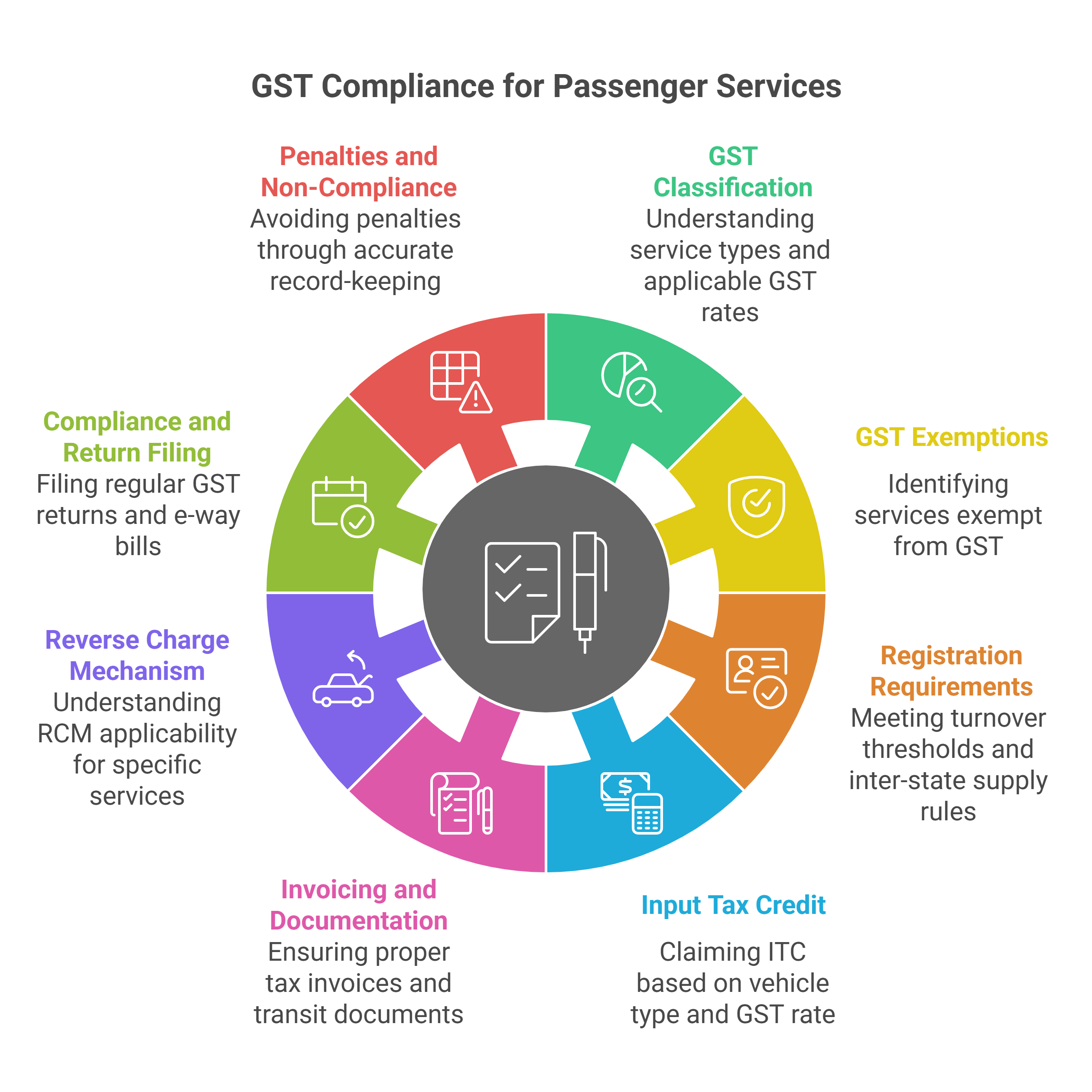

GST Concepts and Procedures for Passenger Service Companies

This comprehensive guide is tailored for the CFO of a company engaged in passenger services, outlining all critical Goods and Services Tax (GST) concepts, compliance requirements, and operational procedures relevant to the sector.

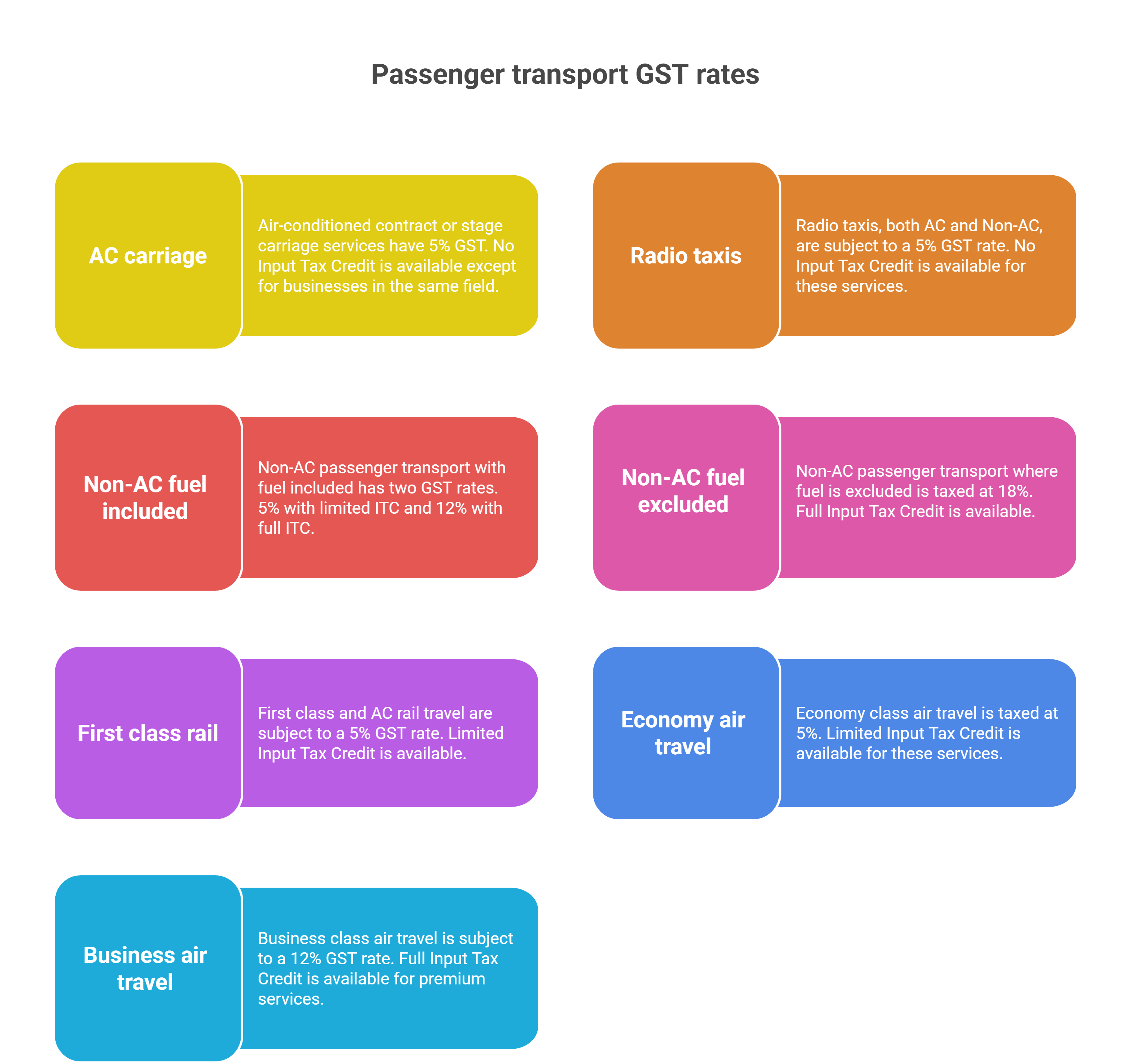

1. GST Classification and Applicability

Passenger transport services are classified under SAC Code 9964. The GST rates and conditions vary based on the type of service and vehicle specifications:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

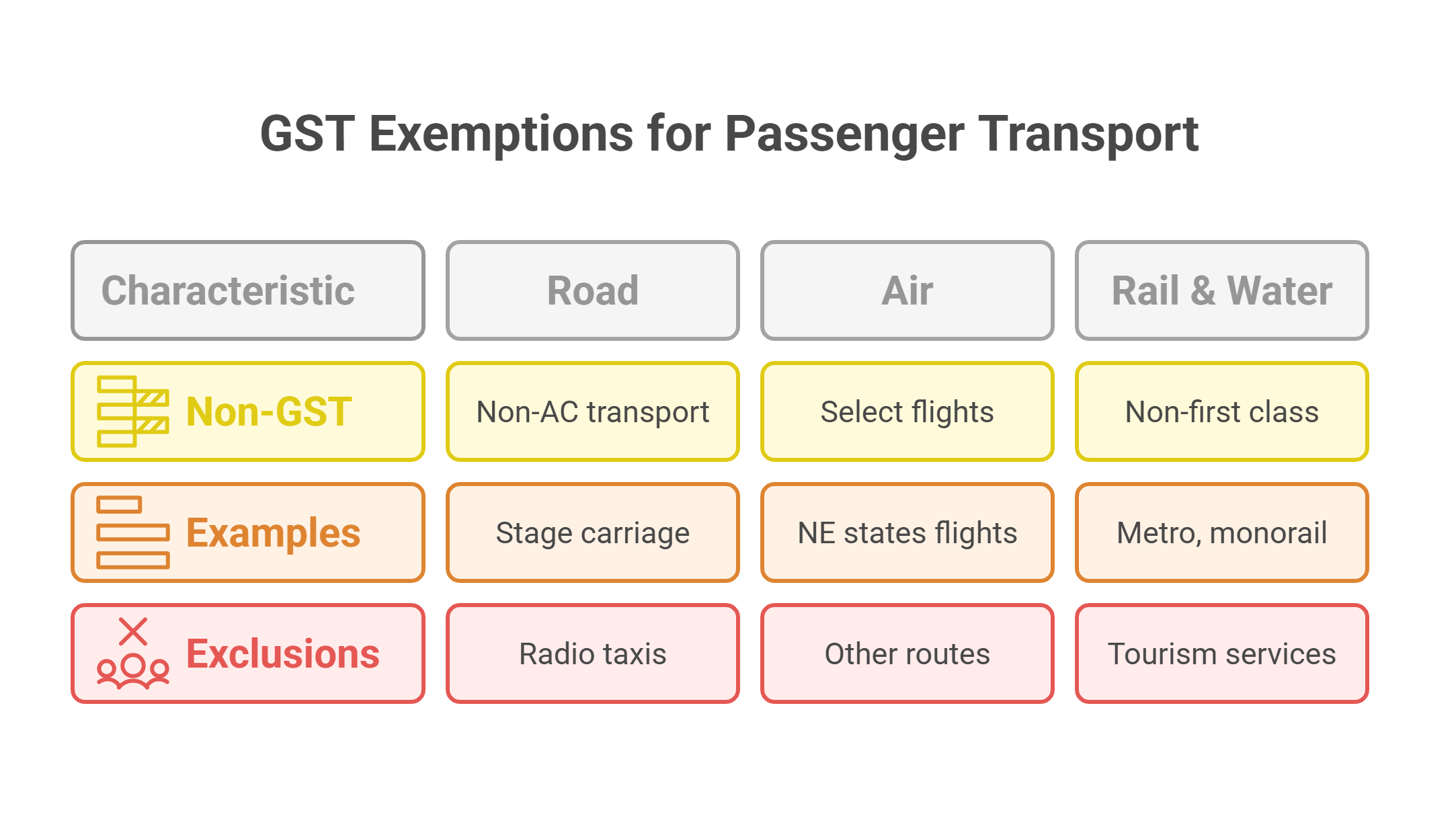

2. GST Exemptions

Certain passenger transport services are exempt from GST:

-

Road Transport:

-

Non-AC contract/stage carriage (excluding radio taxis, tourism, charter, or hire)

-

Public transport, metered cabs, auto-rickshaws (including e-rickshaws)

-

-

Air Transport:

-

Flights to/from airports in North-Eastern states and Bagdogra (West Bengal)

-

-

Rail & Water Transport:

-

Non-first class and non-AC railway services

-

Metro, monorail, tramway

-

Inland vessel transport (excluding tourism)

-

3. GST Registration Requirements

-

Mandatory Registration:

-

Registration is mandatory if the aggregate turnover exceeds ₹40 lakhs in a financial year. For special category states (e.g., Northeastern states, Himachal Pradesh, Uttarakhand), the threshold is ₹20 lakhs.

-

Inter-state supply of passenger transport services (regardless of turnover)

-

Services subject to reverse charge mechanism (RCM)

-

-

Benefits:

-

Ability to claim Input Tax Credit (ITC) where eligible.

-

Enhanced business credibility and compliance.

-

Access to formal contracts and financing.

-

-

Exemptions from Registration:

-

Companies providing only exempt passenger transport services (e.g., non-AC buses, public transport) are not required to register unless they cross the turnover threshold with taxable supplies.

-

Note: GST registration is state-specific; companies operating in multiple states must register separately in each state.

4. Input Tax Credit (ITC) Provisions

-

Eligibility:

-

ITC allowed for vehicles with seating capacity >13 persons (including driver)

-

ITC available on fuel, vehicle purchase, and maintenance (subject to GST rate chosen)

-

-

Restrictions:

-

No ITC for vehicles ≤13 seats (including driver)

-

Limited ITC at 5% GST rate; full ITC at 12% GST rate

-

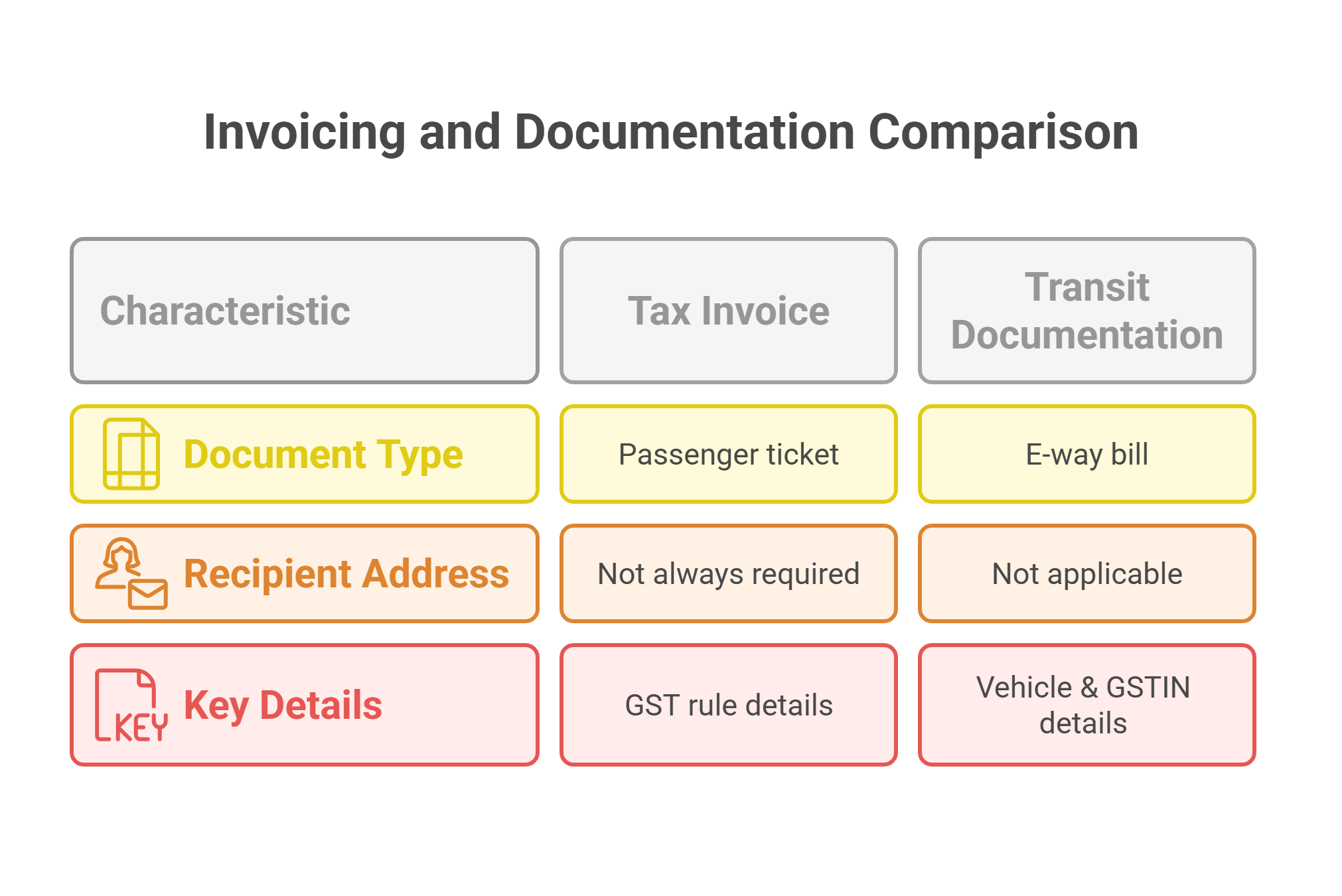

5. Invoicing and Documentation

-

Tax Invoice:

-

Passenger ticket serves as tax invoice (physical or electronic)

-

May not require recipient’s address

-

Must include prescribed details as per GST rules

-

-

Transit Documentation:

-

Valid tax invoice/ticket

-

E-way bill (if transporting goods >₹50,000 in value)

-

Vehicle registration and GSTIN details

-

6. Reverse Charge Mechanism (RCM)

-

General Rule: Passenger transport services are not under RCM.

-

Exceptions: RCM applies to specific vehicle rental services with operator, when:

-

Motor vehicle designed for passenger transport

-

Fuel cost included in consideration

-

Supplier is not a company

-

Supplier charges 5% GST

-

7. GST Compliance and Return Filing

-

Regular Returns:

-

GSTR-1: Outward supplies (monthly/quarterly)

-

GSTR-3B: Monthly summary return

-

GSTR-9: Annual return

-

-

E-way Bill:

-

Required for goods transport (not for pure passenger services)

-

Transporters must enroll for e-way bill generation

-

8. Penalties and Non-Compliance

-

Common Issues:

-

Late return filing

-

Incorrect GST rate application

-

Failure to issue proper invoices

-

Non-registration despite eligibility

-

-

Mitigation:

-

Maintain accurate records

-

Regular compliance checks

-

Professional tax consultation

-

Timely filing and payment

-

9. Recent Updates (as of 2025)

-

HSN Code Reporting: Companies with turnover >₹5 crore must report 8-digit HSN codes for transport services

-

Enhanced Documentation: Stricter requirements for ticketing and record-keeping

10. Best Practices for CFOs

-

Evaluate service mix to determine applicable GST rates and exemptions

-

Monitor ITC eligibility based on vehicle type and GST rate

-

Ensure robust documentation for all transactions and compliance filings

-

Stay updated with GST Council notifications and amendments

By adhering to these GST concepts and procedures, a passenger service company can ensure full compliance, optimise tax liability, and maintain operational efficiency within the regulatory framework.

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified