Provisional Bank Account Attachment Under GST Laws: A Strategic Guide for CFOs and Finance Leaders

Executive Summary

As a CFO or Finance Director, understanding Section 83 of the CGST Act, 2017 is not merely a compliance requirement—it's a critical business continuity imperative. This provision empowers tax authorities to freeze your company's bank accounts provisionally, potentially crippling operations overnight. Recent judicial developments have clarified the boundaries of this power, offering both protection and requiring vigilance from finance leaders.

Key Takeaways for Finance Leaders:

-

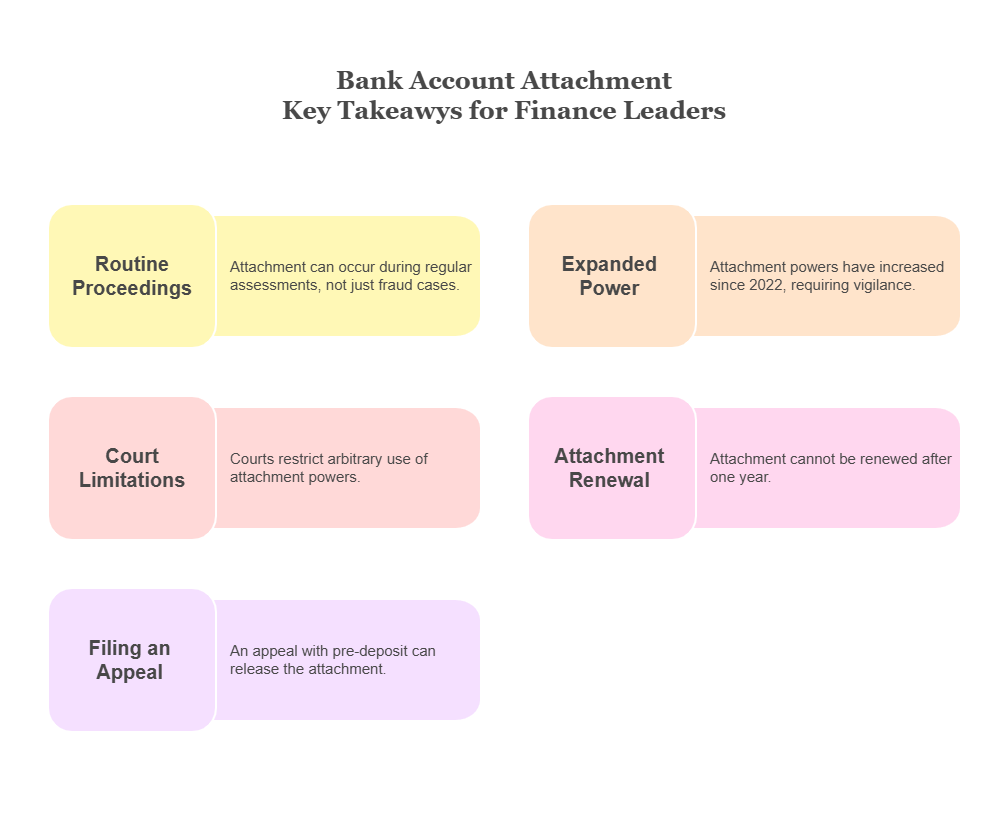

Bank accounts can be attached even during routine proceedings like scrutiny assessments

-

The attachment power has been significantly expanded since 2022

-

Courts have imposed strict limitations on the arbitrary use of this power

-

Renewal of attachment after one year is now legally impermissible

-

Filing an appeal with mandatory pre-deposit can release the attachment

Why CFOs Must Pay Attention: Business Impact

The Goods and Services Tax (GST), implemented on July 1, 2017, fundamentally transformed India's indirect tax landscape. While it simplified the tax structure by replacing VAT, service tax, excise duty, and other levies, it also introduced powerful enforcement mechanisms that can significantly impact business operations.

Section 83's provisional attachment power represents one of the most coercive tools in the GST enforcement arsenal. Unlike traditional recovery proceedings that follow adjudication, this provision allows authorities to freeze assets before determining tax liability. For businesses, this means:

-

Immediate Cash Flow Disruption: Working capital locked without warning

-

Operational Paralysis: Inability to meet payroll, supplier payments, or statutory obligations

-

Reputational Risk: Banking relationships and credit ratings may be affected

-

Strategic Uncertainty: Investment and expansion decisions held hostage

Understanding Section 83: What Finance Teams Need to Know

The Legal Framework Simplified

Section 83(1) grants the Commissioner power to provisionally attach any property, including bank accounts, when:

-

Proceedings are initiated under specified chapters (XII, XIV, or XV)

-

The Commissioner forms an opinion that it's necessary to protect government revenue

-

The attachment is made through a written order

Section 83(2) provides a critical safeguard: any provisional attachment automatically ceases after one year from the date of order.

The 2022 Game Changer: Expanded Scope

Prior to the Finance Act, 2021 (effective January 1, 2022), provisional attachment was limited to specific proceedings like tax evasion investigations. The amendment dramatically widened the net to include:

-

Chapter XII (Sections 59-64): Returns, payment, matching, and assessment processes

-

Chapter XIV (Sections 67-72): Inspection, search, seizure, and arrest

-

Chapter XV (Sections 73-84): Demand and recovery proceedings

What This Means for Your Business: Even routine compliance activities—scrutiny of returns, provisional assessments, or regular audits—can now trigger bank account freezing. The power extends to situations where a simple summons has been issued.

Judicial Guardrails: How Courts Are Protecting Business Interests

1. The "Opinion" Must Be Real, Not Ritualistic

Landmark Supreme Court Guidance: M/s Radha Krishan Industries v. State of Himachal Pradesh [2021 (48) G.S.T.L. 113 (S.C.)]

The Supreme Court established that the Commissioner's opinion must be based on tangible material bearing on the necessity of ordering provisional attachment. Mere suspicion or mechanical reasoning is insufficient.

CFO Implication: If your bank accounts are attached, you have grounds to challenge the order if it lacks substantive reasoning. The attachment order must demonstrate genuine concern about revenue loss, not just boilerplate language.

Action Point for Finance Leaders: Demand copies of attachment orders and scrutinise the reasoning. Engage legal counsel to challenge attachments based on weak or generic justifications.

2. One Year Means One Year: No Renewals Permitted

This is perhaps the most significant recent development for businesses facing prolonged attachment orders.

Breakthrough Case: Kesari Nandan Mobile v. Office of Assistant Commissioner of State Tax [2025] 33 CENTAX 224 (Supreme Court)

Question Before the Court: Can authorities issue a second provisional attachment order after the first one expires after one year?

Supreme Court's Clear Answer: NO. Permitting renewal or fresh attachment would render Section 83(2) meaningless. The one-year limitation is absolute and cannot be circumvented.

Supporting Precedents:

-

Additional Director General, DGGI Kochi v. Ali K. [2025] 27 Centax 209 (Kerala High Court)

-

The Finance Act, 2021 amended Section 83(1) but deliberately left sub-section (2) untouched

-

This reflects legislative intent to restrict provisional attachment strictly to one year

-

Taxation laws cannot be interpreted beyond their explicit language

-

-

Smt. Lalita v. Union of India and Anr. (Writ Tax No. 4082 of 2025) (Allahabad High Court)

-

Court quashed an attachment order issued for the fourth consecutive time

-

Applied the Supreme Court's ratio from Kesari Nandan Mobile case

-

Strategic Implication for CFOs: If your bank accounts have been under provisional attachment for one year:

-

The attachment automatically lapses by law

-

Any fresh attachment order is legally invalid

-

You can immediately approach the High Court for relief

-

Maintain precise records of attachment dates for evidence

Risk Mitigation Strategy: Implement calendar alerts at the 11-month mark to proactively challenge any attempted renewal.

3. Appeal with Pre-Deposit = Attachment Automatically Ends

Leading Case: Radha Krishan Industries v. State of Himachal Pradesh [2021 (48) G.S.T.L. 113 (S.C.)]

Supreme Court's Reasoning:

-

Provisional attachment is valid only during pending proceedings

-

Once an Order in Original is passed against a Show Cause Notice (SCN), proceedings under Section 74 are deemed completed

-

When an appeal is filed with a mandatory pre-deposit, the proceedings are no longer pending

-

Therefore, provisional attachment must cease to subsist

Reinforcing Precedent: M/s MJ Bizcrafts LLP v. Central Goods and Services Tax, Delhi South Commissionerate [2025] 32 Centax 451 (Delhi High Court)

The Delhi High Court explicitly held that once an appeal is filed after making the mandatory 10% pre-deposit, the provisional attachment order is not sustainable, and bank accounts must be unfrozen.

CFO's Playbook:

-

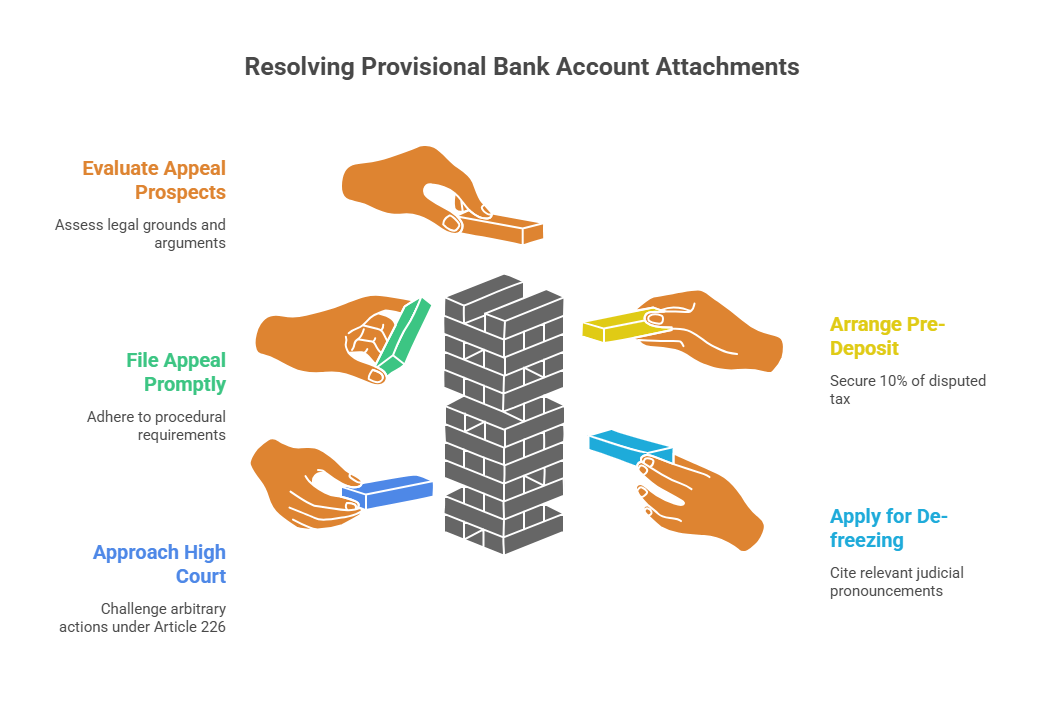

When you receive an Order in Original demanding GST payment, evaluate appeal prospects immediately

-

Arrange for the 10% pre-deposit (this is mandatory for appeal filing)

-

File the appeal promptly with the Appellate Authority

-

Simultaneously file an application for de-freezing bank accounts, citing these judgments

-

If authorities refuse, approach the High Court under Article 226 of the Constitution

Cash Flow Consideration: While arranging 10% pre-deposit requires capital, it's often strategically better than having 100% of your bank balance frozen indefinitely.

4. Only the Taxable Person's Account Can Be Attached

Case: Sakshi Bahl v. The Principal Additional Director General [W.P. (C) 3986/2023] Delhi High Court [2023 TaxoNation 356 (Del.)]

Court's Protection: Section 83 empowers authorities to attach bank accounts only of:

-

The taxable person (the registered entity)

-

Persons specified under Section 122(1A) of CGST Act (certain related parties in fraud cases)

What the Court Prohibited: Authorities cannot attach bank accounts of third parties based on mere assumptions that funds belong to the taxable person.

Critical Implications for Group Companies and Promoters:

If you're a CFO of a group with multiple entities or if promoters have personal accounts:

-

Separate entities = Separate legal identities: Tax department cannot freeze subsidiary accounts for parent company's GST issues (unless fraud is established under Section 122(1A))

-

Personal accounts of directors/promoters: Generally protected unless they fall within Section 122(1A)'s specific categories

-

Nominee accounts: Cannot be attached without establishing beneficial ownership

Defensive Strategy:

-

Maintain clear segregation of business and personal finances

-

Ensure proper documentation of inter-company transactions

-

Avoid commingling of funds across group entities

-

Keep contemporaneous records proving ownership of bank balances

Procedural Requirements: What Actually Happens

Attachment Process (Rule 159 of CGST Rules)

Understanding the mechanics helps finance teams respond effectively:

Step 1: Order Issuance

-

Commissioner passes order in Form GST DRC-22

-

Must specify details of the property being attached

Step 2: Communication to Bank

-

Copy of attachment order sent to the bank

-

Bank places an encumbrance on the account

-

Removal only upon written instructions from the Commissioner

Step 3: Special Provisions

-

Perishable/Hazardous Goods: Can be released if you pay an amount equivalent to the market price or potential tax liability (whichever is lower)

-

If not paid, the Commissioner may dispose of such property and adjust proceeds against tax dues

Step 4: Objection Mechanism

-

You can file objections in Form GST DRC-22A

-

The commissioner must provide an opportunity of being heard

-

If satisfied, the Commissioner may release property via Form GST DRC-23

CFO Action Framework: Proactive and Reactive Measures

Preventive Measures

1. Enhanced GST Compliance Protocols

-

Implement real-time GST reconciliation systems

-

Monthly reviews of input tax credit claims and utilisation

-

Quarterly compliance audits by external GST consultants

-

Maintain comprehensive supporting documentation for all transactions

2. Early Warning Systems

-

Track all GST notices, SCNs, and summons meticulously

-

Understand which proceedings can trigger Section 83 attachment

-

Maintain a "GST Risk Register" tracking open proceedings

-

Conduct periodic self-assessments of exposure areas

3. Treasury Management

-

Diversify banking relationships (maintain accounts with multiple banks)

-

Keep emergency working capital reserves in accounts held by related but separate legal entities (within legal bounds)

-

Establish credit lines that can be activated quickly if main accounts are frozen

-

Consider keeping operational funds in accounts with lower balances, while maintaining reserves elsewhere

4. Documentation Excellence

-

Maintain contemporaneous records of all business decisions affecting GST

-

Document commercial rationale for transactions that may appear questionable

-

Preserve email trails, board minutes, and approval workflows

-

Ensure all input tax credit claims are backed by proper invoices and reconciliation

Reactive Response Protocol

When Bank Accounts Are Attached:

Immediate Actions (Day 1-3):

-

Obtain copy of the attachment order (Form GST DRC-22)

-

Convene an emergency meeting with legal counsel, tax advisors, and senior management

-

Assess immediate cash requirements for critical operations

-

Activate alternative funding arrangements

-

Communicate with key stakeholders (banks, creditors, employees) as appropriate

Legal Strategy (Week 1):

-

Analyse attachment order for legal deficiencies:

-

Is the "opinion" properly reasoned with tangible material?

-

Is there genuine risk to revenue, or is it a mechanical exercise of power?

-

Are proceedings still pending, or have they concluded?

-

Has one year elapsed since any previous attachment?

-

-

File objection under Rule 159(4) in Form GST DRC-22A

-

Simultaneously prepare a writ petition for the High Court if:

-

Attachment is arbitrary or unreasoned

-

One-year period has expired

-

Appeal has been filed with pre-deposit

-

Third-party accounts wrongly attached

-

Negotiation Track (Weeks 1-2):

-

Engage with tax authorities through senior counsel

-

Offer a voluntary deposit or bank guarantee as an alternative to attachment

-

Seek partial release of funds for critical operations

-

Demonstrate genuine compliance intent and lack of flight risk

Appellate Strategy (if SCN/Order exists):

-

Evaluate the merits of filing an appeal

-

Arrange 10% mandatory pre-deposit

-

File an appeal before the Appellate Authority

-

Apply for de-attachment citing Radha Krishan Industries and MJ Bizcrafts precedents

Red Flags That May Trigger Section 83 Attachment

Finance leaders should be especially vigilant when:

-

High-value ITC claims without proportionate turnover growth

-

Frequent amendments to returns, especially reducing output tax liability

-

Significant refund claims, particularly IGST refunds or inverted duty structure refunds

-

Transactions with blacklisted parties or entities with suspended GST registration

-

Mismatches in GSTR-2A/2B reconciliation

-

Classification disputes involving substantial tax differential

-

Place of supply issues in services, especially in e-commerce

-

Investigation into the supply chain, even if your company is not the primary target

-

Round-tripping transactions or circular trading patterns

-

Non-response to notices or SCNs from GST authorities

Financial Planning Considerations

Impact on Financial Statements

Balance Sheet Implications:

-

Frozen bank balances: Disclose as "restricted cash" in notes

-

Contingent liability: Recognise and disclose underlying tax demand

-

Going concern assessment: Material freezing may trigger going concern disclosures

Cash Flow Management:

-

Model scenarios with varying attachment durations (3 months, 6 months, 1 year)

-

Stress-test ability to meet obligations without attached funds

-

Consider impact on debt covenant compliance (especially working capital ratios)

Credit Ratings and Banking:

-

Proactively communicate with lenders and rating agencies

-

Provide context and legal position

-

Demonstrate alternative liquidity sources

Insurance and Indemnification

Consider:

-

Tax liability insurance for large transactions or restructuring

-

Directors and Officers (D&O) insurance covering tax proceedings

-

Indemnification clauses in M&A agreements for legacy GST issues

Recent Developments and Future Outlook

Increasing Use of Section 83

Data suggests revenue authorities are increasingly utilising provisional attachment powers:

-

Faster initiation of attachment proceedings

-

Attachment at earlier stages (even at summons/inspection stage)

-

Higher attachment amounts relative to disputed tax

Legislative and Regulatory Watch

Areas requiring monitoring:

-

Potential amendments to Section 83 in response to restrictive judicial interpretations

-

CBIC circulars or instructions on exercise of attachment powers

-

Emerging patterns in tax authority behaviour post-Kesari Nandan Mobile judgment

Technology Solutions

Progressive finance teams are implementing:

-

GST compliance automation tools with AI-powered reconciliation

-

Predictive analytics to identify high-risk transactions before filing returns

-

Digital documentation systems for instant retrieval during audits or proceedings

-

Dashboard monitoring of pending proceedings and attachment risks

Conclusion: Balancing Compliance and Business Continuity

Section 83's provisional attachment power represents a significant business risk that demands CFO-level attention and strategic management. While the provision serves legitimate revenue protection objectives, recent judicial decisions have established important guardrails against arbitrary exercise.

Key Principles for Finance Leaders:

-

Prevention is Better Than Cure: Robust GST compliance frameworks significantly reduce attachment risk

-

Early Detection Matters: Monitoring proceedings and understanding triggers enables a proactive response

-

Know Your Rights: Judicial precedents provide strong defences against arbitrary attachment

-

One Year is Absolute: No renewal or extension of attachment beyond one year is legally permissible

-

Appeal Strategy Works: Filing an appeal with pre-deposit can secure the release of attached funds

-

Documentation is Defence: Comprehensive records are your best protection

Strategic Imperatives:

-

Elevate GST compliance from tax department function to an enterprise risk management issue

-

Build cross-functional teams (finance, legal, operations, IT) for GST risk management

-

Invest in technology and expertise for proactive compliance

-

Maintain liquidity cushions and alternative funding sources

-

Engage experienced GST counsel for high-risk situations

The courts have made clear that provisional attachment is an extraordinary safeguard, to be invoked sparingly and only in exceptional circumstances. As a CFO, your role is to ensure your organisation operates within compliance boundaries while being prepared to assert legal rights vigorously if arbitrary action is taken.

In the evolving GST landscape, those finance leaders who treat Section 83 as a strategic business risk—rather than a purely legal or tax matter—will best position their organizations for both compliance and growth.

Disclaimer: This article is for informational purposes only and does not constitute legal advice. Organisations should consult with qualified GST counsel for specific situations.

DRC-01a format | GST anti evasion department powers | How to reply for asmt-13 | Power of gst inspector | GST audit procedure | GST audit process

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified