GST Tax Liability in Cases of Merger, Dissolution, and Discontinuance

Under the CGST Act, 2017, Chapter XVI (Sections 85 to 94) contains special provisions dealing with tax liability in cases where the business undergoes structural or legal changes.

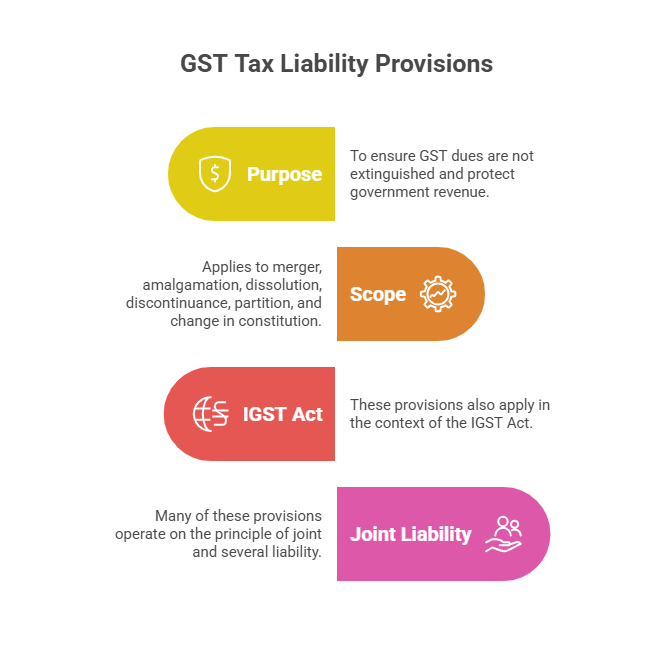

Purpose of These Provisions

- To ensure that GST dues do not get extinguished merely because the business structure changes.

- To protect government revenue in cases of merger, amalgamation, dissolution, discontinuance of business, partition, and change in constitution.

- These provisions also apply in the context of the IGST Act.

- Many of these provisions operate on the principle of joint and several liability.

1. Section 87 – Liability in Case of Amalgamation or Merger of Companies

Where This Section Applies

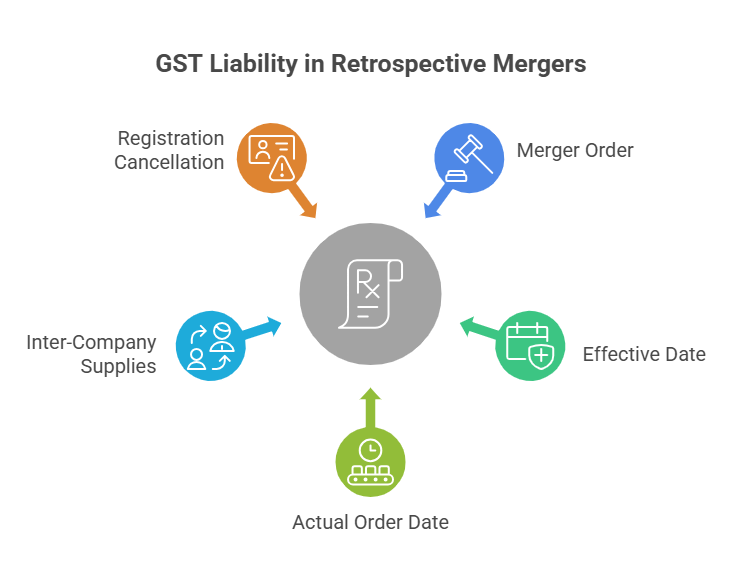

- When two or more companies merge or amalgamate.

- When such merger/amalgamation is pursuant to an order of a Court or Tribunal.

- When the order is made effective from a retrospective date, i.e., from a date earlier than the actual date of the order.

Key Legal Effect

Even if the merger is effective from an earlier date, the companies are treated as distinct taxable persons till the actual date of the Court/Tribunal order.

Practical Implication

Any supply of goods or services between the merging companies during the interim period is taxable. The interim period means from the effective date mentioned in the order up to the actual date of the order.

Important Consequences

- Inter-company transactions during this period are treated as valid taxable supplies.

- They must be included in the turnover of the respective companies.

- They attract GST liability accordingly.

- The registration certificates of the merging entities are cancelled from the date of the order.

Core Takeaway

A retrospective merger under company law does not wipe out GST liability on inter-company supplies made before the order is actually passed.

2. Section 93 – Liability in Case of Dissolution of Firm or Partition of HUF/AOP

(A) Dissolution of a Firm

What Happens on Dissolution

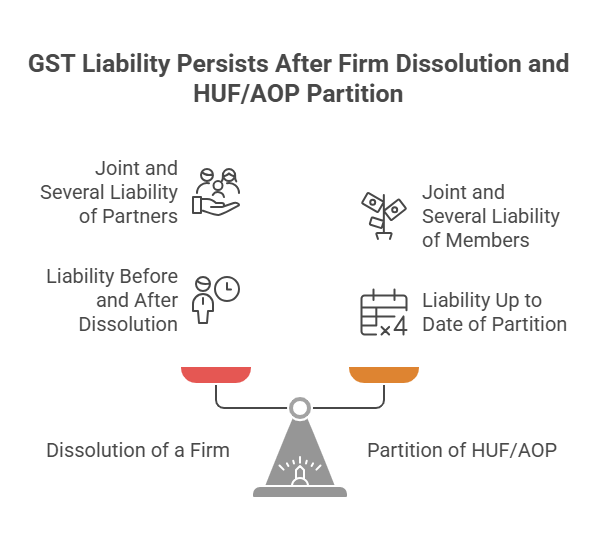

If a taxable firm is dissolved, every person who was a partner at the time of dissolution becomes jointly and severally liable for payment of tax, interest, and penalty payable by the firm.

Important Point

This liability continues whether the dues were determined before dissolution or determined after dissolution.

Meaning in Simple Words

Dissolution of the firm does not end the tax liability. Former partners can still be called upon to pay pending dues.

(B) Partition of HUF or AOP

What Happens on Partition

If the property of a taxable HUF or AOP is partitioned, each member or group of members becomes jointly and severally liable for tax, interest, and penalty due up to the date of partition.

Core Takeaway

Partition of assets does not divide or extinguish GST liability against the Department.

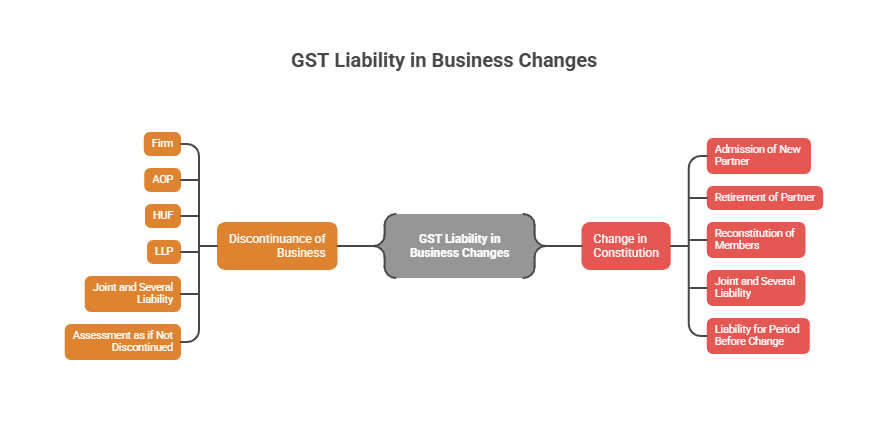

3. Section 94 – Liability in Case of Discontinuance of Business or Change in Constitution

(A) Discontinuance of Business

Where It Applies

When a firm, AOP, or HUF discontinues its business.

Liability Rule

Every person who was a partner or a member at the time of discontinuance becomes jointly and severally liable for tax, interest, and penalty. The dues may be determined as if the business had not been discontinued.

Special Note

For this purpose, an LLP is also treated as a firm.

Core Takeaway

Stopping business operations does not prevent assessment or recovery of past GST dues.

(B) Change in Constitution of Firm or AOP

Where It Applies

When there is a change in the constitution of a firm or AOP — for example, admission of a new partner, retirement of an existing partner, or reconstitution of members.

Liability Rule

The partners/members both before the change and after the change are jointly and severally liable for dues relating to the period before such change.

Core Takeaway

Reconstitution of a firm does not erase earlier GST liabilities.

4. Common Principle Running Through These Provisions

Joint and Several Liability

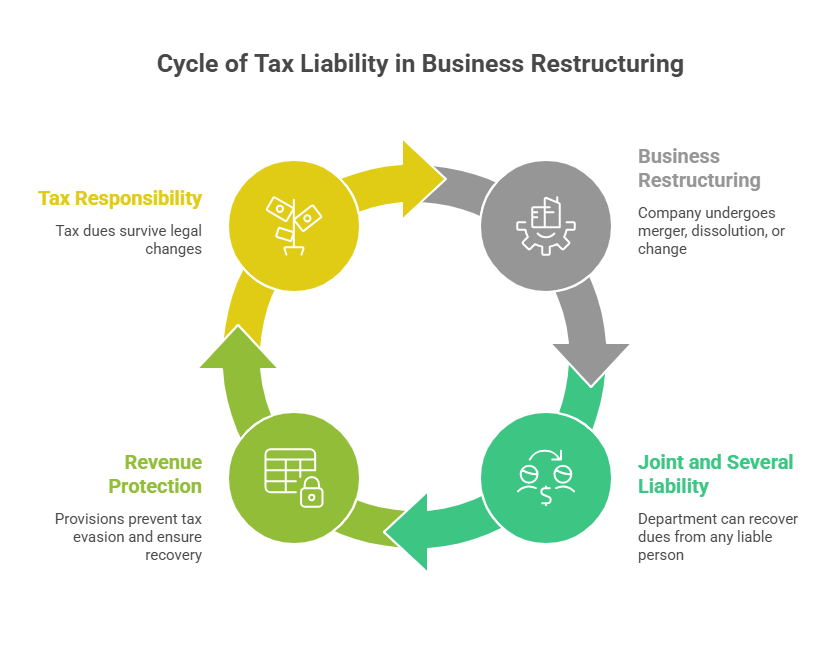

- The Department can recover dues from any one liable person, or from all such persons together.

- It is not necessary for the Department to recover only from the original entity.

Revenue Protection

These provisions are designed to prevent tax evasion, avoid escape of liability during restructuring, and ensure continuity of recovery despite legal changes.

Broader Message of Law

Change in legal structure does not mean change in tax responsibility. Tax dues survive dissolution, discontinuance, merger, partition, and reconstitution.

5. Practical Significance for Businesses and Professionals

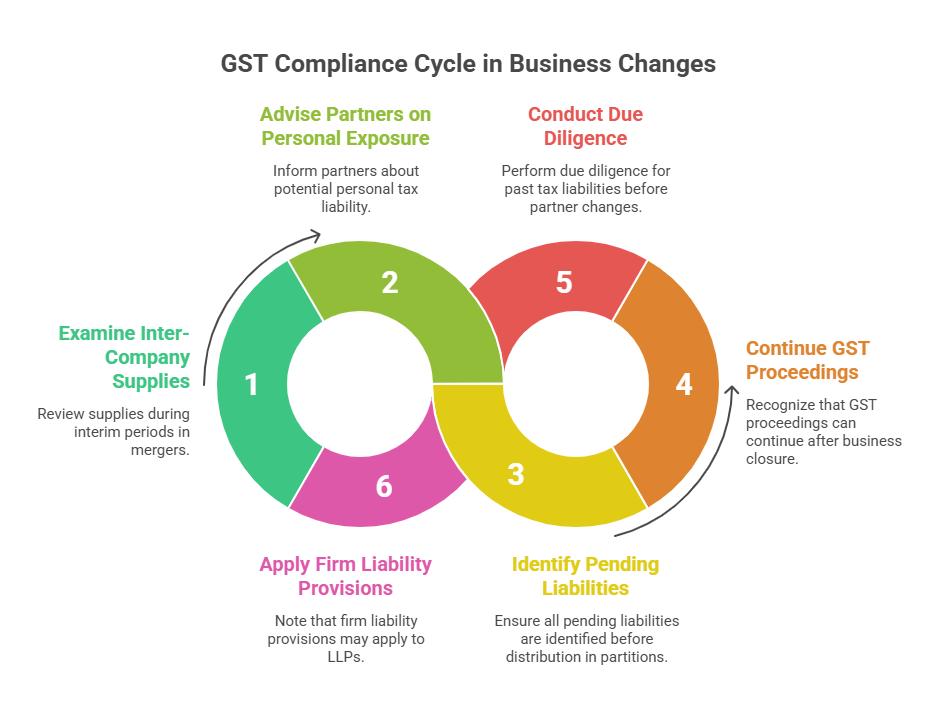

- Merger cases: Examine inter-company supplies during the interim period carefully.

- Dissolution cases: Advise partners that personal exposure to tax dues may continue.

- HUF/AOP partitions: Ensure pending liabilities are identified before distribution of assets.

- Business closure: GST proceedings can continue even after discontinuance.

- Reconstitution of firms: Conduct due diligence for past tax liabilities before admitting or retiring partners.

- LLP cases: Note that liability provisions applicable to firms may also apply to LLPs.

gst audit checklist | gst registration status | section 129 and 130 of gst | input tax credit | statement of facts and grounds of appeal

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified