Finalising accounts from a GST perspective is a critical exercise that extends beyond traditional accounting and auditing. It necessitates a thorough review of financial statements, year-end adjustment entries, and a series of reconciliations to ensure seamless alignment between the books of accounts and GST returns. Key activities include verifying disclosures of GST-related contingent liabilities in the notes to accounts, scrutinising Directors' and Audit reports for GST implications, and ensuring compliance with CARO reporting for statutory dues. Special attention must be paid to the GST impact of year-end adjustments, such as provisions and accruals. The process is anchored by comprehensive reconciliations, primarily between revenue and ITC reported in books versus that declared in GSTR-1, GSTR-3B, and GSTR-9. Advanced analyses, such as evaluating branch-level profit margins and implementing cross-charge mechanisms, are vital for multi-locational entities to ensure accurate valuation and prevent disputes.

Let’s dive deep into the key considerations for finalising accounts from a GST perspective.

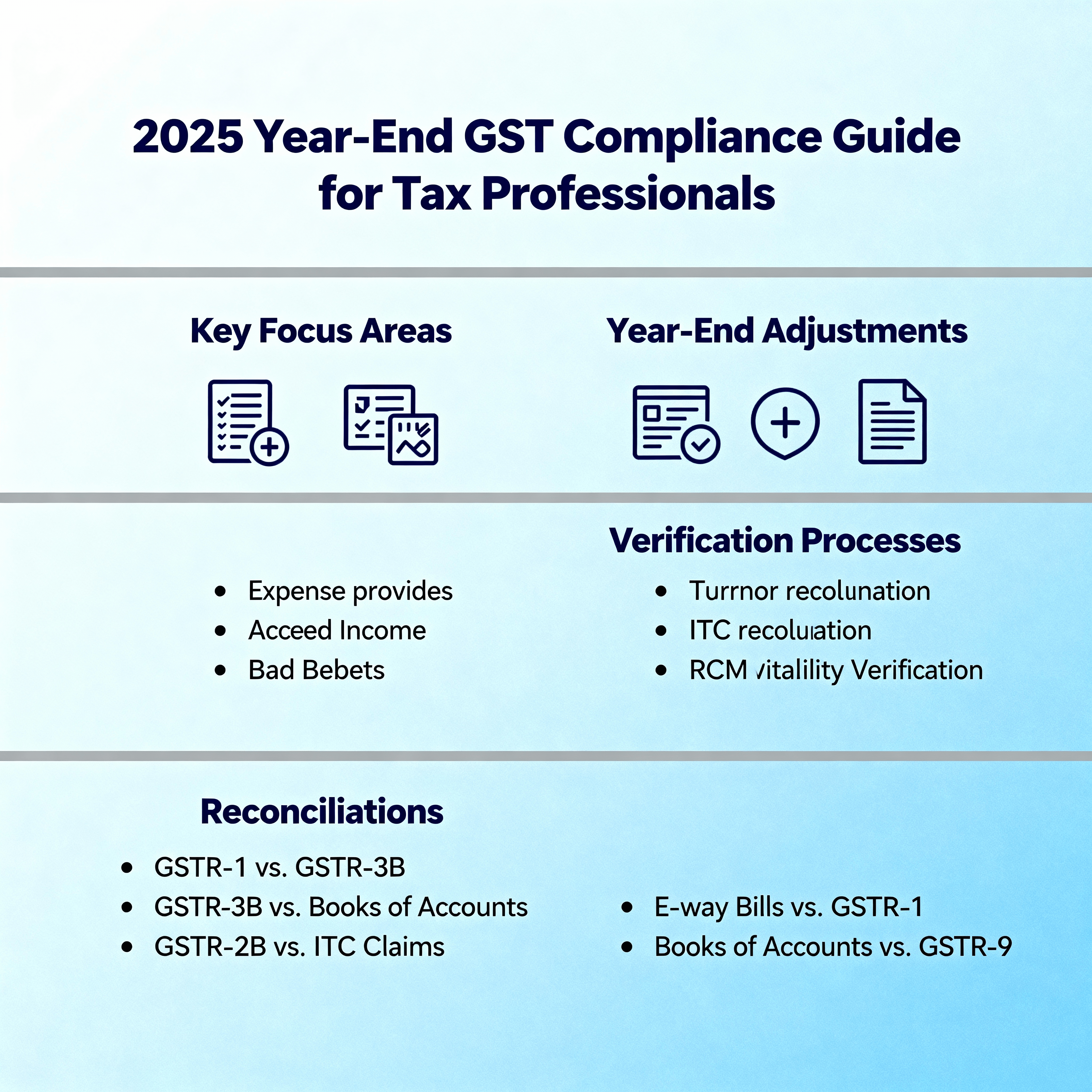

1. Disclosure and Review of Audited Financial Statements for GST

The audited financial statements are not just a reflection of financial health but also a testament to statutory compliance. A review from a GST lens is crucial.

-

Directors’ Report: This report may contain information regarding any significant changes in business operations, litigations, or risks, which could have GST implications. Any comments on the company's internal financial controls may also indicate the robustness of its GST compliance processes.

-

Audit Report: The auditor's opinion is paramount. Any qualifications, emphasis of matter, or other matters paragraphs related to non-payment of GST, incorrect availment of ITC, or pending litigations must be carefully evaluated for their financial impact and disclosure requirements.

-

Notes to Accounts: This section should contain specific and transparent disclosures related to GST:

-

Contingent Liabilities: As per Ind AS 37 / AS 29, all potential liabilities arising from GST demands, show-cause notices, and ongoing litigation must be disclosed. This includes a brief description of the dispute, the amount involved, and the management's assessment of the financial outflow.

-

Accounting Policies: The policy for recognition of revenue, accounting for taxes (GST), and availment and utilisation of Input Tax Credit should be clearly stated.

-

ITC Receivable/Payable: The balance sheet should correctly reflect any GST receivable (ITC) or payable balances at the year-end.

-

Internal Audit Report: These reports often highlight procedural gaps, non-compliances, or control weaknesses in the GST return filing, reconciliation, and payment process. These findings are invaluable for taking corrective action before the statutory audit and finalisation.

-

Reporting under CARO, 2020: Clause (vii) of the Companies (Auditor's Report) Order, 2020, requires the auditor to comment on whether the company is regular in depositing undisputed statutory dues, including GST. It also requires the reporting of details of disputed GST dues (amount and the forum where the dispute is pending). This makes accurate computation and timely payment of GST critical.

2. Year-end Adjustment Entries and Their Impact on GST

Many accounting entries passed during finalisation have direct or indirect GST implications. It is essential to analyse them to ensure correct GST treatment.

| Year-End Adjustment Entry | GST Implication and Action Required |

| Provision for Expenses | ITC cannot be availed on provisions as the tax invoice is not available, and conditions under Section 16 of the CGST Act, 2017 are not met. ITC can be claimed only in the period the invoice is received and accounted for. |

| Accrued Income | GST liability may arise if the "time of supply" under Section 12 or 13 of the CGST Act has been triggered, even if the invoice is raised later. For instance, if services are completed by the year-end, GST liability accrues. |

| Bad Debts Written Off | Writing off bad debts in the books of accounts does not allow the supplier to reduce their output tax liability. The tax once paid is final. |

| Reversal of ITC for Non-payment | As per Rule 37 of the CGST Rules, 2017 read with Section 16, if payment is not made to the supplier within 180 days, the corresponding ITC must be reversed with interest. This should be checked for all creditors with outstanding balances of more than 180 days. |

| Free Samples, Gifts, and Goods Destroyed | As per Section 17(5) of the CGST Act, ITC availed on goods distributed as free samples, gifts, or those lost, stolen, or destroyed must be reversed. This requires careful tracking and reversal entries. |

| Inter-branch Stock Transfers | Stock transfers between branches in different states are treated as taxable supplies under GST. Ensure that such transfers are invoiced with the correct GST and their valuation is done as per Rule 28 of the CGST Rules. |

3. Verification of Returns Filed vs. Financial Statements

This is the cornerstone of GST finalisation and forms the basis for filing the Annual Return (GSTR-9) and the Reconciliation Statement (GSTR-9C).

-

Turnover Reconciliation: The total turnover as per the audited financial statements must be reconciled with the turnover declared in GSTR-1 and GSTR-3B. This involves:

-

Adding non-GST income (e.g., interest) and other incomes not part of the P&L to arrive at the book turnover.

-

Adjusting for supplies declared in the next financial year or supplies of the previous year declared in the current year.

-

The reconciled value must match the figures reported in Table 5 and Table 10/11 of GSTR-9.

-

ITC Reconciliation: A three-way reconciliation of ITC is critical:

-

ITC as per Books of Accounts: Total eligible ITC recorded in the purchase register/expense ledgers.

-

ITC as per GSTR-3B: Total ITC availed in the monthly returns.

-

ITC as per GSTR-2B: The auto-populated statement of eligible ITC.

-

Any differences must be investigated. Discrepancies may arise due to ineligible ITC claimed, ITC missed, or supplier non-compliance. This reconciliation is crucial for Tables 6, 7, 8, and 13 of GSTR-9.

-

Reverse Charge Mechanism (RCM) Liability: The expenses liable to RCM in the books (e.g., legal fees, GTA services) should be reconciled with the RCM liability paid in cash through GSTR-3B and the corresponding ITC availed. Scrutiny parameters often focus on verifying that the tax paid in cash is not less than the RCM liability declared.

4. Significance of Gross Profit (GP) / Net Profit (NP) Rates Across Branches

For businesses with multiple GST registrations for branches in different states, analysing GP/NP rates is a vital analytical tool.

-

Valuation Issues: Significant variations in GP rates between branches could indicate potential undervaluation of inter-state stock transfers. Tax authorities may scrutinise such variations, alleging that goods were transferred at a lower price to a branch in a state with accumulated ITC to shift the tax burden.

-

Transfer Pricing: Consistent losses at one branch and high profits at another could trigger questions about the arm's length nature of inter-branch transactions and the allocation of common costs (cross-charge).

5. Cross Charge

When a Head Office (HO) or a central office incurs common expenses on behalf of branches located in different states, the portion of these expenses attributable to each branch must be cross-charged via a tax invoice.

-

Mechanism: The HO must issue a tax invoice to the respective branches for the support services or common functions performed.

-

Valuation: As per Rule 28 of the CGST Rules, the valuation can be the open market value. However, a proviso allows the invoice value to be deemed the open market value if the recipient branch is eligible for full ITC.

-

Importance: Failure to implement a cross-charge mechanism can lead to the denial of ITC on common expenses at the HO and allegations of non-payment of tax on services provided to branches.

6. Ratio Analysis Relevant to GST

Ratio analysis can serve as a quick health check on GST compliance.

-

ITC to Total Expenses Ratio: (Total ITC Availed / Total Indirect Expenses) can help identify if ITC is being claimed on all eligible expenses or if there is any leakage.

-

RCM Liability to RCM Expenses: (RCM Liability Paid / Total RCM-attracting Expenses) should be close to the applicable tax rate, indicating full compliance.

-

Output Tax to Taxable Turnover: This ratio should align with the primary GST rates applicable to the business. Deviations may indicate misclassification of supplies or incorrect tax payments.

7. Relevant Reconciliations to be Prepared under GST

A comprehensive set of reconciliations is essential for robust GST compliance and accurate annual filings.

| Reconciliation Statement | Purpose and Significance |

| GSTR-1 vs. GSTR-3B | To ensure that the tax liability declared on outward supplies in GSTR-1 matches the tax paid in GSTR-3B for each tax period. This is a primary check during departmental audits. |

| GSTR-3B vs. Books of Accounts | To reconcile both outward tax liability and ITC availed between the books and the returns filed. This forms the basis for GSTR-9C. |

| GSTR-2B vs. ITC in GSTR-3B | To ensure that ITC is claimed only on supplies reported by vendors, as mandated by Section 16(2)(aa). This helps identify non-compliant vendors and minimize ITC disputes. |

| E-way Bills vs. GSTR-1 | To reconcile the value of goods moved as per the e-way bill portal with the outward supplies declared in GSTR-1. Discrepancies may indicate suppressed turnover. |

| Books of Accounts vs. GSTR-9 | This is the final, comprehensive reconciliation to ensure that all transactions for the financial year are correctly reported in the annual return. |

📚 Source

-

Instruction No. 02/2022-GST

-

FAQ on GSTR 9/9C for the FY 2024- 25

-

NOTIFICATION No. 13/2025-Central Tax

-

Circular No. 183/15/2022-GST

-

Circular No. 193/05/2023-GST

Indian Customs Port Code List pdf | Need of GST in India | Negotiable Instruments Classification | Powers of GST Officers | LLP Balance Sheet Format India

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified