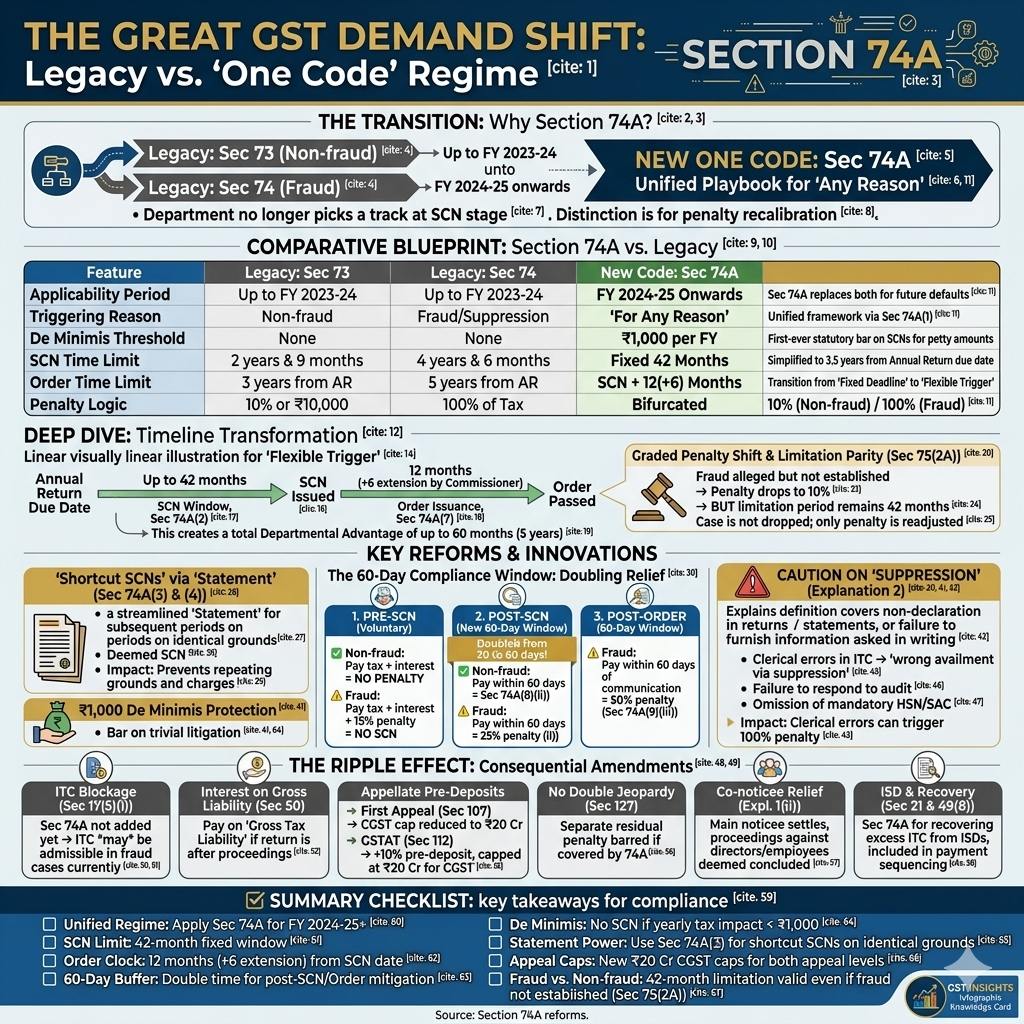

Why was Section 74A introduced?

The Finance Act (No. 2), 2024, has fundamentally restructured the GST demand and recovery landscape by introducing Section 74A. Historically, the Adjudicating Authority operated under a "dual-track" system governed by Section 73 vs Section 74 under GST, where Section 73 dealt with bona fide cases and Section 74 applied to cases involving fraud, willful misstatement, or suppression.

Effective for Financial Year (FY) 2024-25 onwards, this distinction is consolidated into a unified "One Code." While Sections 73 and 74 remain "frozen in time" to resolve legacy disputes up to FY 2023-24, Section 74A serves as the new playbook for all future determinations. For students, the "So What?" is clear: the department no longer needs to justify which track to pick at the SCN stage; instead, the bifurcation between fraud and non-fraud now exists primarily for penalty recalibration within the same section.

Section 73 and 74 vs Section 74A: Key differences

The following blueprint summarises the transition to the unified framework under Section 74A.

| Feature | Legacy: Sec 73 | Legacy: Sec 74 | New Code: Sec 74 A | Remarks/Impact |

| Applicability Period | Up to FY 2023-24 |

Up to FY 2023-24 |

FY 2024-25 Onwards |

Sec 74A replaces both for future defaults. |

| Triggering Reason | Non-fraud |

Fraud/Suppression |

"For Any Reason" |

Unified framework via Sec 74A(1). |

| De Minimis Threshold | None |

None |

₹1,000 per FY |

First-ever statutory bar on SCNs for petty amounts. |

| SCN Time Limit | 2 years & 9 months |

4 years & 6 months |

Fixed 42 Months |

Simplified to 3.5 years from Annual Return due date. |

| Order Time Limit | 3 years from AR |

5 years from AR |

SCN + 12(+6) Months |

Transition from "Fixed Deadline" to "Flexible Trigger." |

| Penalty Logic | 10% or ₹10,000 |

100% of Tax |

Bifurcated |

10% (Non-fraud) / 100% (Fraud). |

How timelines have changed under Section 74A

A critical area for CA final exams is the shift from a deadline tied to the Annual Return to one triggered by the service of the Show Cause Notice (SCN).

Understanding the new SCN and order timelines

Under the old regime, the limitation period for the final Order was a fixed date. Under Section 74A, the clock for the Adjudicating Authority starts ticking only after the SCN is issued.

-

SCN Window (Sec 74A(2)): A uniform 42-month limit from the Annual Return due date applies to all cases.

-

Order Issuance (Sec 74A(7)): The order must be passed within 12 months from the SCN date, extendable by 6 months by the Commissioner.

-

Departmental Advantage: This creates a total window of up to 60 months (5 years):

What happens if fraud is not established?

A vital procedural nuance arises if the department alleges fraud but fails to establish it before an Appellate Authority or Court, highlighting the importance of understanding GST appeals and revisions under Sections 107–121. Under the new regime:

-

Penalty Recalibration: The penalty drops from 100% to 10% (as per Sec 74A(5)(i)).

-

Limitation Parity: Unlike the legacy regime, where the entire proceeding might have been time-barred if moved from Section 74 to 73, under Section 74A, the limitation period remains 42 months. The case is not "dropped" for being out of time; only the penalty quantum is readjusted.

When can the department issue a statement instead of an SCN?

Under Section 74A(3) and (4), the department is empowered to issue a "Statement" instead of a full SCN for subsequent periods if the grounds are identical to an earlier SCN, further expanding the scope of GST notices and departmental communications that taxpayers must carefully evaluate.

-

Deemed SCN: This statement carries the same legal weight as a notice issued under sub-section (1).

-

Efficiency: This prevents the repetition of grounds and charges, streamlining the adjudication of recurring issues.

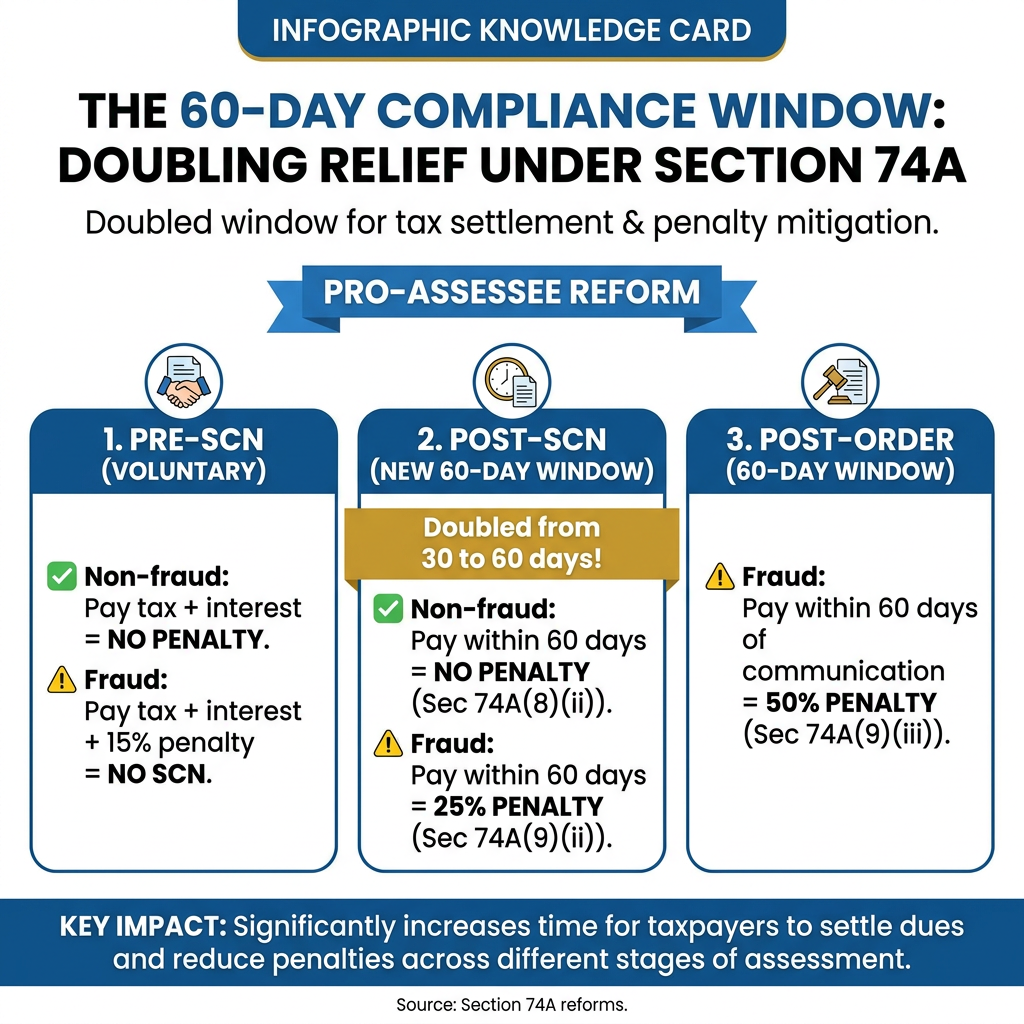

Penalty relief and the new 60-day compliance window

In a significant pro-assessee reform, Section 74A doubles the window for taxpayers to settle dues and receive penalty mitigation.

-

Pre-SCN (Voluntary):

-

Non-fraud: Pay tax + interest = No Penalty.

-

Fraud: Pay tax + interest + 15% penalty = No SCN.

-

-

Post-SCN (60-Day Window):

-

Non-fraud: Pay within 60 days (up from 30) = No Penalty (Sec 74A(8)(ii)).

-

Fraud: Pay within 60 days = 25% penalty (Sec 74A(9)(ii)).

-

-

Post-Order (60-Day Window):

-

Fraud: Pay within 60 days of communication = 50% penalty (Sec 74A(9)(iii)).

-

Threshold limits and the meaning of suppression under Section 74A

While the ₹1,000 De Minimis Protection is a welcome bar on trivial litigation, the re-insertion of Explanation 2 (Suppression) in Section 74A is a point of professional skepticism.

Caution on Suppression: Section 74A(5)(ii) retains a broad definition of suppression, covering non-declaration of facts in returns/statements or failure to furnish information when asked in writing, making a proactive GST litigation, audit, and appeal strategy increasingly important for businesses. This creates a risk where clerical errors or passive omissions are categorized as "suppression" to trigger the 100% penalty.

Practical situations that may trigger suppression allegations:

-

Clerical errors in ITC: Can be treated as "wrong availment via suppression."

-

Failure to respond to audit: Technically meets the definition of suppression.

-

Omission of HSN/SAC: If mandatory, could be viewed as non-declaration of facts.

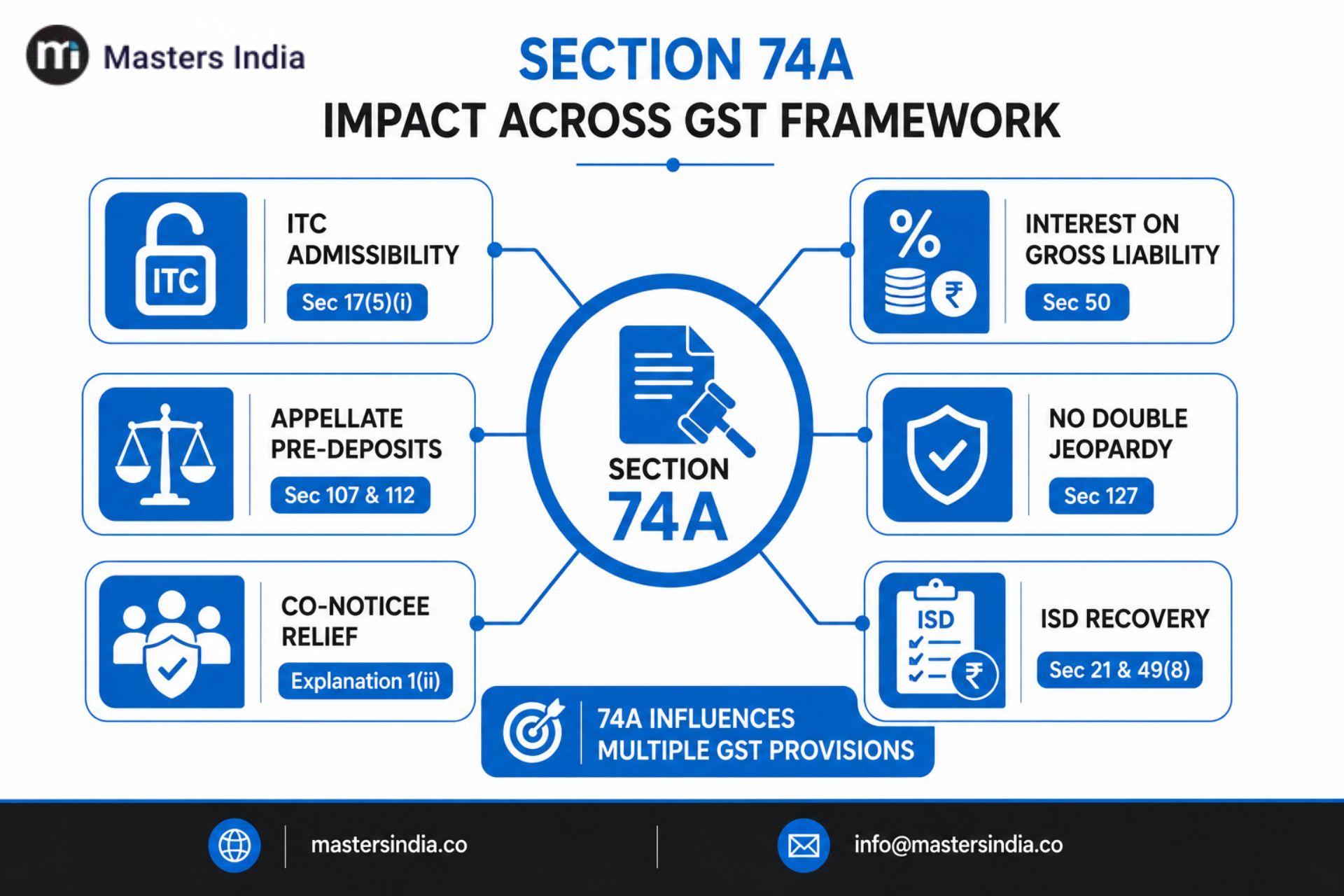

Other GST provisions impacted by Section 74A

Section 74A triggers changes across the GST framework that students must track for comprehensive compliance:

-

The ITC "Loophole" (Sec 17(5)(i)): Currently, ITC blockage is explicitly linked to tax paid under Section 74 for periods up to FY 23-24. Since Section 74A has not yet been added to the blocking list, tax paid even in fraud cases under 74A may currently be admissible for ITC.

-

Interest on Gross Liability (Sec 50): Interest under Section 50(1) is payable on the "Gross Tax Liability" (not just the cash portion) if the return is furnished after the commencement of proceedings under Section 74A.

-

Appellate Pre-Deposits:

-

First Appeal (Sec 107): The CGST cap is reduced to ₹20 Cr.

-

GSTAT (Sec 112): Requires an additional 10% pre-deposit, now also capped at ₹20 Cr for CGST.

-

-

No Double Jeopardy (Sec 127): Section 127 now clarifies that if a penalty is already covered under Section 74A, separate residual penalty proceedings cannot be initiated.

-

Co-noticee Relief: Per Explanation 1(ii), if the main noticee (e.g., the Company) settles the case under Section 74A, proceedings against directors or employees are deemed concluded.

-

ISD and Recovery (Sec 21 & 49(8)): Section 74A is now an established route for recovering excess ITC distributed by ISDs and is included in the mandatory payment sequencing order.

Summary checklist:

-

[ ] Unified Regime: Apply Section 74A for all defaults pertaining to FY 2024-25 onwards.

-

[ ] SCN Limit: 42-month fixed window from the Annual Return due date.

-

[ ] Order Clock: 12 months (+6 extension) triggered by the SCN date.

-

[ ] 60-Day Buffer: Double the time (60 vs 30 days) for penalty mitigation post-SCN/Order.

-

[ ] De Minimis: Ensure no SCN is issued if the yearly tax impact is < ₹1,000.

-

[ ] Statement Power: Use Section 74A(3) for shortcut SCNs on identical grounds.

-

[ ] Appeal Caps: Note the new ₹20 Cr CGST caps for both appeal levels.

-

[ ] Fraud vs. Non-fraud: Remember that even if fraud is not established, the 42-month limitation remains valid under Section 75(2A).

How will Section 74A reshape GST demand and recovery proceedings?

Section 74A marks a significant shift in the GST demand and recovery framework by replacing the separate Section 73 and Section 74 mechanisms for FY 2024-25 onwards. While the new regime simplifies procedures through a unified structure, businesses must continue to pay close attention to timelines, penalty provisions, suppression-related risks, and appeal requirements. Understanding these changes is essential for managing disputes effectively and minimizing compliance exposure.

Organizations that proactively review their GST processes, maintain accurate records, and respond promptly to notices often leverage GST software to strengthen compliance controls and adapt to evolving regulatory requirements.

Masters India helps businesses stay compliant through GST technology solutions, automated reconciliations, GST APIs, e-invoicing systems, and expert compliance support. Connect with our team to simplify GST management and stay ahead of regulatory changes.

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified