GST Section 62 Assessment: Guide for Finance Executives (Non-Filers)

Section 62: Assessment of Non-Filers of Return under GST - A Comprehensive Guide for Finance Executives

Executive Summary

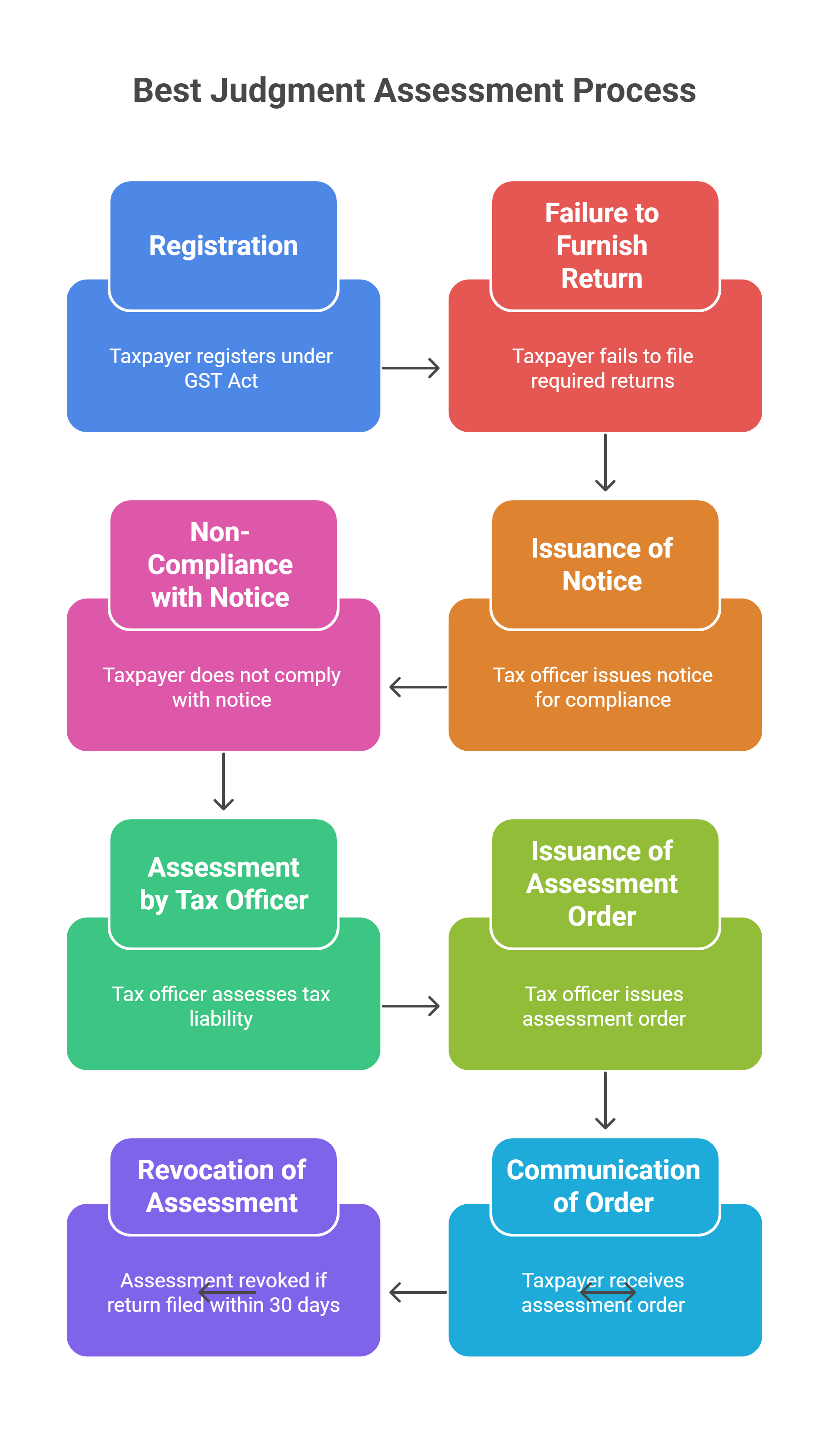

Section 62 of the Central Goods and Services Tax Act, 2017 empowers tax authorities to conduct best judgment assessments (BJA) against registered taxpayers who fail to furnish their GST returns despite statutory notices. This provision represents a critical enforcement mechanism that can result in significant financial implications for non-compliant businesses. For senior finance executives, understanding the procedural nuances, compliance requirements, and strategic considerations surrounding Section 62 assessments is essential for maintaining regulatory compliance and avoiding punitive actions.

Introduction

The GST regime mandates the timely filing of returns as a fundamental compliance requirement. When registered taxpayers fail to meet these obligations, Section 62 provides tax authorities with the power to assess tax liability based on available information through a best judgment assessment. This article examines the practical aspects of Section 62 proceedings, procedural safeguards, judicial interpretations, and preventive measures that finance teams should implement.

Legal Framework and Statutory Provisions

Section 62: Assessment of Non-filers of Return

Section 62 of the CGST Act, 2017 states:

"Notwithstanding anything to the contrary contained in section 73 or section 74, where a registered person fails to furnish the return under section 39 or section 44 or section 45, even after the service of a notice under section 46, the proper officer may proceed to assess the tax liability of the said person to the best of his judgment taking into account all the relevant material which is available or which he has gathered and issue an assessment order within a period of five years from the date specified under section 44 for furnishing of the annual return for the financial year to which the tax not paid relates."

Rule 100 of CGST Rules, 2017

Rule 100 prescribes the procedural aspects for assessment of non-filers of returns, including the forms to be used:

-

Form GST ASMT-13: Assessment order

-

Form GST DRC-07: Summary of assessment order

Conditions Precedent for Invoking Section 62

The invocation of Section 62 requires fulfilment of specific conditions:

-

Return Filing Default: The registered person must have failed to furnish returns under Section 39 (regular monthly/quarterly returns), Section 44 (annual return), or Section 45 (final return).

-

Service of Notice under Section 46: A notice in Form GSTR-3A must have been issued directing the taxpayer to furnish the return within 15 days, and the taxpayer must have failed to comply.

-

Time Limitation: The assessment order must be passed within five years from the due date of furnishing the annual return for the relevant financial year.

Procedural Framework

Step 1: System-Generated Reminders

As per the Standard Operating Procedure outlined in Circular No. 129/48/2019-GST dated 24-12-2019:

-

A system-generated message is sent three days before the due date as a reminder

-

If no return is filed, another message is sent after the due date

-

Five days after the due date, Form GSTR-3A notice is issued

Step 2: Notice under Section 46

The proper officer issues Form GSTR-3A requiring the taxpayer to furnish the pending return within 15 days. This notice serves as the mandatory precondition for initiating proceedings under Section 62.

Step 3: Best Judgment Assessment

If the taxpayer fails to comply with the Section 46 notice, the proper officer proceeds with assessment based on:

-

Details available in GSTR-1 filed by the taxpayer

-

Information from Form GSTR-2A

-

E-way bill portal data

-

Any other relevant information available with the department

Step 4: Assessment Order

The proper officer passes an assessment order in Form GST ASMT-13, with a summary uploaded in Form GST DRC-07. The order must be passed within the prescribed time limit of five years.

Withdrawal of Assessment Order

A crucial provision under Section 62 allows for automatic withdrawal of the assessment order if the taxpayer furnishes a valid return within 30 days of service of the assessment order. However, the liability for interest and late fees continues despite such withdrawal.

Judicial Interpretations and Key Case Laws

Procedural Compliance and Natural Justice

In S.P.Y. Agro Industries Ltd. v. Union of India [2021 (44) G.S.T.L. 337 (A.P.)], the Andhra Pradesh High Court held that assessment proceedings under Section 62 must follow principles of natural justice. The court observed that the department had issued the assessment order on 29-01-2019, merely 14 days after issuing the notice on 15-01-2019, without waiting for the statutory period to expire. The court emphasised that procedures contemplated under Sections 73 or 74, including issuance of show cause notice and following principles of natural justice, must be adhered to even in Section 62 proceedings.

Similarly, in Suman Kumar v. State of Bihar [2021 Taxo.online 342], the court set aside an assessment order passed without affording adequate opportunity of hearing, stating that such proceedings "entail civil consequences, seriously prejudicing the petitioner."

Requirements for Valid Best Judgment Assessment

The Advance Ruling Authority in In Re: Omsai Professional Detective and Security Services Pvt. Ltd. [2020 (37) G.S.T.L. 360 (AA-AP)] laid down important principles for conducting BJA:

-

The assessment must be based on relevant material available or gathered by the assessing authority

-

The authority must provide reasons or basis for estimating quantum of outward taxable supplies

-

Arbitrary enhancement of turnover (150% in this case) without proper enquiry is not permissible

-

Returns filed in Form GSTR-1 cannot be rejected without contradictory evidence

In Golden Mesh Industries v. Assistant Commissioner of State Tax [2021 Taxo.online 476], the court found the method of multiplying monthly SGST by three times to determine tax liability as arbitrary and remanded the matter for fresh consideration.

Timely Compliance Can Negate Recovery Proceedings

In Joy Mathew v. Union of India [2020 Taxo.online 488], the taxpayer filed returns within 30 days of the assessment order. When the department issued recovery notices, the court set them aside, holding that the assessment order stood withdrawn automatically upon filing of returns within the stipulated period.

Interplay with Recovery Proceedings

The relationship between Section 62 assessments and recovery proceedings under Sections 78 and 79 requires careful consideration:

-

Immediate Recovery Action: As per the Standard Operating Procedure, if returns are not furnished even within 30 days of the assessment order, the department initiates recovery proceedings under Sections 78 and 79.

-

Deemed Withdrawal Effect: When an assessment order is deemed withdrawn due to filing of returns within 30 days, any recovery proceedings initiated become invalid, as established in Joy Mathew v. Union of India.

-

Continuing Liabilities: Even when the assessment order is withdrawn, interest under Section 50 and late fees continue to accrue and remain recoverable.

Internal Controls and Preventive Measures

Finance teams should implement robust systems to prevent Section 62 proceedings:

1. Return Filing Monitoring System

Establish a comprehensive monitoring mechanism that includes:

-

Daily dashboard tracking of return filing status across all GSTINs

-

Automated alerts set for T-3 days before due dates

-

Escalation matrix for non-compliance to senior management

-

Monthly compliance certificates from respective teams

2. Documentation and Record Management

Maintain meticulous records of:

-

All communications received from GST authorities

-

Proof of return filing (ARNs and acknowledgments)

-

Correspondence related to technical difficulties, if any

-

Board resolutions or authorizations for return filing

3. Response Protocol for Notices

Develop standard operating procedures for:

-

Immediate acknowledgment of notices received

-

Internal circulation to relevant stakeholders within 24 hours

-

Response preparation timelines with buffer periods

-

Approval matrix for notice responses

4. Periodic Compliance Reviews

Conduct quarterly reviews covering:

-

Analysis of return filing patterns and delays

-

Root cause analysis of any defaults

-

System improvements based on identified gaps

-

Training needs assessment for finance teams

5. Technology Integration

Leverage technology solutions for:

-

Automated return preparation and filing

-

Integration with ERP systems for seamless data flow

-

Real-time tracking of compliance status

-

Predictive analytics for identifying potential defaults

Best Practices for Managing Section 62 Proceedings

When faced with potential or actual Section 62 proceedings, finance executives should:

1. Immediate Response Strategy

Upon receiving a Section 46 notice:

-

Assess the feasibility of filing returns within 15 days

-

If filing is possible, prioritize immediate compliance

-

If challenges exist, document reasons comprehensively

-

Consider filing a reply to the notice explaining genuine difficulties

2. Engagement with Authorities

-

Maintain professional communication with tax officers

-

Request personal hearings when assessment proceedings are initiated

-

Submit all available documents supporting actual turnover

-

Avoid confrontational approaches while asserting legal rights

3. Post-Assessment Actions

If an assessment order is passed:

-

Evaluate the option of filing returns within 30 days for automatic withdrawal

-

Analyze the assessment methodology for legal sustainability

-

Consider filing appeals if the assessment is arbitrary or excessive

-

Maintain detailed documentation for future reference

Common Pitfalls to Avoid

-

Ignoring System-Generated Reminders: These early warnings provide opportunity for timely compliance

-

Delayed Response to Formal Notices: The 15-day timeline under Section 46 is statutory and non-negotiable

-

Incomplete Documentation: Failure to maintain proper records weakens the position during assessment proceedings

-

Non-engagement with Authorities: Absence of response may be construed as an admission of default

-

Missing the 30-Day Window: Failing to utilise the withdrawal provision results in crystallisation of demand

Strategic Considerations for Senior Management

Finance executives must view Section 62 compliance through a strategic lens:

-

Reputational Risk: Non-filing of returns and subsequent assessments can damage corporate reputation and stakeholder confidence

-

Financial Impact: Best judgment assessments often result in inflated tax demands due to lack of input from the taxpayer

-

Resource Allocation: Defending against Section 62 proceedings consumes significant management time and legal resources

-

Compliance Culture: Regular defaults indicate systemic issues requiring top-level intervention

-

Board Reporting: Include GST compliance status as a regular board agenda item with specific focus on return filing compliance

Conclusion

Section 62 represents a powerful enforcement tool in the GST regime that requires proactive management by finance executives. The provision's automatic withdrawal mechanism provides a safety valve, but reliance on this feature indicates poor compliance management. By implementing robust internal controls, maintaining open communication with tax authorities, and ensuring timely compliance, organizations can effectively avoid the pitfalls of best judgment assessments.

The judicial trend clearly indicates that while tax authorities have wide powers under Section 62, these must be exercised following principles of natural justice and based on reasonable assessment of available information. Finance leaders must ensure their teams are equipped with the knowledge, systems, and processes to maintain compliance and respond effectively when faced with potential Section 62 proceedings.

The key to managing Section 62 risks lies not in developing strategies to contest assessments, but in building systems that prevent their occurrence. As the GST regime matures and enforcement mechanisms become more sophisticated, the cost of non-compliance will only increase, making proactive compliance management an essential component of corporate governance.

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified