This document presents a detailed mind map of the GSTR-1 tables, providing an in-depth analysis of each table’s purpose, contents, and key notes. GSTR-1 is a return filed by regular taxpayers in India to report their outward supplies, consisting of various tables that capture different types of transactions. The mind map is structured with the central topic “GSTR-1 Tables” and branches out to individual tables, each with sub-branches detailing their specifics.

GSTR-1 Tables Mind Map

Central Topic: GSTR-1 Tables

GSTR-1 is a monthly or quarterly return that includes details of sales, exports, and other outward supplies made by a taxpayer. The tables within GSTR-1 serve distinct purposes, ensuring comprehensive reporting for GST compliance. Below are the branches representing each table, along with in-depth analysis.

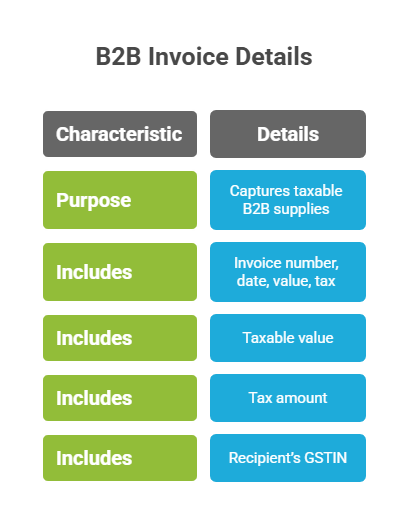

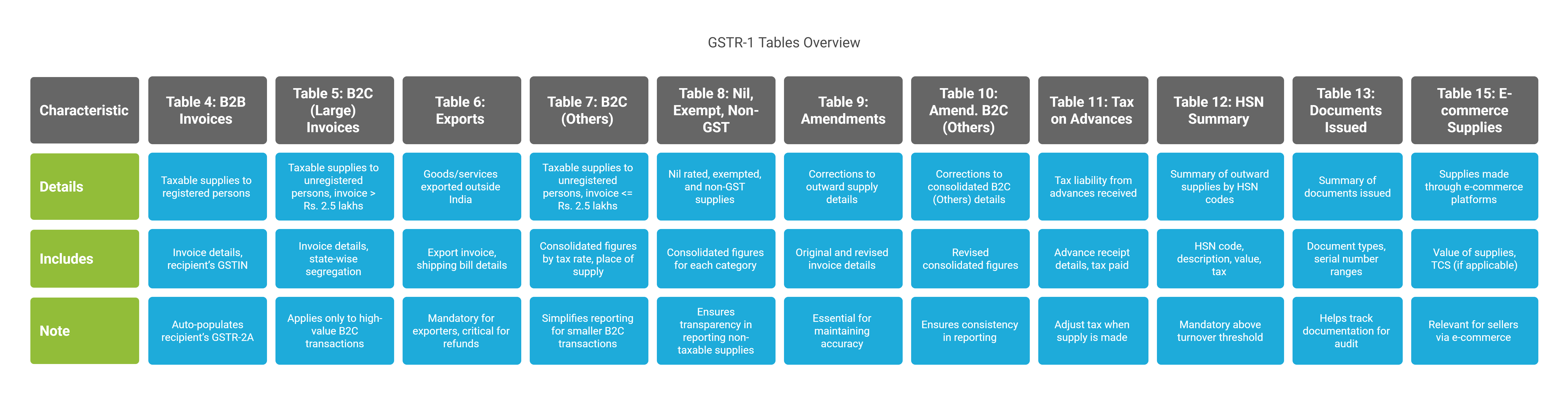

#### Branch 1: Table 4 - B2B Invoices

- Details: Captures taxable supplies made to registered persons (Business-to-Business transactions).

- Includes:

- Invoice number

- Invoice date

- Invoice value

- Taxable value

- Tax amount

- Recipient’s GSTIN

- Note:

- Auto-populated in the recipient’s GSTR-2A, enabling them to claim input tax credit.

- Mandatory for taxpayers with B2B transactions.

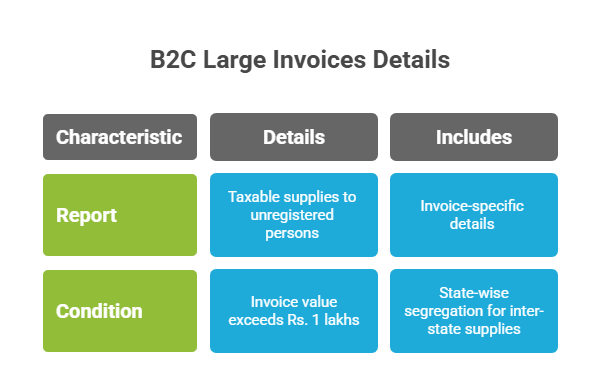

#### Branch 2: Table 5 - B2C (Large) Invoices

- Details: Reports taxable supplies to unregistered persons (Business-to-Consumer) where the invoice value exceeds Rs. 2.5 lakhs.

- Includes:

- Invoice-specific details such as number, date, value, and tax amount.

- State-wise segregation for inter-state supplies.

- Note:

- Applies only to high-value B2C transactions, distinguishing them from smaller transactions reported elsewhere.

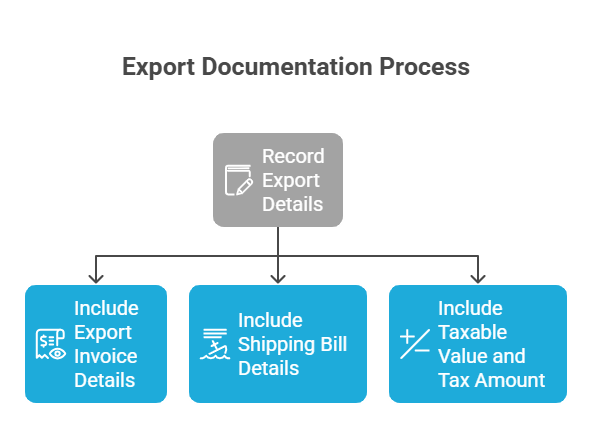

#### Branch 3: Table 6 - Exports

- Details: Records details of goods or services exported outside India.

- Includes:

- Export invoice details (number, date, value).

- Shipping bill or bill of export details.

- Taxable value and tax amount (if applicable, e.g., under bond/LUT or with tax payment).

- Note:

- Mandatory only for taxpayers engaged in export activities.

- Critical for claiming export-related refunds.

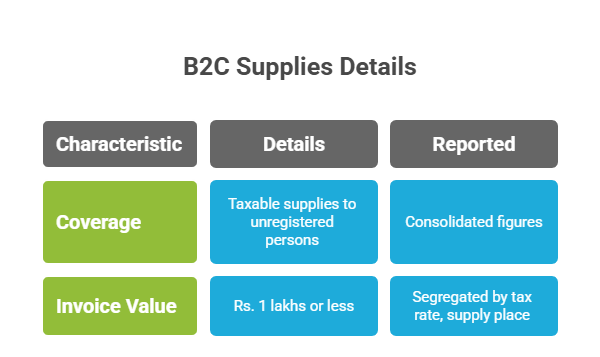

#### Branch 4: Table 7 - B2C (Others)

- Details: Covers taxable supplies to unregistered persons where the invoice value is Rs.2.5 lakhs or less.

- Reported:

- Consolidated figures (not invoice-wise).

- Segregated by rate of tax and place of supply.

- Note:

- Simplifies reporting for smaller B2C transactions by avoiding invoice-level details.

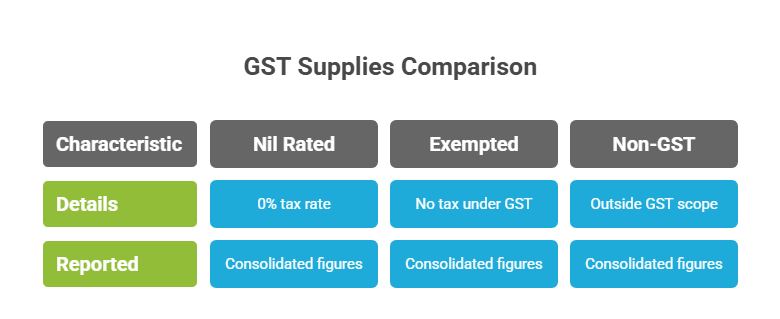

#### Branch 5: Table 8 - Nil Rated, Exempted, and Non-GST Supplies

- Details: Summarizes supplies that are:

- Nil rated (0% tax).

- Exempted (no tax under GST law).

- Non-GST (outside GST scope, e.g., alcohol, petroleum).

- Reported:

- Consolidated figures for each category.

- Note:

- Ensures transparency in reporting non-taxable supplies.

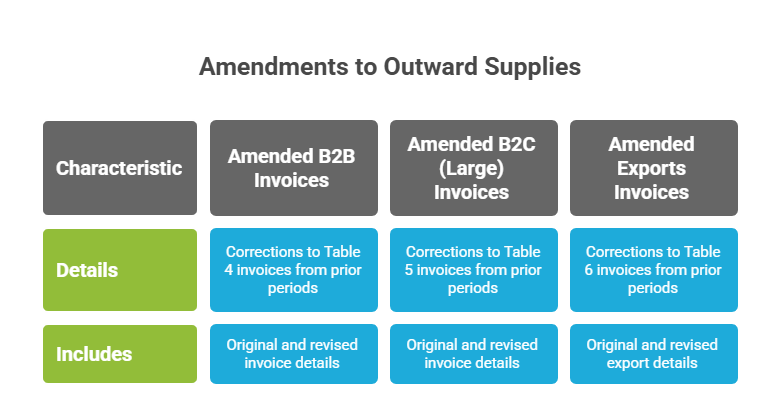

#### Branch 6: Table 9 - Amendments to Outward Supplies

- Details: Facilitates corrections to outward supply details reported in earlier tax periods.

- Table 9A - Amended B2B Invoices

- Details: Corrections to B2B invoices (Table 4) from prior periods.

- Includes: Original and revised invoice details.

- Table 9B - Amended B2C (Large) Invoices

- Details: Corrections to B2C (Large) invoices (Table 5) from prior periods.

- Includes: Original and revised invoice details.

- Table 9C - Amended Exports Invoices

- Details: Corrections to export invoices (Table 6) from prior periods.

- Includes: Original and revised export details.

- Table 9A - Amended B2B Invoices

- Note:

- Essential for maintaining accuracy in previously filed returns.

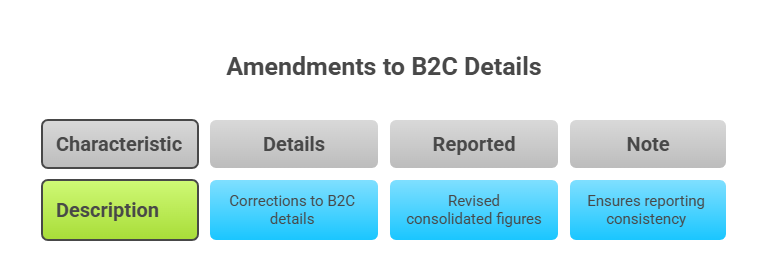

#### Branch 7: Table 10 - Amendments to B2C (Others)

- Details: Corrections to consolidated B2C (Others) details (Table 7) from earlier tax periods.

- Reported:

- Revised consolidated figures.

- Note:

- Ensures consistency in reporting smaller B2C transactions over time.

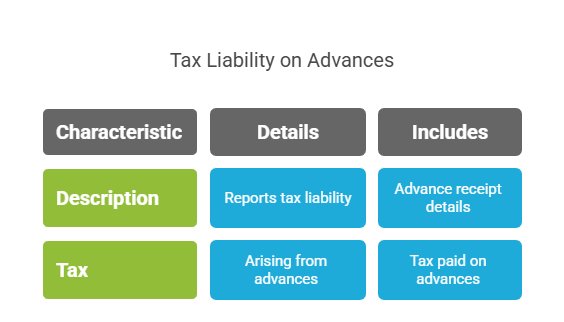

#### Branch 8: Table 11 - Tax Liability on Advances

- Details: Reports tax liability arising from advances received for future supplies.

- Includes:

- Advance receipt details (date, amount).

- Tax paid on such advances.

- Note:

- Taxpayers adjust this tax when the supply is made and invoiced later.

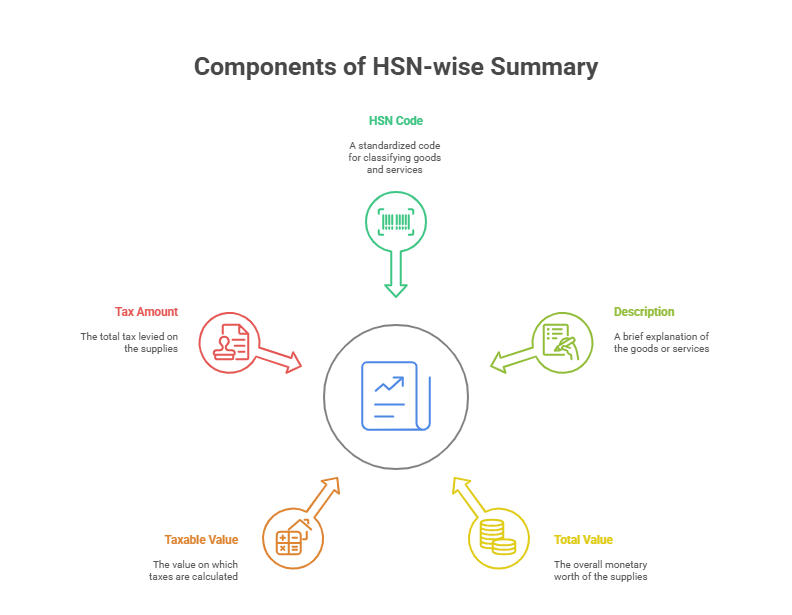

#### Branch 9: Table 12 - HSN-wise Summary

- Details: Provides a summary of outward supplies based on Harmonized System of Nomenclature (HSN) codes.

- Includes:

- HSN code.

- Description of goods/services.

- Total value, taxable value, and tax amount.

- Note:

- Mandatory for taxpayers with turnover above a certain threshold (e.g., 4-digit HSN for turnover > Rs. 5 crore).

- Enhances tax administration by categorizing supplies.

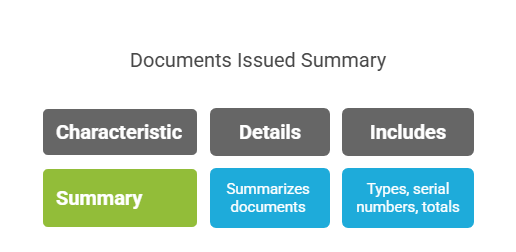

#### Branch 10: Table 13 - Documents Issued

- Details: Summarizes documents issued during the tax period.

- Includes:

- Types of documents (invoices, credit notes, debit notes).

- Serial number ranges.

- Total issued, cancelled, and net issued documents.

- Note:

- Helps track documentation for audit and compliance purposes.

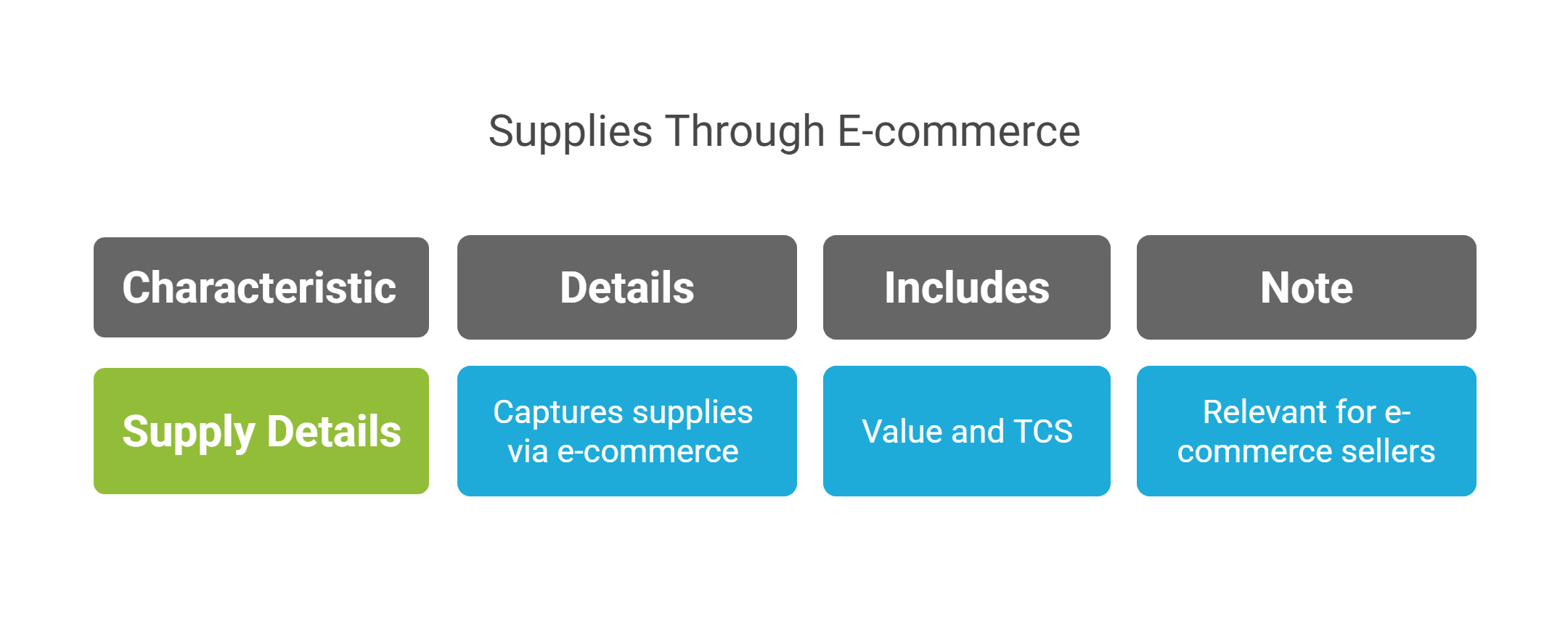

#### Branch 11: Table 15 - Supplies through E-commerce Operators

- •Includes:

- Value of supplies.

- Tax collected at source (TCS) by the e-commerce operator, if applicable.

- Note:

- Relevant only for taxpayers selling through e-commerce operators.

- Ensures proper reporting of online transactions.

Summary and Usage

This mind map outlines the key tables in GSTR-1, each serving a specific role in reporting outward supplies under India’s GST regime. Here’s how it can be visualized:

- Central Node: “GSTR-1 Tables” at the center.

- Radiating Branches: Each table (e.g., Table 4, Table 5) extends outward.

- Sub-branches: Details, included data, and notes extend from each table branch.

Key Insights

- Outward Supplies: Tables 4, 5, 6, 7, and 8 cover the core reporting of sales and exports.

- Amendments: Tables 9 and 10 ensure corrections are tracked systematically.

- Additional Details: Tables 11, 12, 13, and 15 address advances, summaries, documentation, and e-commerce specifics.

- Compliance: Accurate and complete filing of these tables is critical, as GSTR-1 data auto-populates GSTR-3B (summary return) and affects recipients’ input tax credit eligibility.

This structured mind map provides a comprehensive guide to understanding and utilizing the GSTR-1 tables effectively, catering to taxpayers and tax professionals alike.

GSTR-1 Tables Overview

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified