GST Compliance, Audits, and Litigation in India: A Strategic Playbook for Businesses

1.0 Introduction: The GST Paradigm in India

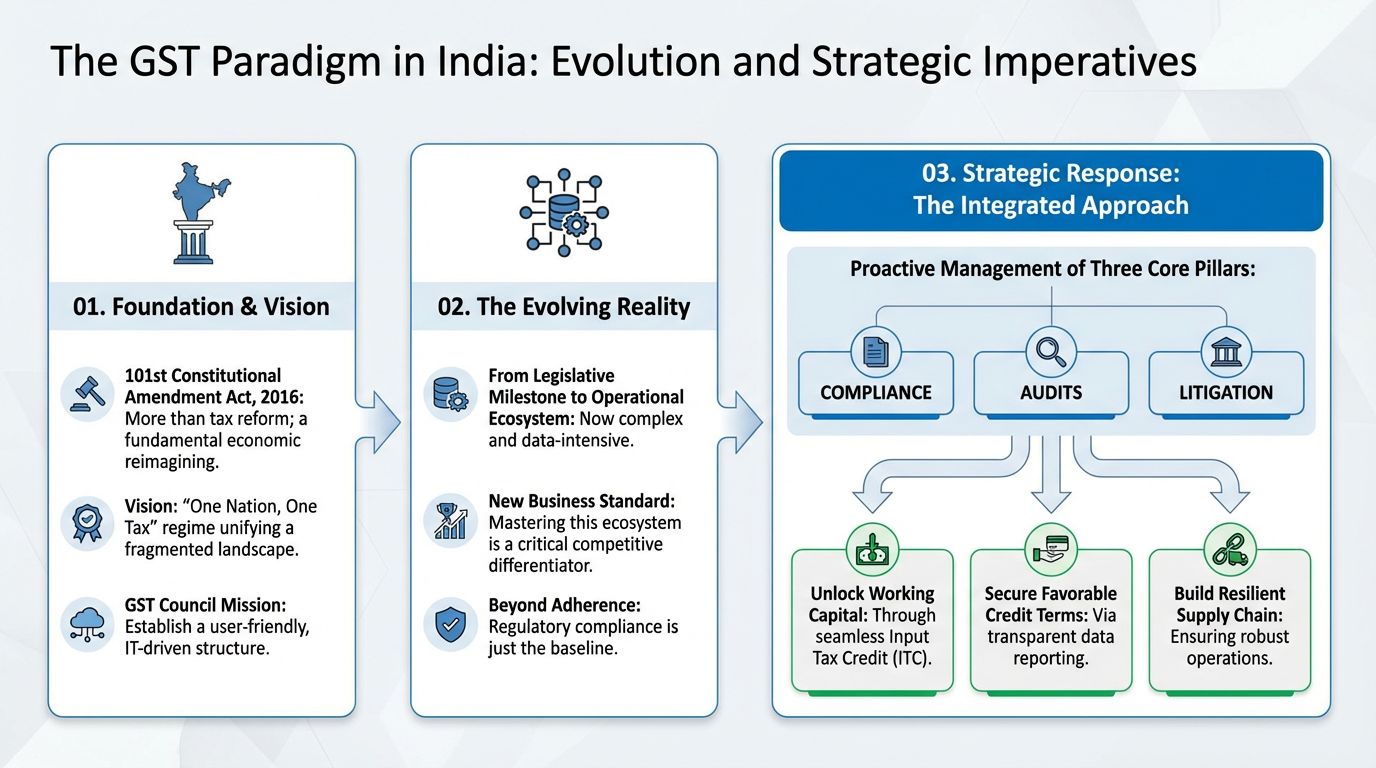

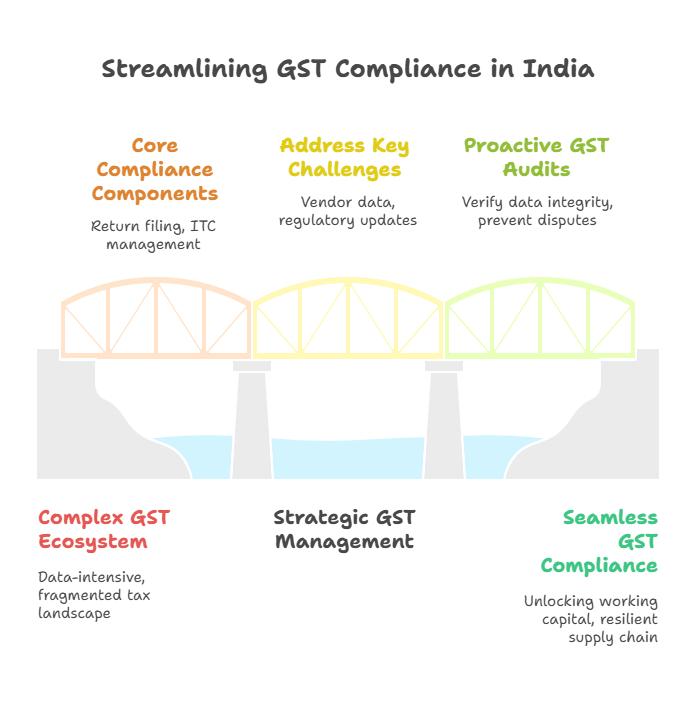

The introduction of the Goods and Services Tax (GST) through the 101st Constitutional Amendment Act of 2016 was not merely a tax reform; it was a fundamental reimagining of India’s economic architecture. Envisioned to unify a fragmented tax landscape into a singular "one nation, one tax" regime, GST has evolved from a legislative milestone into a complex, data-intensive operational ecosystem. For businesses, mastering this ecosystem is no longer just about regulatory adherence—it has become a critical competitive differentiator.

The GST Council’s mission to establish a user-friendly, IT-driven tax structure represents a clear vision. However, the practical reality demands that businesses adopt a strategic and integrated approach to three core pillars: compliance, audits, and litigation. Proactive management of these pillars is key to unlocking working capital through seamless Input Tax Credit, securing favorable credit terms via transparent data, and building a resilient supply chain.

This white paper deconstructs these pillars, offering a strategic guide for navigating the intricacies of the GST compliance framework and its subsequent stages of departmental scrutiny and legal dispute.

2.0 The Modern GST Compliance Framework: Beyond Simple Filing

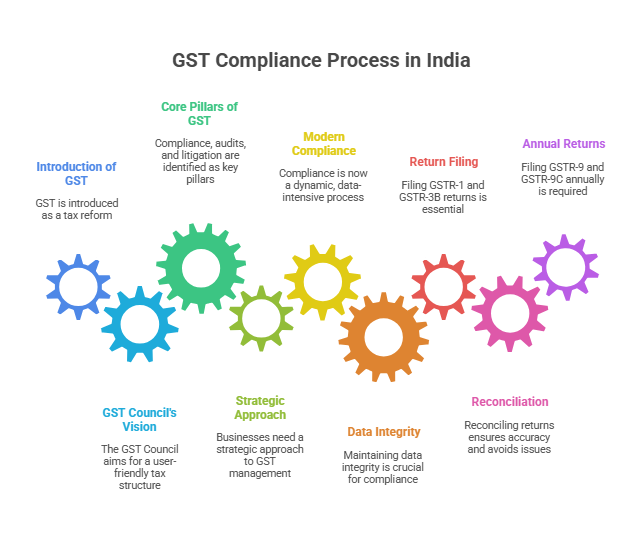

Modern GST compliance is a dynamic, data-intensive process that extends far beyond the mere filing of monthly returns. It is a strategic function where data integrity is paramount, requiring meticulous reconciliation and proactive vendor management. Mastering this framework is critical for safeguarding a business's most valuable GST asset—Input Tax Credit (ITC)—and maintaining healthy operational cash flow.

2.1 Core Compliance Components

The GST ecosystem is built on several interconnected digital components, each generating data that must be flawlessly consistent and accurate to uphold data integrity.

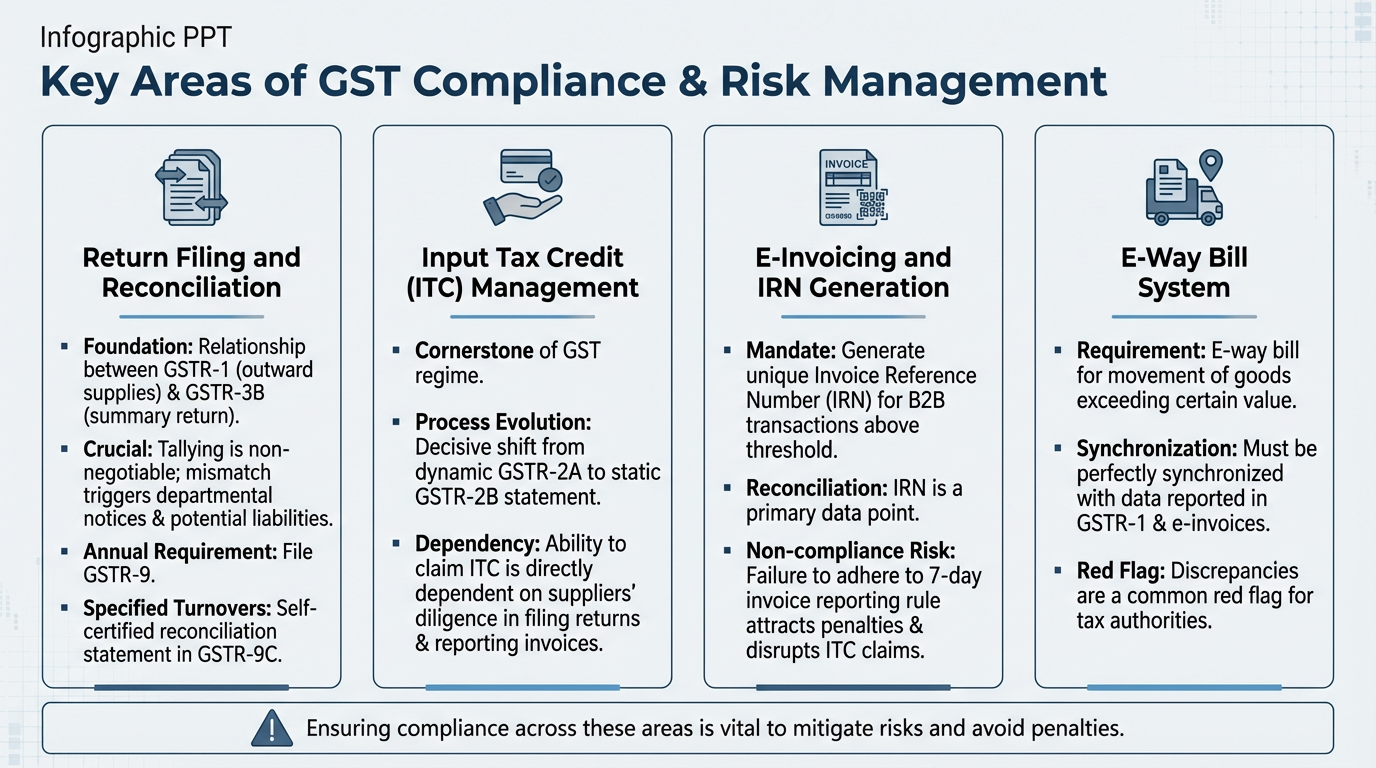

• Return Filing and Reconciliation: The foundation of GST compliance is the relationship between GSTR-1 (details of outward supplies) and GSTR-3B (a summary return). Ensuring these returns tally is non-negotiable, as any mismatch can trigger departmental notices and potential liabilities. Annually, businesses must file GSTR-9 and, for specified turnovers, a self-certified reconciliation statement in GSTR-9C.

• Input Tax Credit (ITC) Management: ITC is the cornerstone of the GST regime. The process for claiming it has evolved, with a decisive shift in reliance from the dynamic GSTR-2A to the static GSTR-2B statement. This change underscores that a business's ability to claim ITC is now directly dependent on its suppliers' diligence in filing their returns and reporting invoices correctly.

• E-Invoicing and IRN Generation: The e-invoicing system mandates the generation of a unique Invoice Reference Number (IRN) for B2B transactions above a specified threshold. The IRN has become a primary data point for reconciliation. Non-compliance, such as failing to adhere to the 7-day invoice reporting rule, can attract penalties and disrupt ITC claims for the recipient.

• E-Way Bill System: The e-way bill, required for the movement of goods exceeding a certain value, must be perfectly synchronised with the data reported in GSTR-1 and e-invoices. Discrepancies are a common red flag for tax authorities.

2.2 Key Compliance Challenges

Navigating the GST framework presents persistent challenges that demand both technological solutions and strategic foresight.

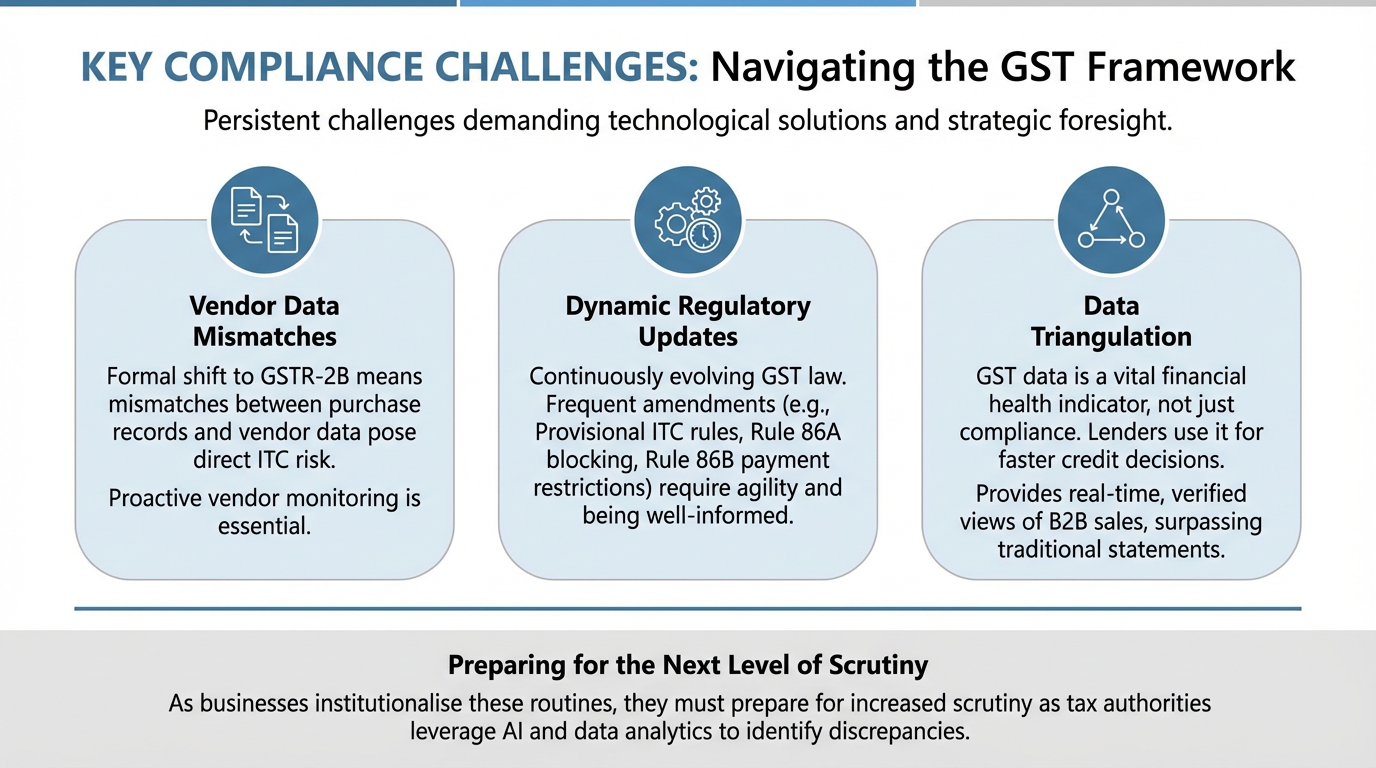

• Vendor Data Mismatches: With the formal shift to GSTR-2B, any mismatch between a business's purchase records and the data reported by its vendors poses a direct risk to ITC claims. Proactive vendor monitoring has become an essential business function.

• Dynamic Regulatory Updates: The GST law is continuously evolving. Frequent amendments, such as rules governing Provisional ITC, Rule 86A (blocking of the electronic credit ledger), and Rule 86B (restricting tax payment from the credit ledger), require businesses to be agile and well-informed.

• Data Triangulation: GST data is no longer a siloed compliance metric; it is a vital indicator of financial health. Lenders and credit agencies now perform triangulation of GST data with other financial data sets to make faster, more informed credit decisions. GST filings provide a real-time, government-verified view of a company's B2B sales, making them a more reliable barometer of business activity than traditional periodic financial statements.

As businesses institutionalise these complex compliance routines, they must also prepare for the next level of scrutiny they will inevitably face, as tax authorities increasingly leverage AI and data analytics to identify discrepancies.

3.0 Navigating GST Audits and Departmental Scrutiny

A GST audit should not be viewed as a punitive measure but as the ultimate test of a taxpayer's data integrity. It is a comprehensive review of compliance health, verifying the accuracy of declared turnover, taxes paid, refunds claimed, and ITC availed. A proactive and

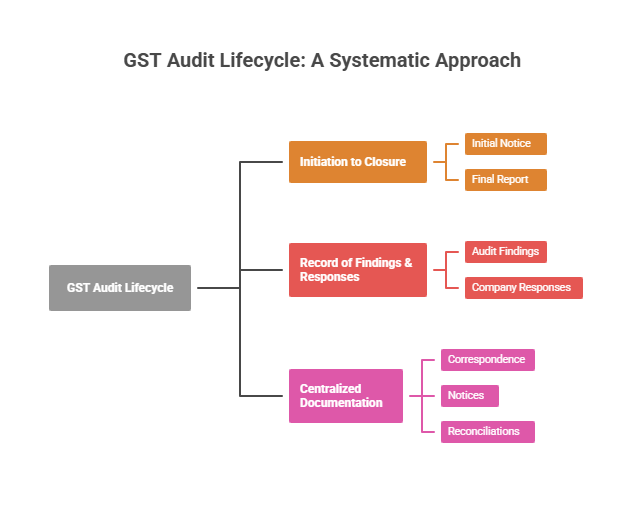

3.1 The GST Audit Lifecycle

Effective audit management demands a systematic approach that ensures transparency, organisation, and control.

1. Initiation to Closure: The entire audit process, from the initial notice to the final report, must be tracked with full visibility. This allows management to monitor progress, anticipate requirements, and ensure deadlines are met without fail.

2. Record of Findings & Responses: Every finding or query raised by the audit team must be meticulously recorded. Equally important is maintaining a structured log of all replies and submissions, creating a clear, chronological record that substantiates the company’s position.

3. Centralized Documentation: The ability to produce supporting documents on demand is critical. Storing all audit-related correspondence, notices, and reconciliations in a secure, centralized digital repository is a strategic advantage. This repository becomes the single source of truth that proves the integrity of the company’s data.

.

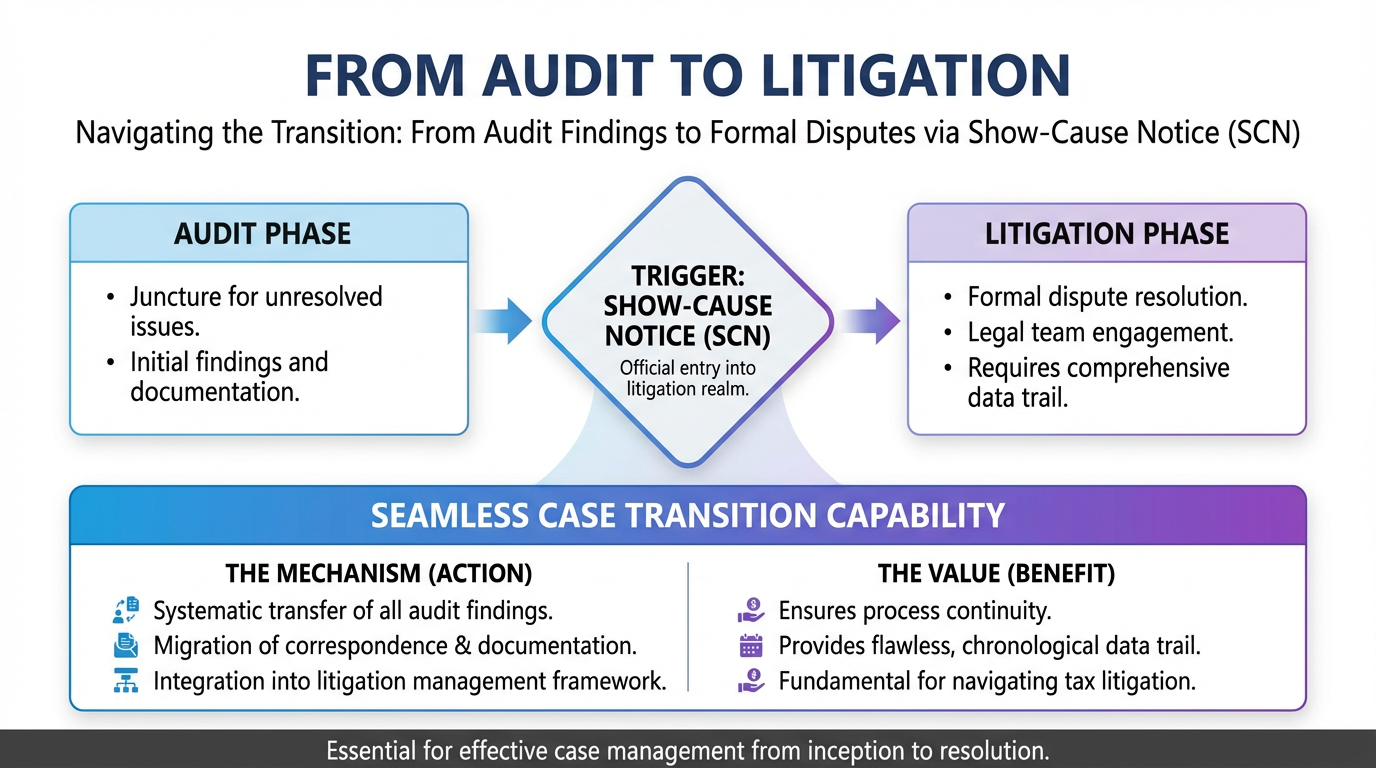

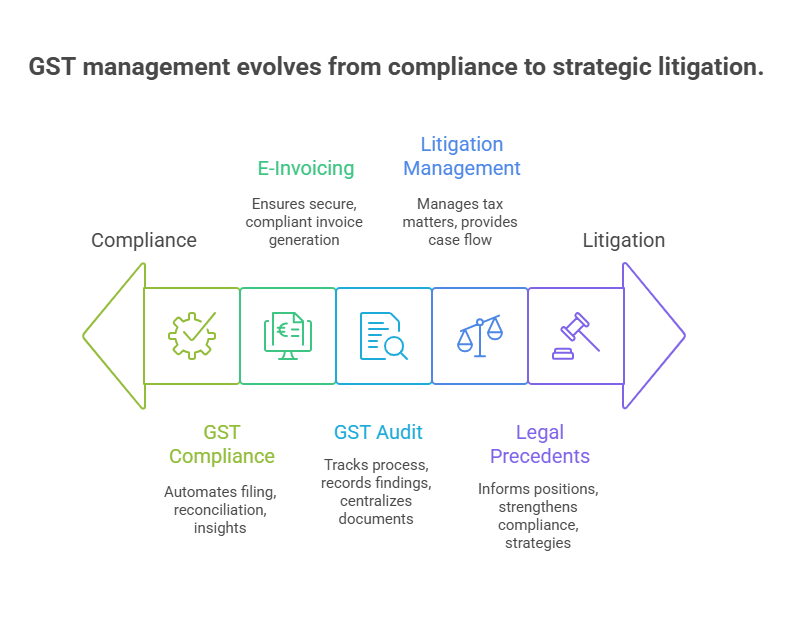

3.2 From Audit to Litigation

An audit often serves as the juncture where unresolved issues transition into formal disputes. When audit findings lead to a Show-Cause Notice (SCN), the matter officially enters the realm of litigation. It is here that a Seamless Case Transition capability becomes invaluable. All audit findings, correspondence, and documentation should be systematically transferred into a litigation management framework. This ensures continuity and provides the legal team with a flawless, chronologically sound data trail from the case's inception.

This seamless escalation from an audit finding to a managed legal case is fundamental to navigating the broader world of tax litigation.

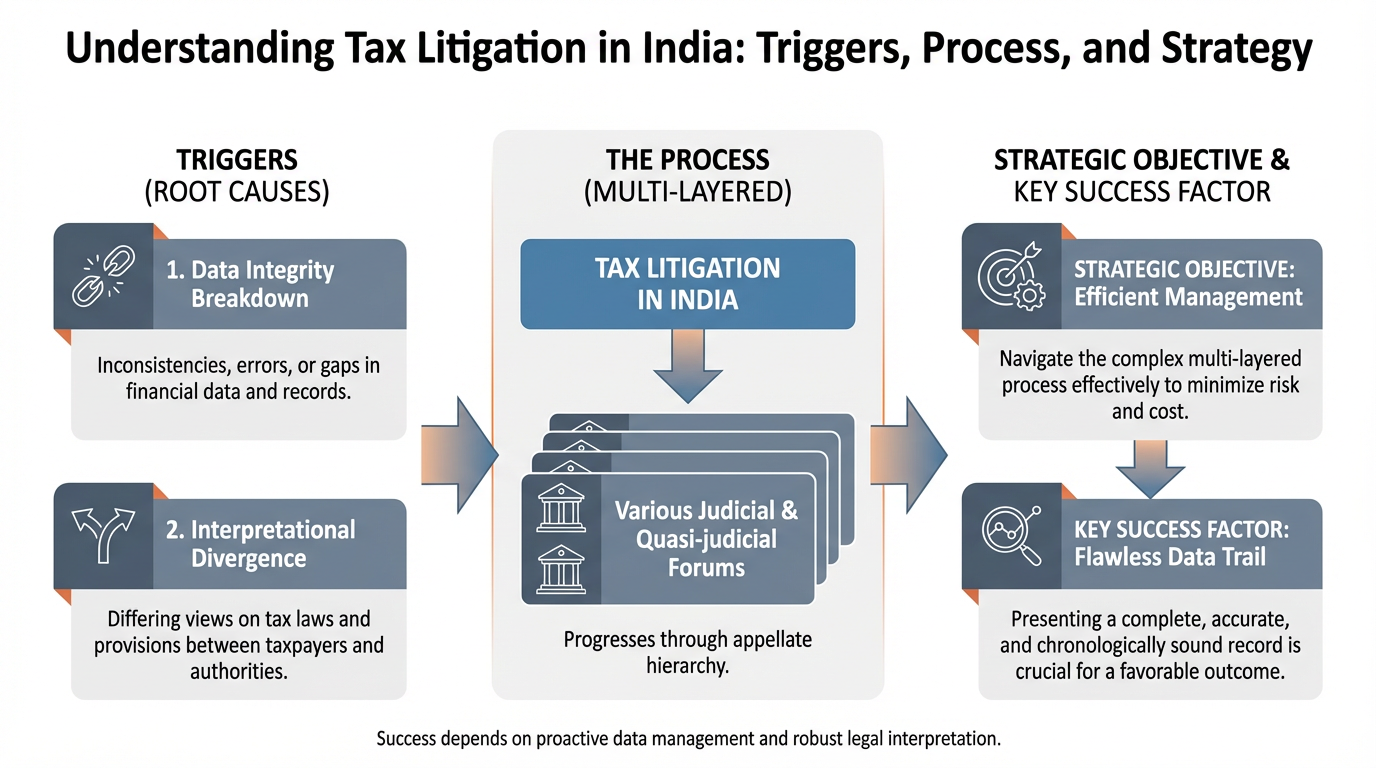

4.0 The Landscape of Tax Litigation in India

Tax litigation in India arises when data integrity breaks down or when interpretations of the law diverge. It is a multi-layered process that unfolds across various judicial and quasi-judicial forums. The strategic objective for any business is to manage this process efficiently, and success often depends on presenting a flawless, chronologically sound data trail.

4.1 Managing the Litigation Spectrum

A robust litigation management system must accommodate disputes from both the current GST regime and legacy indirect tax laws.

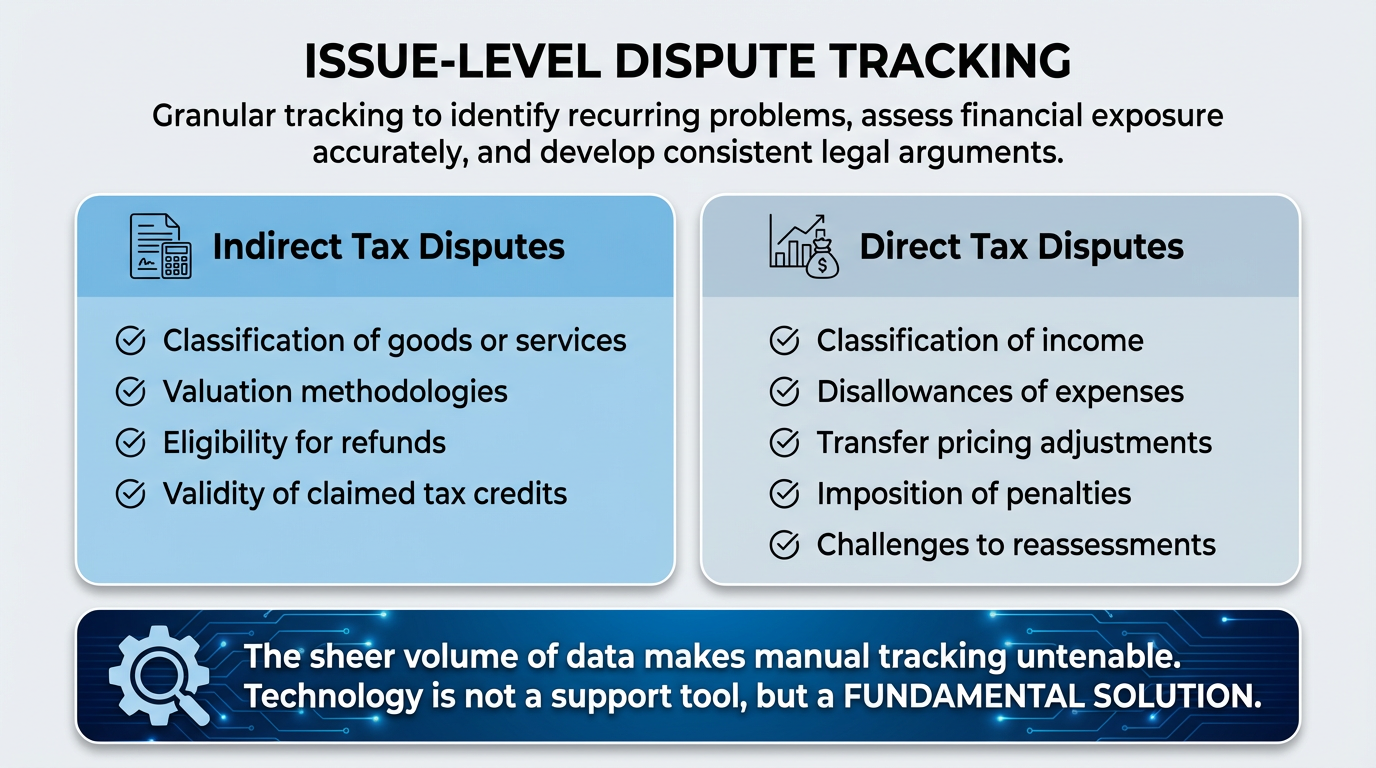

4.2 Issue-Level Dispute Tracking

An effective litigation strategy depends on tracking disputes at a granular, issue-specific level. This allows businesses to identify recurring problems, assess financial exposure accurately, and develop consistent legal arguments. Key dispute categories include:

• Indirect Tax: Classification of goods or services, valuation methodologies, eligibility for refunds, and validity of claimed tax credits.

• Direct Tax: Classification of income, disallowances of expenses, transfer pricing adjustments, imposition of penalties, and challenges to reassessments.

The sheer volume of data involved makes manual tracking untenable, introducing technology not as a support tool, but as a fundamental solution.

5.0 Leveraging Technology as a Strategic Enabler

In India's data-driven tax regime, a company's technology stack is its compliance strategy. It has transcended its role as a support function to become a core strategic asset. An inferior or fragmented tech stack is no longer just an inefficiency; it is a direct and quantifiable liability. Integrated software platforms are essential for transforming tax management from a reactive cost center into a proactive, intelligence-led function that safeguards revenue and mitigates risk.

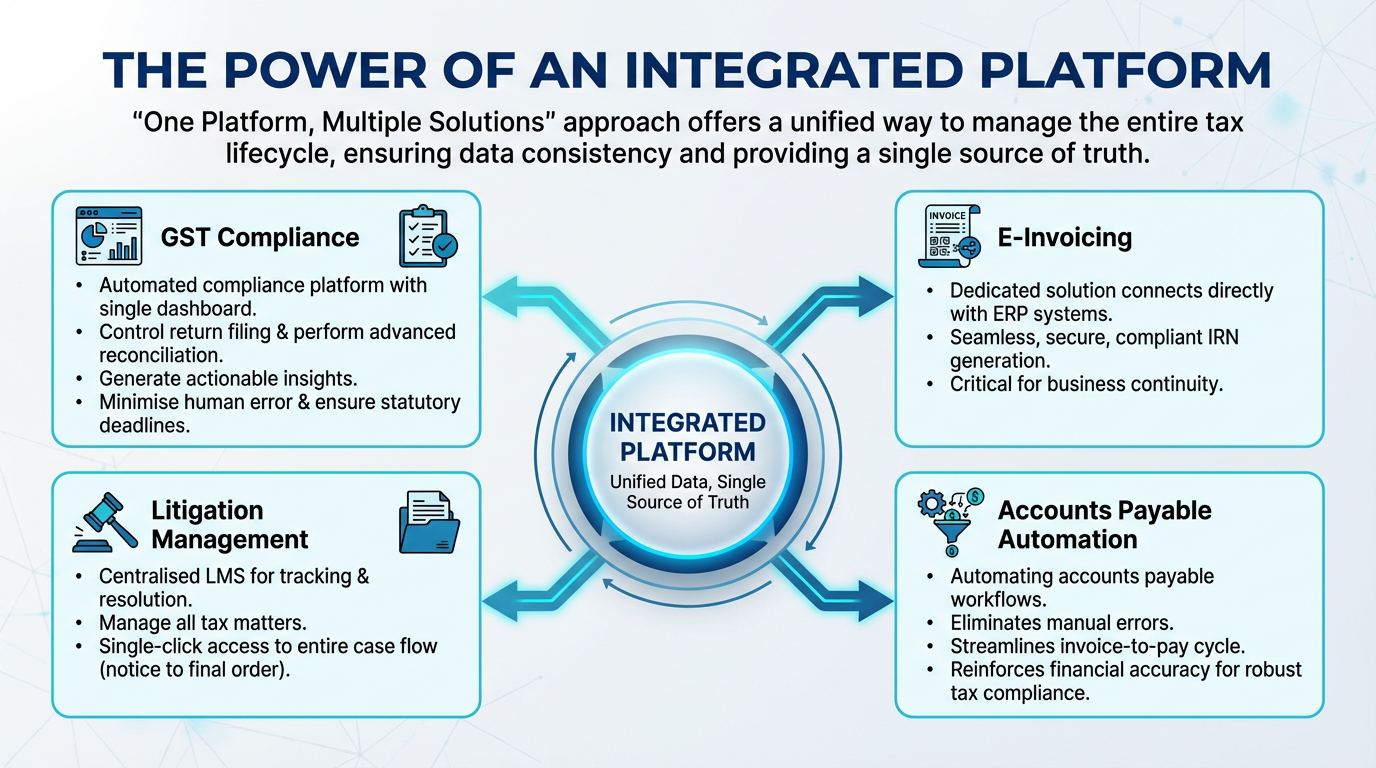

5.1 The Power of an Integrated Platform

A "One Platform, Multiple Solutions" approach offers a unified way to manage the entire tax lifecycle, ensuring data consistency and providing a single source of truth.

• GST Compliance: An automated compliance platform provides a single dashboard to control return filing, perform advanced data reconciliation, and generate actionable insights, minimising human error and ensuring statutory deadlines are met.

• E-Invoicing: A dedicated e-invoicing solution connects directly with a company's ERP systems to ensure seamless, secure, and compliant generation of Invoice Reference Numbers (IRNs), which is critical for business continuity.

• Litigation Management: A centralised Litigation Management System (LMS) allows for the tracking, management, and resolution of all tax matters, providing single-click access to the entire case flow from notice to final order.

• Accounts Payable Automation: Automating accounts payable workflows eliminates manual errors and streamlines the invoice-to-pay cycle, reinforcing the overall financial accuracy that underpins robust tax compliance.

5.2 Quantifiable Business Outcomes

The adoption of such technologies delivers tangible, real-world benefits, as validated by industry leaders:

-

A leading logistics and supply chain organisation highlights how an integrated platform helped them overcome the challenge of maintaining consolidated registers across a geographically dispersed national workforce, enabling effective reconciliation.

-

A diversified business conglomerate attests to the value of a solution that handles both GST return filing and e-invoicing seamlessly, backed by round-the-clock customer support that ensures business continuity.

While technology provides the 'how,' businesses must also understand the 'what'—the core legal principles that define the boundaries of the tax environment.

6.0 Key Legal Precedents and Their Business Implications

The GST framework is a dynamic legal field continuously shaped by judicial interpretations. For businesses, understanding key rulings from the High Courts and the Supreme Court is strategically vital for assessing risks, strengthening compliance positions, and formulating effective litigation strategies.

6.1 Authoritative Rulings and Analysis

Several landmark judicial principles have emerged with direct implications for businesses operating under the GST regime.

1. Principle: ITC Protection for Bona Fide Purchasers. The Supreme Court has ruled that Input Tax Credit cannot be denied to a bona fide purchaser solely because their seller failed to deposit the collected tax with the government. Business Implication: This ruling offers a powerful defense against ITC denial due to vendor default. It reinforces the need to maintain meticulous documentation—including tax invoices and proof of payment—to establish one's status as a bona fide purchaser.

2. Principle: Suspension of Recovery on Appeal Pre-Deposit. The Supreme Court has affirmed that once a taxpayer makes the mandatory 10% pre-deposit required to file an appeal, all departmental recovery proceedings, including bank account attachments, must be suspended. Business Implication: This provides immediate financial relief and certainty to businesses challenging a tax demand, preventing coercive recovery actions while the case is sub-judice and allowing operations to continue without disruption.

3. Principle: Validity of Search & Seizure. The Delhi High Court has upheld the broad powers of GST authorities to conduct searches under Section 67, provided a "reason to believe" is properly documented by officers before initiating the action. Business Implication: While tax authorities possess significant inspection powers, this ruling clarifies such actions are not arbitrary. A business can challenge a search where it can be demonstrated that procedural safeguards were ignored or that the "reason to believe" was not properly recorded.

4. Principle: Limitation Period on Mistaken Refunds. The Andhra Pradesh High Court ruled that the standard two-year limitation period under Section 54 for claiming refunds does not apply to the department's recovery of a refund of tax that was paid by mistake. Business Implication: This ruling clarifies that the department is not constrained by the same time limits as taxpayers when recovering refunds issued due to mistaken payments, expanding the potential period of scrutiny for such transactions.

These legal interpretations, combined with a mastery of compliance, audit readiness, and technology, form the basis of a resilient GST strategy.

7.0 Conclusion: Best Practices for a Resilient GST Strategy

Navigating India's dynamic GST system requires a holistic approach that integrates robust compliance, proactive audit readiness, and strategic litigation management, all enabled by modern technology. Success in this environment is defined by foresight, resilience, and an unwavering commitment to data integrity.

For tax professionals and business leaders, the following best practices serve as an actionable checklist for excellence:

• Embrace Automation: Implement integrated software solutions to automate return filing, reconciliation, and e-invoicing. This minimises human error, ensures data integrity, and frees up skilled professionals for strategic analysis.

• Treat Vendor Compliance as a Core Business Function: Your ITC is a direct dependency on your supply chain's diligence. Implement a rigorous, technology-driven system to monitor vendor filing patterns and data accuracy, protecting your ITC claims and avoiding disputes.

• Maintain a Centralised Digital Repository: Use a dedicated system to store all tax-related documents, correspondence, and notices. This ensures that critical information is secure and immediately accessible during audits and litigation, forming your single source of truth.

• Adopt a Proactive Audit Posture: Treat departmental audits as opportunities to demonstrate compliance health. Ensure that all responses are structured, well-documented, and timely to prevent minor issues from escalating.

• Stay Judicially Informed: The GST landscape is constantly being shaped by the judiciary.

GST Anti Evasion Department Powers | Powers of GST Officers | DRC-01 | Statement of Facts and Grounds of Appeal Format GST | Valuation Rules Under GST

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified