GST 2.0: Preparing for the Next Wave of Audits and Litigation

GST 2.0: Navigating Audits & Litigation with Data Analytics

The Goods and Services Tax (GST) regime in India has evolved significantly since its inception in 2017, and with the introduction of GST 2.0, businesses face an era of unprecedented digital scrutiny. The tax administration has matured into a sophisticated, analytics-driven system that leverages artificial intelligence, machine learning, and real-time data integration to identify compliance gaps and potential fraud. This transformation marks a decisive shift from traditional, manual audit processes to automated, predictive enforcement mechanisms that can detect discrepancies in real-time.

The Age of Analytics: GSTN's Data-Driven Revolution

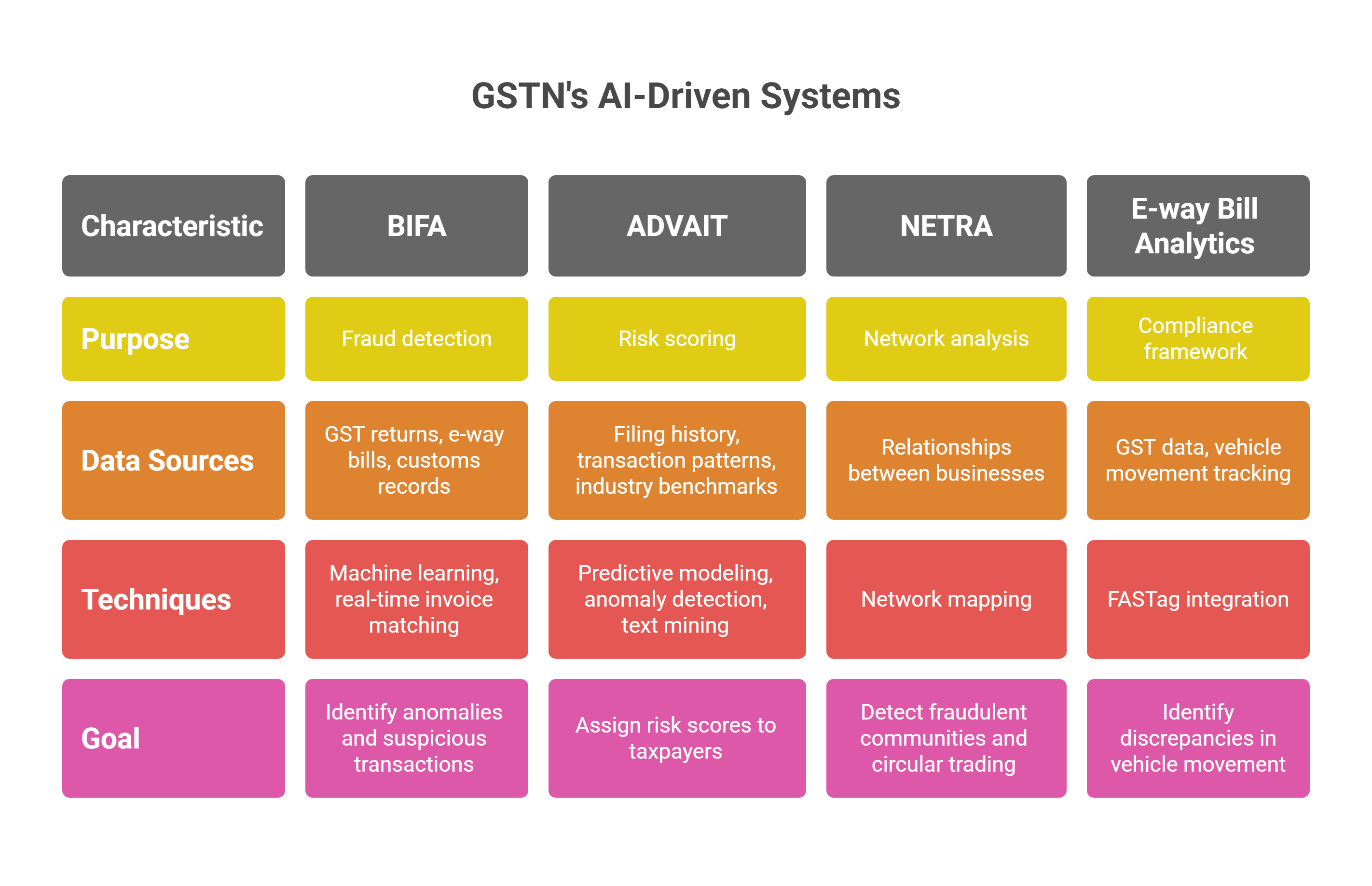

The Goods and Services Tax Network (GSTN) has deployed advanced analytics platforms that fundamentally transform how tax compliance is monitored and enforced. At the heart of this transformation are three powerful AI-driven systems that work in tandem to create a comprehensive surveillance network.

Business Intelligence and Fraud Analytics (BIFA) represents the most sophisticated fraud detection system within the GST ecosystem. Developed in collaboration with technology partners during the GST rollout, BIFA integrates data from GST returns, e-way bills, and customs records to identify anomalies and suspicious transaction patterns. The system employs machine learning algorithms to perform real-time invoice matching, where every input tax credit (ITC) claim by a buyer is automatically cross-referenced with the corresponding sales declaration by the seller. This automated verification process flags discrepancies such as over-claiming of ITC or fictitious invoice generation within minutes of filing.

Advanced Analytics in Indirect Taxation (ADVAIT) serves as CBIC's flagship analytics platform, launched in 2021 with ISO/IEC 20000-1:2018 certification. This system uses predictive modeling and anomaly detection to assign risk scores to taxpayers based on their filing history, transaction patterns, and industry benchmarks. ADVAIT's capabilities extend beyond simple pattern recognition to include text mining and comprehensive compliance dashboards that provide tax officers with actionable intelligence for targeted enforcement.

Networking Exploration Tools for Revenue Augmentation (NETRA) focuses specifically on network analysis to identify fraudulent communities and circular trading arrangements. This system maps relationships between businesses to detect coordinated tax evasion schemes, particularly those involving fake input tax credits and shell companies.

The effectiveness of these systems is evident in the enforcement statistics: during April-December 2023 alone, tax authorities detected 14,597 cases of GST evasion worth ₹18,000 crore using these analytical tools. States like Uttar Pradesh have issued over 6 lakh AI-triggered notices, resulting in additional revenue collection of ₹980 crore.

E-way Bill Analytics Integration further strengthens the compliance framework by connecting GST data with vehicle movement tracking. The system receives approximately 30 lakh daily transactions from over 800 toll plazas through FASTag integration. This allows authorities to identify discrepancies such as vehicle movements without corresponding e-way bills, cancelled e-way bills with continued vehicle movement, and suspicious circular trading patterns.

Common Audit Triggers: The Top 5 Risk Areas

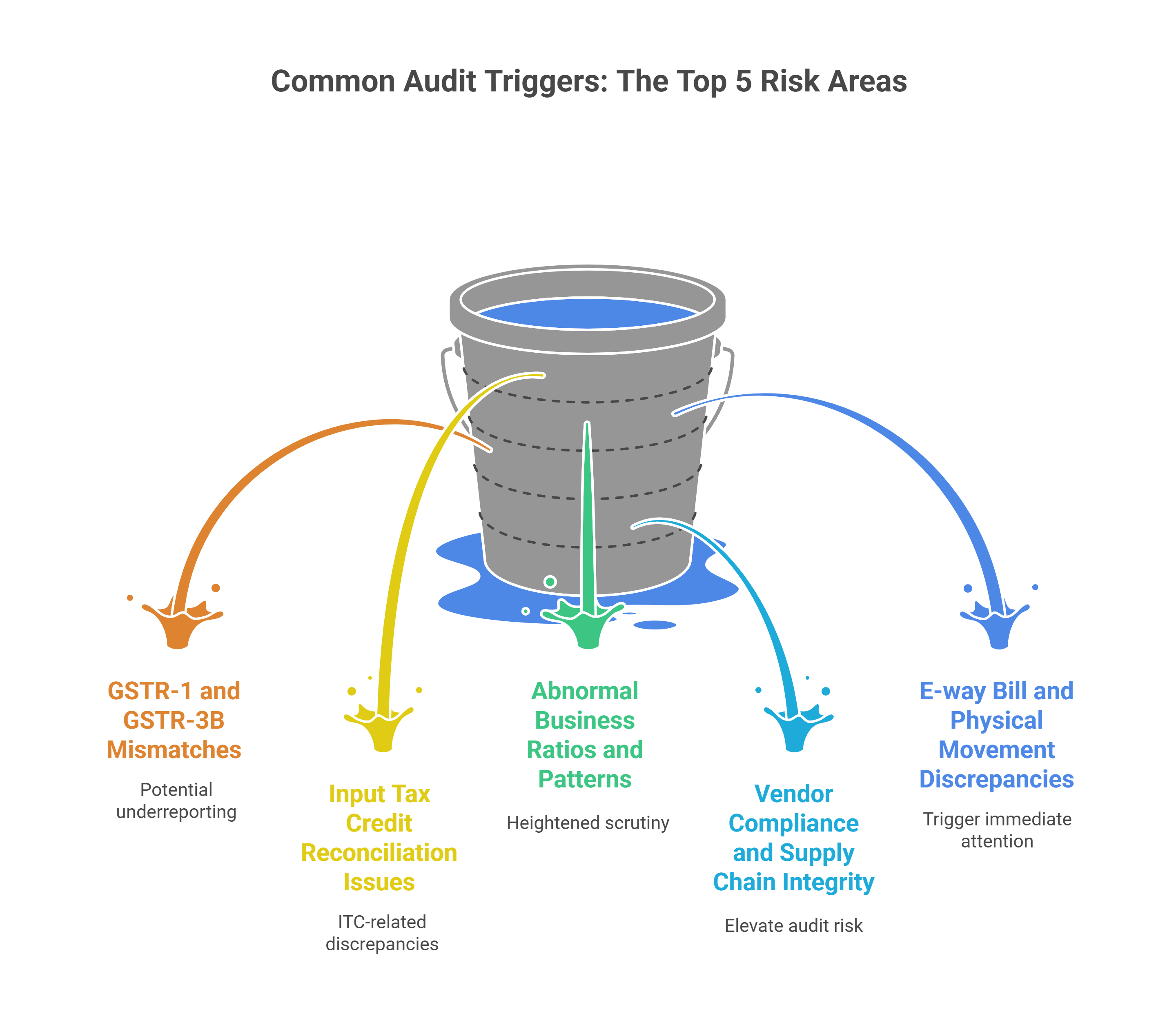

Modern GST audits are no longer random exercises but targeted operations driven by sophisticated risk algorithms. Understanding these trigger points is crucial for businesses to proactively address compliance gaps before they escalate into formal proceedings.

1. GSTR-1 and GSTR-3B Mismatches

The most prevalent audit trigger involves discrepancies between GSTR-1 (outward supplies) and GSTR-3B (summary return with tax payment). The GST system automatically flags cases where GSTR-1 shows higher tax liability than GSTR-3B, indicating potential underreporting. Under Rule 88C, businesses receive automated intimations in Form DRC-01B when such mismatches exceed specified thresholds, requiring explanation or payment within seven days. Failure to respond can result in the blocking of GSTR-1 filing capability and the initiation of formal demand proceedings under Sections 73 or 74.

2. Input Tax Credit Reconciliation Issues

ITC-related discrepancies represent the largest source of GST litigation. The system continuously monitors alignment between ITC claimed in GSTR-3B and credits available in GSTR-2A/2B. Common triggers include claiming ITC before supplier filing, availing credit on ineligible purchases under Section 17(5), and failure to reverse ITC when supplier payments exceed 180 days. The implementation of Invoice Management System (IMS) has introduced additional system-based controls that automatically restrict ITC availability based on real-time vendor compliance status.

3. Abnormal Business Ratios and Patterns

AI algorithms continuously benchmark taxpayer performance against industry peers and historical patterns. Businesses exhibiting abnormal ITC-to-turnover ratios, excessive refund claims without corresponding export activity, or sudden spikes in turnover without proportional increase in operational indicators face heightened scrutiny. The system also flags taxpayers with unusual filing patterns, such as consistent nil returns despite active e-way bill generation or significant amendments to previously filed returns.

4. Vendor Compliance and Supply Chain Integrity

The interconnected nature of GST requires businesses to monitor their entire supply chain compliance. Transactions with high-risk vendors, newly registered entities with suspicious profiles, or suppliers with poor filing history automatically elevate audit risk. The system tracks supplier networks to identify potential circular trading arrangements and fake invoice chains that could compromise ITC claims.

5. E-way Bill and Physical Movement Discrepancies

Integration with transportation tracking systems has created new audit triggers related to goods movement. Discrepancies between e-way bill declarations and actual vehicle movements, recycling of e-way bill numbers, generation of multiple e-way bills for the same consignment, or movement of high-value goods by unregistered persons all trigger immediate attention. The system's ability to cross-reference HSN codes, vehicle capacities, and route analysis helps identify under-invoicing and tax evasion schemes.

Building a 'Litigation-Proof' System: Best Practices for Robust Compliance

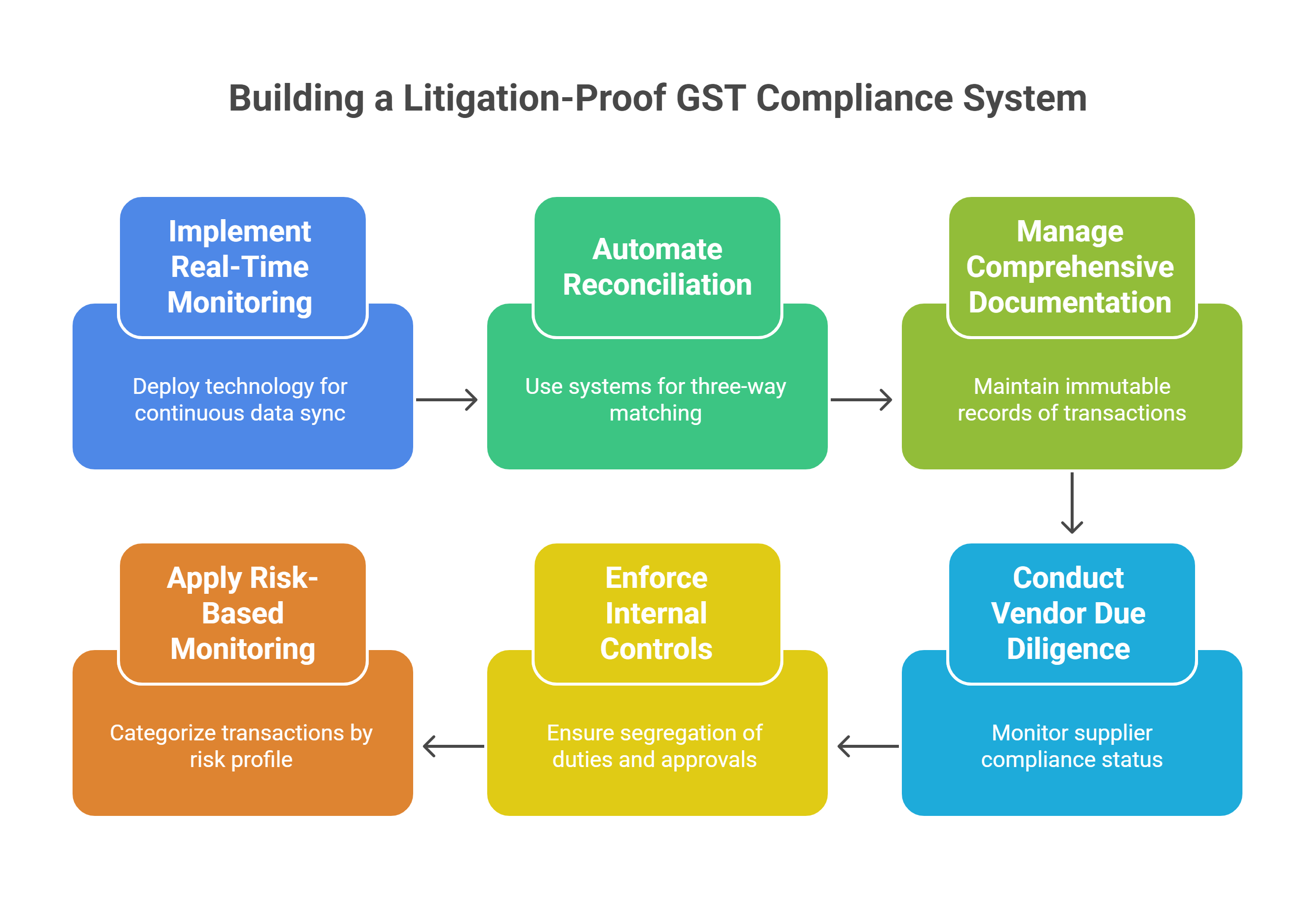

Creating a litigation-resistant GST compliance framework requires a comprehensive approach that combines technology, processes, and governance structures. The goal is to build systems that not only ensure compliance but also create defensible audit trails that can withstand regulatory scrutiny.

Automated Reconciliation and Real-Time Monitoring

Modern compliance frameworks must move beyond monthly reconciliation cycles to implement real-time monitoring systems. This involves deploying technology solutions that continuously sync data between ERP systems, GST portals, and banking platforms. Automated three-way matching between purchase orders, goods receipt notes, and vendor invoices should be implemented with exception handling workflows for discrepancies. Real-time GSTR-2A/2B monitoring ensures ITC claims are validated against supplier filings before return submission.

Comprehensive Documentation and Audit Trail Management

Every transaction must be supported by a complete audit trail that includes electronic timestamps, approval workflows, and change logs. Digital invoice management systems should maintain immutable records of all document versions, amendments, and supporting evidence. The audit trail should capture not just the final transaction but also the decision-making process, approval hierarchies, and supporting documentation that justifies each GST treatment.

Vendor Master Management and Due Diligence

Robust vendor management extends beyond basic KYC to include continuous monitoring of supplier compliance status. This involves real-time verification of GSTIN validity, monitoring of supplier filing patterns, and assessment of vendor risk scores based on compliance history. Automated alerts should trigger when vendors miss filing deadlines, face enforcement actions, or exhibit suspicious transaction patterns that could jeopardize ITC claims.

Advanced Internal Controls and Segregation of Duties

Internal control frameworks must include clear segregation of duties, maker-checker approvals for high-value transactions, and regular exception reporting. Role-based access controls should ensure that individuals cannot both create and approve transactions without independent verification. Regular internal audits should test the effectiveness of these controls and identify potential weaknesses before they become compliance issues.

Risk-Based Transaction Monitoring

Implementing risk-based monitoring involves categorizing transactions based on their audit risk profile and applying appropriate controls. High-risk transactions, such as those involving new vendors, unusual HSN codes, or significant value variations, should trigger enhanced verification procedures. Automated risk scoring algorithms should continuously assess transaction patterns and flag anomalies for manual review.

Managing Legacy Issues: Strategic Approaches to Past Disputes

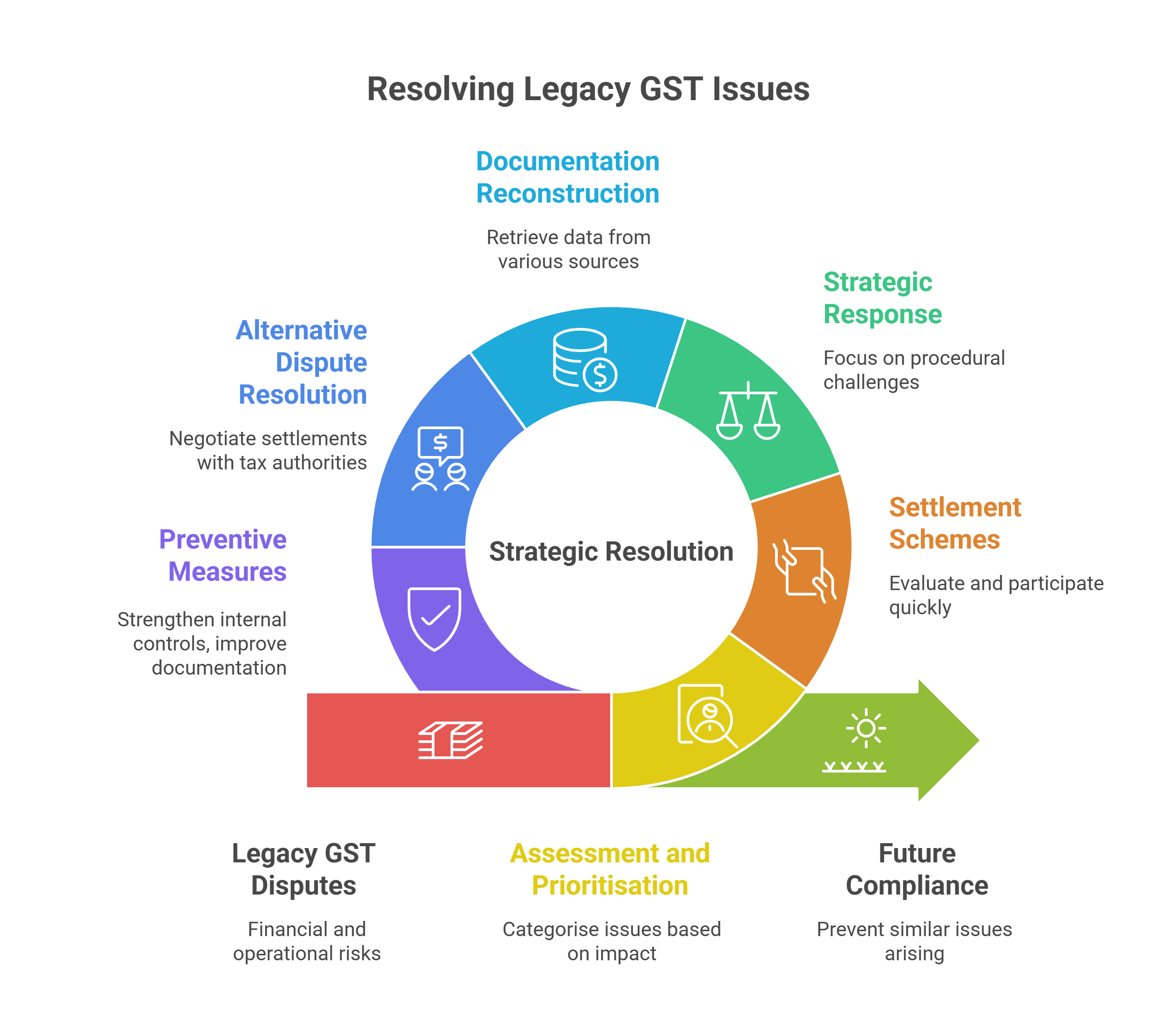

Legacy GST issues present unique challenges that require careful strategic planning and proactive resolution approaches. The accumulation of past disputes, pending notices, and unresolved assessments can create significant financial and operational risks that must be systematically addressed.

Assessment and Prioritisation of Legacy Matters

The first step in managing legacy issues involves conducting a comprehensive audit of all pending matters, outstanding notices, and potential disputes. This assessment should categorize issues based on their financial impact, legal merit, and likelihood of successful resolution. High-value disputes with strong factual and legal foundations may warrant vigorous defines, while cases with weak positions might be candidates for voluntary disclosure or settlement schemes.

Leveraging Settlement Schemes and Amnesty Programs

The government has periodically introduced settlement schemes similar to the Sabka Vishwas Legacy Dispute Resolution Scheme that provided relief for pre-GST indirect tax disputes. These schemes typically offer significant reductions in penalty and interest components in exchange for voluntary disclosure and payment of core tax liability. Businesses should maintain readiness to quickly evaluate and participate in such schemes when announced, as they often have limited time windows for participation.

Strategic Response to Show Cause Notices

When facing show cause notices for legacy issues, the response strategy should focus on procedural challenges before addressing substantive merits. This includes verifying proper jurisdiction of the issuing officer, ensuring compliance with time limitations under Sections 73 and 74, and confirming adherence to pre-notice consultation requirements where applicable. Procedural defects can often invalidate notices entirely, avoiding the need to defend on the merits.

Documentation Reconstruction and Evidence Preservation

Legacy disputes often involve challenges in locating and organising historical records. Businesses should implement systematic documentation reconstruction processes that involve retrieving data from ERP systems, bank records, and third-party sources. Electronic records should be preserved in formats that maintain their evidentiary value, including metadata and digital signatures where available.

Alternative Dispute Resolution and Negotiated Settlements

For complex legacy matters, exploring alternative dispute resolution mechanisms can provide faster and more cost-effective outcomes than traditional litigation. This may involve direct negotiations with tax authorities, mediation through industry associations, or structured settlement agreements that address multiple related issues comprehensively.

Preventive Measures for Future Compliance

While addressing legacy issues, businesses must simultaneously implement measures to prevent similar issues from arising in the future. This includes strengthening internal controls, improving documentation practices, and establishing regular compliance monitoring systems that can identify and address potential issues before they become formal disputes.

Final Words:

The GST 2.0 era demands a fundamental shift in how businesses approach tax compliance and dispute management. The integration of artificial intelligence, real-time data analytics, and automated monitoring systems has created an environment where traditional reactive compliance approaches are no longer sufficient. Success in this new landscape requires proactive, technology-enabled compliance frameworks that anticipate and prevent issues rather than merely responding to them after they occur.

Businesses that invest in robust internal controls, comprehensive vendor management, and advanced reconciliation systems will find themselves better positioned to navigate the increasingly sophisticated audit environment. Simultaneously, those with legacy issues must adopt strategic approaches that balance aggressive defence of strong positions with pragmatic resolution of weaker cases. The key to thriving in the GST 2.0 environment lies in building systems that are not just compliant but genuinely litigation-proof, capable of withstanding the most sophisticated analytical scrutiny while maintaining operational efficiency and business agility.

GST Bill Online | Check Invoice Number Online | E Invoicing Software | GST Return Filing Software | Ewaybill Api

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified