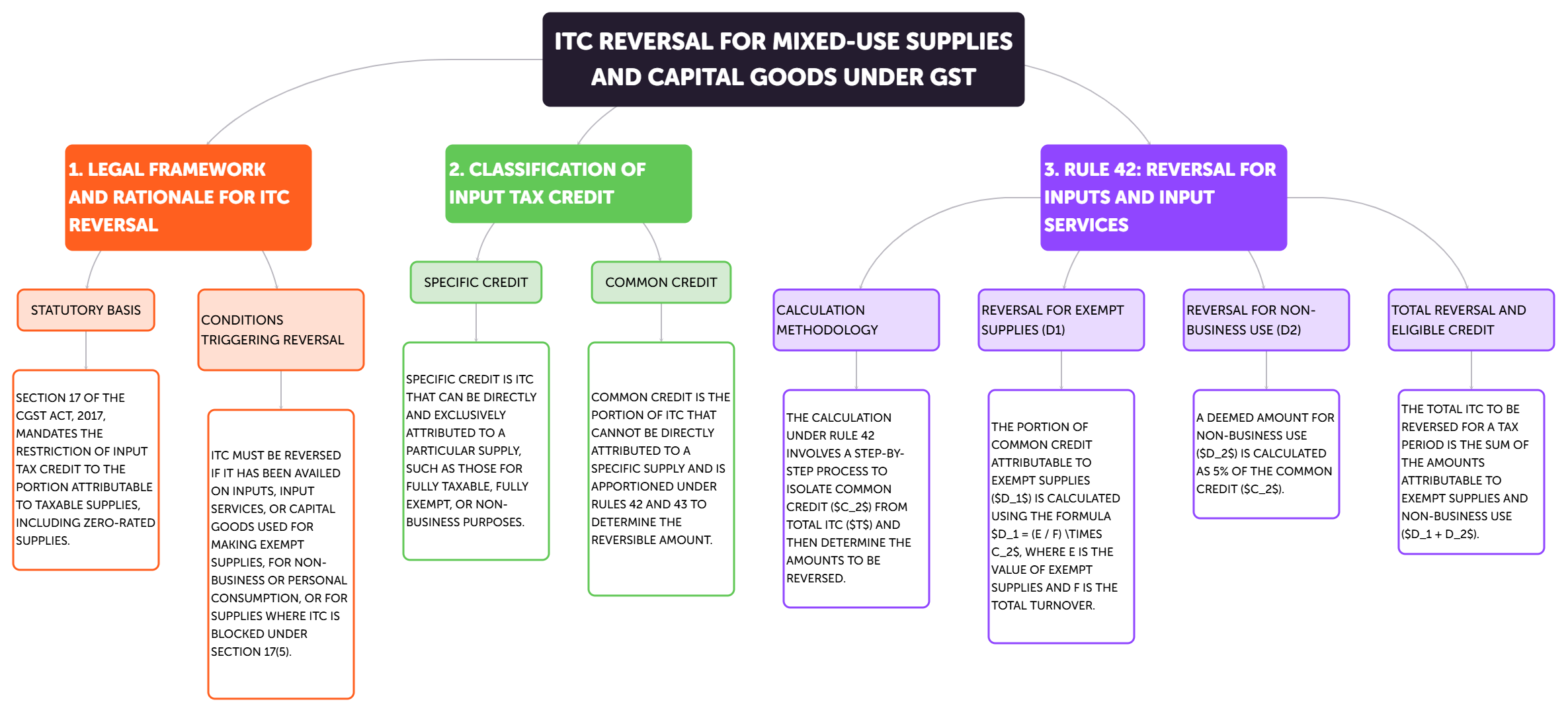

Rule 42 and the concept of ITC reversal under GST

What is Rule 42?

Rule 42 of the Central Goods and Services Tax (CGST) Rules, 2017 pertains to the reversal of Input Tax Credit (ITC) in situations where goods or services are used both for:

- Business and non-business purposes

- Taxable (including zero-rated) and exempt supplies

If you use goods or services for both purposes, you cannot claim full ITC; you must proportionately reverse (i.e., pay back) the ITC attributable to non-business purposes and exempt supplies.

How is ITC reversal calculated under Rule 42?

Steps:

1. Total ITC on Inputs/Input Services is identified (T).

2. ITC attributable to non-business use (T1) – Directly identified and not available.

3. ITC attributable to exempt supplies (T2) – Directly identified and not available.

4. Remaining ITC after T1 and T2 (C1 = T – T1 – T2).

5. ITC on inputs used exclusively for taxable supplies (T3) – Credit is fully available.

6. Common Credit (C2 = C1 – T3) – Credit on goods/services commonly used for both taxable & exempt supplies.

Proportionate Reversal:

- ITC attributable to exempt supplies = (Exempt Turnover ÷ Total Turnover) × Common Credit (C2)

- ITC attributable to non-business use = 5% of Common Credit (C2)

Total ITC to be reversed = ITC for exempt supplies + ITC for non-business use

What is ITC Reversal?

ITC Reversal means:

- When you have claimed ITC earlier, but then you use the goods/services partly for exempt supplies or non-business purposes, the proportionate ITC corresponding to such usage needs to be reversed (i.e., paid back to the government).

Practical Example:

Suppose, during a month:

- Total ITC on input services: ₹10,000 (T)

- ITC on services used exclusively for exempt supplies: ₹2,000 (T2)

- ITC on services used exclusively for taxable supplies: ₹5,000 (T3)

- Remaining is common credit (used for both): ₹10,000 – ₹2,000 – ₹5,000 = ₹3,000 (C2)

If the exempt turnover is 20% of the total turnover for the month:

- ITC to be reversed for exempt supply = 20% of ₹3,000 = ₹600

ITC to be reversed for non-business use = 5% of ₹3,000 = ₹150

Total ITC to be reversed = ₹600 + ₹150 = ₹750

Summary Table:

| Turnover Type | ITC Type | ITC Allowed / Reversed |

| Taxable Use Only | Full ITC allowed (T3) | Allowed |

| Tax + Exempt/Non-b | Proportionate Reversal applies | Partly Reversed (Rule 42) |

| Exempt Use Only | No ITC allowed (T2) | Reversed/Not Claimed |

Rule ITC Reversal Under GST

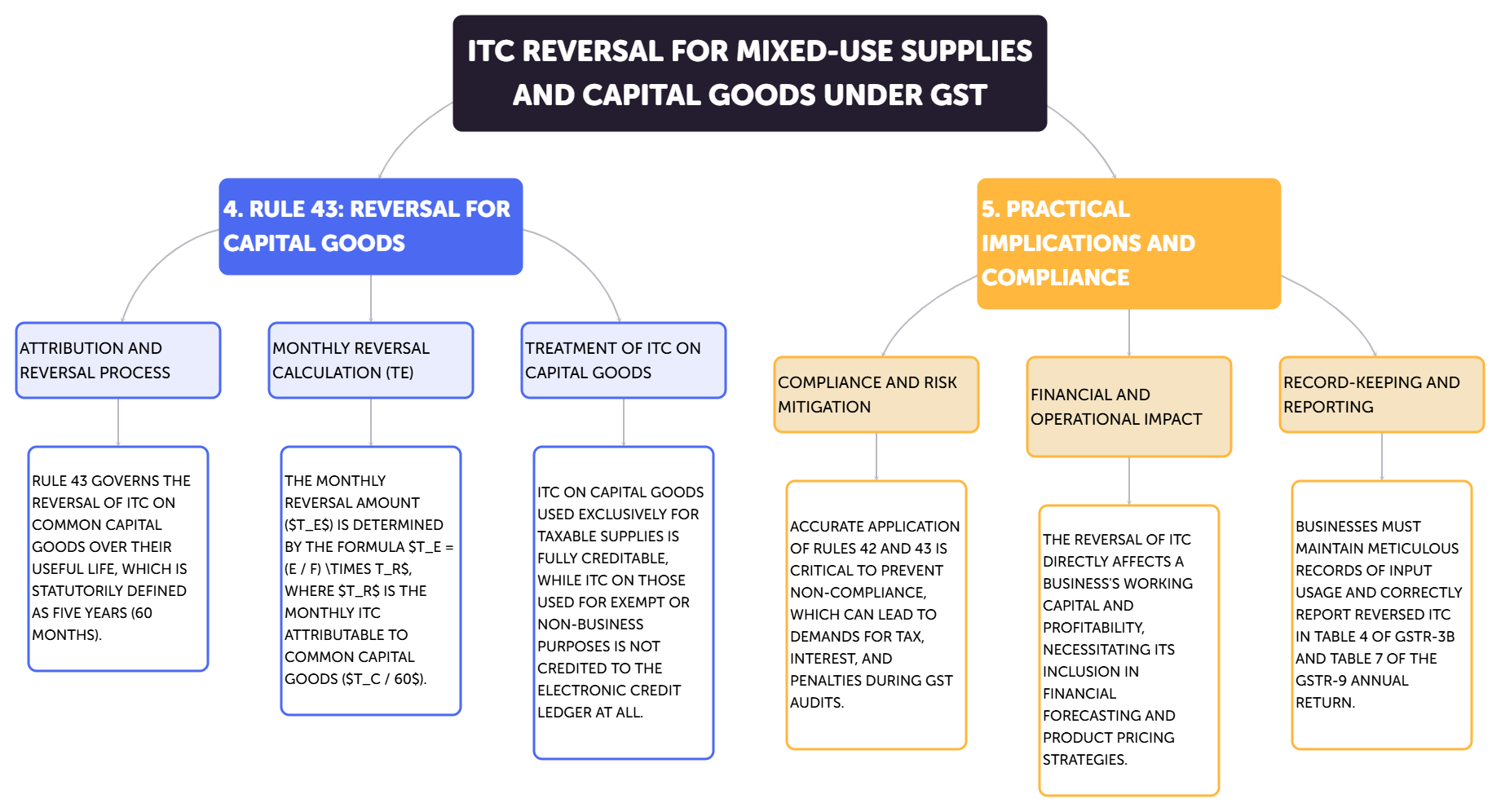

"ITC reversal" under GST is the broader concept governed by Rule 42 (inputs/input services) and Rule 43 (capital goods). Whenever you use inputs, input services, or capital goods in making both taxable and exempt supplies, or for business and non-business purposes, you must reverse the proportionate ITC.

Key Points:

1. Reversal is done monthly (final adjustment annually).

2. Non-compliance attracts interest & penalty.

3. Disclosure: ITC reversal details must be filled in GSTR-3B return.

Difference between Rule 42 and Rule 43

Rule 42: Inputs and Input Services

Applies to: Input Tax Credit (ITC) on inputs and input services.

Inputs are raw materials, components, etc., used to manufacture goods or provide services.

Input services are services used by a registered person for their business (e.g., accounting services, repairs, etc.).

Purpose: Specifies the methodology for determining the amount of ITC that needs to be reversed when inputs and input services are used for:

Business and non-business purposes.

Making taxable (including zero-rated) and exempt supplies.

Calculation: The reversal is based on a formula involving the proportion of exempt turnover to total turnover. It considers ITC that's exclusively for taxable or exempt supplies, segregates the Common Credit (used for both), and allocates the reversal portion.

Frequency: Adjustments and reversals are to be made monthly.

Rule 43: Capital Goods

Applies to: Input Tax Credit (ITC) on capital goods.

Capital goods are assets used in the business with a useful life of more than one year (e.g., machinery, equipment, computers).

Purpose: To determine the ITC reversal on capital goods when they are used for both:

Making taxable (including zero-rated) and exempt supplies. (Note: Rule 43 primarily deals with taxable vs exempt supplies and doesn't directly address business/non-business use. Any capital goods used for non-business purposes would likely disqualify ITC claim altogether.)

Calculation: The calculation for capital goods differs from that for inputs/input services. It factors in the asset's remaining useful life.

Key steps:

1. Determine the common credit: Total ITC on the capital asset.

2. Calculate monthly common credit: Divide the total ITC by 60 (assuming a useful life of 5 years, or 60 months).

3. Reverse ITC based on exempt supplies: Multiply the monthly common credit by the ratio of exempt turnover to total turnover for the tax period.

Frequency: Adjustments are also made monthly.

Key Differences Summarised:

| Feature | Rule 42 (Inputs/Input Services) |

Rule 43 (Capital Goods) |

| Applies To | Inputs and Input Services | Capital Goods |

| Primary Focus | ITC reversal when inputs/services are used for: business & non-business and taxable & exempt supplies. | ITC reversal when capital goods are used for taxable & exempt supplies. |

| Calculation | Complex formula involving identifying direct ITC, common credit, and turnover ratio. | Amortises ITC over 60 months, then reverses the portion based on the exempt turnover ratio. |

| Formula Aspect | Considers direct attribution, common credit distribution based on turnover and even a 5% mandatory reversal for non-business use from the common credit. | Focuses on the common credit from capital goods and distributing a monthly portion for reversal based on the proportion to exempt turnover. |

In simpler terms:

Rule 42 applies to your everyday purchases (raw materials, services) that might be used for taxable or exempt activities.

Rule 43 is for your longer-term assets (machinery, computers) that might also be used for both taxable and exempt activities.

Example to Illustrate the Difference:

Rule 42 example: A bakery buys flour (input) and pays for accounting services (input service). Some of their baked goods are taxable, and some are exempt (e.g., certain types of bread). They must reverse some of the ITC on the flour and on accounting services under Rule 42.

Rule 43 example: The same bakery buys a new oven (a capital good). If they use the oven to bake both taxable cakes and exempt bread, they must reverse a portion of the ITC on the oven under Rule 43.

In Conclusion:

Both rules are essential to ensuring that businesses claim ITC only on inputs, input services, and capital goods used to make taxable supplies. They prevent businesses from claiming full ITC and unfairly benefiting from exempt supplies.

Matching reversal and reclaim of ITC | ITC 03 time limit | GST set off new rules’ notification | Supreme court ITC to be given to the purchaser even if tax is not deposited by seller | ITC on staff welfare expenses | ITC on uniform expenses

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified