GST Registration Cancellation: Non-Filing Returns & Legal Procedures

GST Laws for Cancellation of GST Registration for Non-Filing of GST Returns

Overview

GST registration can be cancelled by the proper officer either suo moto (on their own motion) or upon application by the registered person . One of the primary grounds for suo moto cancellation is the non-filing of GST returns for a prescribed period. The law prescribes specific periods, procedures, and rights for both the GST officer and the taxpayer regarding cancellation due to non-compliance in filing returns.

Statutory Provisions & Rules

1. Relevant Statutory Provisions:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2. Grounds for Cancellation Related to Non-Filing (Post-Finance Act, 2022 & Latest

Rule 21 (as amended by Notification No. 19/2022-CT dt. 28.09.2022):

-

For monthly filers (GSTR-3B): Failure to furnish returns for a continuous period of six months

-

For QRMP scheme filers: Failure to file returns for a continuous period of two tax periods (quarters)

-

For composition scheme filers: As amended by Finance Act, 2022, non-filing of annual return for a financial year beyond three months from the due date

Section 29(2)(c) (as amended by Finance Act, 2022):

-

Wording changed to “such continuous tax period as may be prescribed” to allow the government to prescribe periods by notification.

Related Notification:

-

Notification No. 18/2022 – CT dated 28.09.2022 (w.e.f. 01.10.2022): Brings the above changes into force.

3. Procedural Steps for Cancellation

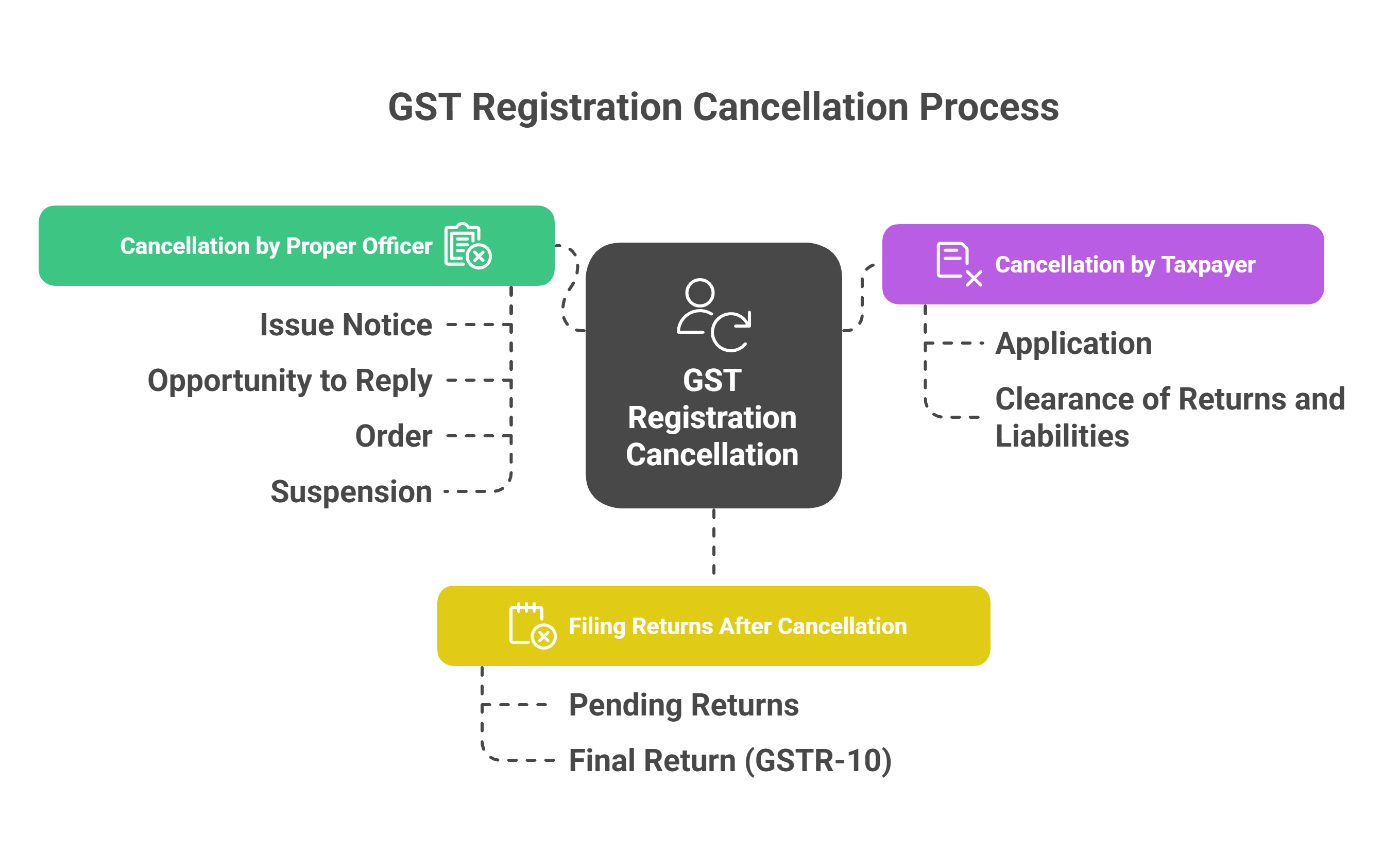

A. By Proper Officer (Suo Moto):

-

Issue Notice: In Form GST REG-17, giving the taxpayer a chance to show cause within 7 working days (Rule 22(1)).

-

Opportunity to Reply: Reply submitted in Form GST REG-18.

-

Order: If reply is unsatisfactory or no reply, order for cancellation in Form GST REG-19 within 30 days.

-

Suspension: Registration may be suspended during the process (Rule 21A).

B. By Application of Taxpayer:

-

Application: Form GST REG-16 (within 30 days of event warranting cancellation).

-

Necessary to clear returns and liabilities till the date of intended cancellation.

C. Filing of Returns:

-

Even if registration is cancelled, taxpayer is liable to file all pending returns up to the date of cancellation (Rule 22(3)) and pay due taxes, interest, and late fees.

-

Final return (GSTR-10) must be filed within 3 months of cancellation or order of cancellation, whichever is later (Section 45 & Rule 81).

Cancellation Due to Non-Filing

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Practical Implications & Tips

-

Ensure Regular Filing: Even if no business activity, NIL returns must be filed to avoid cancellation risk.

-

Opportunity to Rectify: On receipt of SCN, respond with valid reasons and, wherever possible, promptly file pending returns with payment of dues.

-

Revocation of Cancellation: File all pending returns and pay all liabilities, then apply for revocation within the stipulated period. Special amnesty windows may apply as per latest notifications.

-

Effect of Cancellation: Cancellation does not absolve liabilities for tax, interest, or penalty for the period registration was active.

-

Final Return: Mandatory filing of GSTR-10 after cancellation.

Key Notifications & Relevant Amendments

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Default Periods Leading to Cancellation

|

|

|

|

|

|

|

|

|

|

|

|

Conclusion

-

Proper Officer may initiate cancellation if returns are not filed for the prescribed period.

-

SCN and opportunity of being heard is compulsory before cancellation.

-

Suspension of registration is automatic during pendency of proceedings.

-

Pending returns, interest, penalty, and tax must be cleared to avoid or revoke cancellation.

-

Final return in GSTR-10 must be filed post-cancellation.

-

Retrospective cancellation must not be arbitrary and requires explicit reasoning.

For detailed procedures or in case of disputes, consult a GST practitioner or refer to the official CBIC guidelines/circulars.

Know Your GST, GST Verification, GST Calculator, HSN Code Search, GST Return Status

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified