GST Audit Under Section 65: A Strategic Guide for CFOs & Finance Leaders

Navigating GST Audit Under Section 65: A Strategic Guide for CFOs and Finance Directors

As a CFO or Director of Finance, you're likely familiar with the self-assessment nature of India's GST regime. However, what happens when tax authorities decide to verify your company's compliance through an audit under Section 65?

This comprehensive guide will help you understand the audit process, prepare your organization effectively, and manage potential outcomes strategically.

Understanding the Foundation: Why Section 65 Matters to Your Organization

The GST system operates on trust - businesses self-assess and file returns, but the government reserves the right to verify compliance. Section 65 of the CGST Act, 2017 provides tax authorities with comprehensive powers to examine your company's records, returns, and documents. Think of it as a health check-up for your GST compliance, where authorities verify whether your declared turnover, taxes paid, refunds claimed, and input tax credits are accurate.

Unlike the routine statutory audits under Section 35(5) that you might be familiar with, or the more intensive special audits under Section 66, Section 65 audits occupy a middle ground. They're discretionary, risk-based examinations that can significantly impact your organization's financial position and reputation if not managed properly.

The Trigger Points: How Your Company Gets Selected for Audit

Understanding why companies get selected for audit helps you assess and manage your risk profile. The selection process follows a sophisticated risk-based methodology that considers multiple factors:

Financial Indicators That Raise Red Flags:

-

Significant variations in turnover compared to previous years

-

Unusual patterns in input tax credit claims

-

Mismatches between GSTR-3B and GSTR-2A filings

-

Mismatches between E-Way Bill and GSTR-1

-

Non-payment to Creditors within 180 days leads to reversal of ITC

-

Abnormal financial ratios like gross profit margins or sales-purchase ratios

Compliance History Matters:

Your past behavior influences future scrutiny. Delayed return filings, previous compliance issues, or patterns of amendments can increase your audit risk. Think of it as a credit score for tax compliance - every action contributes to your overall risk profile.

Industry and Size Classifications:

Tax authorities categorize businesses based on turnover and complexity. Large taxpayers receive 40% of available audit resources, making them more likely targets. If your company operates in sectors known for compliance challenges or has multi-location operations, you're automatically in a higher risk category.

The Audit Journey: What to Expect When You're Being Audited

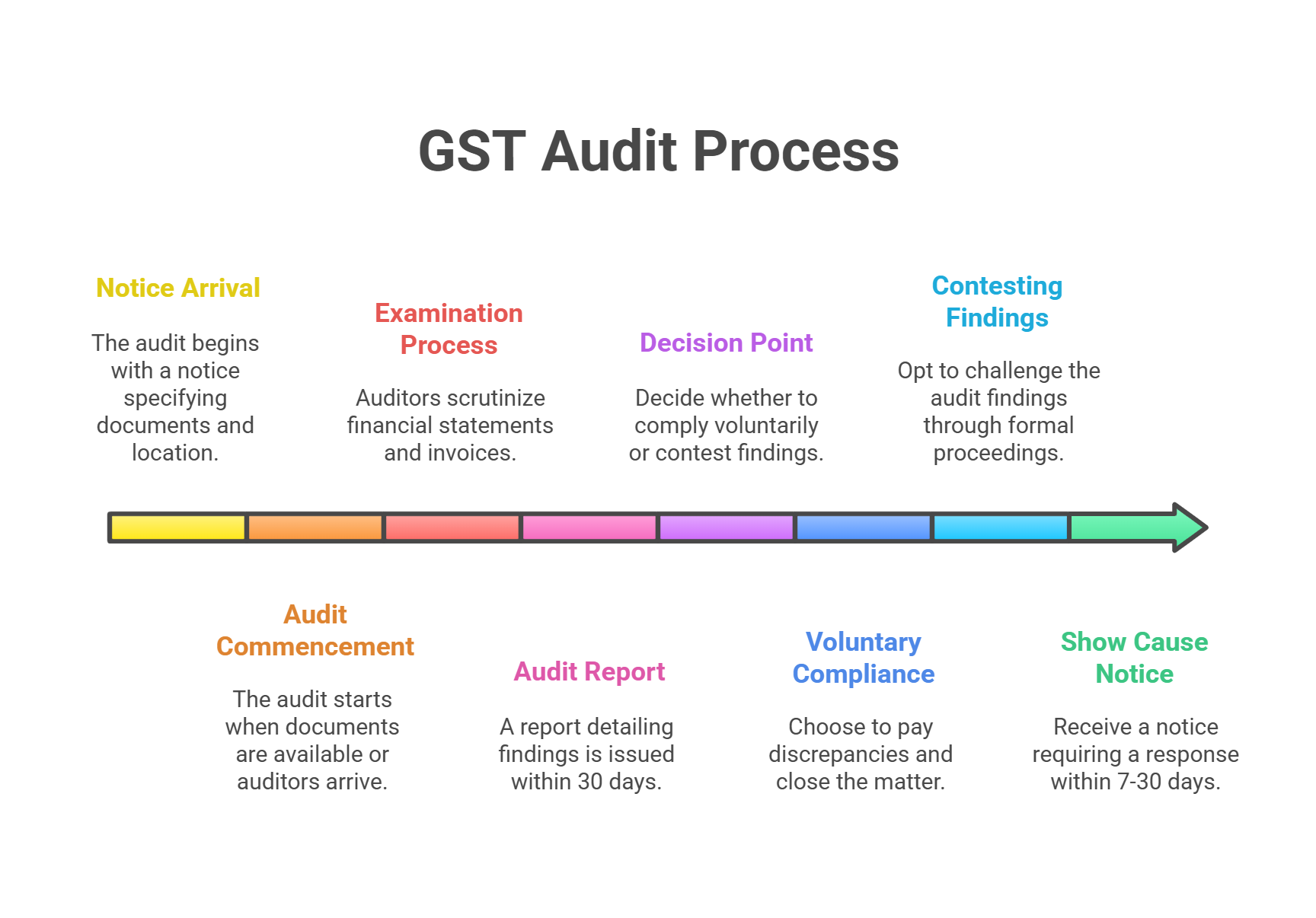

Phase 1: The Notice Arrives

Your audit journey begins when you receive Form GST ADT-01, providing at least 15-30 working days' advance notice. This isn't just a formality - it's your roadmap for the audit. The notice specifies which documents the auditors want to examine and where the audit will take place (either at your premises or the tax office).

Strategic Tip: Use these 15-30 days wisely. This is your preparation window, not a grace period. Mobilize your finance team immediately to gather and review the requested documents.

Phase 2: Audit Commencement and Duration

The audit officially begins when you make documents available to the auditors or when they arrive at your premises, whichever is later. Here's a critical insight: audits must be completed within three months, though this can extend to nine months with proper justification.

What Determines Duration?

-

Manufacturing companies typically face longer audits than service providers

-

Multi-location businesses require more time

-

Complex supply chains or high transaction volumes extend timelines

-

The auditor's initial findings may trigger deeper examination

Phase 3: The Examination Process

During the audit, officers will scrutinize various aspects of your GST compliance:

-

Verification of financial statements against GST returns

-

Examination of purchase and sales invoices

-

Review of input tax credit documentation

-

Analysis of exemptions and deductions claimed

-

Checking the accuracy of tax rates applied

Your Rights During This Phase: You can have your regular employees handle the audit, or engage professionals like Chartered Accountants or advocates. This representation right is crucial - it allows your business operations to continue while specialists manage the audit process.

Managing Audit Outcomes: From Findings to Resolution

Understanding the Audit Report (Form GST ADT-02)

Within 30 days of audit completion, you'll receive Form GST ADT-02 detailing the findings. Here's a crucial point many executives miss: this report isn't a tax demand - it's a communication of findings that may lead to formal proceedings.

The report will categorize discrepancies into:

-

Short payment of various tax components (IGST, CGST, SGST, Cess)

-

Incorrectly claimed input tax credits

-

Erroneous refund claims

-

Interest and Penalties

-

Other compliance gaps

The Critical Decision Point: Responding to Findings

When discrepancies are found, you face a strategic crossroads that can significantly impact your financial exposure:

Option 1: Voluntary Compliance Under Section 73(5) If the findings are accurate, voluntary payment offers several advantages:

-

Potential reduction in penalties

-

Faster closure of the matter

-

Preservation of goodwill with tax authorities

-

Avoiding lengthy litigation

Option 2: Contesting the Findings If you disagree with the audit findings, formal proceedings will follow under either:

-

Section 73: For non-fraudulent discrepancies (3-year time limit)

-

Section 74: For cases involving fraud or willful misstatement (5-year time limit, higher penalties)

The Show Cause Notice Process

If authorities proceed with formal action, you'll receive Form GST DRC-01. This is when the stakes become real - you have just 7 days to respond initially (to avoid GSTR-1 filing restrictions) and 30 days for a comprehensive response.

Strategic Consideration: The distinction between Sections 73 and 74 is critical. Section 74 proceedings carry penalties ranging from 15% to 100% of the tax amount, while Section 73 penalties are significantly lower. The characterization of your case can dramatically impact your financial exposure.

Building Your Audit Defence Strategy

Pre-Audit Preparation: Your Best Investment

Think of audit preparation as insurance - the investment you make before an audit significantly reduces your exposure during one. Here's your preparation framework:

Documentation Excellence:

-

Maintain real-time reconciliation between books of accounts and GST returns

-

Ensure all invoices have proper supporting documentation

-

Create audit trails for all input tax credit claims

-

Document the business rationale for exemptions and deductions

Internal Audit Program: Conduct quarterly internal reviews focusing on:

-

GSTR-1 and GSTR-3B reconciliation

-

Input tax credit eligibility verification

-

Proper tax rate application

-

Timely return filing compliance

Technology Infrastructure: Invest in GST compliance software that provides:

-

Automated reconciliation capabilities

-

Mismatch identification tools

-

Audit trail maintenance

-

Document management systems

During-Audit Best Practices

Communication Strategy:

-

Designate a single point of contact for auditors

-

Maintain professional, cooperative relationships

-

Document all auditor requests and your responses

-

Seek clarification on ambiguous requests immediately

Information Management:

-

Provide only what's specifically requested

-

Ensure all provided documents are complete and accurate

-

Maintain copies of everything submitted

-

Track timelines for all submissions

Post-Audit Action Plan

Immediate Steps:

-

Analyze the audit report thoroughly with your tax advisors

-

Quantify the financial impact of findings

-

Assess the strength of your position on disputed items

-

Make the voluntary compliance vs. litigation decision

Long-term Improvements: Use audit findings as a diagnostic tool to:

-

Strengthen weak compliance areas

-

Update internal controls

-

Enhance team training

-

Refine your GST processes

Financial Impact Considerations

As a CFO or Finance Director, you need to understand the potential financial implications:

Direct Costs:

-

Tax dues identified

-

Interest charges (18% per annum)

-

Penalties (varying based on Section 73 vs. 74)

-

Professional fees for representation

Indirect Costs:

-

Management time and attention

-

Potential reputational impact

-

Opportunity cost of locked working capital

-

System and process upgrade investments

Risk Mitigation Strategies

Organizational Readiness Assessment

Evaluate your audit readiness across five key dimensions:

-

Documentation Quality: Are your records audit-ready at any time?

-

Process Robustness: Do you have documented GST compliance processes?

-

Team Capability: Is your team trained to handle audit queries?

-

Technology Support: Do your systems support compliance and audit requirements?

-

Professional Support: Do you have access to specialized GST expertise?

Creating an Audit Response Framework

Develop a documented audit response plan that includes:

-

Roles and responsibilities matrix

-

Document production protocols

-

Escalation procedures

-

Communication guidelines

-

Decision-making frameworks for voluntary compliance

Key Takeaways for Leadership

-

Proactive Compliance is Cost-Effective: The cost of maintaining robust compliance is fraction of potential audit exposures.

-

Early Engagement Matters: How you respond in the first 30 days after receiving audit findings can significantly impact outcomes.

-

Documentation is Your Defense: Well-maintained records and clear audit trails are your best protection against adverse findings.

-

Professional Support is Strategic: Engaging specialized professionals during audits isn't an expense - it's risk management.

-

Learn from Every Audit: Whether findings are favorable or adverse, each audit provides insights for strengthening your compliance framework.

Conclusion: Turning Compliance into Competitive Advantage

GST audit under Section 65 need not be a crisis - with proper preparation and strategic management, it becomes an opportunity to validate your compliance processes and identify improvement areas. As financial leaders, your role is to ensure your organization views GST compliance not as a regulatory burden but as a business discipline that protects value and enhances operational efficiency.

Remember, in today's transparent tax environment, the question isn't whether you'll face an audit, but when. The organizations that thrive are those that are always audit-ready, treating compliance as an ongoing journey rather than a destination.

By implementing the strategies outlined in this guide, you'll not only minimize audit risks but also build a compliance culture that serves as a competitive advantage in the marketplace. After all, in the world of GST, the best audit defense is a good compliance offense.

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified