GST and M&A Transactions: Due Diligence & Integration Challenges

Executive Summary

In the complex landscape of mergers and acquisitions, Goods and Services Tax (GST) considerations have emerged as critical value drivers—and potential deal-breakers. A comprehensive GST assessment during due diligence can uncover hidden liabilities ranging from 10-30% of deal value, while post-merger integration challenges can disrupt business continuity and erode anticipated synergies.

In the complex landscape of mergers and acquisitions, Goods and Services Tax (GST) considerations have emerged as critical value drivers—and potential deal-breakers. A comprehensive GST assessment during due diligence can uncover hidden liabilities ranging from 10-30% of deal value, while post-merger integration challenges can disrupt business continuity and erode anticipated synergies.

For CEOs, CFOs, and Finance Directors navigating M&A transactions, understanding GST implications is no longer optional—it's a strategic imperative that directly impacts valuation, deal structuring, and post-merger value realisation.

The Strategic Importance of GST in M&A

GST complexity in M&A transactions stems from multiple dimensions: historical compliance gaps, ongoing litigation, input tax credit (ITC) eligibility, classification disputes, and transfer pricing implications. Unlike other tax considerations, GST liabilities can crystallise rapidly post-transaction, creating immediate cash flow pressures and reputational risks.

Recent regulatory developments—including increased scrutiny through data analytics, stricter ITC reconciliation requirements, and e-invoicing mandates—have amplified these risks. Acquirers who overlook GST due diligence often face post-acquisition surprises that materially impact IRR and stakeholder confidence.

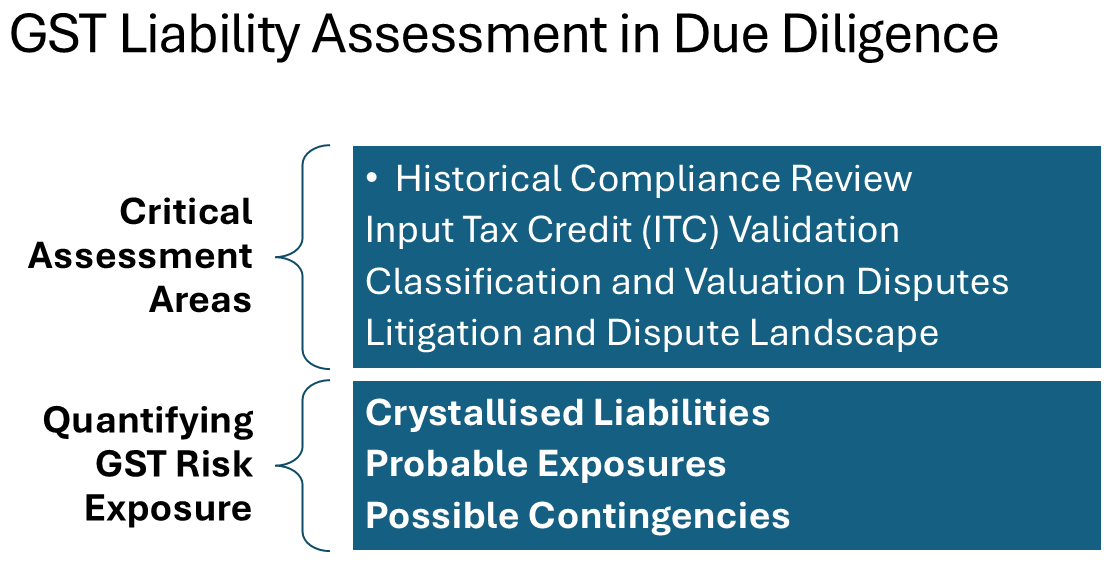

1. GST Liability Assessment in Due Diligence

Critical Assessment Areas

A. Historical Compliance Review

The foundation of GST due diligence lies in assessing the target's compliance track record over the assessment period (typically 3-5 years). This involves examining:

-

Return Filing Consistency: Verification of GSTR-1, GSTR-3B reconciliation and timely filing across all GSTINs. Persistent mismatches between outward supplies reported and actual filings indicate systemic issues.

-

Payment History Analysis: Assessment of interest and penalty exposures arising from delayed payments. Even minor delays compound significantly, affecting working capital projections.

-

Assessment and Audit History: Review of GST audits, assessments under Section 61, anti-profiteering investigations, and demand notices. Pending assessments represent contingent liabilities requiring specific indemnities.

B. Input Tax Credit (ITC) Validation

ITC represents a significant asset on the balance sheet, yet it's often the most vulnerable area in GST due diligence:

-

Eligibility Verification: Confirmation that ITC claimed relates to eligible inputs, input services, and capital goods used for taxable supplies. Common issues include ITC on blocked credits (motor vehicles, construction, food & beverages) and personal consumption items.

-

Documentary Compliance: Validation of invoice-level documentation, vendor GSTIN verification, and supplier filing status. The "no payment, no ITC" rule after 180 days creates reversals that many targets fail to account for.

-

Reconciliation Status: GSTR-2A/2B matching with books of accounts and GSTR-3B. Unreconciled differences often indicate inflated ITC claims vulnerable to reversal during scrutiny.

-

Transitional Credit: For older acquisitions, verification of TRAN-1/TRAN-2 credit claims and proper documentation of pre-GST credit transitions.

C. Classification and Valuation Disputes

Classification drives tax rates and can create substantial exposure:

-

Product/Service Classification: Assessment of whether goods/services have been correctly classified under the appropriate HSN/SAC codes. Healthcare, food processing, and technology sectors face particular complexity.

-

Valuation Disputes: Review of related party transactions, free supplies, discounts, and composite supply determinations. Transfer pricing adjustments can trigger GST implications under the anti-abuse provisions.

-

Place of Supply Issues: For inter-state transactions and services, validation of correct place of supply determination affecting IGST vs. CGST/SGST treatment.

D. Litigation and Dispute Landscape

Outstanding litigation creates uncertainty that must be quantified:

-

Pending Appeals: Assessment of cases pending at various appellate levels, probability of success, and financial exposure, including interest and penalties.

-

Pre-GST Legacy: For businesses operating before July 2017, exposure from VAT, excise, and service tax disputes that may impact GST positions or transitional credits.

-

Show Cause Notices: Evaluation of pending investigations, their merit, and potential financial impact. Strategic decisions on settlement vs. litigation affect deal timing and structure.

Quantifying GST Risk Exposure

Finance leaders should employ a three-tiered risk quantification approach:

-

Crystallised Liabilities: Known demands, confirmed assessment orders, and admitted errors requiring immediate provisioning.

-

Probable Exposures: Issues with >50% likelihood of materialisation based on regulatory precedents and audit patterns. These should factor into purchase price adjustments.

-

Possible Contingencies: Lower probability issues requiring disclosure and indemnification clauses but not necessarily impacting headline valuation.

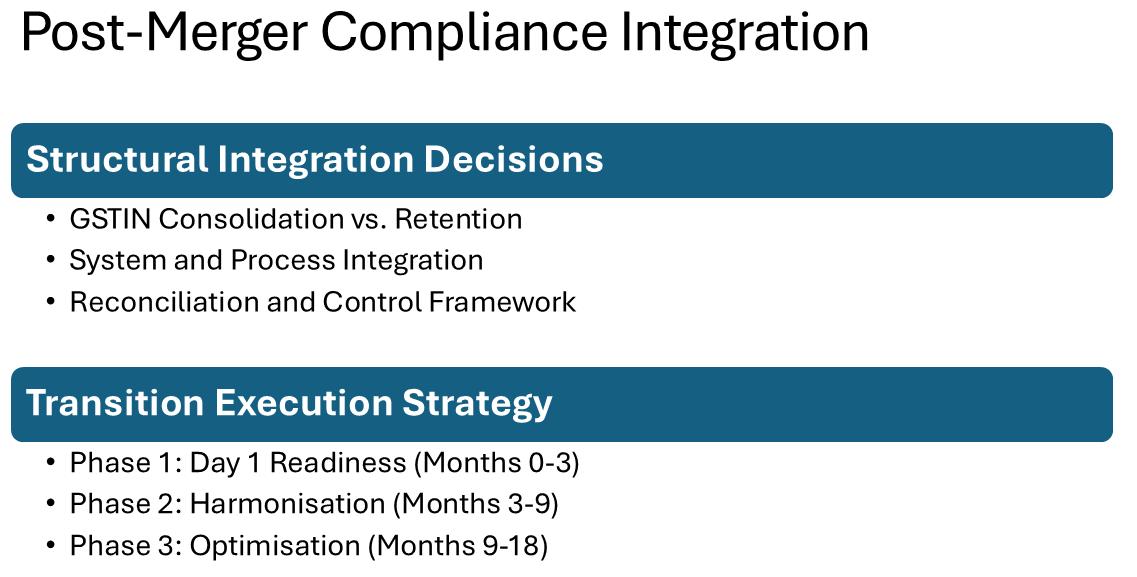

2. Post-Merger Compliance Integration

Post-merger integration is where GST complexity translates into operational reality. Poor integration planning can result in compliance failures, business disruptions, and loss of input tax credits worth millions.

Structural Integration Decisions

A. GSTIN Consolidation vs. Retention

One of the first strategic decisions post-acquisition involves the target's GST registrations:

-

Consolidation Benefits: Centralised compliance, reduced filing burden, unified ITC pool, simplified reporting. Suitable when businesses are genuinely integrated with common operations.

-

Retention Rationale: Preservation of separate registrations may be necessary for multi-state operations, distinct business verticals, special economic zone (SEZ) units, or when maintaining operational autonomy.

-

Regulatory Requirements: Transfers of business as a going concern require proper GSTIN succession planning to prevent ITC loss and ensure continuity of registrations.

The decision impacts working capital (ITC utilisation across units), compliance costs, and operational flexibility.

B. System and Process Integration

Successful GST integration demands harmonisation across:

-

ERP Systems: Integration or interfacing of accounting systems, ensuring GST-compliant invoice formats, automated return generation, and real-time ITC tracking.

-

E-invoicing and E-way Bills: Consolidation of e-invoice registration, API integrations, and transportation documentation systems. Different system architectures often create integration challenges.

-

Master Data Management: Harmonisation of vendor master data, GSTIN validation, product classification codes (HSN/SAC), and tax rate matrices. Inconsistent master data is the leading cause of post-merger compliance failures.

C. Reconciliation and Control Framework

Establishing robust controls is critical:

-

Monthly Reconciliation Protocols: Standardised processes for GSTR-2A/2B matching, ITC eligibility reviews, and compliance certifications across all merged entities.

-

Reverse Charge Monitoring: Consolidated tracking of reverse charge obligations, particularly for imported services and GTA (Goods Transport Agency) services.

-

Compliance Calendar: Unified compliance calendar incorporating all return filing deadlines, payment obligations, and audit requirements across jurisdictions.

Transition Execution Strategy

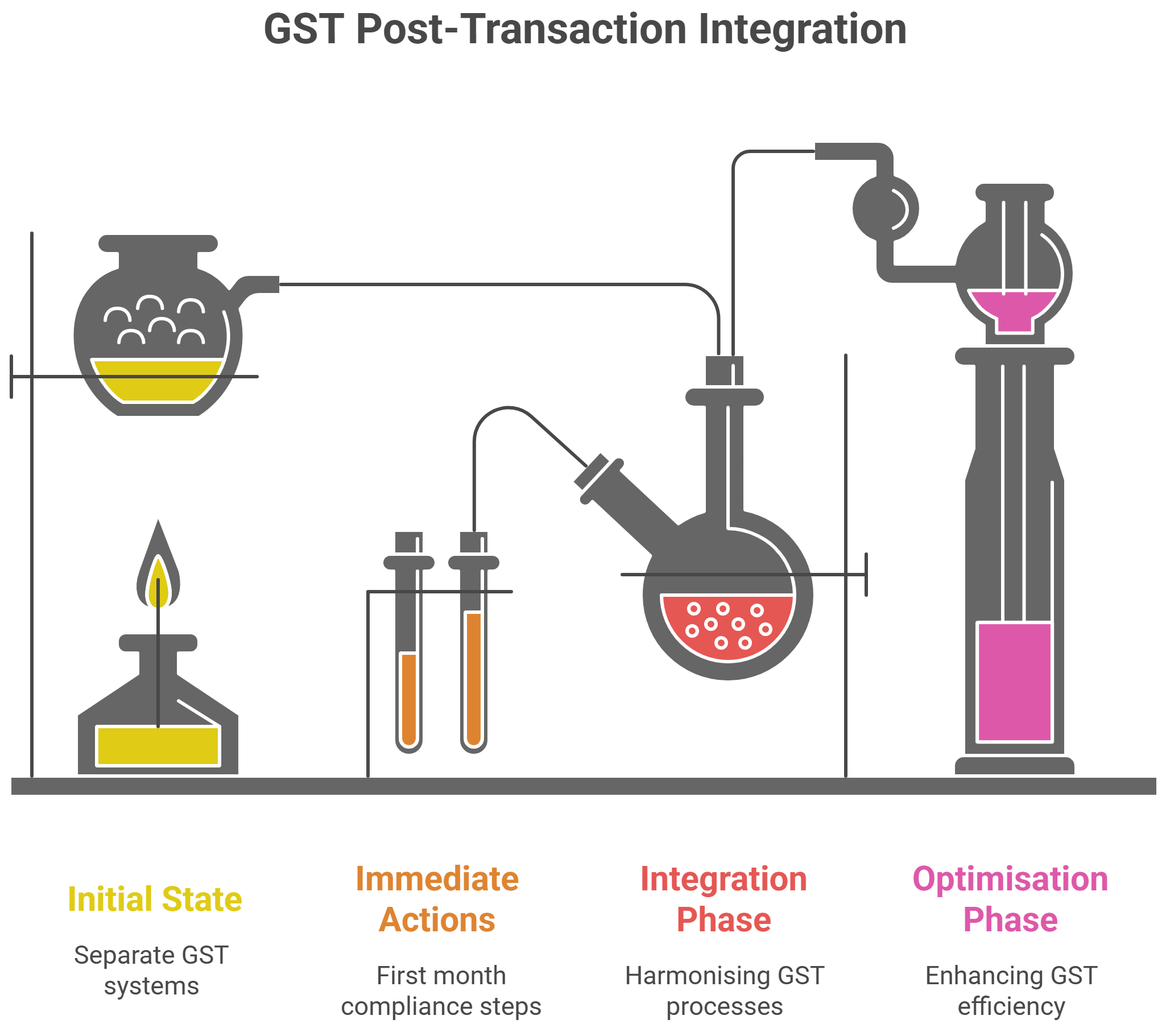

Phase 1: Day 1 Readiness (Months 0-3)

-

Ensure continuation of all GST registrations and immediate filing obligations

-

Establish interim reporting lines and compliance responsibilities

-

Implement emergency protocols for time-sensitive filings

-

Communicate with vendors and customers about transition arrangements

Phase 2: Harmonisation (Months 3-9)

-

Standardise the chart of accounts and GST accounting policies

-

Implement integrated compliance technology platforms

-

Train combined finance teams on harmonised processes

-

Execute GSTIN consolidation if strategically decided

Phase 3: Optimisation (Months 9-18)

-

Rationalise supply chains for GST efficiency

-

Optimise ITC utilisation across the combined entity

-

Implement advanced analytics for compliance monitoring

-

Realise tax efficiency synergies through structural optimisation

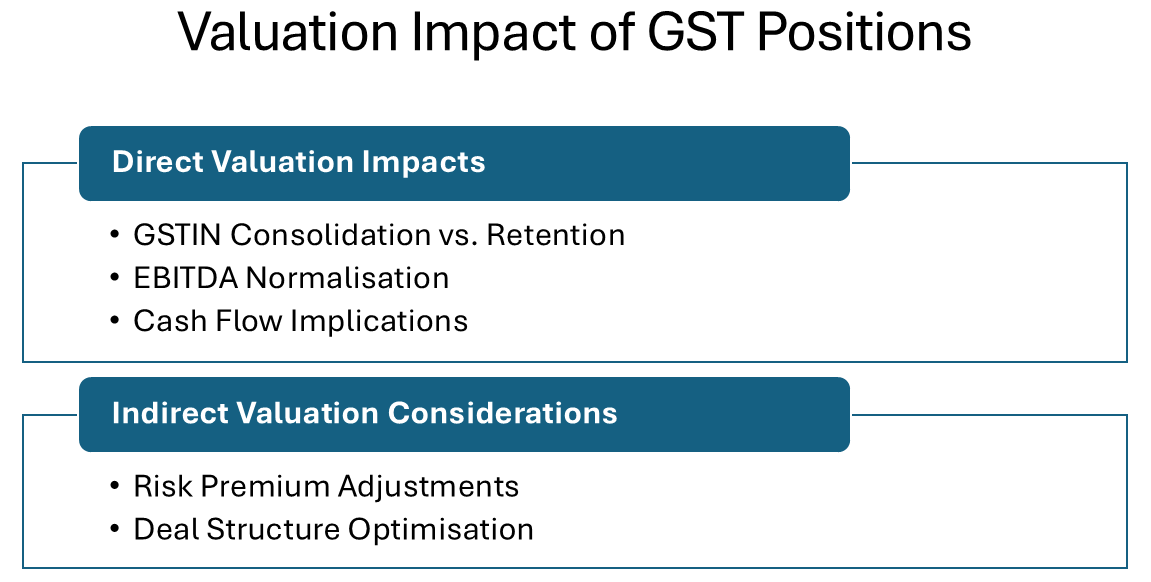

3. Valuation Impact of GST Positions

GST considerations directly impact M&A valuation through multiple channels, yet they're often insufficiently reflected in financial models.

Direct Valuation Impacts

A. Working Capital Adjustments

GST positions significantly affect normalised working capital:

-

ITC Receivable Quality: ITC booked in balance sheets requires adjustment for eligibility issues, vendor filing gaps, and time-barred credits. A 15-25% haircut on ITC balances is common in risk-adjusted valuations.

-

GST Payable Recognition: Unrecorded liabilities from revenue timing differences, classification disputes, or compliance gaps must be normalised. These often emerge from the reconciliation of GSTR-3B with books.

-

GST Refund Claims: Pending refunds (particularly for exports, inverted duty structure, or accumulated ITC) should be discounted for realisation risk and timing.

B. EBITDA Normalisation

GST disputes and non-compliance create below-the-line adjustments:

-

Interest and Penalty Provisions: Ongoing interest on delayed payments and potential penalties should be normalised out of EBITDA to reflect true operating performance.

-

One-time Compliance Costs: Expenditure on rectification, professional fees for dispute resolution, and settlement costs should be treated as non-recurring.

-

ITC Reversals: Material ITC reversals due to compliance failures require adjustment to present accurate gross margins.

C. Cash Flow Implications

GST affects cash flow projections through:

-

Cash Tax Rates: Actual GST cash outflow considering ITC utilisation efficiency, assessment payments, and refund timing.

-

Working Capital Intensity: GST compliance gaps often require additional working capital infusion post-acquisition for catch-up payments and system improvements.

Indirect Valuation Considerations

A. Risk Premium Adjustments

Significant GST exposures may warrant:

-

Higher discount rates reflecting execution risk and regulatory uncertainty

-

Shorter forecast horizons due to compliance unpredictability

-

Scenario analysis with downside cases for adverse litigation outcomes

B. Deal Structure Optimisation

GST considerations influence asset vs. share purchase decisions:

-

Asset Purchases: GST implications on slump sale (going concern transfer) vs. itemised asset purchase. The former attracts no GST but requires specific compliance; the latter creates GST cost affecting deal economics.

-

Share Purchases: No direct GST impact on share transfers, but acquirer inherits all historical liabilities. Requires a robust indemnification framework.

-

Demerger/Restructuring: Pre-transaction restructuring for GST efficiency must consider timing, costs, and regulatory approvals.

4. Transition Planning Strategies

Effective transition planning bridges due diligence insights with post-merger integration execution, ensuring the protection and realisation of value.

Pre-Closing Transition Framework

A. Risk Mitigation Structure

-

Indemnification Clauses: Specific GST indemnities covering historical liabilities, ongoing disputes, and ITC reversal risks. Indemnity caps and baskets should reflect quantified exposures.

-

Escrow Arrangements: Portion of purchase consideration held in escrow against identified GST contingencies with clear release triggers.

-

Warranty Framework: Comprehensive GST warranties covering compliance status, litigation disclosure, and ITC validity. Survival periods should extend beyond the assessment statute of limitations.

B. Pre-Closing Remediation

For material issues identified during due diligence:

-

Voluntary Disclosure: Strategic assessment of voluntary disclosure under GST provisions to minimise penalty exposure before transaction closing.

-

Dispute Settlement: Evaluation of settlement schemes or alternative dispute resolution mechanisms to crystallise and cap liabilities.

-

Compliance Catch-up: Coordinated effort to complete pending filings, rectify returns, and regularise documentation before ownership transfer.

Post-Closing Integration Roadmap

A. Governance and Accountability

-

Integration PMO: Dedicated workstream for GST integration with clear ownership, milestones, and escalation protocols.

-

Compliance Committee: Cross-functional committee (finance, legal, operations, IT) overseeing GST transition with defined meeting cadence and decision rights.

-

Performance Metrics: KPIs tracking filing timeliness, reconciliation closure rates, ITC realisation efficiency, and audit readiness.

B. Stakeholder Management

-

Tax Authority Engagement: Proactive communication with GST authorities regarding ownership change, GSTIN succession, and pending matters.

-

Vendor/Customer Communication: Transparent communication about invoice formatting changes, GSTIN updates, and payment term impacts.

-

Internal Change Management: Comprehensive training programs for finance teams, awareness sessions for business stakeholders, and helpdesk support during transition.

C. Technology Enablement

-

Compliance Technology: Investment in GST software for automated return filing, reconciliation, and analytics. Solutions should handle multi-entity complexity post-merger.

-

Data Migration: Careful planning for historical data migration, ensuring no loss of ITC documentation or compliance records.

-

Integration Architecture: API-based integrations between ERP, banking, and GST portal for seamless data flow and real-time compliance visibility.

M&A GST Due Diligence Checklist

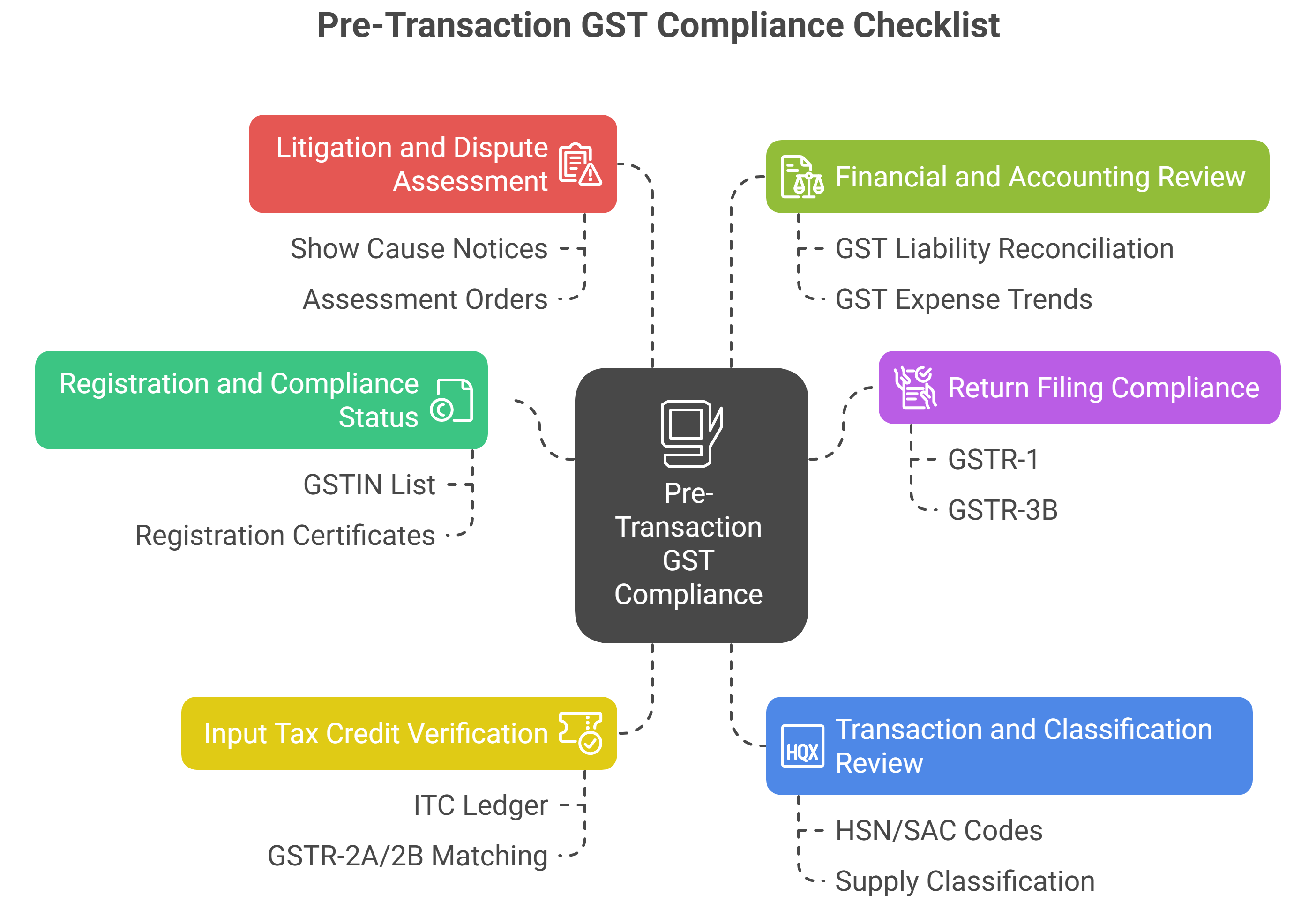

Pre-Transaction Phase

Registration and Compliance Status

-

Obtain the list of all GSTINs across states and business verticals

-

Verify registration certificates and business constitution details

-

Confirm voluntary registration status where applicable

-

Check for any cancelled or suspended registrations

-

Validate registration of all branches, warehouses, and operating locations

Return Filing Compliance

-

Review GSTR-1, GSTR-3B filing history for past 3 years

-

Check for any late filings and interest/late fee payments

-

Verify GSTR-9 (annual return) filing for all applicable years

-

Confirm GSTR-9C (audit reconciliation) submission where required

-

Analyse filing pattern for consistency and red flags

Input Tax Credit Verification

-

Obtain the ITC ledger and reconcile with GSTR-3B claims

-

Perform GSTR-2A/2B matching for the recent 6-12 months

-

Identify mismatches and assess recovery/reversal requirements

-

Review ITC on capital goods and reversal methodology

-

Verify blocked credit segregation (ineligible ITC)

-

Check Rule 42-43 reversal compliance (common/exempt supplies)

-

Confirm vendor filing status for significant ITC suppliers

Transaction and Classification Review

-

Sample test invoices for HSN/SAC code accuracy

-

Review inter-state vs. intra-state supply classification

-

Assess the place of supply determination for services

-

Analyse export/import documentation and LUT/bond status

-

Review related party transactions for valuation correctness

-

Check composite supply and mixed supply treatments

-

Validate reverse charge mechanism compliance

-

Verify e-invoicing compliance (turnover > threshold)

Litigation and Dispute Assessment

-

Obtain a list of all show cause notices and their status

-

Review assessment orders and demands raised

-

Analyse pending appeals and their financial exposure. If appeal needs to be filed before GSTAT then check the date to file it.

-

Check the status of refund claims and delays

-

Assess anti-profiteering complaints or investigations

-

Review any special audits or investigations initiated

-

Identify pre-GST legacy disputes affecting GST positions

Financial and Accounting Review

-

Reconcile GST liability as per books vs. GST portal

-

Analyse GST expense trends and unusual spikes

-

Review provisioning policy for GST contingencies

-

Check GST balance sheet treatment (advances, provisions)

-

Validate revenue recognition practices for GST timing

-

Assess the impact of GST on revenue and margin trends

Post-Transaction Integration

Immediate Actions (Day 1-30)

-

Notify GST authorities of ownership change

-

Ensure continuity of all GST registrations

-

Establish interim compliance responsibility matrix

-

Complete all pending filing obligations

-

Conduct first reconciliation post-acquisition

-

Set up emergency compliance protocols

Integration Phase (Month 1-6)

-

Decide on GSTIN consolidation strategy

-

Harmonise the chart of accounts and GST accounting

-

Integrate/interface technology systems

-

Standardise invoice formats and documentation

-

Unify vendor and customer master data

-

Implement consolidated reconciliation process

-

Train the combined finance team on harmonised procedures

Optimisation Phase (Month 6-12)

-

Review supply chain for GST efficiency opportunities

-

Optimise ITC utilisation across the merged entity

-

Implement advanced compliance analytics

-

Conduct post-merger GST health check

-

Document lessons learned and refine playbook

GST Risk Assessment Framework

Risk Rating Matrix

| Risk Category | High Risk | Medium Risk | Low Risk |

| Filing Compliance | >5% returns delayed or pending | 2-5% returns delayed | <2% returns delayed |

| ITC Matching | <70% GSTR-2A/2B matched | 70-85% matched | >85% matched |

| Litigation Exposure | Exposure >5% of deal value | Exposure 2-5% of value | Exposure <2% of value |

| Audit History | Multiple demands, adverse findings | 1-2 minor observations | Clean audit history |

| Classification Issues | Systemic misclassification | Isolated classification queries | Consistent correct classification |

Valuation Adjustment Guidelines

High Risk Profile

-

Working capital adjustment: 20-30% haircut on ITC

-

EBITDA normalisation: Full provision for probable exposures

-

Risk premium: +2-3% to discount rate

-

Indemnity: 10-15% of purchase price in escrow

Medium Risk Profile

-

Working capital adjustment: 10-20% haircut on ITC

-

EBITDA normalisation: 50% provision for identified issues

-

Risk premium: +1-2% to discount rate

-

Indemnity: 5-10% of purchase price in escrow

Low Risk Profile

-

Working capital adjustment: 0-10% haircut on ITC

-

EBITDA normalisation: Specific provision for known items only

-

Risk premium: Minimal or no adjustment

-

Indemnity: Standard warranties with basket and cap

Integration Success Factors

Critical Success Factors for GST Integration

-

Executive Sponsorship: Active CFO involvement in GST integration decisions ensures alignment with broader financial strategy and resource allocation.

-

Early Planning: GST integration planning should commence during the due diligence phase, not post-closing. Early identification of integration challenges allows for structure optimisation.

-

Dedicated Resources: Assignment of dedicated tax and compliance professionals to lead integration, rather than treating it as an add-on to existing responsibilities.

-

Technology Investment: Adequate investment in compliance technology prevents manual errors and scales with organisational complexity post-merger.

-

Change Management: Systematic change management addressing people, process, and technology dimensions ensures smooth transition and minimises disruption.

Common Pitfalls to Avoid

Underestimating Complexity Many acquirers treat GST as a routine compliance matter, failing to recognise its systemic nature. GST touches every transaction, requiring changes across procurement, sales, finance, IT, and operations.

Delayed Integration Postponing GST integration decisions creates compliance gaps, ITC leakage, and compounds reconciliation challenges. Immediate action on critical compliance matters is essential.

Inadequate Documentation Failure to preserve target company's GST documentation, particularly ITC supporting documents, can result in permanent loss of tax benefits and audit vulnerabilities.

System Integration Shortcuts Attempting manual workarounds instead of proper system integration creates ongoing compliance risks and prevents the realisation of efficiency synergies.

Insufficient Testing Inadequate testing of integrated systems before go-live results in invoice errors, filing failures, and customer disruption.

Conclusion: A Strategic Imperative

GST considerations in M&A transactions have evolved from compliance checkboxes to strategic value drivers. For CEOs, CFOs, and Finance Directors, three imperatives emerge:

1. Elevate GST in Deal Strategy GST due diligence should commence early in the transaction lifecycle, informing valuation, structure, and negotiation strategy. What appears as a 10% contingency in due diligence can become a 25% value erosion if mismanaged post-acquisition.

2. Build Robust Integration Capability. Organisations executing multiple acquisitions should develop GST integration playbooks, standardised toolkits, and dedicated expertise. The learning curve from first acquisition to mature capability significantly impacts deal success rates.

3. Focus on Value Realisation Beyond risk mitigation, GST integration presents opportunities for supply chain optimisation, working capital efficiency, and tax structure improvements. Proactive planning can unlock 2-5% value creation through GST efficiency alone.

The complexity of GST in M&A transactions demands that finance leadership treat it not as a technical compliance exercise, but as a strategic component of deal success. Organisations that master GST due diligence and integration convert a potential risk into a competitive advantage in the M&A marketplace.

Recommended Actions for Finance Leaders

For Immediate Implementation:

-

Develop Deal Playbook: Create standardised GST due diligence checklists and integration frameworks customised to your industry and acquisition strategy.

-

Build Internal Capability: Train M&A team members on GST implications and establish partnerships with specialised tax advisors for complex transactions.

-

Implement Technology: Invest in compliance technology that can scale with acquisitions and provide real-time visibility across multiple entities.

-

Conduct Portfolio Review: For recent acquisitions, perform post-integration GST health checks to identify and remediate vulnerabilities before they crystallise.

-

Document Lessons Learned: Systematically capture insights from each transaction to refine the approach and avoid repeated mistakes.

The M&A landscape continues to evolve, and GST complexity shows no signs of diminishing. Finance leaders who proactively address these challenges will protect deal value, ensure smooth integrations, and position their organisations for sustainable growth through acquisitions.

How to Find GST Number of a Company by Name | Search Company by CIN | Revenue Neutral Rate | Commission HSN Code | legal Name of Business

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified