GSTAT E-Filing: Staggered Timelines & Limitation Rules Under Section 112 Explained

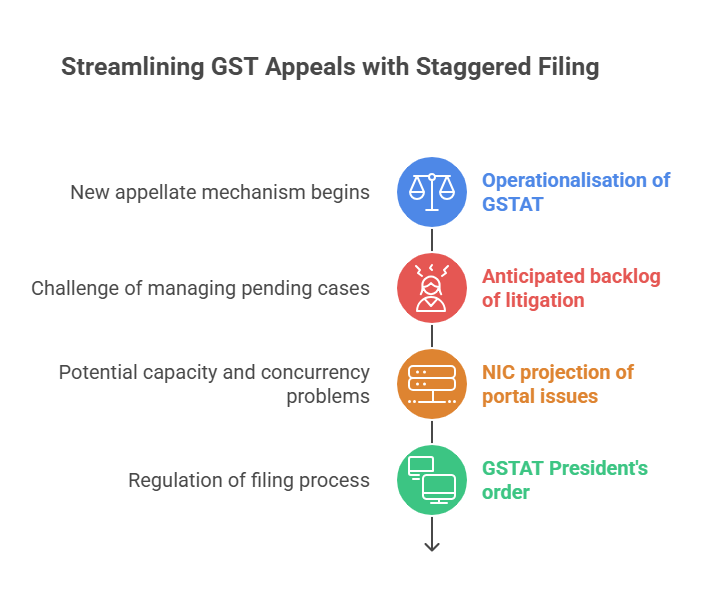

The operationalisation of the Goods and Services Tax Appellate Tribunal (GSTAT) marks a significant milestone in the maturation of India's GST framework. However, the commencement of this new appellate mechanism brings the challenge of managing a substantial backlog of pending litigation. With a large volume of appeals anticipated from both assesses and the Revenue against orders passed by the First Appellate Authorities (FAA) and Revisional Authorities, the National Informatics Centre (NIC) has projected significant "portal capacity and concurrency issues."

To mitigate the risk of systemic overload and ensure a smooth transition, the President of the GSTAT has promulgated a specific order to regulate the filing process. This post provides a technical breakdown of the new staggered filing system and the overarching limitation periods codified by the Central Government.

The Legal Basis for Staggered Filing

GSTAT Order No. establishes the procedural framework for this phased approach. F.No. GSTAT/Pr. Bench/Portal /125/25-26/1499-1502, dated September 24, 2025.

This order is issued in the exercise of powers conferred under Rule 123 of the GSTAT (Procedure) Rules, 2025. The express purpose is to "streamline the filing system" and "reduce the burden on the electronic system" by staggering the influx of appeals filed under Section 112 of the Central Goods and Services Tax (CGST) Act, 2017.

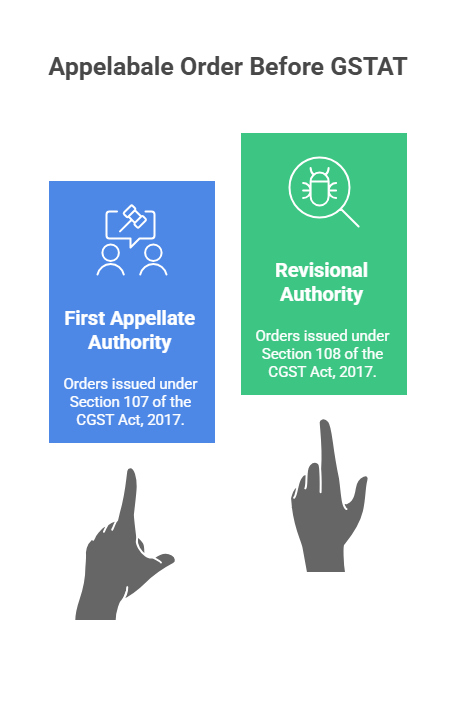

This directive applies to all appeals against:

-

Orders issued by the First Appellate Authority under Section 107 of the CGST Act, 2017.

-

Orders issued by the Revisional Authority under Section 108 of the CGST Act, 2017.

The Phased Filing Schedule (GSTAT Order)

The GSTAT order mandates a specific filing window for appeals based on the date of the original appeal filing (Form APL-01/APL-03) or the issuance of the revisional notice (Form RVN-01).

Tax professionals must meticulously observe the following schedule:

| Category | Period of filing appeal (Form APL-01/APL-03) u/s 107 or issuance of notice (Form RVN-01) u/s 108 | Period during which the appeal under Section 112 of the Act before the GSTAT may be filed |

| 1 | On or before January 31, 2022 | September 24, 2025 – October 31, 2025 |

| 2 | February 1, 2022 – February 28, 2023 | November 1, 2025 - November 30, 2025 |

| 3 | March 1, 2023 – January 31, 2024 | December 1, 2025 – December 31, 2025 |

| 4 | February 1, 2024 – May 31, 2024 | January 1, 2026 – January 31, 2026 |

| 5 | June 1, 2024 – March 31, 2026 | February 1, 2026 onwards |

| 6 | Not filed by March 31, 2026 | March 1, 2026 onwards |

The Overarching Limitation Framework (Central Government Notification)

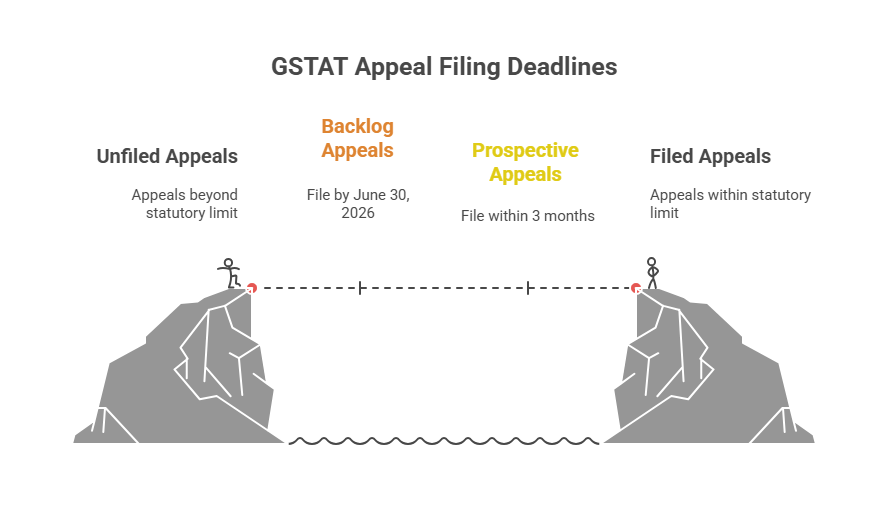

Concurrent with the procedural order from the GSTAT, the Central Government has issued Notification No. S.O.4220(E) dated September 17, 2025. This notification formally amends the statutory limitation period to accommodate this transition.

The implications of this notification are two-fold and establish the ultimate terminus ad quem (final deadline) for filing:

-

For the Backlog (Orders communicated before April 1, 2026):

For the entire accumulated backlog of impugned orders communicated to the appellant prior to April 1, 2026, the final date to file an appeal before the GSTAT is June 30, 2026. This serves as the statutory backstop, superseding all other calculations for this specific cohort of appeals.

-

For Prospective Cases (Orders communicated on or after April 1, 2026):

For any impugned order communicated on or after April 1, 2026, the standard statutory limitation period prescribed under Section 112(6) of the CGST Act, 2017—i.e., within three months from the date of communication of the order—shall be applicable.

Conclusion and Practitioner Advisory

This dual-instrument approach represents a pragmatic administrative measure to manage the anticipated deluge of GSTAT filings. While the GSTAT Order provides the procedural staggered windows, the S.O. Notification provides the statutory limitation deadlines.

Litigants and tax professionals must docket these timelines with precision. Adherence to the specific staggered window provided in the GSTAT Order is critical for case management, even though the statutory deadline for the entire backlog extends to June 30, 2026. Failure to file within the prescribed timelines could render an appeal time-barred, jeopardising the litigant's right to this crucial appellate remedy.

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified