Optimising Working Capital under GST: Credit Blocks, Refunds, and Cash-Flow Strategies

Optimising Working Capital under GST

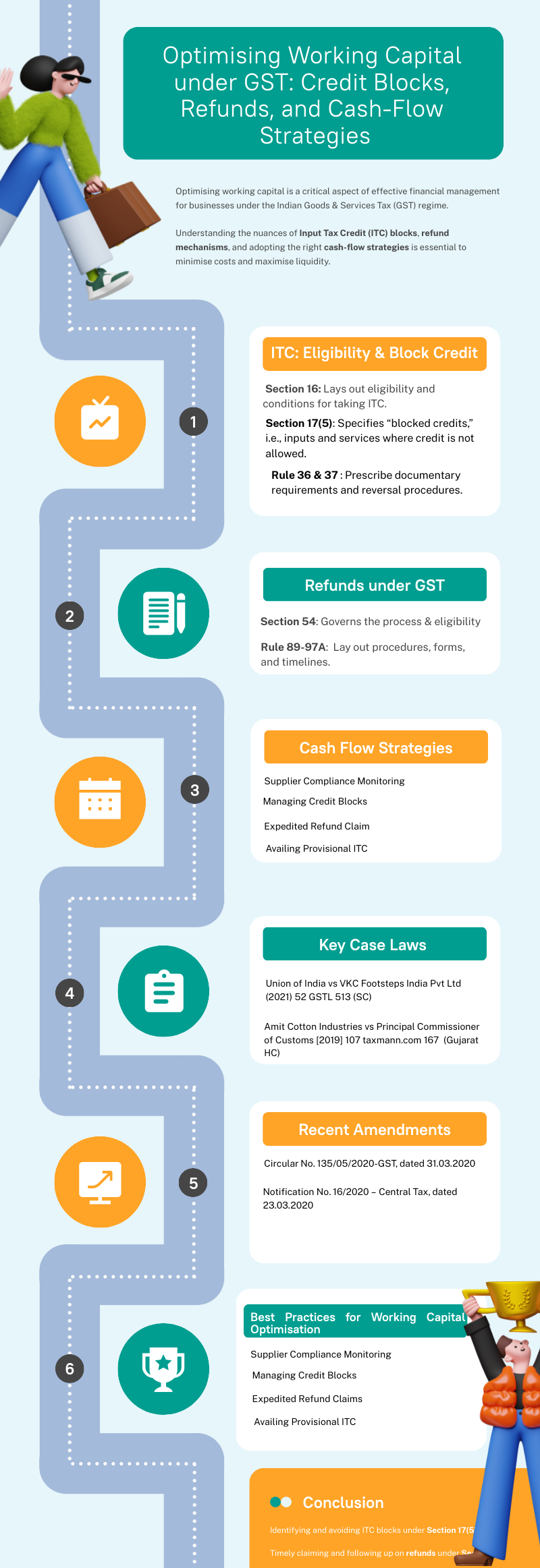

Optimising working capital is a critical aspect of effective financial management for businesses under the Indian Goods & Services Tax (GST) regime. Understanding the nuances of Input Tax Credit (ITC) blocks, refund mechanisms, and adopting the right cash-flow strategies is essential to minimise costs and maximise liquidity.

1. Input Tax Credit (ITC) – Eligibility and Credit Blocks

Relevant Sections & Rules

-

Section 16 of CGST Act, 2017: Lays out eligibility and conditions for taking ITC.

-

Section 17(5) of CGST Act, 2017: Specifies “blocked credits,” i.e., inputs and services where credit is not allowed.

-

Rule 36 & 37 of CGST Rules, 2017: Prescribe documentary requirements and reversal procedures.

Key Provisions

|

|

|

|

|

|

|

|

|

|

|

|

Recent Amendments

-

Notification No. 40/2019 – Central Tax, dated 29.11.2019: ITC restriction to 20% of eligible credit as per GSTR-2A, later reduced to 5% via Notification No. 94/2020 – Central Tax, dated 22.12.2020.

2. Refunds under GST

Relevant Provisions

-

Section 54 of CGST Act, 2017: Governs the process and eligibility for claiming refunds.

-

Rule 89 – 97A of CGST Rules, 2017: Lay out procedures, forms, and timelines.

Types of Refunds

-

Refund of ITC on exports (zero-rated supplies) without payment of tax

-

Refund of taxes in case of inverted duty structure

-

Refunds due to excess payments or mistake

-

Refunds on account of year-end or volume based discounts

Key Case-Law

-

Union of India vs VKC Footsteps India Pvt Ltd (2021) 52 GSTL 513 (SC): Supreme Court upheld that only inputs (not input services) are eligible for refund under the inverted duty structure.

-

Amit Cotton Industries vs Principal Commissioner of Customs [2019] 107 taxmann.com 167 (Gujarat HC): Clarified eligibility and procedural aspects regarding refund of unutilized ITC.

Recent Amendments & Circulars

-

Circular No. 135/05/2020-GST, dated 31.03.2020: Restricts refund claims to proportionate ITC pertaining to the zero-rated supply.

-

Notification No. 16/2020 – Central Tax, dated 23.03.2020: Prescribes that the refund of accumulated ITC on account of an inverted duty structure is not allowed for certain products.

3. Cash-Flow Strategies

Best Practices for Working Capital Optimisation

-

Supplier Compliance Monitoring

-

Verify timely filing of GSTR-1 and GSTR-3B by suppliers to ensure ITC eligibility.

-

Use internal tools or third-party solutions to reconcile 2A/2B/8A reports.

-

-

Managing Credit Blocks

-

Avoid procurement of goods/services falling under Section 17(5) blocks, unless business justification or alternate structuring is feasible.

-

Plan capex and Capex activities considering ITC eligibility.

-

-

Expedited Refund Claims

-

File timely refund applications; periodically reconcile electronic credit and cash ledgers.

-

Maintain robust documentation to avoid delays or rejections.

-

-

Availing Provisional ITC

-

Use the allowed provisional ITC judiciously (currently restricted to 5%) until matched invoices are uploaded by suppliers.

-

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Comparative Table: ITC Block vs Eligible ITC

4. Practical Steps and Recommendations

-

Periodic Vendor Communication: Clarify the importance of timely return filing for ITC claim.

-

Automate GST Reconciliation: Invest in technology to quickly identify and reconcile mismatches.

-

Plan High Value Purchases: Schedule capital-intensive purchases to maximise credit flow.

-

Follow Latest Notifications: Stay updated with changes in the GST law, especially amendments impacting credit eligibility and refunds.

Conclusion

Optimising working capital under GST hinges on:

-

Identifying and avoiding ITC blocks under Section 17(5)

-

Timely claiming and following up on refunds under Section 54

-

Implementing robust internal and technology-driven cash-flow strategies

Frequent amendments and evolving case laws necessitate continuous monitoring. Businesses should conduct regular GST health-checks to ensure all eligible credits are availed, refund opportunities are not missed, and cash outflows are minimised.

For expert assistance or further clarifications, consult GST professionals or reach out to your GST consultant.

Online Invoice Generator GST | GST Invoice Check Online | E Invoice Software India | Online GST Software | E Way Bill Developer Portal

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified