Why Your GST Refund Cannot Be Denied: Key Court Judgments Every Business Must Know

Why This Article Matters to Your Business

GST refunds are among the most critical yet legally contentious aspects of the Goods and Services Tax regime in India. An unrecovered refund is, in practical terms, a cost imposed upon a business — a cost that was never legislatively intended. Two pervasive and chronic concerns afflict businesses that deal with refund applications: first, delays in securing endorsements from Special Economic Zone (SEZ) units on invoices; and second, the imposition of Integrated Goods and Services Tax (IGST) on ocean freight charges under the Reverse Charge Mechanism (RCM) — a levy that has since been declared constitutionally impermissible.

This article distils the ratio decidendi of four landmark judicial pronouncements — spanning the Madras High Court, the Delhi High Court (Division Bench), and the Supreme Court of India — into actionable intelligence for business owners, Chief Financial Officers, Directors of Finance, and tax practitioners. Each precedent is examined with complete citation details, the precise legal crux, and a structured exposition of how the ruling may be harnessed to protect and recover legitimate tax refunds.

This article distils the ratio decidendi of four landmark judicial pronouncements — spanning the Madras High Court, the Delhi High Court (Division Bench), and the Supreme Court of India — into actionable intelligence for business owners, Chief Financial Officers, Directors of Finance, and tax practitioners. Each precedent is examined with complete citation details, the precise legal crux, and a structured exposition of how the ruling may be harnessed to protect and recover legitimate tax refunds.

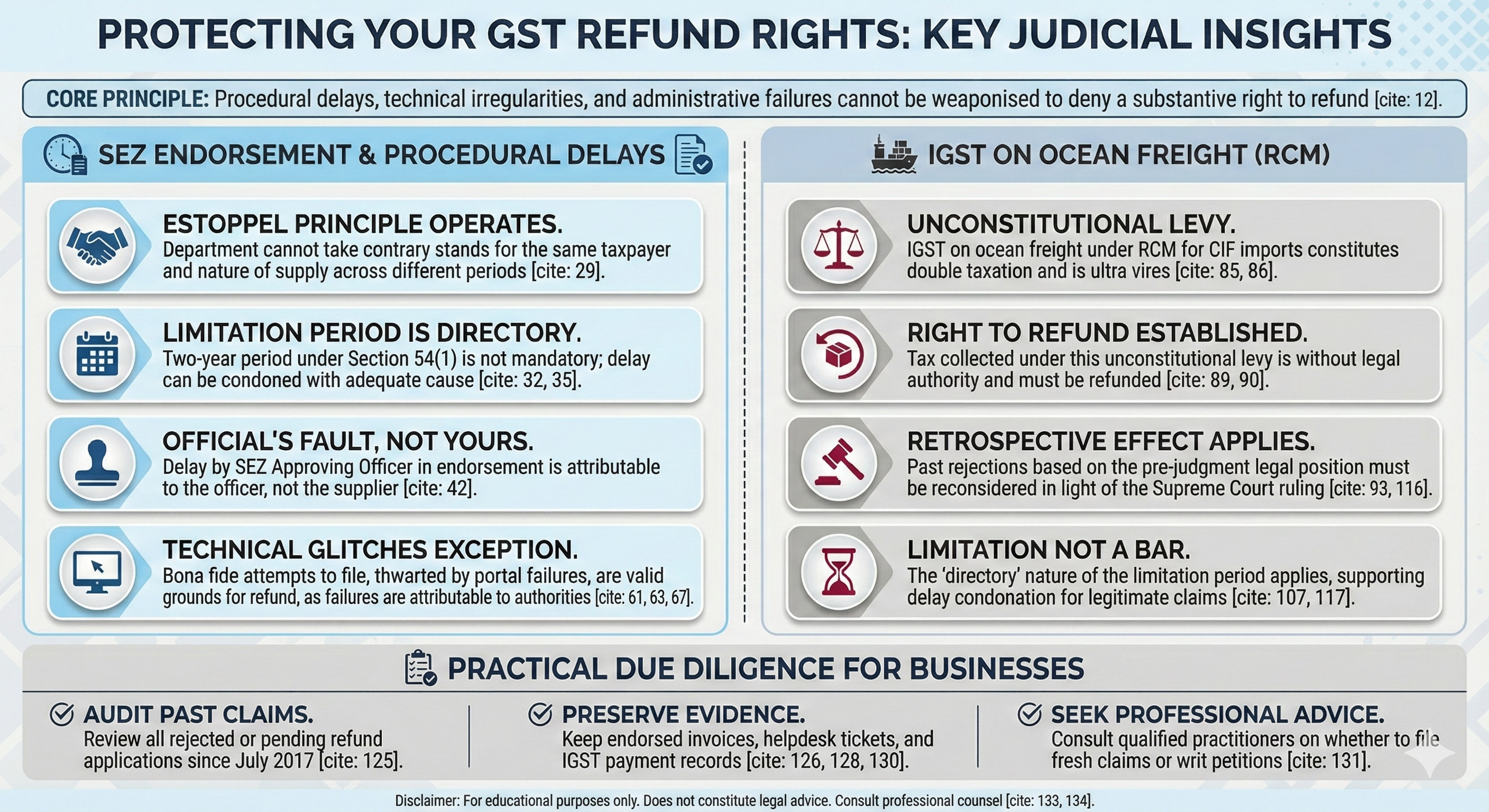

Key Message: The law, as interpreted by courts, is unambiguous — procedural delays, technical irregularities, and administrative failures on the part of government authorities shall not be weaponised to deny a taxpayer's substantive right to refund. If your refund application was previously rejected, the judgments discussed herein may offer you a viable legal pathway to recovery.

PART I

SEZ Endorsement Delays & The Right to Refund — Madras High Court

CASE 1 OF 4 — LENOVO (INDIA) PRIVATE LIMITED

Complete Citation Details

| Case Name | Lenovo (India) Private Limited v. Joint Commissioner of GST (Appeals-I) |

| Writ Petitions | W.P. Nos. 23604 and 23605 of 2022 |

| Date of Pronouncement | 06th November 2023 |

| Court | Madras High Court |

| Taxmann Citation | [2023] 156 taxmann.com 467 |

| GSTL Citation | 79 GSTL 299 |

| GST Reporter | [2024] 101 GST 4 (Mad.) |

| Centax Citation | (2023) 12 Centax 230 (Mad.) |

| Provisions Examined | Section 54(1) of the CGST Act, 2017; Section 16(3)(b) of the IGST Act, 2017; Rule 89, Rule 90(3) of the CGST Rules, 2017; SEZ Rules, 2006 (Rule 30) |

Background & Factual Matrix

Lenovo (India) Private Limited, a prominent supplier of technology hardware, had made zero-rated supplies to SEZ units. Under the IGST framework, such supplies are accorded the benefit of zero-rating, which allows the exporter/supplier to either supply goods without payment of tax under a Letter of Undertaking (LUT) or claim a refund of the IGST paid on such supplies.

In the present case, Lenovo had paid IGST on its supplies to the SEZ unit and accordingly filed refund applications for the tax periods of December 2019, January 2020, and February 2020. These applications were filed in early 2022 — a period of approximately two years after the relevant tax periods.

Two distinct objections were raised by the Revenue Authorities in opposing the refund claims:

-

The proof of delivery documents (endorsed invoices) were not submitted at the time of filing the refund applications but were instead produced during the personal hearing — Revenue contended that this late submission, particularly for the periods of January 2020 and February 2020, barred the claims on account of limitation.

-

Revenue Authorities sought to establish that the goods supplied must have been used for 'authorised operations' within the SEZ, citing provisions of the SEZ Rules, 2006. They further highlighted that procurement of endorsements had been delayed beyond the permissible 45-day window under the SEZ Rules.

The Crux: Legal Principles Established

The Madras High Court ruled comprehensively in favour of the assessee on all issues. The following four legal principles constitute the ratio of this decision:

Principle 1 — Estoppel Operates Against the Department

When the Revenue Department accepted documents submitted during personal hearing for December 2019 and processed the refund application thereon, it was estopped from taking a contrary stand for the subsequent periods of January 2020 and February 2020. The Department cannot apply one standard for one period and a different, more stringent standard for a subsequent period in respect of the same taxpayer and the same nature of supply.

Principle 2 — The Two-Year Limitation Under Section 54(1) is Directory, Not Mandatory

The Court undertook a textual analysis of Section 54(1) of the CGST Act, 2017, which employs the word 'may' in the expression 'may make application before two years from the relevant date.' The Court held that the legislature's use of the permissive expression 'may' — as opposed to 'shall' — renders the limitation period directory in nature. Therefore:

-

A taxpayer is not precluded from filing a refund application after the expiry of two years from the relevant date.

-

The legitimate claim of refund cannot be denied solely on the ground of delay in filing, where the assessee can demonstrate adequate cause.

Principle 3 — Deficiencies Must Be Pointed Out Under Rule 90(3), Not Used as a Ground for Rejection

Where the Revenue Authorities contended that the applications were filed with deficiencies, the law mandates that they ought to have issued a deficiency memo under Rule 90(3) of the CGST Rules, 2017, identifying the specific deficiencies and affording the applicant an opportunity to cure them. The failure to issue such a memo — and instead using the alleged deficiency as a post-hoc ground for rejection — is procedurally impermissible.

Principle 4 — Pre-Amendment Position Under Section 16 of IGST Act Does Not Require Proof of Authorised Operations

The Court unambiguously held that the pre-amendment provisions of Section 16 of the IGST Act, 2017, did not contemplate any requirement for the supplier to prove that the goods were used for 'authorised operations' within the SEZ. The amendment to Section 16 which introduced the stipulation regarding authorised operations was effected prospectively with effect from 01.10.2023 and cannot be applied retrospectively to supplies made during 2019–2020.

Principle 5 — Fault of the Approving Officer Cannot Be Attributed to the Taxpayer

This is the most impactful principle for operational businesses: The Approving Officer (AO) of the SEZ is the designated authority for endorsing invoices. If the AO fails to make endorsements within the prescribed 45-day window under the SEZ Rules, the fault is attributable to the AO and not to the supplier. The supplier's right to zero-rated benefit under Section 16(3)(b) of the IGST Act cannot be defeated on account of an administrative delay caused by a government official. Any delay or technical irregularity in such endorsement — so long as the authenticity of the signature is not in doubt — constitutes a mere technical irregularity that does not vitiate the substantive entitlement.

How Your Business Can Leverage This Judgment

If you are a supplier who has made zero-rated supplies to SEZ units and your refund application has been rejected — either on grounds of limitation or on account of delayed endorsements — this judgment provides a robust legal foundation to challenge such rejection. The specific scenarios where this judgment applies are outlined below:

-

Your refund application was filed after the two-year period from the relevant date due to delays in obtaining endorsed invoices from the SEZ unit — the judgment holds that the limitation period is directory, and delay, if explained, cannot be a ground for absolute denial.

-

Revenue denied your claim because endorsed invoices were not uploaded with the original application but were submitted subsequently during personal hearing — the judgment holds that the Department is estopped from taking different positions for different periods in respect of identical transactions.

-

Revenue demanded proof that your goods were used for 'authorised operations' for supplies made prior to 01.10.2023 — the judgment holds that no such requirement existed under the pre-amendment law.

-

Your endorsed invoices bear endorsements made after the 45-day window under SEZ Rules — the judgment expressly holds that such delay is attributable to the AO and cannot result in the denial of the supplier's refund.

-

Revenue rejected your application without issuing a deficiency memo under Rule 90(3) — the judgment holds that this procedural lapse by the Department itself vitiates the rejection order.

CASE 2 OF 4 — SETHI (SONS) INDIA (DELHI HIGH COURT, DIVISION BENCH)

Complete Citation Details

| Case Name | Sethi (Sons) India v. Assistant Commissioner |

| Writ Petition | W.P. (C) 4179 of 2022 |

| Date of Pronouncement | 22nd December 2023 |

| Court | Delhi High Court (Division Bench) |

| Bench Composition | Division Bench (Two-Judge Bench) |

| Key Issue | Limitation period under Section 54(1) of CGST Act — Directory vs. Mandatory; Denial of refund due to GST portal technical failures |

Background & Factual Matrix

Sethi (Sons) India is an exporter who had effected exports during the period July 2017 to March 2018 — the very first year of the GST regime's operationalisation. The assessee attempted to file refund applications for these periods but encountered persistent and documented technical glitches on the GSTN portal, which prevented timely filing.

The assessee had escalated the technical issue through the portal's grievance mechanism, and a ticket was indeed generated acknowledging the problem. However, there was no timely resolution of the issue by the portal authorities, and the assessee could eventually upload the refund claim only in February 2020 — beyond the two-year limitation period reckoned from the relevant dates. The assessee's attempts to file manual refund claims were also refused by the Revenue Authority.

The Crux: Legal Principles Established

The Delhi High Court Division Bench respectfully disagreed with the Madras High Court's broader holding that the two-year limitation period under Section 54(1) of the CGST Act is directory in nature. However, the Court upheld a more targeted and equally powerful principle: where a taxpayer has made a bona fide attempt to file a refund application within the prescribed period but was prevented from doing so on account of technical glitches on the GST portal or due to any delay or failure attributable to the GST authorities themselves, the refund claim cannot be denied on account of such delay.

The key legal principles established by the Delhi High Court are:

Principle 1 — Bona Fide Effort + Authority-Attributable Delay = No Denial on Limitation

The Court drew a principled distinction between a taxpayer who has simply failed to file within time through their own inaction, and a taxpayer who made bona fide attempts to comply but was thwarted by systemic failures. In the latter case, the limitation period cannot be applied rigidly to defeat a valid claim.

Principle 2 — Portal Technical Failures Are Attributable to the GST Authorities

The GSTN portal is administered and maintained under the oversight of the government and its designated authorities. Technical failures on the portal — which prevent a taxpayer from uploading or filing a refund application — constitute a failure attributable to the GST authorities. The taxpayer's documentary evidence of having raised a grievance ticket on the portal is direct and corroborative proof of bona fide intent.

How Your Business Can Leverage This Judgment

This judgment provides targeted protection in the following circumstances:

-

You are an early-period GST registrant (July 2017 to March 2019) whose refund applications could not be filed timely due to portal non-operability or technical errors — this judgment validates your claim that the delay was not voluntary.

-

You have documentary evidence of having raised a portal grievance ticket, written to the helpdesk, or made attempts to file manually — such documentation constitutes proof of bona fide intent, which the Court held must be considered before denying the refund on limitation grounds.

-

Revenue Authority refused your manual refund application during the period of portal non-availability — the Court's observations support that such refusal was itself impermissible.

PART II

IGST on Ocean Freight — Refund Rights Under the Mohit Minerals Doctrine

CASE 3 OF 4 — UNION OF INDIA v. MOHIT MINERALS (P.) LTD. — SUPREME COURT

Complete Citation Details

| Case Name | Union of India & Others v. Mohit Minerals Private Limited |

| Citation — Taxmann | [2022] 138 taxmann.com 331 |

| Citation — GST Reporter | 92 GST 101 |

| Citation — GSTL | 2022 (61) G.S.T.L. 257 (S.C.) |

| Citation — TMI | 2022 (5) TMI 968 |

| Court | Supreme Court of India |

| Coram | Constitution Bench (Five-Judge Bench) |

| Provisions Examined | Entry 10 of Schedule III of CGST Act, 2017; Notification No. 10/2017-Integrated Tax (Rate); Article 286 of the Constitution of India; Section 5(4) of the IGST Act (RCM on services) |

Background & Legal Issue

This is the landmark Supreme Court Constitution Bench ruling that fundamentally altered the landscape of IGST on ocean freight in the context of CIF (Cost, Insurance, and Freight) imports into India. The central issue was whether the Indian Government could levy IGST on ocean freight services under the Reverse Charge Mechanism (RCM) on the importer — when IGST was already being levied on the entire CIF value of the imported goods (which, by definition, includes the freight component).

In a CIF import transaction, the exporter (located outside India) contracts with a foreign shipping line to transport goods to India. The cost of freight is embedded within the CIF contract price. The importer in India pays IGST on the entire CIF value — which inherently includes the ocean freight component. The government had separately issued Notification No. 10/2017-IGST(Rate) to impose an additional IGST levy on ocean freight under RCM, treating the importer as the recipient of transport services.

The Crux: The Constitutional Bar on Double Taxation

The Supreme Court, in a landmark Constitution Bench ruling, struck down Notification No. 10/2017-IGST(Rate) and Entry 10 of Schedule III of the CGST Act as unconstitutional and ultra vires. The Court held that the levy of IGST on ocean freight under RCM on the importer constituted double taxation — since the freight cost was already subsumed within the CIF value on which IGST had been paid. Parliament's taxing power under GST does not extend to creating a second levy on the same economic event. The levy was held to be beyond the legislative competence of Parliament.

The Gujarat High Court had first struck down this levy and the Supreme Court affirmed the said ruling. The tax collected from importers across the country on account of IGST on ocean freight under RCM thus became an amount collected without legal authority.

How Your Business Can Leverage This Judgment

If your business has paid IGST on ocean freight charges under RCM during the period when Notification No. 10/2017-IGST(Rate) was operative — specifically for periods prior to the date the levy was struck down — the Supreme Court's ruling creates a constitutional entitlement to refund of such amounts. The specific scenarios are:

-

Your enterprise is an importer of goods on CIF terms and has paid IGST on ocean freight under RCM in addition to IGST on the CIF value of goods — you are entitled to claim refund of the ocean freight IGST paid under RCM.

-

Your refund application was rejected because the Revenue Authority had not accepted the legal position (as the Mohit Minerals judgment had not yet been delivered at that time) — the Supreme Court's ruling, being retrospective in effect, requires the Revenue to reconsider such applications.

-

Your refund claim was denied partly on grounds of limitation — the ARS Energy judgment discussed below directly addresses this situation.

CASE 4 OF 4 — ARS ENERGY PVT. LTD. v. ADDITIONAL COMMISSIONER (APPEALS)

Complete Citation Details

| Case Name | ARS Energy Private Limited v. Additional Commissioner (Appeals), Chennai |

| Citation — Centax | (2023) 13 Centax 300 (Mad.) |

| Citation — Taxmann | 2023 (157) taxmann.com 610 (Madras) |

| Court | Madras High Court |

| Writ Petition | Arising out of challenge to Order dated 24-09-2020 passed by Appellate Authority |

| Provisions Examined | Section 54(1) of CGST Act, 2017; Supreme Court ruling in Mohit Minerals; Madras HC ruling in Lenovo (India) — W.P. No. 23604 of 2022 |

Background & Factual Matrix

ARS Energy Private Limited is an importer who had paid IGST on ocean freight charges under RCM for the months of December 2017 (Rs. 10,53,594) and January 2018 (Rs. 13,25,232). The company duly filed a refund application to recover these amounts. The Revenue Authority rejected the application on 18.06.2020, and the Appellate Authority confirmed the rejection vide order dated 24.09.2020.

At the time of rejection of the refund application, the Supreme Court had not yet delivered its ruling in Mohit Minerals. Consequently, the Revenue took the position that the levy was legally valid and that refund was not admissible. The rejection was also partly premised on limitation grounds.

ARS Energy then filed a writ petition before the Madras High Court challenging the rejection order — and the landscape had by then entirely changed, with the Supreme Court having delivered the Mohit Minerals ruling affirming that the ocean freight levy was unconstitutional.

The Crux: Legal Principles Established

The Madras High Court held that the rejection of ARS Energy's refund application was legally unsustainable on both grounds invoked by the Revenue. The Court observed that: (i) ARS Energy had, as an importer, paid IGST on the entire CIF value including the embedded freight component, and had additionally paid IGST on ocean freight under RCM — resulting in double IGST on the freight element, which was constitutionally impermissible per Mohit Minerals; and (ii) the limitation ground was equally unavailable to the Revenue, as the two-year limitation under Section 54(1) of the CGST Act is directory in nature per the Lenovo ruling — and in this case, the delay in filing was explained by the fact that the controlling legal position (Mohit Minerals) had not existed at the time.

The Court set aside the rejection order and remitted the matter to the Revenue for fresh consideration, with the following binding directions:

-

The refund application is to be re-considered in light of the law laid down by the Supreme Court in Mohit Minerals and the Madras HC in the Lenovo case.

-

A personal hearing must be afforded to the petitioner before passing any fresh order.

-

All issues raised by both parties are to be considered on merits and in accordance with law.

-

The entire exercise is to be completed within three months of receipt of the Court's order.

How Your Business Can Leverage This Judgment

This judgment is particularly significant for importers who may have previously received an unfavourable order on their ocean freight IGST refund applications on the ground that the law did not support their claim. The following scenarios are directly addressed by this ruling:

-

Your refund application for IGST paid on ocean freight under RCM was rejected because the Supreme Court's Mohit Minerals ruling had not been delivered at that time — the ARS Energy judgment confirms that such cases must be re-examined in light of the subsequently delivered controlling precedent.

-

Revenue invoked limitation to block your refund claim even though the legal basis for your claim (i.e., the unconstitutionality of the levy) was only established after the Mohit Minerals decision — the Court's application of the 'directory' nature of Section 54(1) limitation directly supports your case for delay condonation.

-

Your refund claims for December 2017 and/or January 2018 were refused by both the adjudicating authority and the appellate authority — you may re-approach the appropriate authority citing this judgment and seek fresh adjudication.

Consolidated Action Plan for Businesses

The four judgments discussed in this article collectively establish a taxpayer-friendly framework that substantially shifts the balance of power in refund proceedings. The following action plan is recommended for businesses that fall within the ambit of these rulings:

| # | Situation | Applicable Precedent |

| 1 | SEZ supplier denied refund due to delayed endorsement by SEZ Approving Officer | Lenovo (India) — Madras HC [2023] |

| 2 | SEZ supplier denied refund as documents submitted at personal hearing, not at application stage | Lenovo (India) — Estoppel Principle |

| 3 | Refund application filed beyond two years due to administrative / endorsement delays | Lenovo (India) — Section 54(1) is directory |

| 4 | Refund rejected without issuing Rule 90(3) deficiency memo | Lenovo (India) — Procedural Safeguard |

| 5 | Exporter could not file refund on time due to GSTN portal technical failure | Sethi (Sons) — Delhi HC DB [2023] |

| 6 | Importer paid IGST on ocean freight under RCM in addition to IGST on CIF goods value | Mohit Minerals — Supreme Court [2022] |

| 7 | Ocean freight IGST refund rejected when Mohit Minerals ruling was not yet available | ARS Energy — Madras HC [2023] |

Practical Due Diligence Steps

Before initiating any legal action or fresh refund application on the basis of the precedents discussed, businesses are advised to undertake the following preparatory steps:

-

Conduct a comprehensive audit of all refund applications filed since July 2017 — identify those that were rejected, those pending for disposal, and those where orders were passed without affording an opportunity of personal hearing.

-

For SEZ suppliers: compile and preserve all endorsed invoices, even if endorsements were made beyond 45 days. Verify whether the endorsement is signed and authentic — courts have held that mere delay in endorsement does not vitiate the endorsement itself.

-

For importers on CIF terms: obtain IGST payment records for both (a) IGST on the CIF value of goods and (b) IGST paid on ocean freight under RCM. The double payment is the cornerstone of the refund entitlement.

-

Preserve all documentary evidence of portal grievance tickets, helpdesk communications, or any written representation to the Revenue Authority evidencing the bona fide attempt to file within time.

-

Consult with a qualified GST practitioner to determine whether refund applications should be filed afresh or whether a writ petition before the appropriate High Court is the more efficacious remedy, particularly where limitation bars ordinary administrative filing.

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified