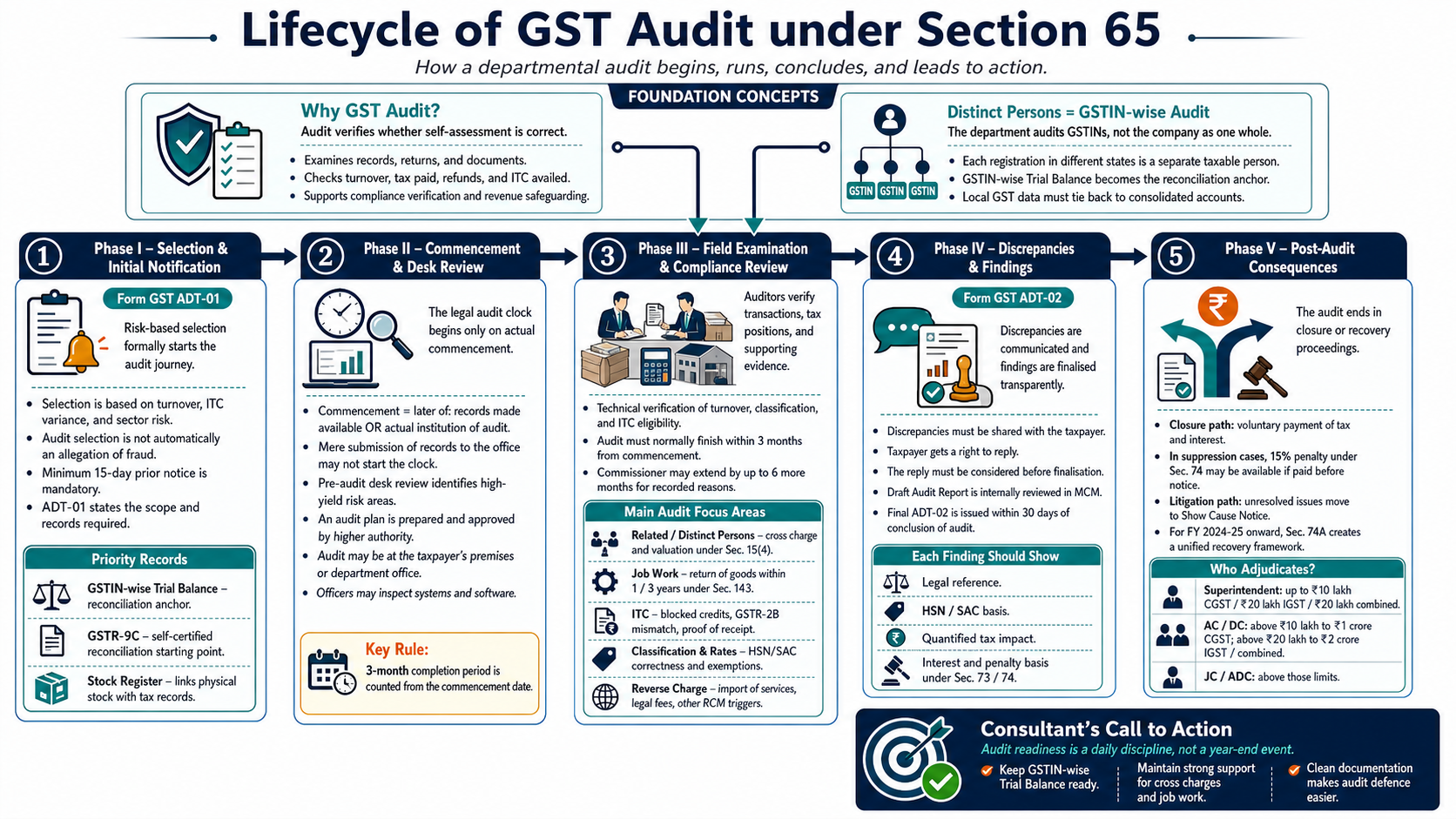

Understanding the purpose of GST departmental audits

In a trust-based self-assessment regime, the integrity of the tax system rests on the accuracy of the taxpayer’s own declarations. However, "trust" is not a substitute for verification. Under Section 2(13) of the CGST Act, an audit is defined as the examination of records, returns, and other documents to verify the correctness of declared turnover, taxes paid, refunds claimed, and input tax credit (ITC) availed, making a thorough understanding of the GST audit process essential for businesses.

Professionals must recognise that departmental audits are the ultimate check-and-balance mechanism designed to safeguard the Government’s treasury and enhance systemic transparency.

This dual-purpose role is summarised below:

Why does the GST department conduct audits?

| Objective | Description |

| Compliance Verification | Validating the accuracy of self-assessed declarations and ensuring a documented audit trail exists for every transaction. |

| Revenue Safeguarding | Identifying tax evasion, fictitious ITC claims, or short payments to protect the integrity of the national exchequer. |

A critical technicality for practitioners is the concept of "distinct persons" under Section 25(4). Because GST is state-centric, every registration (GSTIN) held by a single PAN across different states is treated as a separate legal entity. Consequently, the department does not audit "the company"; it audits specific GSTINs. This necessitates a GSTIN-wise Trial Balance, which serves as the accounting anchor for reconciling local operations with consolidated financial statements.

Now that we understand the purpose, let’s look at how the department selects its subjects and begins the formal process.

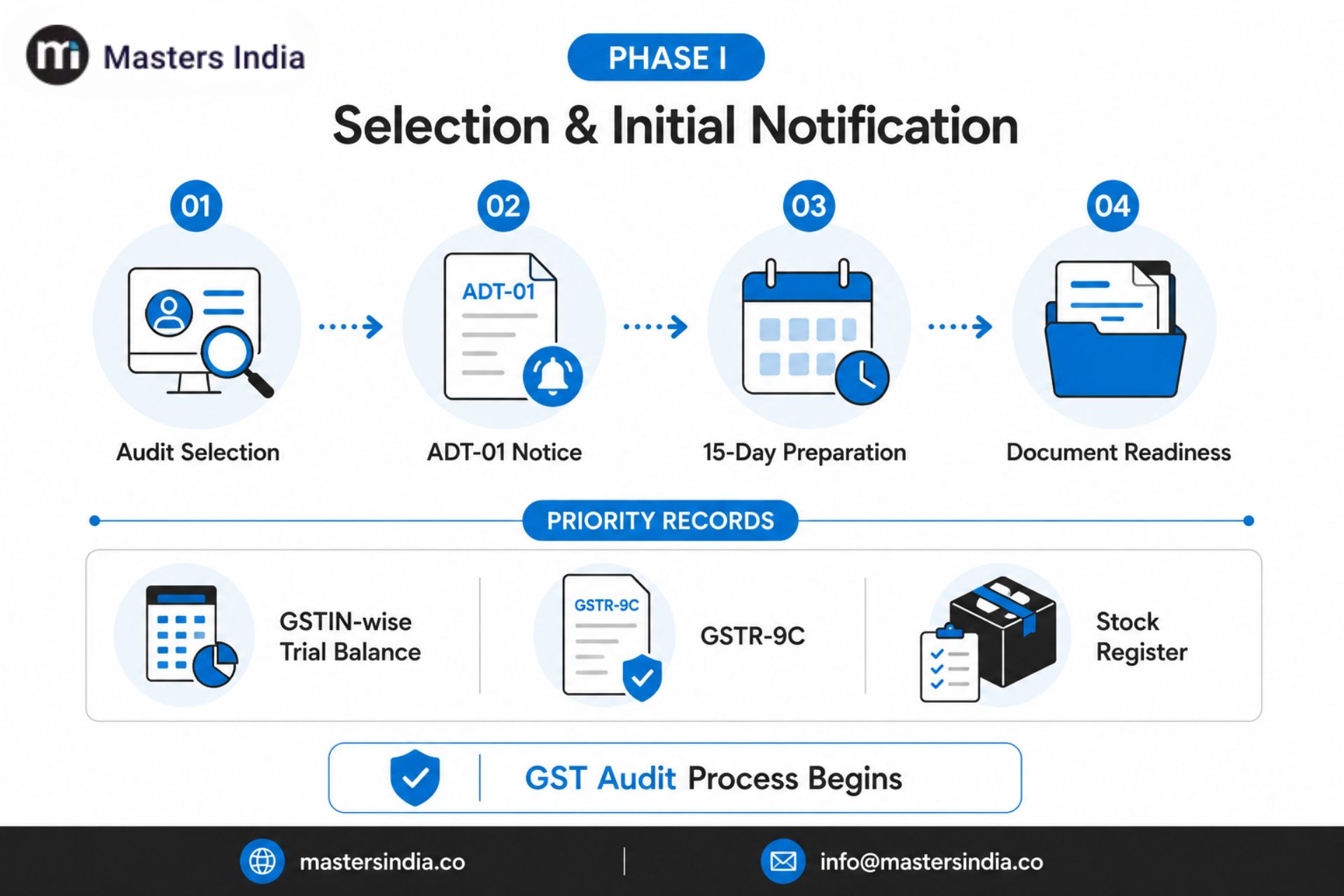

Phase I: Selection and initial notification (form GST ADT-01)

Professionalism notwithstanding that audit selection is a risk-based metric, not an indictment of fraud. Through Step 1 (Audit Selection), the department uses parameters like turnover size, ITC variance, and sector-specific risk profiles to identify taxpayers, which is why many organisations rely on GST reconciliation software to continuously monitor compliance risks.

A fifteen-day notice period serves as a mandatory procedural safeguard. This period is not merely for document collection but for the taxpayer to conduct a final internal review. The formal notification is served via Form GST ADT-01, specifying the scope and the records required.

Core Document Requisition: The Consultant’s Priority List

While the department may request a broad "Master File," professionals must prioritise the following three items as the most critical for audit defence:

-

GSTIN-wise Trial Balance: This is the primary tool for reconciliation. It allows the auditor to verify how specific registrations affect the entity's consolidated financials, ensuring that no income has been "lost" across state borders.

-

Form GSTR-9C: This is the "self-certified truth." As a pre-reconciled statement between the annual return and audited accounts, it is the auditor's starting point for identifying potential discrepancies.

-

Stock Register: This provides the physical-to-paper bridge. Auditors examine this to ensure that credits claimed on inputs match the physical movement or consumption of goods, preventing "paper-only" transactions.

With the notice served and records prepared, the narrative shifts to the official "commencement" of the audit.

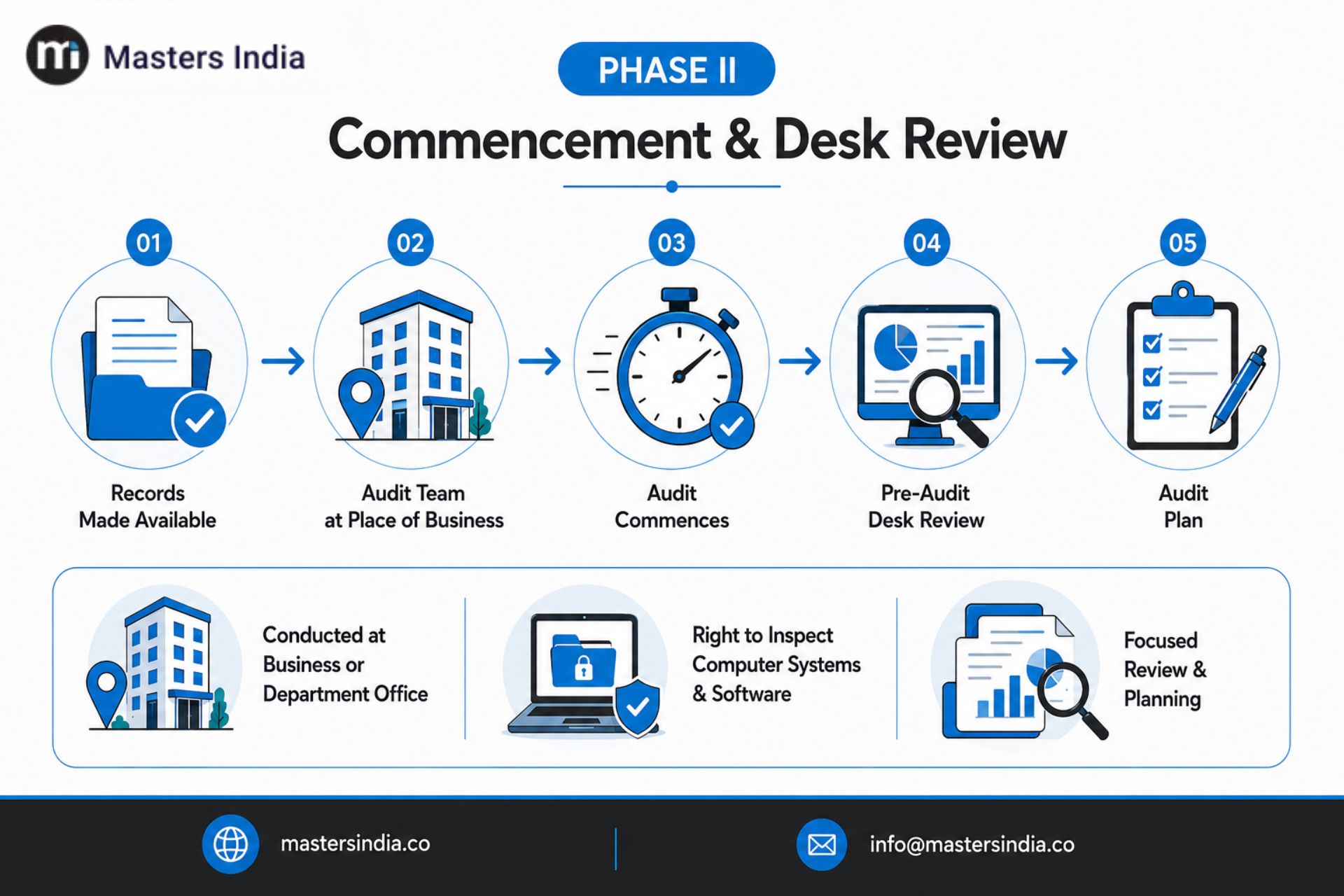

Phase II: Commencement and the desk review

The "clock" for an audit is governed by a strict legal definition. According to the Explanation to Section 65(4), the Commencement of Audit is the later of:

-

The date on which records called for are made available by the registered person; OR

-

The date of the actual institution of the audit at the place of business.

Practitioner’s Note: Mere submission of records to the department's office does not always trigger the commencement clock. The "actual institution" or physical arrival of the team is often the deciding factor, a nuance critical for tracking the three-month completion deadline.

Before the field visit, the department conducts a Pre-audit Desk Review (Step 4). This is not a "fishing expedition"; it is a targeted analysis where the team identifies "maximum yield" areas. This culminates in Step 5: The Audit Plan, a structured roadmap approved by a higher authority to ensure the audit remains efficient and focused on high-risk technicalities.

Per Section 65(2), the audit may be conducted at the taxpayer’s registered place of business or the department's office. Regardless of the location, the department retains the right to inspect computer systems and software to ensure revenue interests are protected.

Once the audit has officially commenced, the focus turns to the rigorous verification of financial data.

Phase III: Field examination and areas of compliance

During the field examination, the audit team verifies the technical accuracy of turnover, classification, and ITC eligibility. The law imposes a Three-Month Completion Limit from the date of commencement, though the Commissioner may extend this by a further six months for recorded reasons.

Technical Audit Focus Areas

| Compliance Area | Key Risk Issue | Primary Documents to be Examined |

| Related/Distinct Person Transactions | Undervaluation or lack of "Cross Charge" (Section 15(4)). | Inter-unit ledgers, Cost allocations, Transfer pricing docs. |

| Job Work Compliance | Failure to return goods within 1/3 years (Section 143). | Form ITC-04, Delivery Challans, Gate registers. |

| Input Tax Credit (ITC) | Claims on "Blocked Credits" (Sec 17(5)) or GSTR-2B mismatch. | Purchase registers, Invoices, Proof of receipt (GRN). |

| Classification & Rates | Incorrect HSN/SAC or misinterpretation of exemptions. | Tax invoices, Contracts, Rate notifications. |

| Reverse Charge (RCM) | Failure to pay tax on import of services or legal fees. |

Foreign remittances, Bank statements, Expense ledgers. |

Following the verifications, any identified gaps are brought to the taxpayer's attention for reconciliation, a process increasingly supported through automated compliance workflows powered by GST APIs.

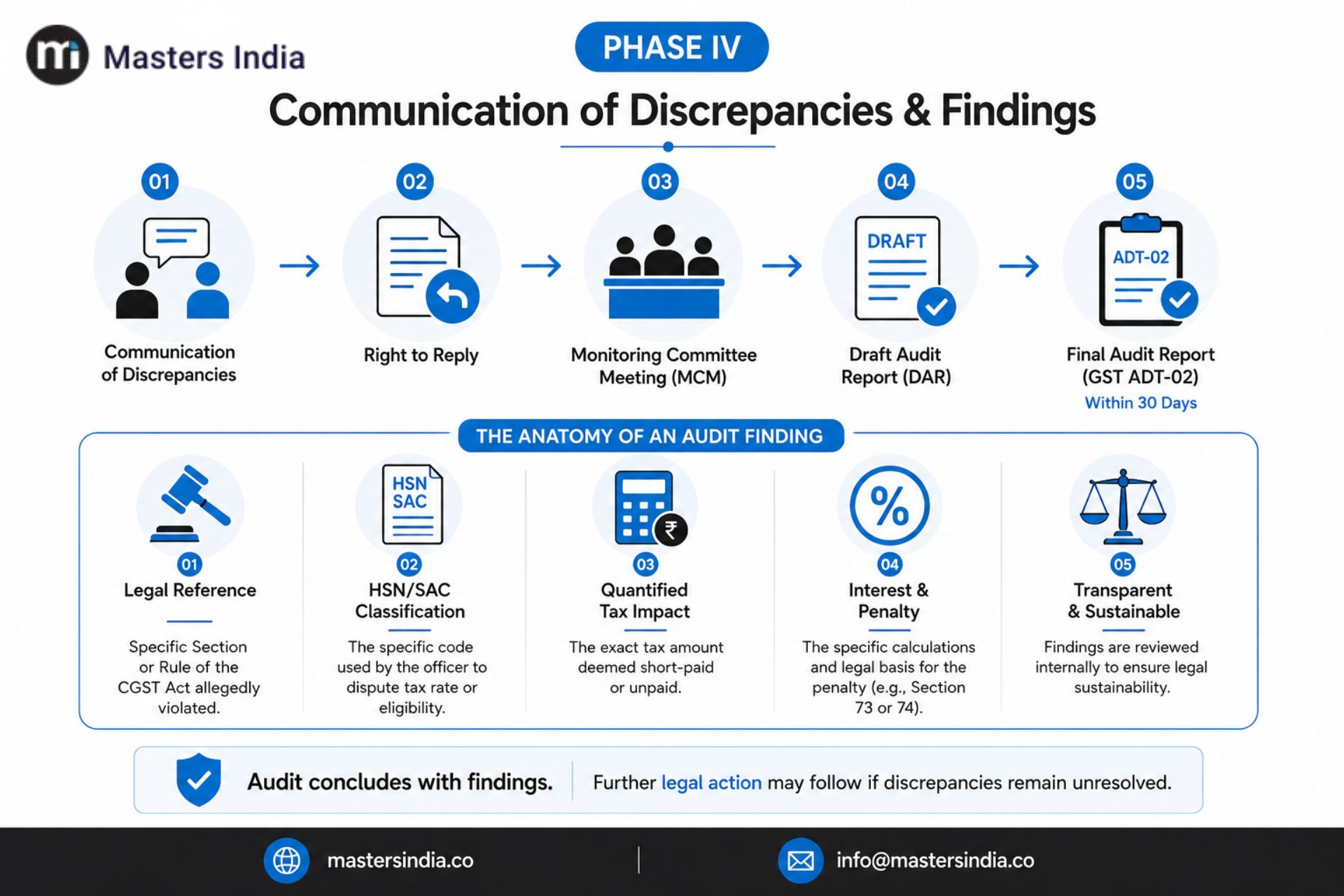

Phase IV: Communication of discrepancies and findings (form GST ADT-02)

Transparency is enforced through Step 8: Communication of Discrepancies. The auditor must provide the taxpayer with an opportunity to file a reply (the Right to Reply), which must be considered before the audit is finalised.

Crucially, professionals should be aware of Step 9: The Draft Audit Report (DAR). Before a report is issued to the taxpayer, observations are reviewed internally by a Monitoring Committee Meeting (MCM). This internal departmental check ensures that the findings are legally sustainable.

The final output is Form GST ADT-02, issued within thirty days of the audit's conclusion.

The Anatomy of an Audit Finding: A Professional Checklist. Each finding in the final report must contain:

-

Legal Reference: The specific Section or Rule of the CGST Act allegedly violated.

-

HSN/SAC Classification: The specific code used by the officer to dispute the tax rate or eligibility.

-

Quantified Tax Impact: The exact tax amount deemed short-paid or unpaid.

-

Interest & Penalty: The specific calculations and the legal basis for the penalty (e.g., Section 73 or 74).

While the audit ends with the findings report, it may trigger further legal actions if discrepancies remain unresolved.

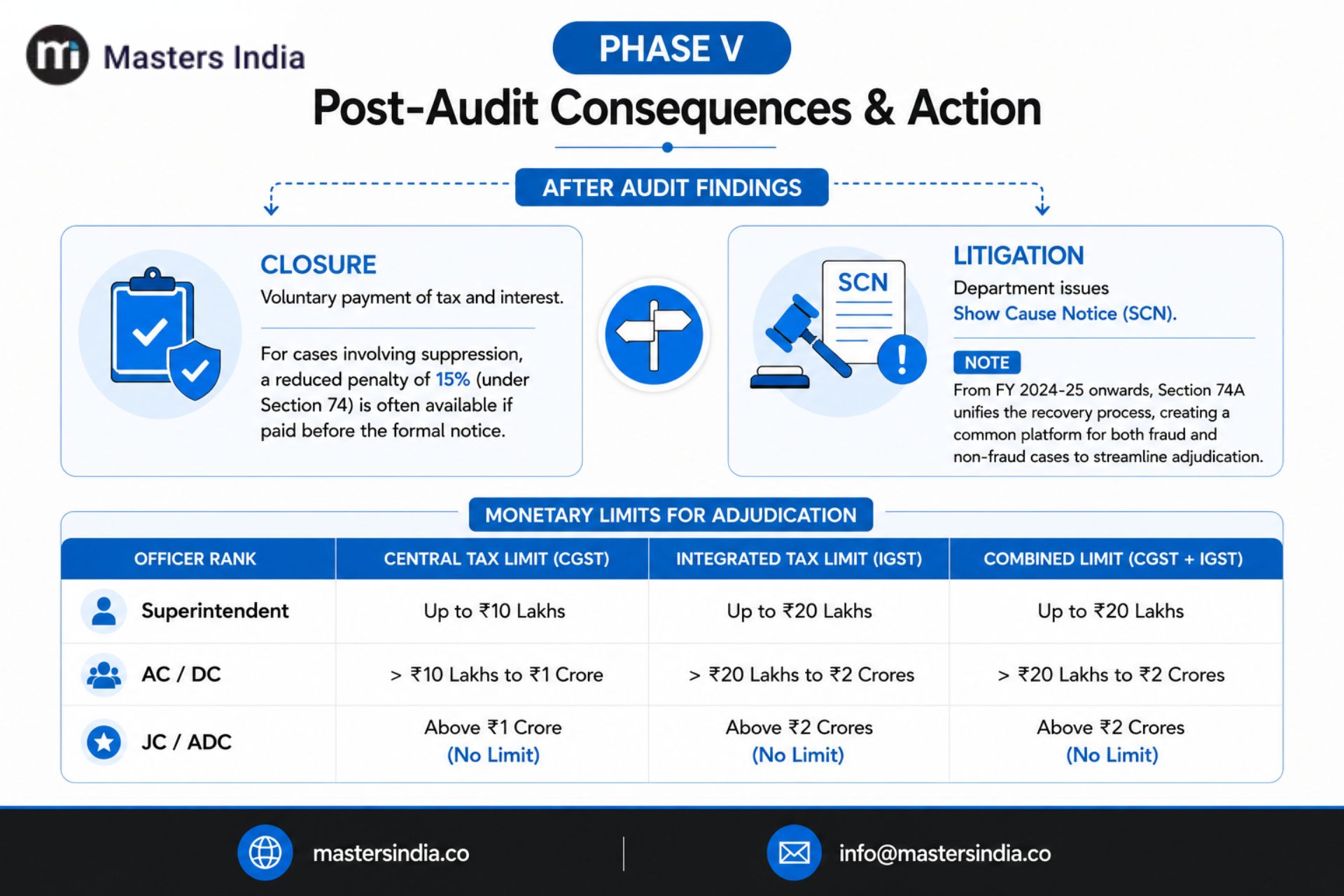

Phase V: Post-audit consequences and action

The conclusion of an audit leads to one of two paths:

-

Closure: Voluntary payment of tax and interest. For cases involving suppression, a reduced penalty of 15% (under Section 74) is often available if paid before the formal notice.

-

Litigation: If disputed, the department issues a Show Cause Notice (SCN). Note for Aspiring Professionals: For periods from FY 2024-25 onwards, Section 74A unifies the recovery process, creating a common platform for both fraud and non-fraud cases to streamline adjudication.

The authority to adjudicate depends on the monetary value of the tax in question:

Monetary Limits for Adjudication

| Officer Rank | Central Tax Limit (CGST) | Integrated Tax Limit (IGST) | Combined Limit (CGST + IGST) |

| Superintendent | Up to ₹10 Lakhs | Up to ₹20 Lakhs | Up to ₹20 Lakhs |

| AC / DC | > ₹10 Lakhs to ₹1 Crore | > ₹20 Lakhs to ₹2 Crores | > ₹20 Lakhs to ₹2 Crores |

| JC / ADC | Above ₹1 Crore (No Limit) | Above ₹2 Crores (No Limit) | Above ₹2 Crores (No Limit) |

Is your business prepared for a GST audit under Section 65?

A GST audit under Section 65 demonstrates that compliance is not a year-end exercise but an ongoing business discipline. The audit process is designed to verify the accuracy of tax payments, turnover reporting, Input Tax Credit (ITC) claims, and statutory records. For businesses managing multiple GST registrations, maintaining a GSTIN-wise Trial Balance, reconciling returns regularly, and keeping proper documentation for cross-charge transactions, job work activities, and ITC claims are critical for audit readiness.

By adopting a proactive compliance approach, businesses can reduce litigation risks, avoid unnecessary tax demands, and navigate audits with greater confidence. Masters India helps organizations strengthen GST compliance through automated reconciliation, GST software, e-invoicing solutions, GST APIs, and tax technology expertise.

Connect with our team to streamline GST processes, improve audit preparedness, and build a stronger compliance framework for your business.

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified