Key Learning for Sections 73, 74 and 74A of CGST Act, 2017

-

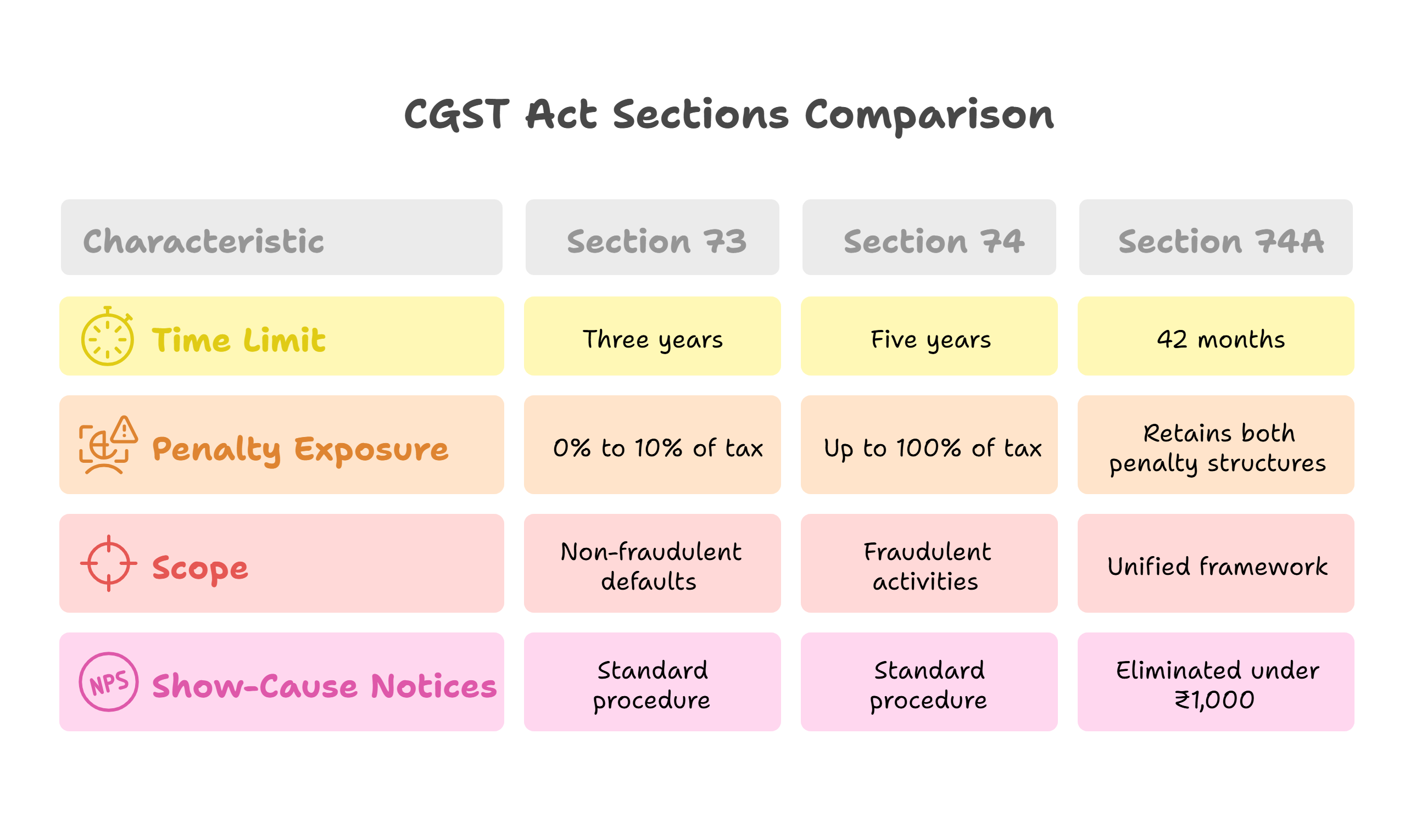

Section 73 empowers tax authorities to recover unpaid tax, excess ITC or erroneous refunds arising from any cause other than fraud within three years, and it caps penalty exposure at 0 – 10 % of the tax when the assessee pays promptly.

-

Section 74 tackles the same defaults caused by fraud, wilful mis-statement or suppression, lengthening the limitation to five years and escalating penalties up to an amount equal to the tax (with 15 %, 25 % and 50 % relief bands for early payment).

-

Section 74A—introduced for liabilities from FY 2024-25 onward—folds both regimes into a single 42-month notice period, keeps the lower penalty matrix for non-fraud cases and the higher one for fraud, and eliminates show-cause notices altogether where the differential tax is under ₹1,000, streamlining adjudication.

Comparison between Sections 73 vs 74 vs 74A (CGST Act, 2017)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Five take-aways for CFOs & Finance Leads 📌

-

Single yard-stick from FY 2024-25

Officers will issue all demand notices—fraud or not—under one section (74A). The earlier need to defend “intent” at SCN stage fades; the focus shifts to rebutting fraud allegations during adjudication. -

Uniform yet tighter limitation

The 42-month SCN clock under Section 74A is longer than Section 73 but shorter than Section 74, giving businesses a predictable “4½-year” exposure window. Plan record-retention and reconciliations accordingly. -

Extra breathing space for quick closures

The “reduced-penalty” window doubles from 30 days to 60 days (pre-SCN and post-SCN) under Section 74A—use it to cut litigation costs where the differential tax is not in dispute. -

Low-value disputes disappear

Demands below ₹1,000 will not generate an SCN under Section 74A, sparing finance teams from immaterial battles. -

Penalty matrix still hinges on fraud

Even under Section 74A, proving the absence of fraud keeps the penalty at 10 %; failure bumps it to the full tax amount. Robust documentation and timely corrections remain the best fraud-defence strategy.

Practical Tip:

Update your internal GST compliance SOPs to reference Section 74A for any differential liability arising in FY 2024-25 onward. Keep separate workflows for legacy years (till 2023-24) that may still attract SCNs under Section 73 or 74.

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified