GST Registration Cancellation and Suspension: A Complete Guide for Finance Professionals

Understanding the procedures for cancelling or suspending GST registration is crucial for finance teams to ensure compliance and protect business interests. This comprehensive guide covers all aspects of handling show cause notices, suspension proceedings, and cancellation processes under GST law.

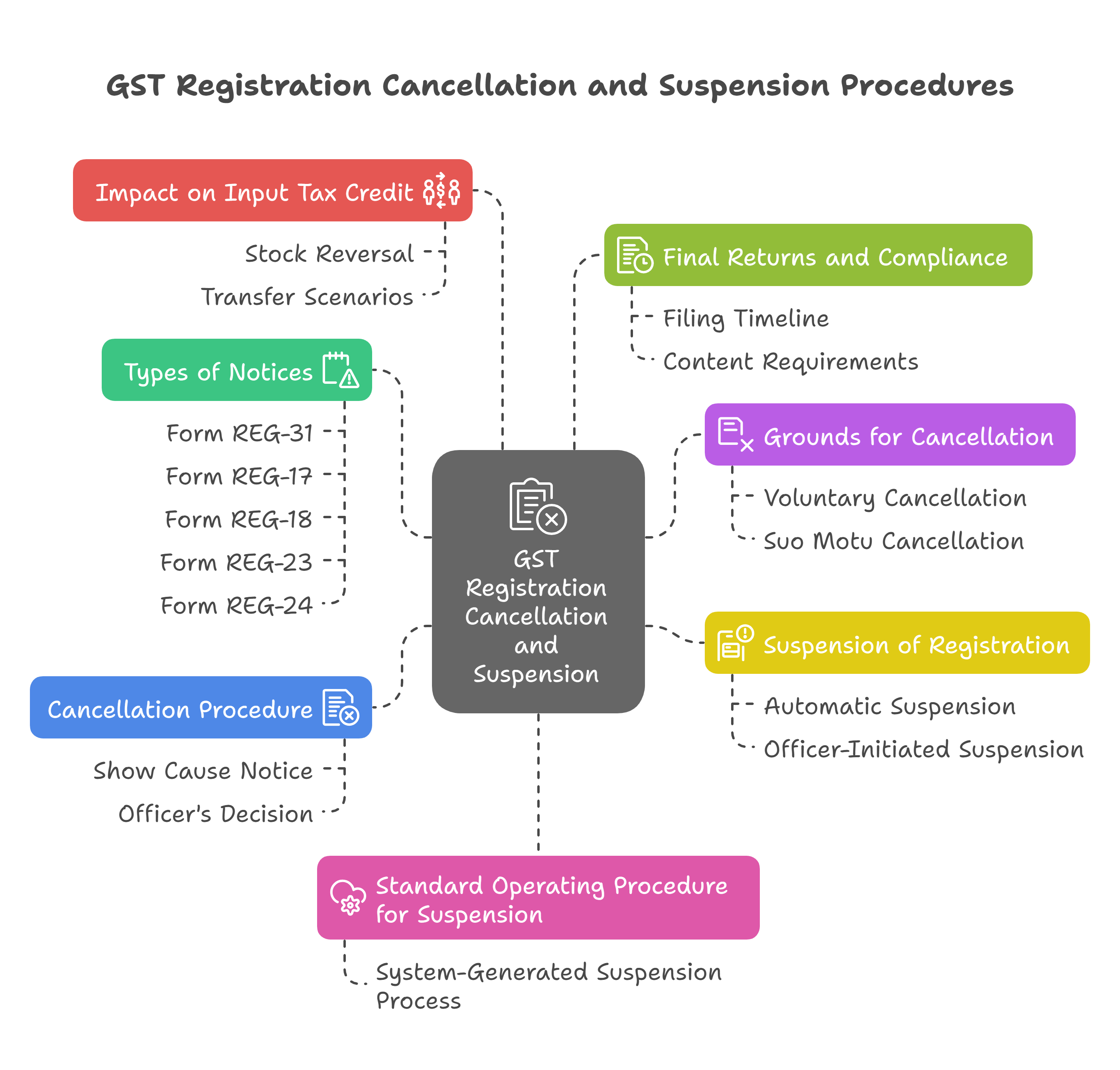

1. Types of Notices for Registration Cancellation

Key Notice Categories

Form REG-31 (Rule 21A(2A))

• Notice seeking cancellation due to discrepancies between GSTR-3B and GSTR-1

• Issued when significant differences indicate potential violations

• Immediate suspension of registration upon issuance

Form REG-17 (Rule 22(1))

• Show cause notice for suo motu cancellation by Proper Officer

• Issued when officer believes registration is liable for cancellation

• Requires response within seven working days

Form REG-18 (Rule 22(1))

• Reply format for taxpayers responding to REG-17 notices

• Must be filed within seven working days of notice receipt

• Point-wise responses required against allegations

Form REG-23 (Rule 23(3))

• Notice seeking rejection of revocation application

• Relates to attempts to restore cancelled registration

Form REG-24 (Rule 23(3))

• Reply format for responding to REG-23 notices

• Seven working days response period

2. Grounds for Registration Cancellation

Voluntary Cancellation Scenarios (Section 29(1))

Business Discontinuation

• Business has been discontinued permanently

• Full transfer of business operations

• Death of proprietor in sole proprietorship

• Amalgamation or demerger with other entities

Constitutional Changes

• Changes in business constitution

• Partnership modifications

• Conversion between business structures

Registration No Longer Required

• Turnover falls below mandatory registration threshold

• Voluntary opt-out from registration

• No longer liable under Section 22 or 24

Suo Motu Cancellation Grounds (Section 29(2))

Compliance Violations (Rule 21)

• No business conducted from declared premises

• Issuing invoices without actual supply of goods/services

• Violation of anti-profiteering measures (Section 171)

• Non-furnishing of bank account details (Rule 10A)

• Improper input tax credit availment (Section 16)

• Excess outward supplies in GSTR-1 vs. valid returns

• Non-payment of 1% tax through electronic cash ledger (Rule 86B)

Return Filing Defaults

• Composition dealers: Non-filing for three consecutive periods

• Regular taxpayers: Non-filing for six consecutive months

• Voluntary registration: No business commencement within six months

Fraudulent Registration

• Registration obtained through fraud

• Wilful misstatement of facts

• Suppression of material information

3. Suspension of Registration

Automatic Suspension Triggers (Rule 21A)

Application-Based Suspension

• Immediate suspension upon filing cancellation application

• Effective from application date or requested cancellation date (whichever is later)

• Continues until cancellation proceedings complete

Officer-Initiated Suspension

• When officer believes cancellation is warranted

• Discretionary suspension pending investigation

• Specified effective date determined by officer

System-Generated Suspension (Rule 21A(2A))

• Automatic suspension based on data analytics

• Comparison between GSTR-1 and GSTR-3B reveals discrepancies

• Immediate effect upon system detection

Suspension Consequences

Supply Restrictions

• Cannot make any taxable supplies during suspension

• No tax invoice issuance permitted

• No tax charging allowed on supplies

Return Filing Relief

• No requirement to file returns under Section 39

• Compliance obligations suspended temporarily

Refund Restrictions

• No refunds granted under Section 54 during suspension

• All refund processing halted until resolution

Response Requirements During Suspension

Mandatory Actions Within 30 Days

• File reply in Form REG-18 through GST portal

• Explain discrepancies and anomalies highlighted

• Provide compliance details and supporting documents

• Submit reasons why registration should not be cancelled

Alternative Compliance Routes

• File all pending returns if suspension due to non-filing

• Make complete tax payments including interest and late fees

• Address specific violations mentioned in suspension notice

4. Cancellation Procedure

Show Cause Notice Process

Notice Issuance (Form REG-17)

• Proper Officer must specify precise cancellation reasons

• Vague notices are not sustainable in law

• Must enable taxpayer to provide meaningful response

Response Requirements

• Seven working days to file reply in Form REG-18

• Point-wise responses to all allegations

• Supporting documentation upload mandatory

• Personal hearing attendance if required

Officer's Decision Options

Proceeding Dropped (Form REG-20)

• When reply is found satisfactory

• When all pending returns filed and dues cleared

• Registration status restored to active

Cancellation Order (Form REG-19)

• Issued within 30 days of application/reply

• Specifies effective cancellation date

• Cannot be earlier than application date

• Details arrears and payment requirements

Special Situations

Death of Sole Proprietor

• Legal heirs can apply for cancellation

• Business transfer to successor possible

• Input tax credit transfer provisions available

• Registration liability continues for successor

Tax Deductor/Collector Cancellation

• When no longer liable for TDS/TCS under Sections 51/52

• Cancellation communicated in Form REG-08

• Written request or inquiry-based proceedings

5. Impact on Input Tax Credit

Stock Reversal Requirements (Section 29(5))

Calculation Methodology

• Input tax credit on inputs in stock

• Credit on inputs in semi-finished goods

• Credit on inputs in finished goods

• Higher of credit amount or output tax liability

Capital Goods Treatment

• Pro-rata calculation based on remaining useful life

• Useful life considered as 5 years for computation

• Reduced by prescribed percentage points

• Compared with transaction value tax liability

Payment Mechanism

• Debit from electronic credit ledger first

• Balance amount paid through cash ledger

• Final return (GSTR-10) includes complete details

• Not prerequisite for cancellation application

Transfer Scenarios

Business Transfer on Death

• Unutilised credit transferable to successor

• Form ITC-02 filing by transferee required

• Joint liability for transferor's dues

• Legal heir addition to existing GSTIN needed

Multiple Registration Transfer

• Form ITC-02A filing within 30 days

• Credit transferred in asset value ratio

• Acceptance by transferee entity required

• Pro-rata basis calculation mandatory

6. Final Returns and Compliance

Final Return Requirements (Form GSTR-10)

Filing Timeline

• Within three months of cancellation date

• Within three months of cancellation order date

• Whichever is later applies

Content Requirements

• Complete liability discharge under Section 29(5)

• Stock details as on day preceding cancellation

• Input tax credit reversal calculations

• Outstanding dues and payment details

Non-Compliance Consequences

Notice Process

• Form GSTR-3A notice issued for non-filing

• 15-day compliance period after notice

• Assessment order (Form ASMT-13) if still non-compliant

Assessment Under Section 62

• Best judgement assessment by officer

• Based on available information

• Withdrawal possible if return filed within 30 days

• Interest and late fee liability continues

7. Standard Operating Procedure for Suspension

System-Generated Suspension Process

Data Analytics Trigger

• Council recommendation-based taxpayer identification

• System-generated Form REG-31 notice

• Email communication to registered address

• Dashboard visibility for proper officers

Officer Action Requirements

• Task creation in officer dashboard

• 30-day response period monitoring

• Reply examination and decision making

• Order issuance in appropriate form (REG-19/REG-20)

Status Management

• Automatic GSTIN status updates

• "Active" for dropped proceedings

• "Cancelled Suo-moto" for cancellation orders

• Real-time portal reflection

8. Best Practices for Finance Teams

Proactive Compliance Measures

Regular Monitoring

• Monthly reconciliation between GSTR-1 and GSTR-3B

• Timely return filing without defaults

• Maintenance of supporting documentation

• Bank account details updates as required

Response Preparedness

• Designated team for notice handling

• Standard operating procedures for replies

• Legal counsel engagement protocols

• Document repository maintenance

Notice Response Strategy

Immediate Actions Upon Receipt

• Notice analysis and categorisation

• Timeline calculation and calendar marking

• Response team assembly and role assignment

• Preliminary document compilation

Reply Preparation

• Point-wise responses to all allegations

• Supporting evidence compilation

• Legal precedent research where applicable

• Draft review by senior finance leadership

Follow-up Procedures

• Response acknowledgement tracking

• Hearing attendance if required

• Order receipt and analysis

• Appeal consideration if necessary

9. Key Compliance Reminders

Critical Deadlines

• Seven working days for REG-17 responses

• 30 days for REG-31 suspension replies

• 30 days for cancellation application filing

• Three months for final return submission

Documentation Requirements

• Complete stock details with valuations

• Input tax credit supporting invoices

• Bank account verification documents

• Business discontinuation proof where applicable

Cost Implications

• Input tax credit reversal on stock

• Interest on delayed compliance

• Late fees for pending returns

• Potential assessment under best judgement

This comprehensive approach to GST registration cancellation and suspension ensures that finance teams can effectively navigate these complex procedures while maintaining compliance and protecting business interests.

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified