A 2025 Playbook for Accounts & Finance Professionals

1️. Statutory Meaning of “Educational Institution”

-

Derived from Clause 2(y) of Notification No. 12/2017-CTR—covers only:

-

Pre-school to higher-secondary (or equivalent).

-

Courses forming part of a curriculum that culminates in a qualification recognised by Indian law.

-

Approved vocational education courses (now vetted by NCVET, post-Oct 2024 amendment).

-

-

Private coaching centres, adult skilling platforms or MOOC providers do not fall inside this definition unless their course is formally recognised.

-

Consequence: exemption entries hinge on this label—wrong classification can trigger unwelcome 18 % tax plus interest and penalty.

2️. 100 % Exempt Supplies – BY an Educational Institution

-

Core services to students/faculty/staff (tuition, library, lab, convocation, placement-linked training).

-

Entrance‐exam services—including CAT/JEE/NEET—if the exam is conducted by the institution itself or a government-established testing body.

-

Boarding, lodging & in-house meals where education is the “principal supply”.

-

Flagship programmes of IIMs (2-year PGDM, FPM, 5-year IPM)—but not Executive Development Programmes.

-

Education delivered by charitable trusts registered u/s 12AA/12AB to vulnerable groups (orphans, prisoners, rural 65+ etc.).

3️. Exempt Inputs – TO Pre-School & K-12 Institutions

(The famous Entry 66(b) carve-out)

-

Student/faculty transport.

-

Catering, incl. Mid-Day Meal (even if sponsored by CSR or grants).

-

Security, cleaning, housekeeping contracts.

-

Services “relating to admission or conduct of examination”.

⚠️ Higher-education entities lose these breaks—they pay GST on outsourced buses, canteen, security etc. Remember to factor this into budgeting & fee fixation.

4️. Spotlight on Special Exemptions & Clarifications

-

Affiliation fees:

-

Government schools—zero-rated from 10 Oct 2024 (Entry 66A).

-

Private schools & university–college arrangements—taxable @ 18 %.

-

-

Skill ecosystem: services by or to NSDC/NCVET stakeholders remain exempt (Entry 69, tweaked Jan 2025).

-

Rehabilitation therapy & counselling inside an educational campus—non-taxable when supplied by professionals registered under the RCI Act.

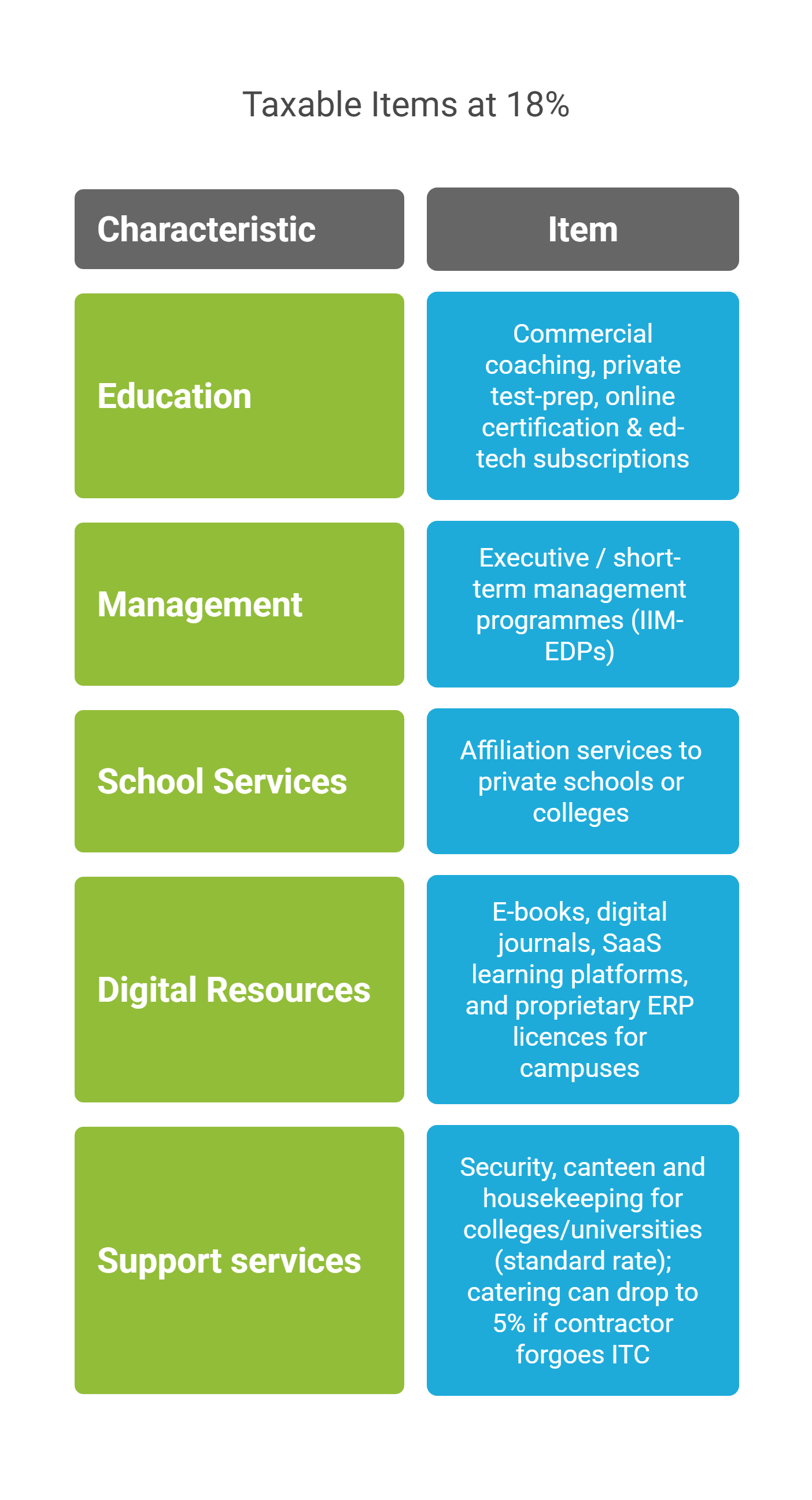

5️. What’s Taxable @ 18 % (Unless Notified Otherwise)

-

Commercial coaching, private test-prep, online certification & ed-tech subscriptions.

-

Executive / short-term management programmes (IIM-EDPs).

-

Affiliation services to private schools or colleges.

-

E-books, digital journals, SaaS learning platforms, and proprietary ERP licences for campuses.

-

Security, canteen and housekeeping for colleges/universities (standard rate); catering can drop to 5 % if contractor forgoes ITC.

6️. Quick-Glance Rate Card for Goods

7️. Compliance Checklist (May 2025 Edition)

-

Registration

-

Exempt-only schools: no GSTIN needed (s.23).

-

Mixed supplies or annual aggregate turnover > ₹20 lakh: compulsory GSTIN (s.22).

-

-

Return Suite

-

GSTR-3B monthly (or QRMP) for taxable institutions.

-

GSTR-1 outward supplies; GSTR-9 annual reconciliation.

-

-

Records—keep separate books for exempt v. taxable streams (rule 56).

-

Input Tax Credit

-

Blocked on inputs attributable to exempt core education (s.17 (2)).

-

Apportion via rule 42/43 if campus runs a taxable canteen/book-shop.

-

-

Reverse Charge—watch services under Notif. 13/2017 (e.g., legal services from advocates).

-

E-Invoice / E-Way Bill obligations apply once turnover thresholds kick in (₹5 crore & ₹50k consignment respectively).

8️. Recent Amendments & Judicial Signals

-

Notification 08/2024-CTR (10 Oct 2024) — new Entry 66A for board affiliation to government schools.

-

Notification 06/2025-CTR (16 Jan 2025) — extended NCVET coverage in vocational exemptions.

-

Circular 234/28/2024-GST — crystal-clear that university–college affiliation is taxable.

-

Educational Initiatives (Guj. HC)—exam services to schools treated as “examination” and therefore exempt.

9️. Advisory Nuggets for Practitioners

-

Bundle smartly—where education is dominant, subsume hostel/mess to keep the supply composite & exempt.

-

Segment accounting—track taxable ancillaries (canteen, bookstore, rentals) to protect ITC and avoid disputes.

-

Contract vetting—affiliation, transport, catering agreements should quote the exact GST entry and rate to avert vendor mismatch.

-

Due-diligence on ed-tech vendors—verify if software is SaaS (service) or licence (goods); tax position differs.

-

Monitor Council minutes—GST Council updates (esp. on CSR-funded schemes, hybrid learning) often surface via press releases before formal notifications.

🔚 Conclusion

India’s GST law preserves a zero-tax corridor for core, recognised education while taxing the commercial fringes. For finance controllers and accountants, the winning strategy is precise classification, airtight documentation, and proactive planning around mixed supplies. Follow the bullet-point map above to stay compliant, optimise input credits, and insulate your campus—or your client’s—against audit surprises.

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified