Blocked Credit Under GST: Section 17(5) Explained

Introduction to blocked credit under GST

The GST regime, established under the CGST Act, 2017, functions on the backbone of Input Tax Credit (ITC) to mitigate tax leakage and eliminate the cascading effect of taxation, which is why enterprises increasingly integrate GST APIs into their compliance and reconciliation workflows. As per Section 2(63), ITC is the credit of "input tax," while Section 2(62) defines "input tax" as the tax charged on any supply of goods or services, including those under the Reverse Charge Mechanism (RCM) and imports.

To maintain statutory compliance and avoid litigation, a strategist must distinguish between three procurement categories:

-

Input [Section 2(59)]: Goods used or intended for business use, excluding capital goods.

-

Input Service [Section 2(60)]: Services used or intended for business use.

-

Capital Goods [Section 2(19)]: Goods whose value is capitalized in the books of account of the person claiming the ITC.

Is input tax credit a right or a concession?

The judiciary has frequently debated the nature of ITC. In TVS Motor Company Ltd vs. State of Tamil Nadu, the Supreme Court categorized ITC as a concession granted by the legislature, subject to strict statutory fulfillment. However, once conditions are met and credit is lawfully availed, it matures into a vested right, as established in Eicher Motors Ltd vs. Union of India. A failure to adhere to the restrictive mandates of Section 17(5) can result in the immediate forfeiture of this right.

When can businesses claim input tax credit?

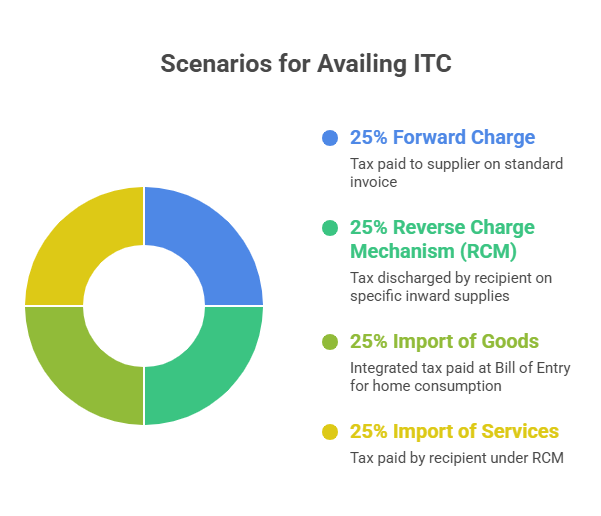

-

Forward Charge: Tax paid to the supplier on a standard invoice.

-

Reverse Charge Mechanism (RCM): Tax discharged by the recipient on specific inward supplies.

-

Import of Goods: Integrated tax paid at the time of filing the Bill of Entry for home consumption.

-

Import of Services: Tax paid by the recipient under RCM.

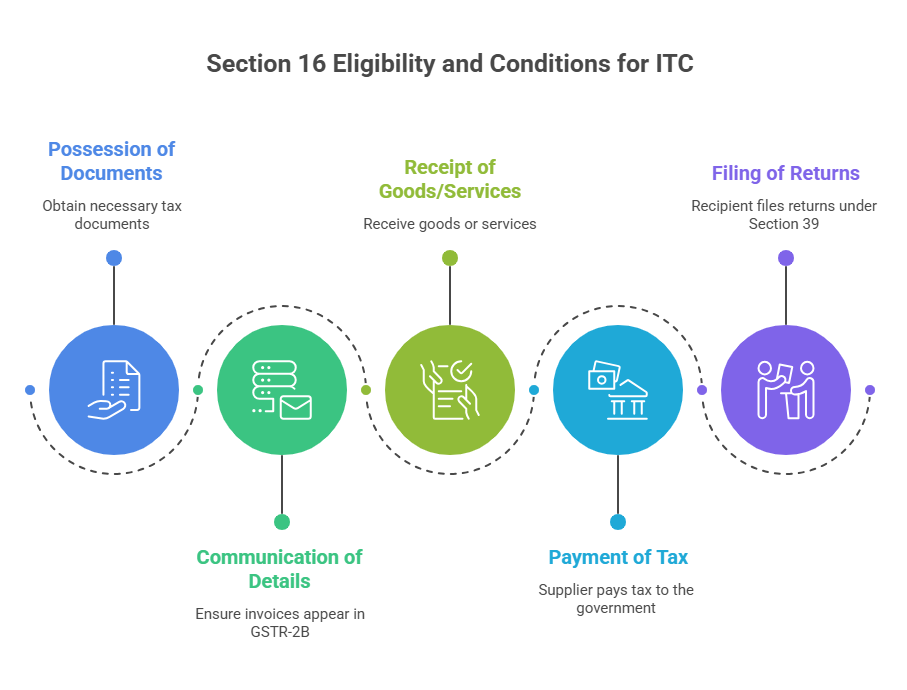

Section 16 conditions for claiming ITC

Before navigating the specific blockages of Section 17(5), one must pass the "Gateway to Credit" under Section 16(2). Any failure at this stage renders the discussion on blocked credit moot, as the credit was never eligible to begin with.

| Statutory Requirement | Documentary Evidence/Condition |

| Possession of Documents | Tax Invoice, Debit Note, Self-Invoice (Section 31(3)(f)), or Bill of Entry. |

| Communication of Details | Invoices must appear in GSTR-2B via Section 16(2)(aa), matching is verified via Rule 88C (DRC-01B). |

| Receipt of Goods/Services | Physical receipt or "Deemed Receipt" in Bill-to-Ship-to models. |

| Payment of Tax | Tax must be actually paid to the Government by the supplier [Section 16(2)(c)]. |

| Filing of Returns | The recipient must have furnished the return under Section 39. |

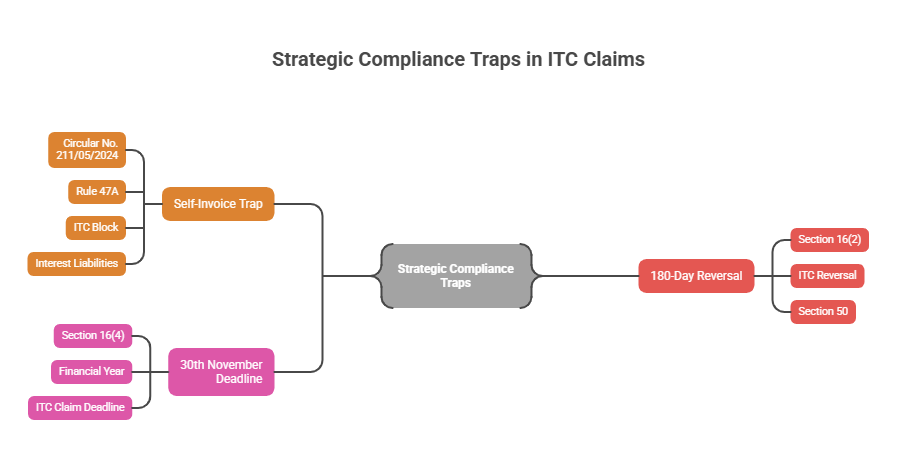

Common ITC compliance mistakes to avoid

-

The Self-Invoice Trap (Rule 47A): While Circular No. 211/05/2024 initially offered flexibility for RCM credit from unregistered persons, the introduction of Rule 47A (w.e.f. 01.11.2024) imposes a strict 30-day limit for raising self-invoices. Missing this deadline creates a hard block on ITC and triggers interest liabilities.

-

180-Day Reversal: Under the second proviso to Section 16(2), failure to pay the supplier within 180 days necessitates an ITC reversal with interest under Section 50.

-

The 30th November Deadline: In accordance with Section 16(4), the window for claiming ITC for a financial year slams shut on the 30th of November of the following year.

Blocked credit on vehicles, vessels, and aircraft

ITC rules for passenger motor vehicles

ITC is generally blocked for motor vehicles designed for transporting persons with an approved seating capacity of not more than 13 persons (including the driver). Exceptions (ITC allowed) when used for:

-

Further supply of such motor vehicles (e.g., automobile dealers).

-

Taxable supplies of transportation of passengers.

-

Imparting training on driving such motor vehicles.

Note: Eligibility is strictly governed by the "approved/designed" seating capacity as per the Regional Transport Authority (RTA). Actual usage for cargo is secondary to the vehicle's structural design and registration.

When is ITC allowed on vessels and aircraft?

The restriction for vessels and aircraft is even more stringent, with a general block unless used for:

-

Further supply, passenger transport, or training (navigating/flying).

-

Transportation of goods: Unlike motor vehicles, where cargo vehicles are never blocked, vessels and aircraft have a cargo-use exception to the general block.

Insurance, repair, and maintenance credits

Under Section 17(5)(ab), ITC is blocked for general insurance, repairs, and maintenance if they relate to assets for which ITC is already restricted under clauses (a) or (aa).

ITC treatment of demo vehicles and agency models

While Circular No. 231/25/2024-GST clarifies that authorized dealers may claim ITC on demo vehicles as they facilitate "further supply," businesses increasingly rely on e-invoicing software to maintain proper documentation and audit trails for such transactions. If a dealer acts as an agent and the manufacturer invoices the end-customer directly (Agency Model), the dealer is providing marketing services, not a supply of vehicles on their own account. In such cases, ITC on the demo vehicle is blocked.

Personal indulgence and employer obligations: Section 17(5)(b)

ITC on food, catering, and health services

Historically, ITC is blocked for food, beverages, catering, and health services. However, the 56th GST Council meeting introduced a seismic shift: individual life and health insurance are now Nil-rated (0%) effective from 22nd September 2025 (Notification No. 16/2025-CT(R)). For individual policies (non-group), the blockage is now moot as no tax is charged.

When employers can claim otherwise blocked ITC

The Section 17(5)(b) proviso is the ultimate mitigation tool for corporate taxpayers. ITC is available for otherwise blocked services (canteens, transport, insurance) if it is obligatory for an employer to provide them under any law (e.g., Factories Act, 1948, requiring canteens for over 250 workers).

Difference between employee perquisites and gifts

-

Contractual Perquisites: Services provided under an employment contract are not a "supply" per Schedule III. While no GST is paid on the recovery, ITC on the inward cost remains blocked unless mandated by law.

-

Voluntary Gifts: Under Schedule I, gifts exceeding Rs. 50,000 per financial year are taxable. If the gift is taxed, ITC on the inward supply is salvageable as a "further supply."

Three common employee benefit scenarios

-

Free Perquisite: Contractual; no GST on recovery, ITC generally blocked.

-

Voluntary Gift: Taxable if > Rs. 50,000; ITC allowed if tax is paid.

-

Nominal Recovery: Often viewed as a non-supply, though ITC is only available to the extent mandated by statutory law.

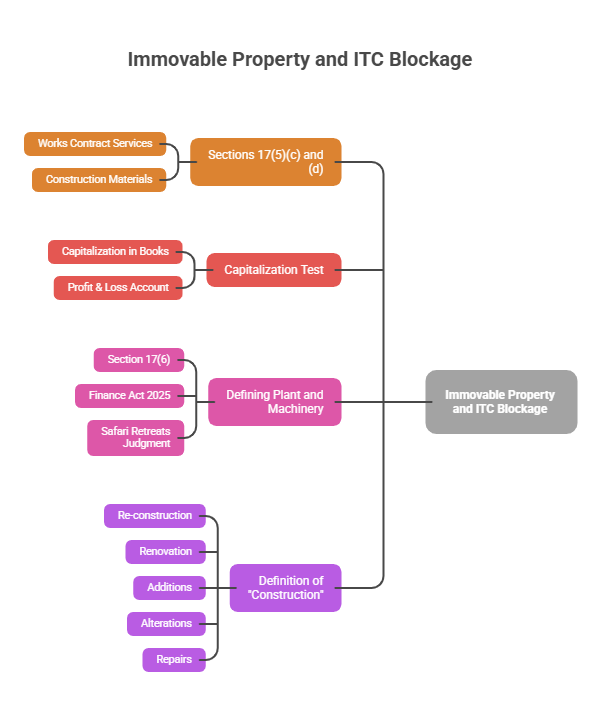

Blocked credit on immovable property and construction

Sections 17(5)(c) and (d) block ITC for works contract services and construction materials for immovable property built on "own account."

Understanding the capitalization test

This is a critical lever for tax strategists. ITC is only blocked to the extent of capitalization in the books of account (Explanation 1). Expenses charged to the Profit & Loss account (Revenue repairs) remain fully eligible for ITC.

Plant and machinery rules and Finance Act 2025 changes

The block excludes "Plant and Machinery," defined in Section 17(6) as apparatus fixed to earth by foundation. However, it specifically excludes land, buildings, telecommunication towers, and pipelines. Crucial Amendment: The Finance Act 2025 retrospectively (from 01.07.2017) changed "Plant or Machinery" to "Plant and Machinery" in clause (d) to prevent aggressive interpretations that sought to bypass the building exclusion. Strategists must note the Supreme Court's pushback in the Safari Retreats (2024) judgment, which underscores the "functional test" for buildings that act as plant.

What qualifies as construction under GST?

As per Explanation 1, "Construction" includes:

-

Re-construction

-

Renovation

-

Additions

-

Alterations

-

Repairs

-

Constraint: Only to the extent of capitalization to the immovable property.

-

Other blocked credits under GST

ITC reversal on lost, stolen, or free-sample goods

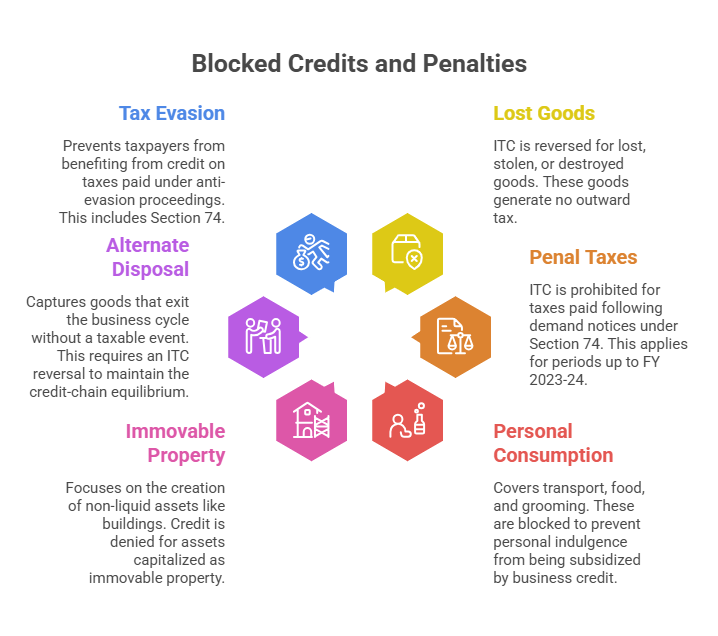

Section 17(5)(h) mandates the reversal of ITC for goods that are lost, stolen, destroyed, written off, or given as free samples. Since these goods generate no outward tax, the inward credit is deemed "unutilized for business."

Can businesses claim ITC on penal taxes?

ITC is strictly prohibited for taxes paid following demand notices issued under Section 74 (fraud/willful misstatement) for periods up to FY 2023-24.

Major categories of blocked credits under GST

Bundle 1: Personal Consumption

Covers transport, food, and grooming. These are blocked to prevent personal indulgence from being subsidized by business credit.

Bundle 2: Immovable Property

Focuses on the creation of non-liquid assets like buildings. Credit is denied for assets capitalized as immovable property, preserving the "Plant and Machinery" exception.

Bundle 3: Alternate Disposal

Captures goods that exit the business cycle without a taxable event (gifts, samples, theft), requiring an ITC reversal to maintain the credit-chain equilibrium.

Bundle 4: Tax Evasion

Prevents taxpayers from benefiting from credit on taxes paid under anti-evasion proceedings (e.g., Section 74).

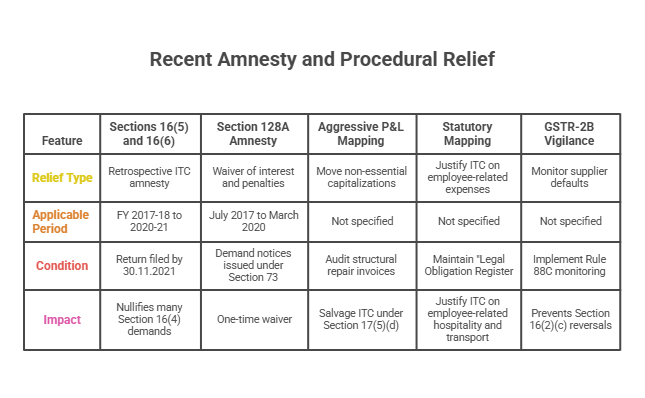

Recent GST amnesty schemes and compliance relief

The Finance (No. 2) Act, 2024 provided unprecedented relief for historic ITC disputes:

-

Sections 16(5) and 16(6): Retrospective amnesty allowing ITC for FY 2017-18 to 2020-21, provided the return was filed by 30.11.2021. This effectively nullifies many Section 16(4) demands.

-

Section 128A Amnesty: A one-time waiver of interest and penalties for demand notices issued under Section 73 (non-fraud cases) for the period July 2017 to March 2020.

-

Aggressive P&L Mapping: Audit all structural repair invoices. Move non-essential capitalizations to the Revenue account to salvage ITC under Section 17(5)(d).

-

Statutory Mapping: Maintain a "Legal Obligation Register" referencing the Factories Act or Labour Codes to justify ITC on employee-related hospitality and transport.

-

GSTR-2B Vigilance: Businesses increasingly rely on GST software for implementing Rule 88C monitoring to ensure supplier defaults do not contaminate the credit ledger and lead to Section 16(2)(c) reversals.

How can businesses effectively manage blocked credit under GST?

Understanding blocked credit under GST is essential for protecting your Input Tax Credit and avoiding costly reversals, penalties, and compliance disputes. Since Section 17(5) contains several exceptions, conditions, and evolving interpretations, businesses must regularly review procurement, capitalization practices, employee benefits, and vendor compliance processes. A proactive approach can help maximize eligible ITC while reducing litigation risks.

If your organization needs assistance with GST compliance, ITC management, e-invoicing, GST APIs, or automated tax workflows, Masters India offers technology-driven solutions designed to simplify complex GST requirements and improve compliance efficiency. Connect with our experts to streamline your GST operations and make informed tax decisions with confidence.

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified