Consideration of the Reply while Passing GST Adjudication Orders

The core principle governing the passing of any adverse order is the adherence to the Principles of Natural Justice (PNJ), particularly the rule of *Audi Alteram Partem* (let the other side be heard) [1-6]. In the context of GST law, this obligation is codified, requiring the proper officer to actively consider the taxpayer's submissions.

1. How the Reply Should Be Considered and What Are the Grounds and Considerations

The consideration of the reply is integral to the proper adjudication process, which is considered a quasi-judicial proceeding .

Grounds and Mandatory Considerations:

1. Mandatory Opportunity of Hearing (OBH): An opportunity of hearing shall be granted in two situations:

* Where a request is received in writing from the person chargeable with tax or penalty.

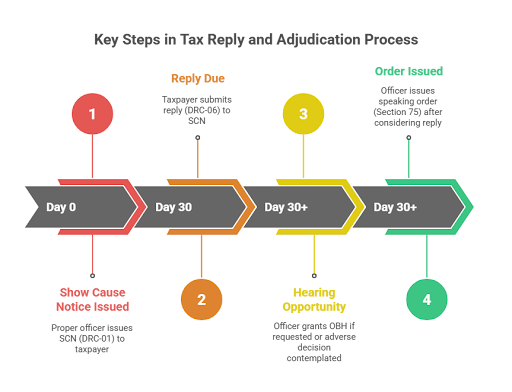

* Where any adverse decision is contemplated against such person Even if a personal hearing was not specifically requested, if an adverse order is intended, OBH is mandatory

2. Statutory Mandate (Section 75: The resulting order must be a "Speaking Order". A speaking order requires the proper officer to set out the relevant facts and the basis of his decisions

3. Scope of Order: The amount demanded in the order must not exceed the amount mentioned in the Show Cause Notice (SCN) Furthermore, the order must be in conformity with the grounds laid out in the SCN. An order cannot go beyond or be contrary to the SCN

4. Impartiality: The officer issuing the final order must often be different from the officer who issued the Audit Report or SCN

# Contexts of Reply:

* Scrutiny (ASMT-10): The taxpayer files a reply in FORM GST ASMT-11 either accepting the demand or providing an explanation for the discrepancy within 30 days (or further period permitted by the officer). If the reply is found satisfactory, the officer issues an order of acceptance in FORM GST ASMT-12. If the reply is not accepted, the proper officer initiates proceedings under Section 73 or 74.

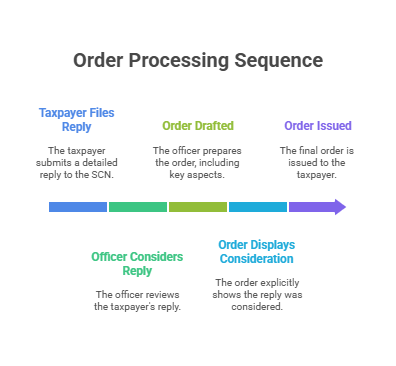

* SCN (DRC-01): The taxpayer files a detailed reply (representation) to the SCN (issued under Section 73 or 74) in FORM GST DRC-06. This reply should address each allegation, furnish evidence, and cite legal precedents. The proper officer, after considering this representation, determines the amount of tax, interest, and penalty due and issues the order

2. How the Order Will Display that Reply Has Been Considered

A valid order, especially an adverse one, must explicitly demonstrate the application of mind and consideration of the reply.

The adjudication order (often summarized in FORM GST DRC-07 for final assessment (like in Provisional Assessment resulting in FORM GST ASMT-07) typically contains the following aspects, where the consideration of the reply is displayed:

1. Brief facts .

2. Submissions by the applicant (i.e., detailing the arguments made in the reply/representation).

3. Discussion and finding (specifically addressing and rebutting the submissions/arguments made by the taxpayer) .

4. Conclusion and order.

Judicial Insight on Displaying Consideration:

The reasons provided are the "heart and soul of the order". The proper officer must avoid taking a "blinkered view". The order should objectively refer to the language used in the reply itself and address the arguments raised, rather than relying on internal explanations given later.

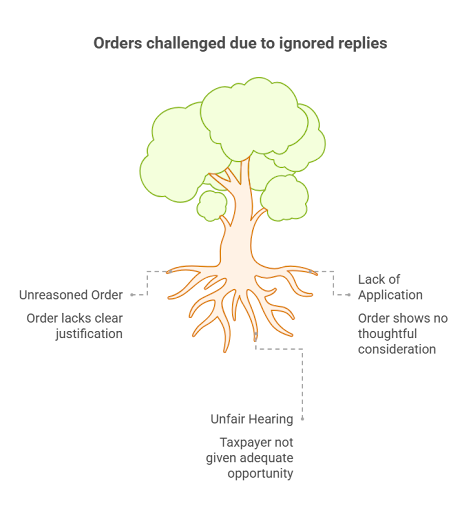

3. What If Reply Is Not Considered, and Whether the Order Can Be Challenged on this Ground

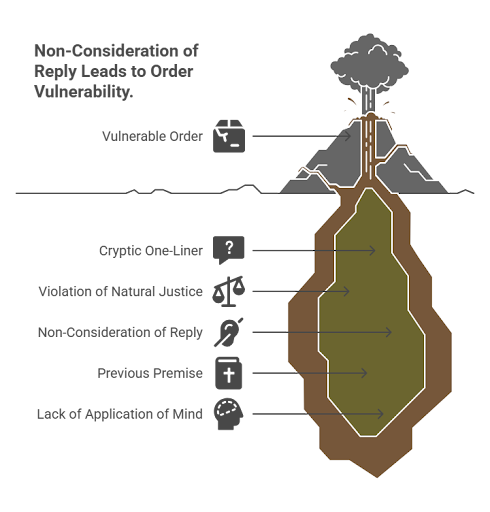

If the reply is not considered, the order is highly vulnerable to challenge.

Consequences of Non-Consideration:

When an order is passed with a cryptic one-liner stating the reply was merely "verified and not accepted so far," or similarly vague phrasing, the order is liable to be set aside.

Judicial decisions confirm that orders passed without giving an opportunity for a personal hearing or without considering the reply constitute a fundamental flaw and a violation of the principles of natural justice .

For instance, the Delhi High Court set aside an order cancelling GST registration because the subsequent order dismissing the revocation application failed due to the "non-consideration of reply to SCN". Similarly, passing a Demand Order without responding to the assessee's prayer for time or personal hearing was deemed a violation of statutory requirements and led to the quashing of the order .

If the order is passed based on a previous premise (like that the assessee filed no reply) when a reply was actually filed, or relies on an assumption that the reply was considered when it clearly was not ("Cut-Copy-Paste" order), the order is flawed. An order passed "without application of mind" and "without considering the records" has been set aside by courts.

Challenge Grounds for Orders Failing to Consider Reply:

The order can absolutely be challenged on the ground that the reply was not considered, which fundamentally relates to the violation of PNJ. Grounds of appeal related to this issue often include :

1. The order is "Not a reasoned order or non-speaking order.

2. The order was passed "Without application of mind.

3. The taxpayer was "Not given fair or reasonable hearing".

If the adjudicating authority fails to provide a mandatory hearing or pass a speaking order, the appellate authority generally cannot rectify this deficiency simply by giving a subsequent hearing; the consensus from various judgments is that both the original order and the appellate order may be quashed and the matter remanded back to the original authority.

When violation of the principles of natural justice is established, such an order is fundamentally flawed and amenable to challenge by way of a writ petition under Article 226 of the Constitution of India, notwithstanding the availability of an alternative statutory remedy . The courts emphasize that liberal interpretation of Articles 14 and 21 readily brings in the requirements of natural justice to administrative actions against a person.

Powers of GST Officers | How to Reply for ASMT-13 | GST audit checklist | GST inspector power | GST Audit Process | Supreme court itc to be given to the purchaser even if tax is not deposited by seller

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified