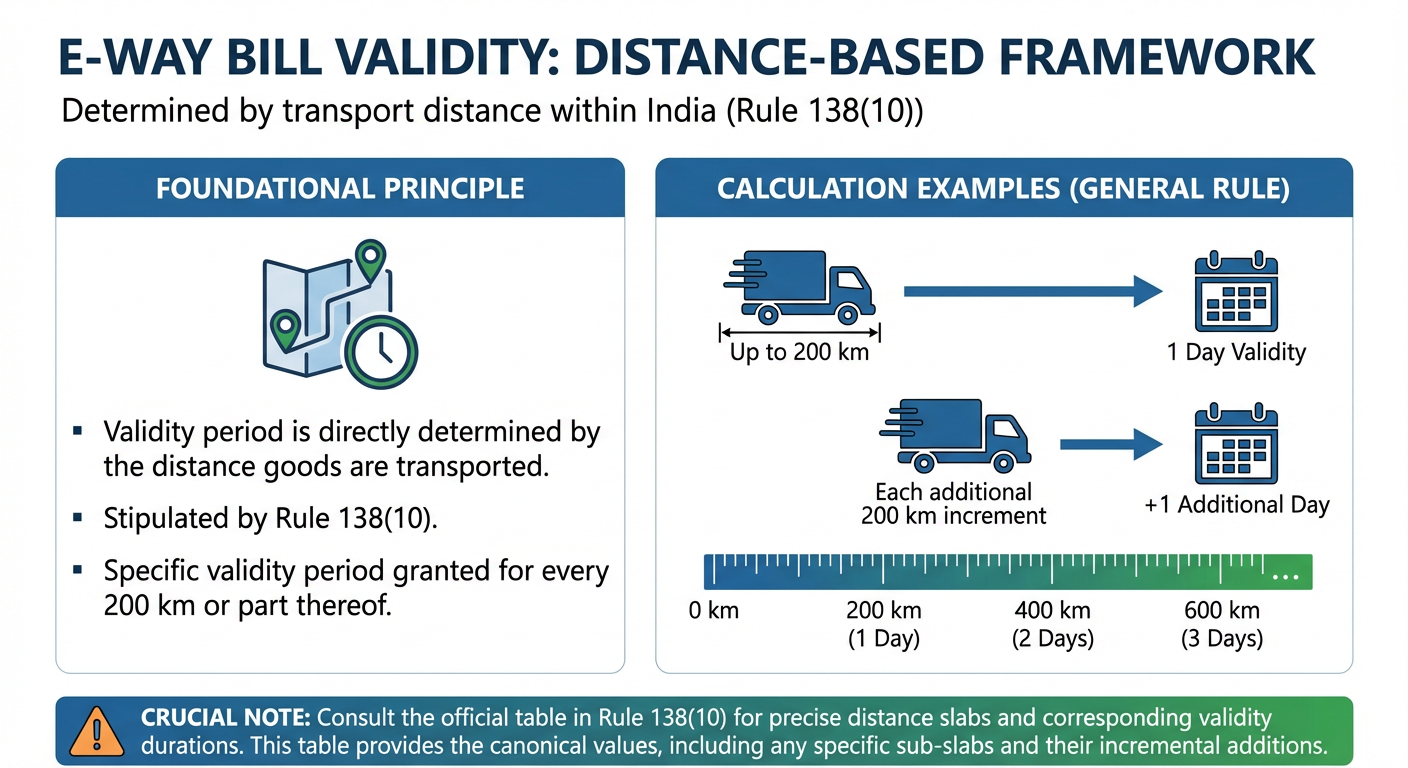

Inspection of Goods in Movement (Section 68): Distinct from Section 67, Section 68 empowers officers to inspect goods in transit. This includes stopping conveyances, demanding production of documents and devices, and inspecting the goods themselves. Non-compliance can lead to penalties or confiscation, particularly in relation to e-way bill requirements for goods exceeding specified values.

In summary, Section 67 provides critical powers for GST administration, but its application is tempered by the principle of ‘reason to believe’ and reinforced by procedural requirements from other sections of the GST Act and the CrPC, thereby ensuring accountability and fairness in its execution.