GST HSN Classification Guide: Technical Framework for Finance Leaders

GST Classification Framework:

A Technical Guide for Finance Leadership

Executive Summary

The accurate determination of Harmonised System of Nomenclature (HSN) classification constitutes a fundamental pillar of Goods and Services Tax (GST) compliance architecture. For finance leadership, the strategic implementation of precise commodity classification protocols directly impacts fiscal liability, regulatory adherence, and operational continuity under the GST regime.

Regulatory Imperatives of HSN Classification

Fiscal Impact Assessment

The HSN classification framework serves as the determinative mechanism for tax rate applicability across the tiered GST structure. The classification decision triggers specific tax implications:

Rate Determination Matrix:

-

Standard Rate (18%): Applied to majority of goods under general provisions

-

Concessional Rates (5% & 12%): Applicable to essential commodities and specified goods

-

Peak Rate (28%): Imposed on luxury and demerit goods with additional cess provisions

Compliance Architecture

Accurate classification ensures adherence to the constitutional and statutory provisions under:

-

Central Goods and Services Tax Act, 2017

-

Integrated Goods and Services Tax Act, 2017

-

State Goods and Services Tax Acts (respective state legislations)

Risk Mitigation Framework

Misclassification triggers cascading compliance failures including:

-

Differential Tax Liability: Demand notices under Section 73/74 of CGST Act

-

Interest Computations: Compounded at 18% per annum on unpaid tax

-

Penalty Impositions: Up to 100% of differential tax under Section 122

-

Criminal Liability: Under Section 132 for willful evasion exceeding specified thresholds

Systematic Classification Methodology

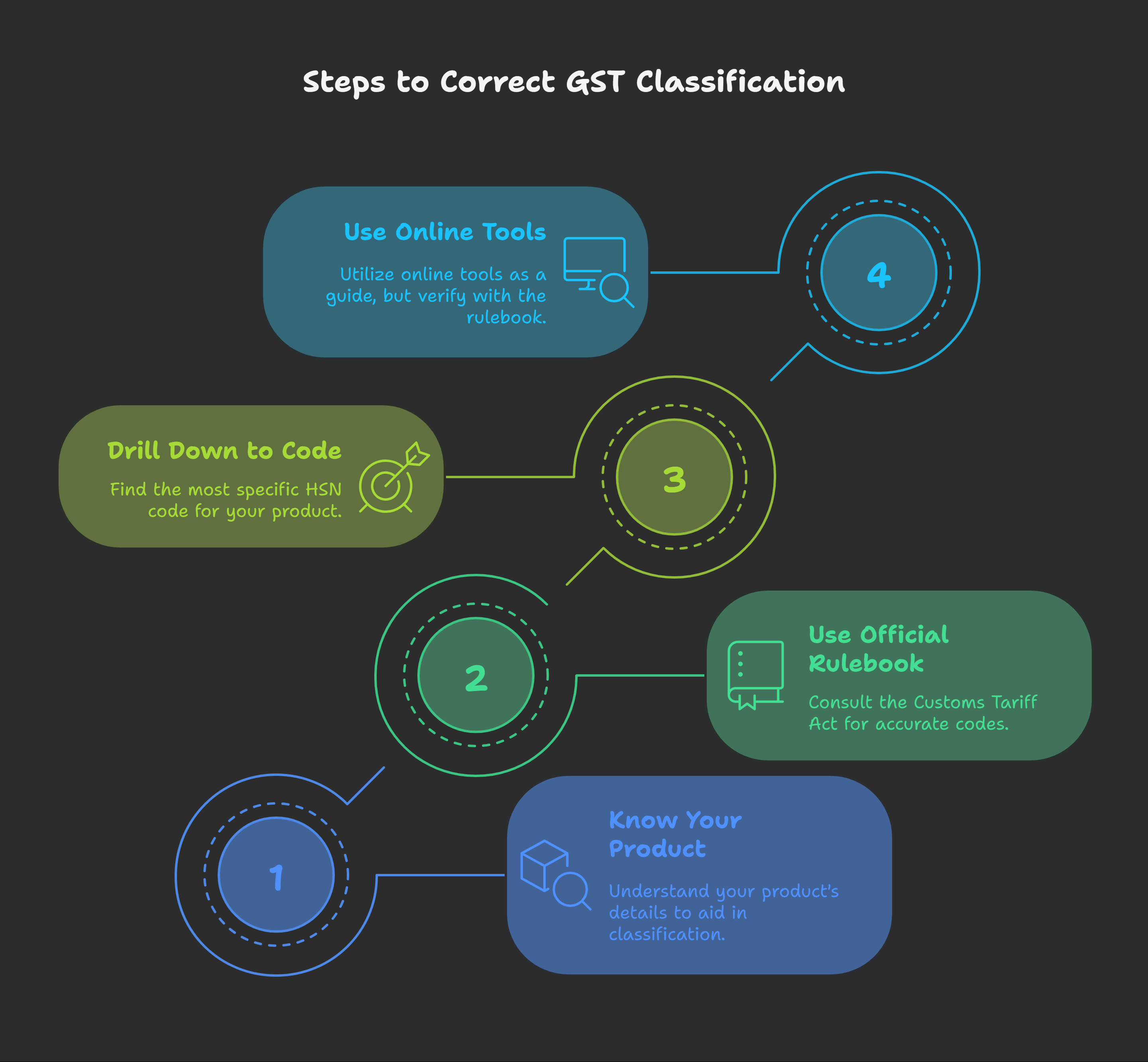

Phase I: Product Characterisation and Technical Analysis

Finance leadership must establish comprehensive product dossiers encompassing:

Technical Specifications:

-

Raw material composition and manufacturing processes

-

Functional characteristics and intended commercial use

-

Packaging methodologies and presentation standards

-

Quality parameters and technical standards compliance

Commercial Context:

-

Market positioning and consumer perception

-

Distribution channels and sales methodologies

-

Value addition processes and manufacturing stages

Phase II: Statutory Framework Navigation

Primary Legal Reference: Customs Tariff Act, 1975

The classification exercise must commence with systematic analysis of the Customs Tariff Act, 1975, which forms the foundational legal framework for HSN implementation in India.

Interpretative Hierarchy:

-

Section Notes: Chapter-specific interpretative provisions with legal precedence

-

General Interpretative Rules (GIR): Six fundamental classification principles

-

Explanatory Notes: Harmonized System Committee interpretations

-

Judicial Precedents: Supreme Court and High Court pronouncements

Phase III: Hierarchical Code Determination

Chapter Identification (2-digit classification): Initial broad categorization based on product nature and commercial characteristics.

Heading Specification (4-digit classification): Sub-classification within chapters based on specific product attributes and functional applications.

Sub-heading Precision (6-digit classification): Mandatory for entities exceeding Rs. 5 crore annual aggregate turnover, requiring granular product differentiation.

Tariff Item Designation (8-digit classification): Optional detailed classification for enhanced specificity and administrative convenience.

Phase IV: Technology-Assisted Verification

GST Portal HSN Search Tool: Utilize the official government portal (www.gst.gov.in) for preliminary reference, subject to independent verification against statutory provisions.

Caution Advisory: Portal-generated classifications require validation against primary legal sources and should not constitute sole reliance for compliance purposes.

Strategic Risk Management Protocols

Common Compliance Pitfalls

Supplier Classification Reliance: Finance departments must maintain independent classification protocols rather than adopting supplier-declared HSN codes, as ultimate compliance responsibility rests with the selling entity.

Generic Code Application: Utilization of broad or non-specific HSN codes constitutes prima facie evidence of non-compliance and attracts scrutiny under risk-based assessment frameworks.

Inadequate Documentation: Absence of classification rationale documentation impedes defense during audit proceedings and assessment challenges.

Professional Consultation Framework

Complex Product Classifications: Engage specialized GST counsel for products involving:

-

Multi-component assemblies with diverse HSN applications

-

Emerging technologies without established classification precedents

-

Cross-border transaction implications requiring international treaty considerations

Advance Ruling Mechanism: For significant volume transactions or novel products, consider obtaining Advance Rulings under Chapter XX of respective GST Acts to establish binding classification positions.

Operational Implementation Guidelines

Internal Control Systems

Classification Committees: Establish cross-functional teams comprising finance, legal, and technical personnel for classification decisions.

Documentation Protocols: Maintain comprehensive classification files including technical specifications, legal analysis, and decision rationale for audit defence.

Periodic Review Mechanisms: Institute quarterly classification reviews to address product modifications, regulatory changes, and emerging jurisprudential developments.

Technology Integration

ERP Integration: Embed HSN classification controls within enterprise resource planning systems to ensure systematic compliance across transaction volumes.

Automated Validation: Implement system-level checks to prevent invoice generation without appropriate HSN code specification and rate application.

Conclusion

The HSN classification framework represents a critical intersection of tax policy, legal compliance, and operational efficiency. Finance leadership must approach classification as a strategic compliance function requiring systematic methodology, technical expertise, and continuous monitoring. The investment in robust classification protocols yields dividends through reduced audit risks, optimised tax positions, and enhanced regulatory standing.

Disclaimer: This technical guidance serves as a framework for finance leadership and does not constitute specific legal advice. Organisations should engage qualified GST professionals for transaction-specific classification matters

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified