Section 164 of the CGST Act, 2017 – Power of Government to Make Rules

1. Overview

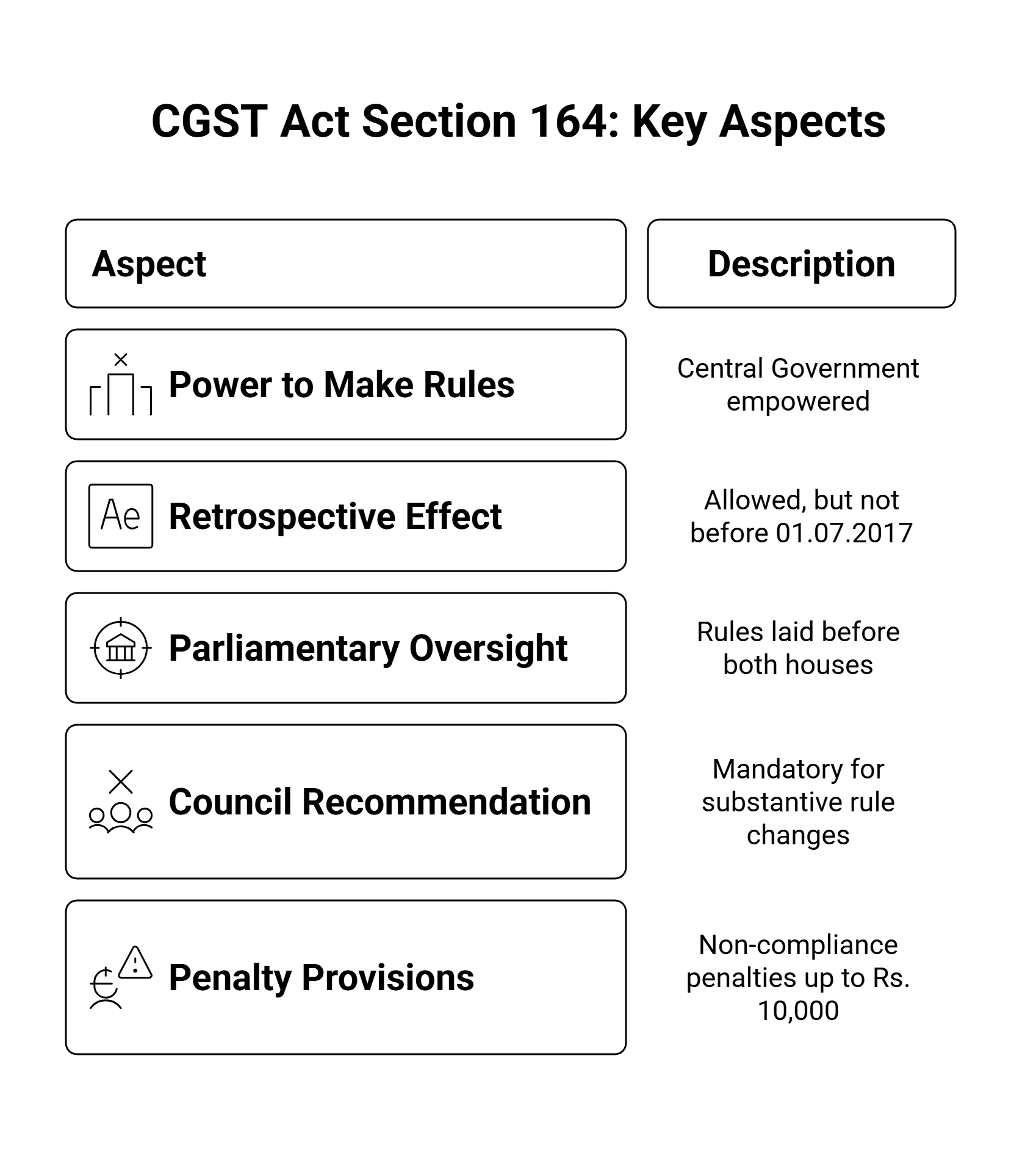

Section 164 of the Central Goods and Services Tax Act, 2017 (CGST Act) empowers the Central Government to make rules for carrying out the provisions of the Act. This section plays a critical role in the GST law framework, as the operation and implementation of many statutory provisions depend on rules made under this authority.

2. Text of Section 164 – Key Provisions

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

- Section 164 is the cornerstone provision granting the Central Government broad powers to notify rules, including with retrospective effect, but not before 01.07.2017 (date of commencement).

- All subsidiary rules made under this section are subject to prior recommendations of the GST Council.

- Any such rules must also be laid before Parliament (see Section 166).

3. Relevant GST Rules and Their Link to Section 164

Central Goods and Services Tax Rules, 2017 and all subsequent amendments are issued under Section 164.

Rule-making power is exercised for various operational aspects, including:

- Registration (Rules 1–27)

- Tax invoice and records (Rules 46–56)

- Returns (Rules 59–67A)

- Input tax credit (Rules 36–45)

- Recovery, refund, assessment, appeals, etc.

Select Example Notification under Section 164:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

All notifications amending the CGST Rules, 2017, specifically mention Section 164 as the empowering provision.

4. Procedural Safeguards – Laying Before Parliament

Section 166, CGST Act:

- All rules made under section 164 must be laid before both houses of Parliament.

- Ensures transparency and Parliamentary oversight.

5. Practical Implications & Examples

- Retrospective Rule-Making:

- Rules may be issued with effect from a back date, but not before 01.07.2017.

- Example: Refund provisions under Rule 89(5) were amended retrospectively via notifications, based on Section 164(3).

- Penalty Provisions in Rules:

- Certain GST Rules specify penalties for non-compliance, not exceeding Rs. 10,000, as per Section 164(4).

- Council’s Recommendation Mandatory:

- All substantive rule changes must be placed before the GST Council for recommendation prior to notification.

6. Table: Salient Aspects of Section 164

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7. Recent Developments

- Notification & Amendments:

- All major amendments to GST Rules in 2023 and 2024 (relating to e-invoicing, special procedures, etc.) have been made under Section 164.

- GST Council Recommendations:

- Section 164 acts in synergy with the recommendations of the GST Council (see GST notifications and recent GST Council decisions for 2024 proposals).

Conclusion: Key Takeaways

- Section 164 is the enabling provision for all rule-making under the GST law.

- Retrospective effect is allowed but only from the date of commencement of CGST Act.

- Mandatory recommendation of the GST Council is required for all rules.

- Rule amendments (registration, returns, e-invoicing, ITC, etc.) are notified under this provision.

- Parliamentary oversight is ensured under Section 166.

- Penalties under the rules are limited as per Section 164(4).

- No major litigation directly on its validity; it is foundational to GST’s legislative ecosystem.

For professionals: Always review the latest rules and notifications issued under Section 164 for compliance and procedural updates in GST.

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified