Why Does This Subject Matter?

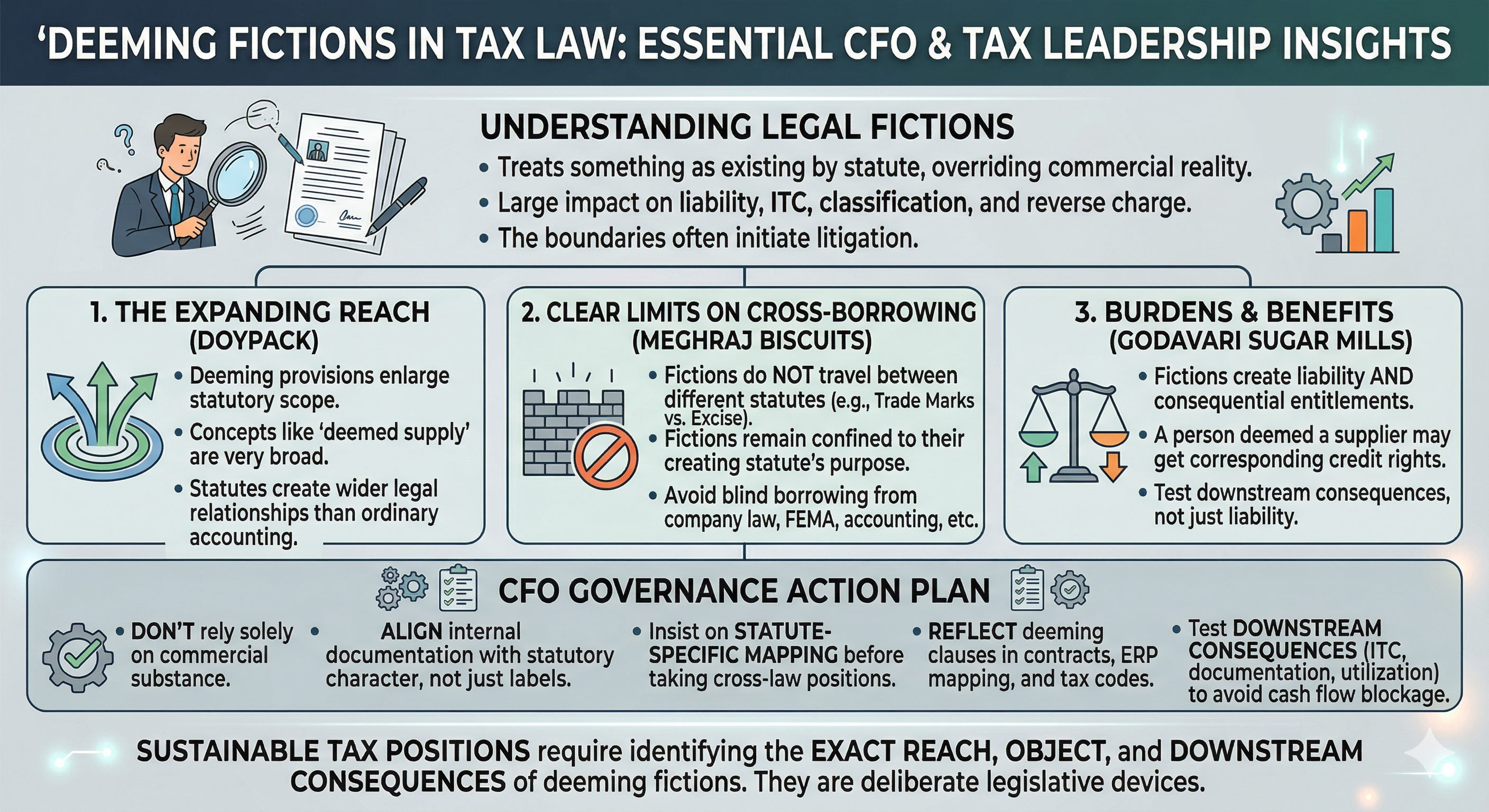

Modern tax statutes often tax a person, transaction, or status not because it exists in ordinary commercial reality, but because the statute says it shall be "deemed" to exist. That is the essence of a legal fiction. When a person is deemed to be something, the law requires him to be treated as such even though, in reality, he may not be so. A deeming provision is intended to enlarge the meaning of a word and to bring within the statute matters which may otherwise fall outside its natural scope.

For CFOs and VP Taxation, this is not an academic issue. It directly affects tax incidence, credit entitlement, classification, reverse charge, brand-related benefits, and the legal limits of departmental interpretation. A deeming fiction can enlarge a charging or machinery provision. But it cannot be extended beyond the purpose for which the legislature created it. That boundary is where most litigation begins.

The Interpretative Foundation of Deeming Provisions

A Deeming Clause Enlarges the Statutory Field

In Doypack Systems (P) Ltd. v. Union of India, the Supreme Court explained that a deeming provision is meant to enlarge the meaning of a particular word or include matters which may or may not otherwise fall within the main provision. The Court also treated expressions such as "in relation to", "pertaining to", and "arising out of" as expressions of wide amplitude. They are words of expansion, not contraction.

But the Fiction Must Still Remain Within Its Legislative Purpose

While construing a legal fiction, the court must assume all facts necessary for the fiction to operate. At the same time, the fiction cannot be pushed beyond the statutory object that created it. That discipline becomes crucial in fiscal disputes where taxpayers and the Department both attempt to draw wider consequences from a deeming clause.

Case Law Analysis

1. Doypack Systems (P) Ltd. v. Union of India

1988 (36) ELT 201 (SC)

Core Principle

The Supreme Court held that a deeming provision is an enlarging provision. It broadens the reach of the statutory expression. The Court further held that expressions like "in relation to" and "pertaining to" are words of the widest amplitude. They may carry both direct and indirect significance, depending on context.

What the Court Emphasized

The Court observed that the concerned section was an expanding section that introduced a deeming provision using inclusive language. It used expressions such as "all other rights and interests", "ownership", "possession", "power", and "control" in relation to the undertaking. On that basis, the Court adopted an expansive construction and held that the shares also vested in the Central Government.

CFO Takeaway

For tax leadership, Doypack is a reminder that where GST law uses words like "in relation to", "deemed supply", "deemed distinct persons", "includes", or "treated as", the provision will often be construed broadly. A narrow commercial reading may fail if the statute expressly creates a wider legal relationship. That has immediate relevance in disputes involving cross-charges, related party transactions, branch transfers, input tax credit nexus, and composite valuation questions.

Governance Lesson

Tax teams should not rely only on commercial substance. They must also test whether the statute creates a legal fiction that displaces ordinary accounting or business understanding. Where such fiction exists, internal documentation should align with the statutory character, not merely the commercial label.

2. Meghraj Biscuits Industries Ltd. v. Commissioner of Central Excise, U.P.

2007 (210) ELT 161 (SC)

Core Principle

The Supreme Court dealt with SSI exemption and the use of another person's brand name. The assessee relied on retrospective trade mark registration. The Court held that the deeming fiction under the Trade Marks law could not automatically be imported into Excise law. The fiction of deemed public user or deemed equivalence remained confined to the statute that created it. It did not, by itself, rewrite the conditions of the exemption notification under Central Excise.

Why This Ruling Is Important

This judgment lays down a sharp limit on deeming provisions. A fiction created under one enactment does not necessarily travel into another enactment. The Court made it clear that the object of the SSI exemption was to benefit industries which did not enjoy the advantage of a brand name. Therefore, trade mark doctrines could not be used to defeat the fiscal condition attached to the exemption.

CFO Takeaway

This principle is directly relevant in GST. Tax positions often attempt to borrow concepts from company law, FEMA, customs, SEZ law, trade mark law, or accounting standards. Meghraj warns that such cross-statute borrowing has limits. If a GST consequence is governed by a specific deeming provision or condition, relief cannot be claimed merely because another statute deems a different legal position.

Practical Framework for Tax Leadership

This reasoning matters where businesses argue that a treatment accepted under another law should automatically govern GST. The correct enquiry is always:

- What is the exact fiction created?

- What is its statutory object?

- Does the GST enactment expressly adopt that fiction? If not, the fiction may remain confined to its parent statute.

Risk Management Lesson

Before taking a tax position based on a legal status created elsewhere, CFOs should insist on a statute-specific mapping exercise. The tax team should identify whether the foreign concept is merely persuasive or legally incorporated. That discipline reduces exposure in exemption, valuation, and eligibility disputes.

3. Commissioner of Central Excise & Customs, Belgaum v. Godavari Sugar Mills Ltd.

2015 (40) STR 1063 (Kar.)

Core Principle

The Karnataka High Court considered the effect of the deeming fiction under Section 68(2) of the Finance Act, 1994. By virtue of that provision, the assessee was treated as the provider of output service for Goods Transport Service under reverse charge. On that footing, the Court held that there was no bar to taking CENVAT credit of service tax paid on such services and re-utilising the same for payment of service tax under Rule 3(4)(e) of the CENVAT Credit Rules, 2004.

Why This Matters

This decision shows the constructive side of deeming provisions. A deeming fiction does not only create liability. It may also carry consequential entitlements where the statutory scheme so permits. If the law deems the assessee to be the service provider, then the corresponding credit mechanics may also operate in its favour.

CFO Takeaway

For CFOs and VP Taxation, this is highly relevant to reverse charge design, input tax credit architecture, and compliance automation. Where the statute deems the recipient to occupy the place of supplier or service provider for tax payment purposes, one must examine whether the law also confers connected credit rights, procedural rights, or documentary consequences. A fiction should be applied fully for the purpose for which it is created.

Operational Lesson

Tax teams should not stop at the liability clause. They should also test the downstream consequences of the fiction. This includes:

- Eligibility of credit

- Manner of utilisation

- Invoice and documentation trail

- Return disclosure

- Audit defence

A half-read deeming provision often causes avoidable cash-flow blockage.

What These Cases Mean for GST Leadership Today

1. Deeming Provisions Are Powerful

They can alter legal character. They can override commercial reality. They can expand liability and compliance obligations. Doypack strongly supports a broad reading where the statutory language is expansive.

2. Their Expansion Is Not Limitless

A legal fiction must remain tethered to the enactment and purpose that created it. Meghraj Biscuits is the clearest authority on this restraint.

3. The Fiction Can Carry Both Burden and Benefit

If the statute deems a person into a tax position, the consequential compliance and credit results must also be examined. Godavari Sugar Mills illustrates this point.

4. Drafting, Documentation, and Litigation Strategy Must Reflect the Fiction

Tax governance cannot be based only on commercial intent. It must be based on statutory character. Legal review of contracts, ERP mapping, tax codes, and note-to-file positions should expressly deal with applicable deeming clauses.

Concluding Note for CFOs and VP Taxation

In indirect tax law, a deeming provision is never ornamental. It is a deliberate legislative device. Sometimes it expands the tax net. Sometimes it creates compliance symmetry. Sometimes it prevents importation of concepts from another statute. The real task for tax leadership is to identify the exact reach of the fiction, its statutory object, and its downstream consequences. That is where sustainable tax positions are built.

input tax credit | deemed supply under schedule 1 | gst on tdr under rcm | e commerce operator in gst | how to change mobile number in gst eway bill portal

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified