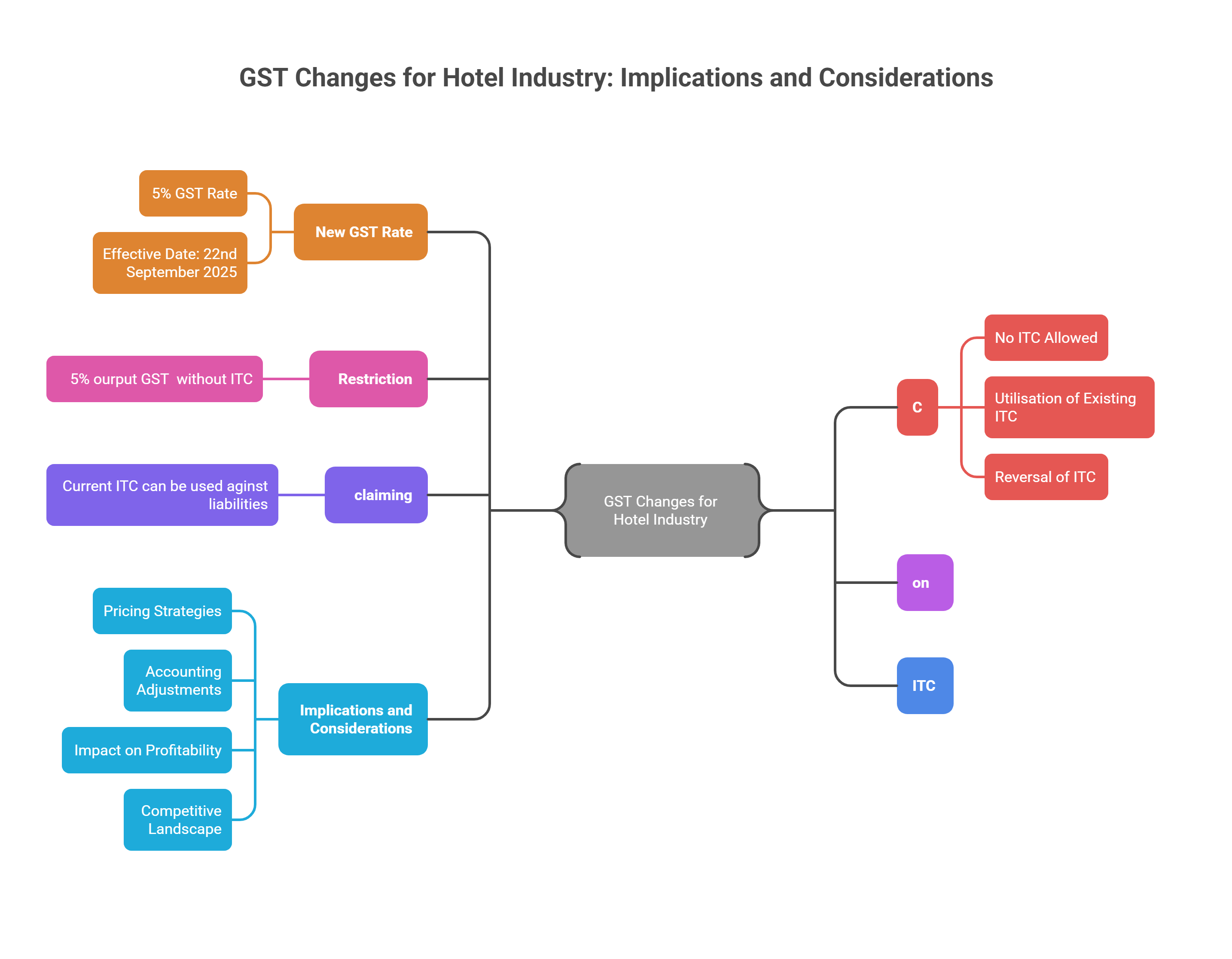

The changes to the Goods and Services Tax (GST) rate for hotel accommodation services, as recommended by the 56th GST Council, are analysed, and the implications of these changes on Input Tax Credit (ITC) are discussed. Specifically, it focuses on the reduction of the GST rate to 5% for hotel accommodations with a value of supply up to ₹7,500 per unit per day and the corresponding restriction on claiming ITC. The document also addresses the effective date of these changes, the utilisation of existing ITC, and the reversal of ITC for supplies made under the new rate structure.

The changes to the Goods and Services Tax (GST) rate for hotel accommodation services, as recommended by the 56th GST Council, are analysed, and the implications of these changes on Input Tax Credit (ITC) are discussed. Specifically, it focuses on the reduction of the GST rate to 5% for hotel accommodations with a value of supply up to ₹7,500 per unit per day and the corresponding restriction on claiming ITC. The document also addresses the effective date of these changes, the utilisation of existing ITC, and the reversal of ITC for supplies made under the new rate structure.

Changes for the Hotel Industry

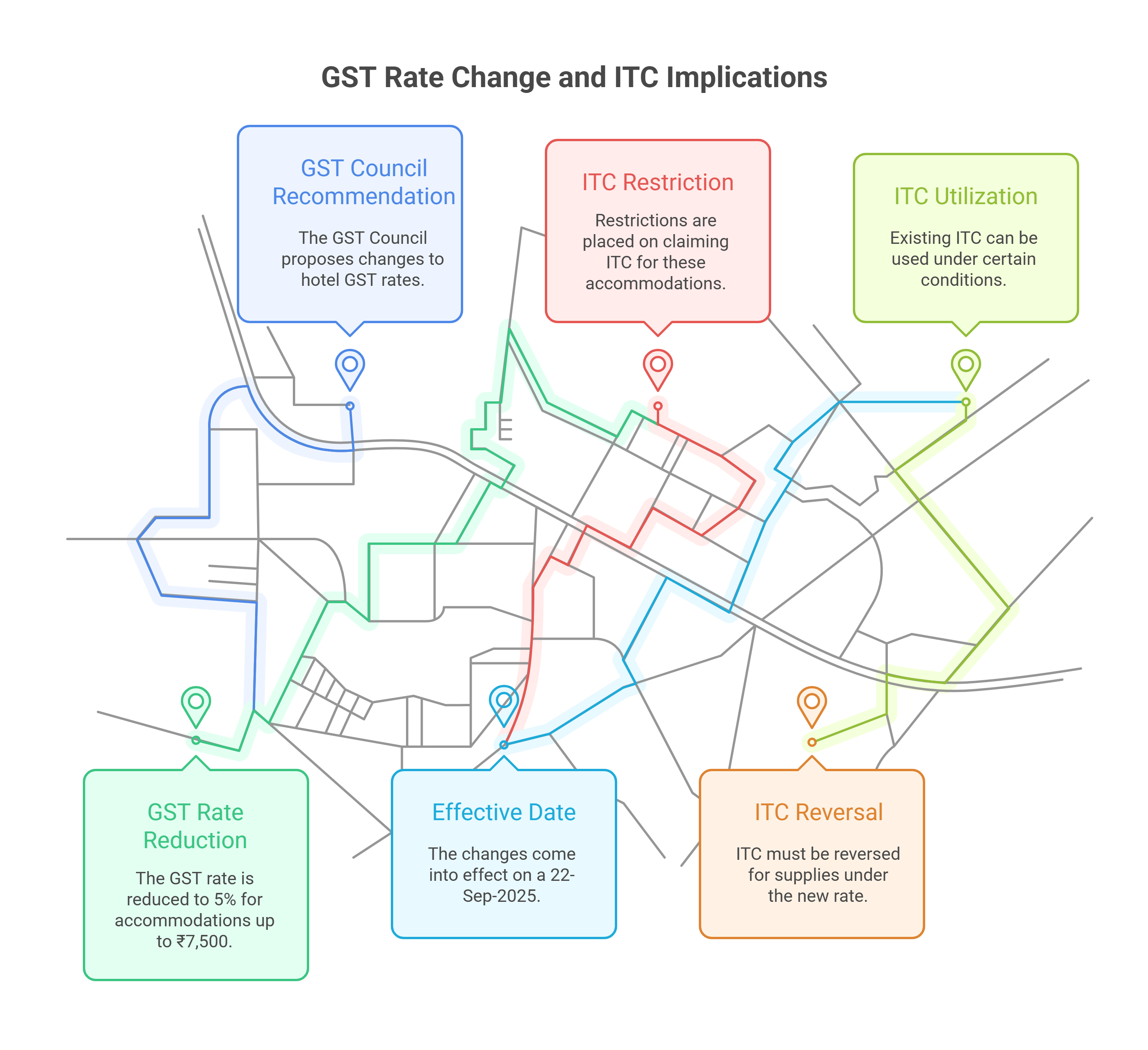

The 56th GST Council has proposed a significant change in the GST rate applicable to hotel accommodation services, aiming to provide relief to budget-friendly hotels and potentially boost tourism. To stay updated with such developments, you must regularly track GST rates in India across different sectors.

-

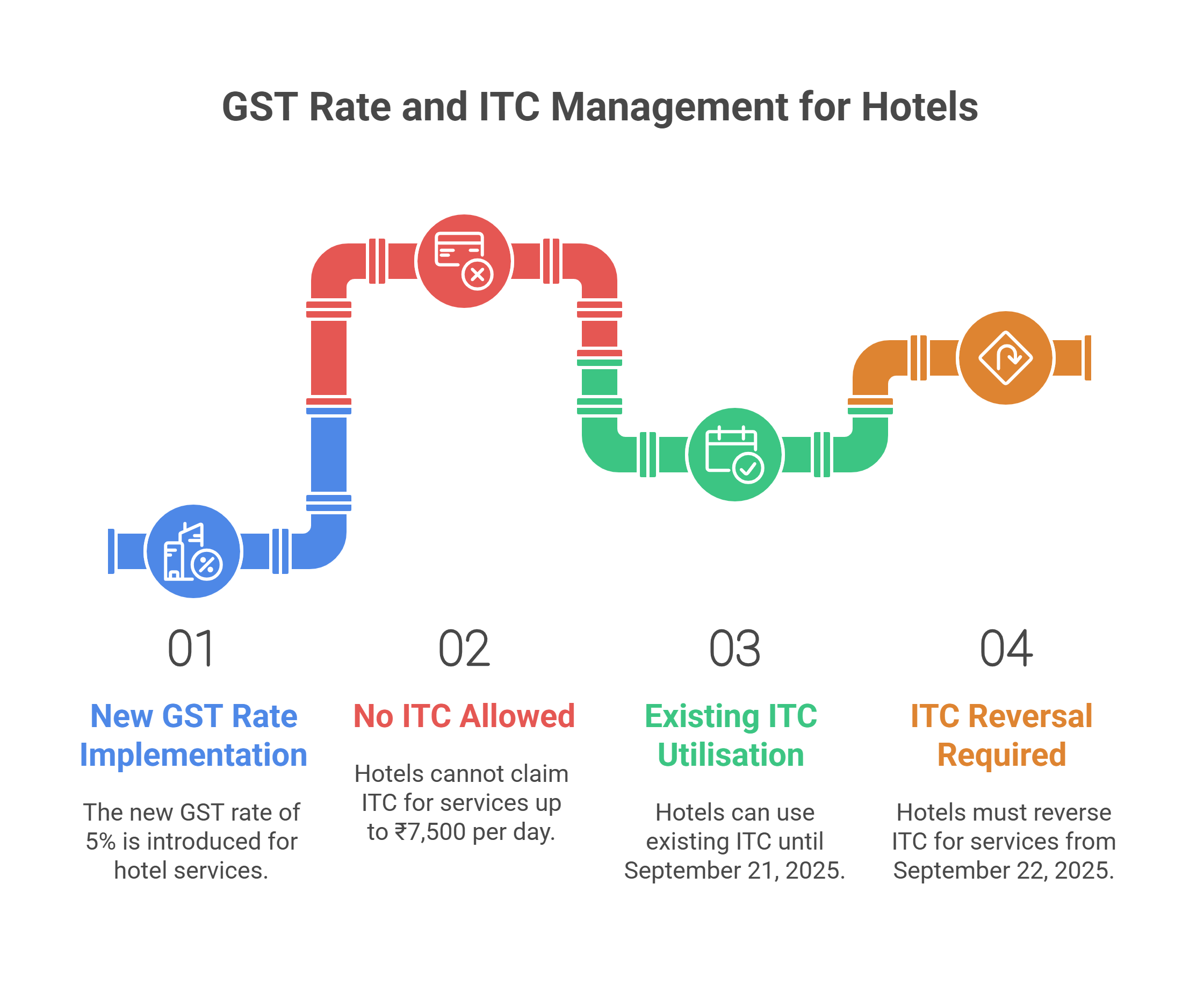

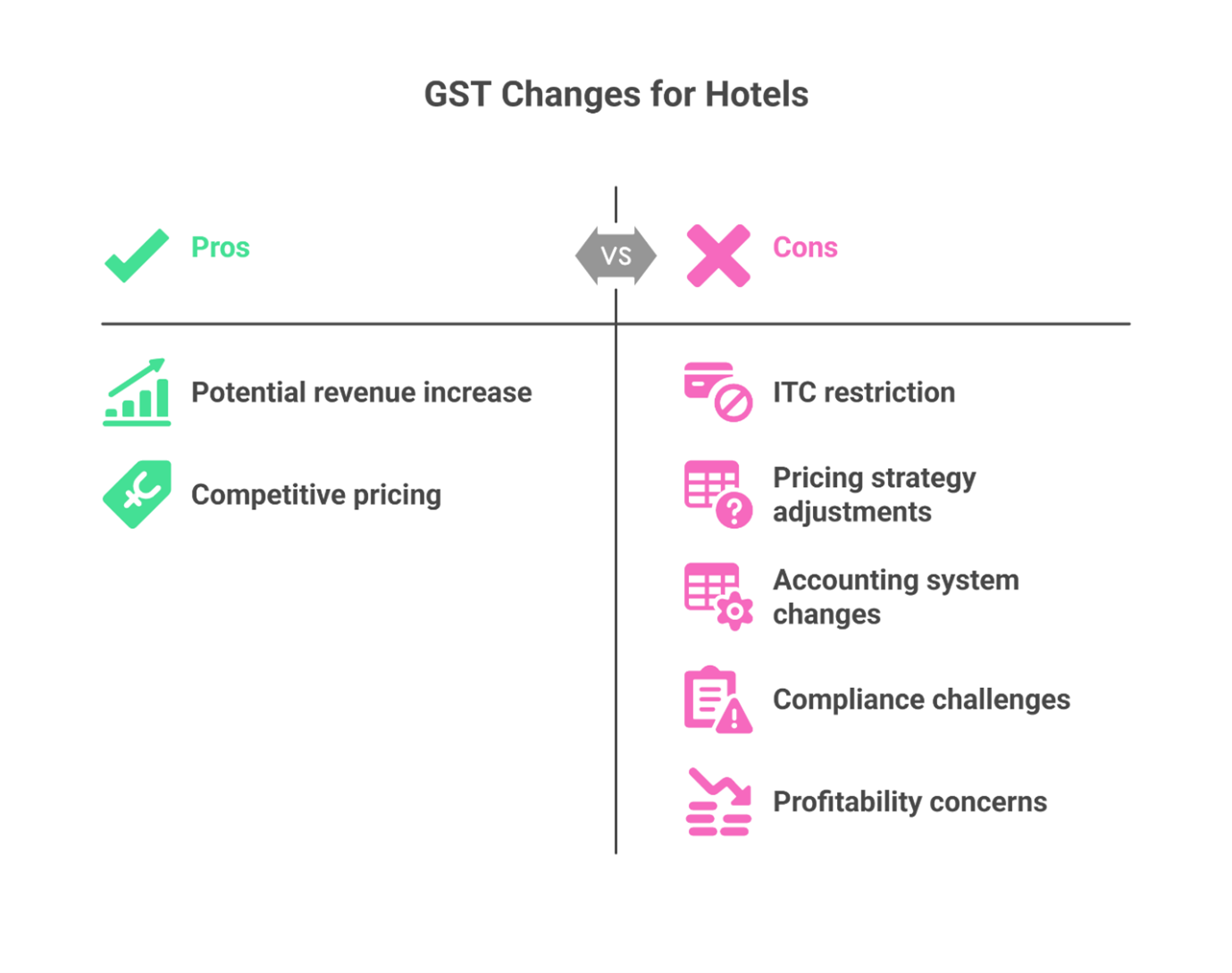

New GST Rate: The GST rate for the "supply of ‘hotel accommodation’ having value of supply of a unit of accommodation less than or equal to seven thousand five hundred rupees per unit per day or equivalent" will be reduced from 12% to 5%. This reduction is intended to make these accommodations more affordable and competitive.

-

Effective Date: This change, along with other changes to GST rates on services, will come into force from 22nd September 2025. This provides the hotel industry with a lead time to adjust its pricing strategies and accounting systems to comply with the new regulations.

Impact on Input Tax Credit (ITC)

A crucial aspect of the new GST rate for hotel accommodation is the restriction on claiming Input Tax Credit (ITC). This condition significantly impacts the financial implications of the rate reduction for hotel businesses.

-

No ITC Allowed: Hotel accommodation services with a value up to ₹7,500 per unit per day will attract the new GST rate of 5% without ITC. This means that businesses providing these services will not be able to claim credit for the GST they pay on their inputs (goods and services used to provide the accommodation service). This includes expenses such as laundry services, food supplies, maintenance, and other operational costs.

-

Utilisation of Existing ITC: Any ITC already present in a business's electronic credit ledger can be used to pay off output tax liabilities for supplies made up to 21st September 2025. This allows businesses to utilise their existing ITC before the new rate structure comes into effect.

-

Reversal of ITC: For supplies made from 22nd September 2025 onwards under the new exempt rate structure, any accumulated ITC will need to be reversed as per the provisions of the CGST Act, 2017. This means that hotels must carefully calculate and reverse any ITC attributable to supplies made under the 5% GST rate without ITC. Proper compliance therefore requires a clear understanding of ITC reversal rules under Rule 42 and Rule 43.

Implications and Considerations

The reduction in the GST rate for hotel accommodation up to ₹7,500 per day to 5% is a welcome move for budget hotels. However, the condition that the service provider can no longer claim Input Tax Credit on their business expenses needs careful consideration.

-

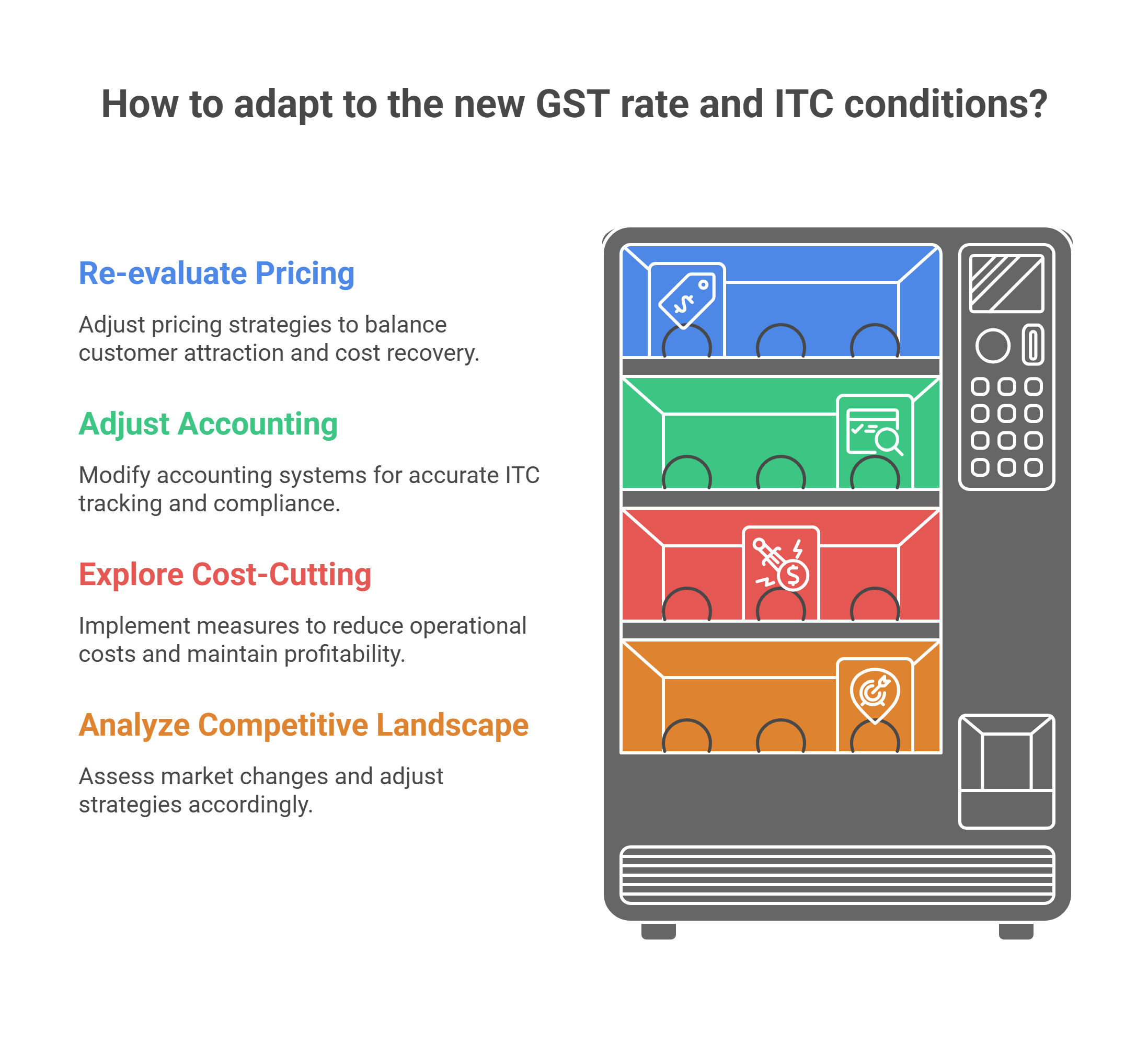

Pricing Strategies: Hotels need to re-evaluate their pricing strategies to account for the loss of ITC. While the lower GST rate may attract more customers, the inability to claim ITC on inputs could increase the overall cost of providing the service. Hotels can estimate the financial impact of such rate changes using a GST calculator for more accurate planning.

-

Accounting Adjustments:

Hotels must adjust their accounting systems to accurately track and reverse ITC related to supplies made under the new rate structure. This requires meticulous record-keeping and compliance with the CGST Act, 2017. In practice, many businesses also opt for a good gst software to stay updated with frequent GST changes, manage ITC reversals correctly, and avoid manual errors during compliance.

Hotels must adjust their accounting systems to accurately track and reverse ITC related to supplies made under the new rate structure. This requires meticulous record-keeping and compliance with the CGST Act, 2017, especially as frequent GST changes, rate updates, and ITC rules make manual tracking difficult, which is why most businesses eventually move towards using a good GST software to manage these adjustments more accurately.

-

Impact on Profitability: The overall impact on profitability will depend on the extent to which hotels can pass on the increased cost of inputs to customers. Hotels may need to explore cost-cutting measures to mitigate the impact of the ITC restriction.

-

Competitive Landscape: The new GST rate structure could alter the competitive landscape of the hotel industry. Hotels that primarily cater to budget travellers may benefit from the lower GST rate, while those that offer higher-end accommodations may not be significantly affected.

Conclusion

The proposed changes to the GST rate for hotel accommodation services, while seemingly beneficial, come with the significant condition of restricting Input Tax Credit. Hotels must carefully analyse the implications of these changes on their pricing strategies, accounting systems, and overall profitability. Compliance with the CGST Act, 2017, regarding the reversal of ITC is crucial to avoid penalties. The hotel industry needs to adapt to these changes to remain competitive and sustainable in the evolving GST landscape.

Know Your GST, GST Verification, GST Calculator, HSN Code Search, GST Return Status

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified