Introduction

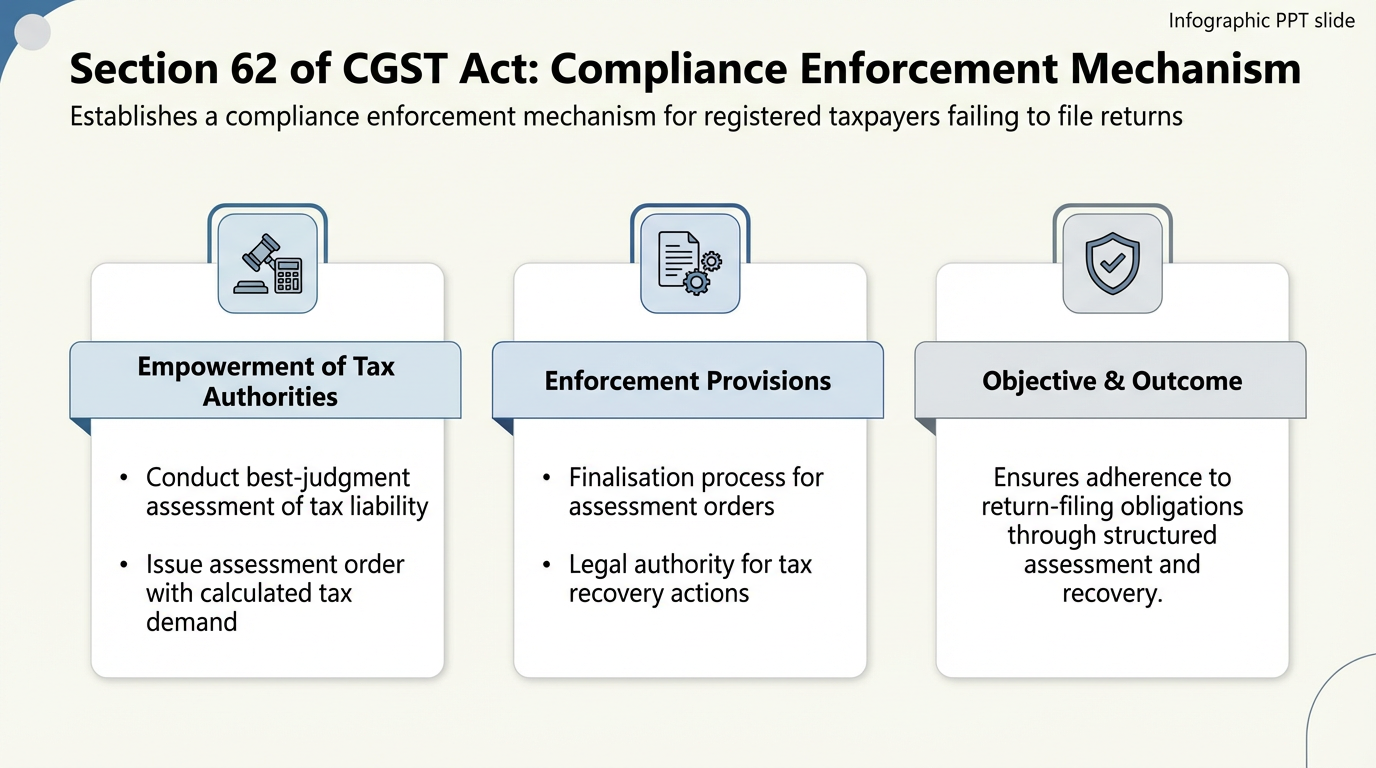

Chapter 13: Assessment (Sections 59-64) of the Central Goods and Services Tax Act, 2017 (CGST Act), Section 62: Assessment of Non-Filers of Returns provides a mechanism for tax authorities to determine the tax liability of registered persons who have failed to meet their return-filing obligations. This is a form of "best judgment assessment", distinct from the self-assessment typically followed in GST, and is invoked specifically when a registered person fails to file returns after receiving a statutory notice.

Prerequisites for Best Judgment Assessment

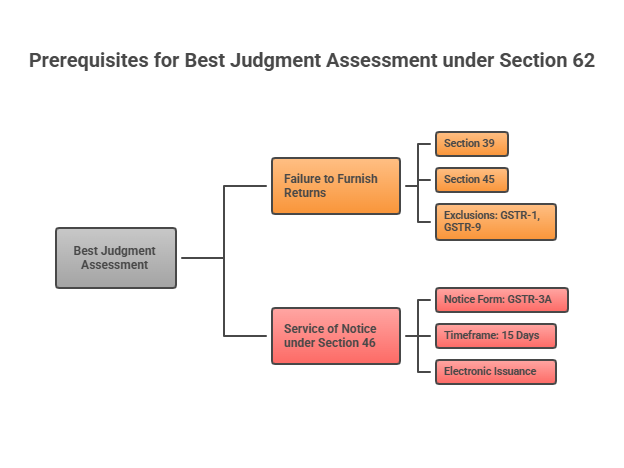

A best judgment assessment under Section 62 can be initiated under the following conditions:

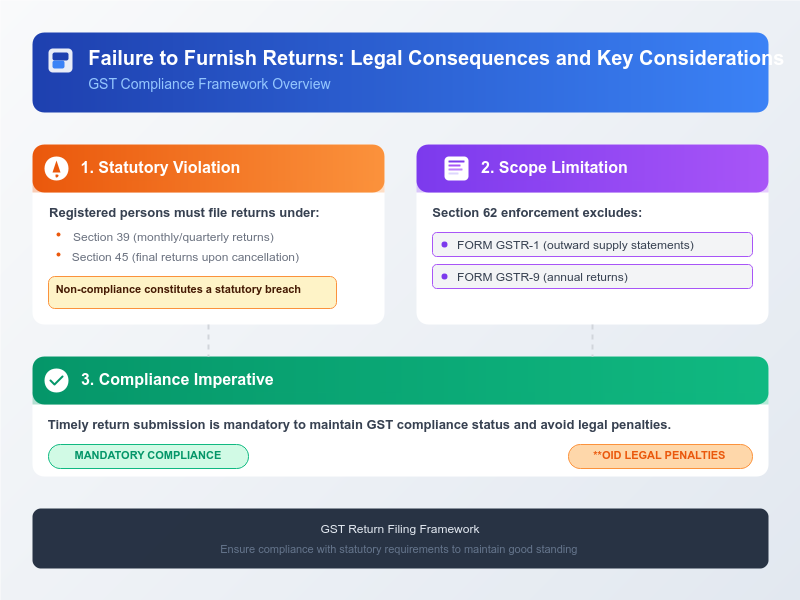

1. Failure to Furnish Returns: A registered person must have failed to furnish a return under either Section 39 (pertaining to regular monthly or quarterly returns) or Section 45 (pertaining to final returns filed upon cancellation of registration). It's important to note that Section 62 cannot be invoked for non-filing of FORM GSTR-1 (a statement of outward supplies, not a return) or FORM GSTR-9 (the annual return).

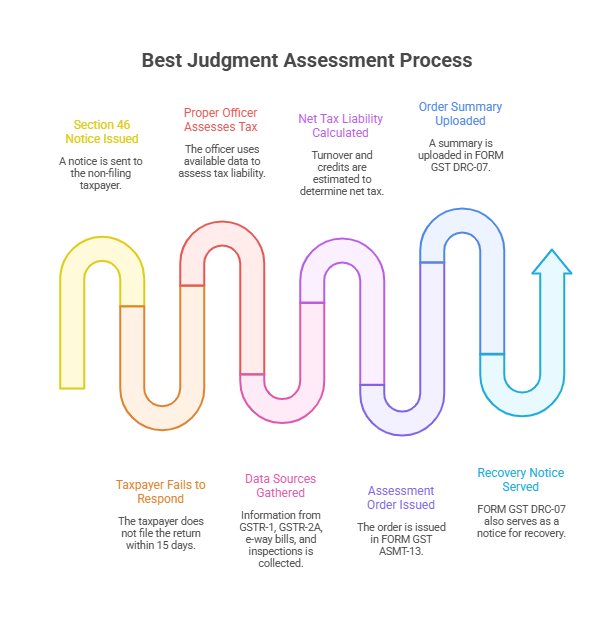

2. Service of Notice under Section 46: Crucially, this failure must persist even after the service of a notice under Section 46. Section 46 mandates that when a registered person fails to submit a return under Section 39, Section 44 (annual return), or Section 45, a notice will be issued to them.

2. Service of Notice under Section 46: Crucially, this failure must persist even after the service of a notice under Section 46. Section 46 mandates that when a registered person fails to submit a return under Section 39, Section 44 (annual return), or Section 45, a notice will be issued to them.

◦ Notice Form and Timeframe: This notice is issued electronically in FORM GSTR-3A. It mandates the defaulter to furnish the required return within fifteen days of its service. Non-compliance with this notice paves the way for Section 62 proceedings.

Nature of Best Judgment Assessment

If the registered person fails to furnish the return within the stipulated fifteen days after the Section 46 notice, the Proper Officer may proceed to assess the tax liability of the said person to the best of their judgment.

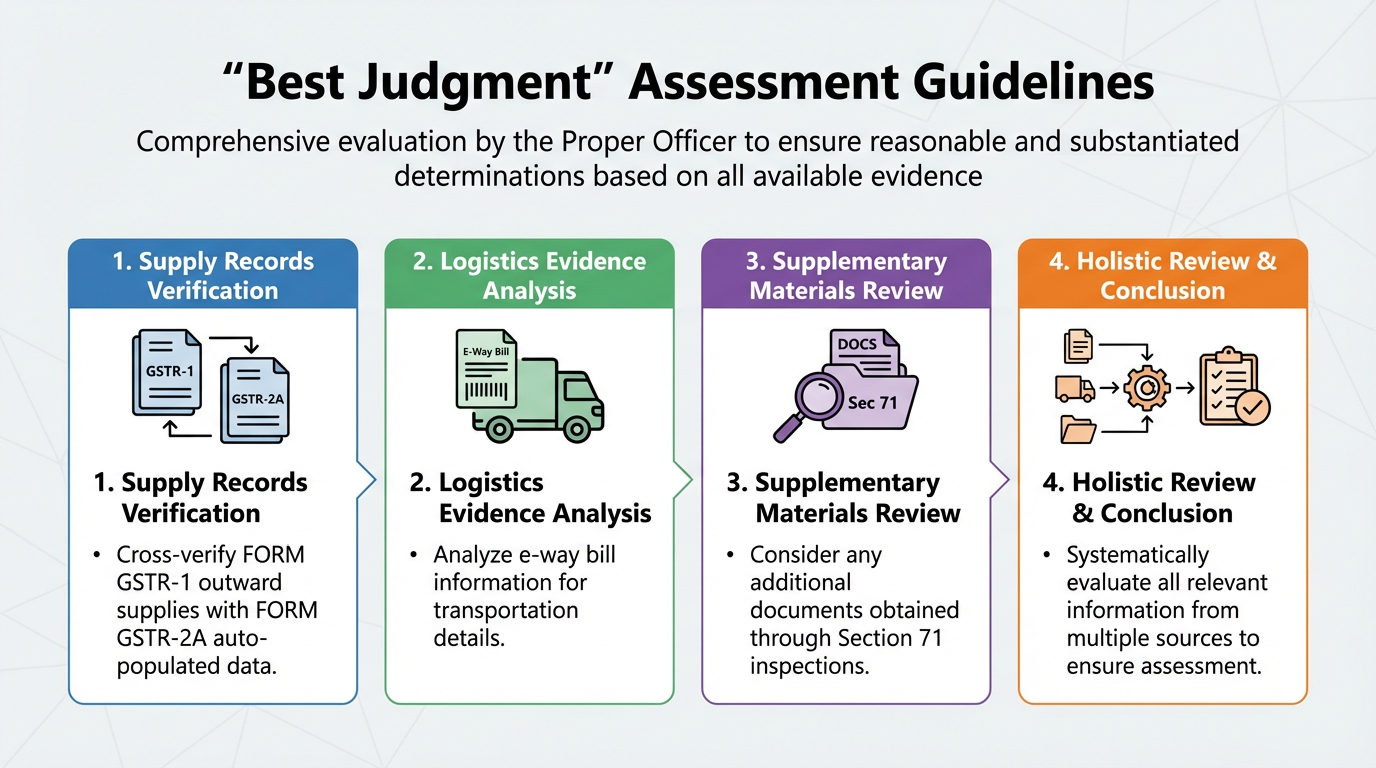

• "Best Judgment" Criteria: This assessment is not intended to be arbitrary or an "outlandish estimation". The Proper Officer must take into account all relevant material available or which they have gathered. This may include:

◦ Details of outward supplies available in FORM GSTR-1.

◦ Details of supplies auto-populated in FORM GSTR-2A.

◦ Information available from e-way bills.

◦ Any other information from various sources, including from inspection under Section 71.

• Net Tax Liability: Experts suggest that when turnover is projected, corresponding credits should also be estimated proportionally to arrive at the "net tax liability".

• No Opportunity of Hearing: A best judgment assessment under Section 62 can be completed without giving notice of hearing to the assessee.

Assessment Order and Communication

The assessment order under Section 62(1) is issued in FORM GST ASMT-13. A summary of this order is uploaded electronically in FORM GST DRC-07. This FORM GST DRC-07 also serves as a notice for recovery.

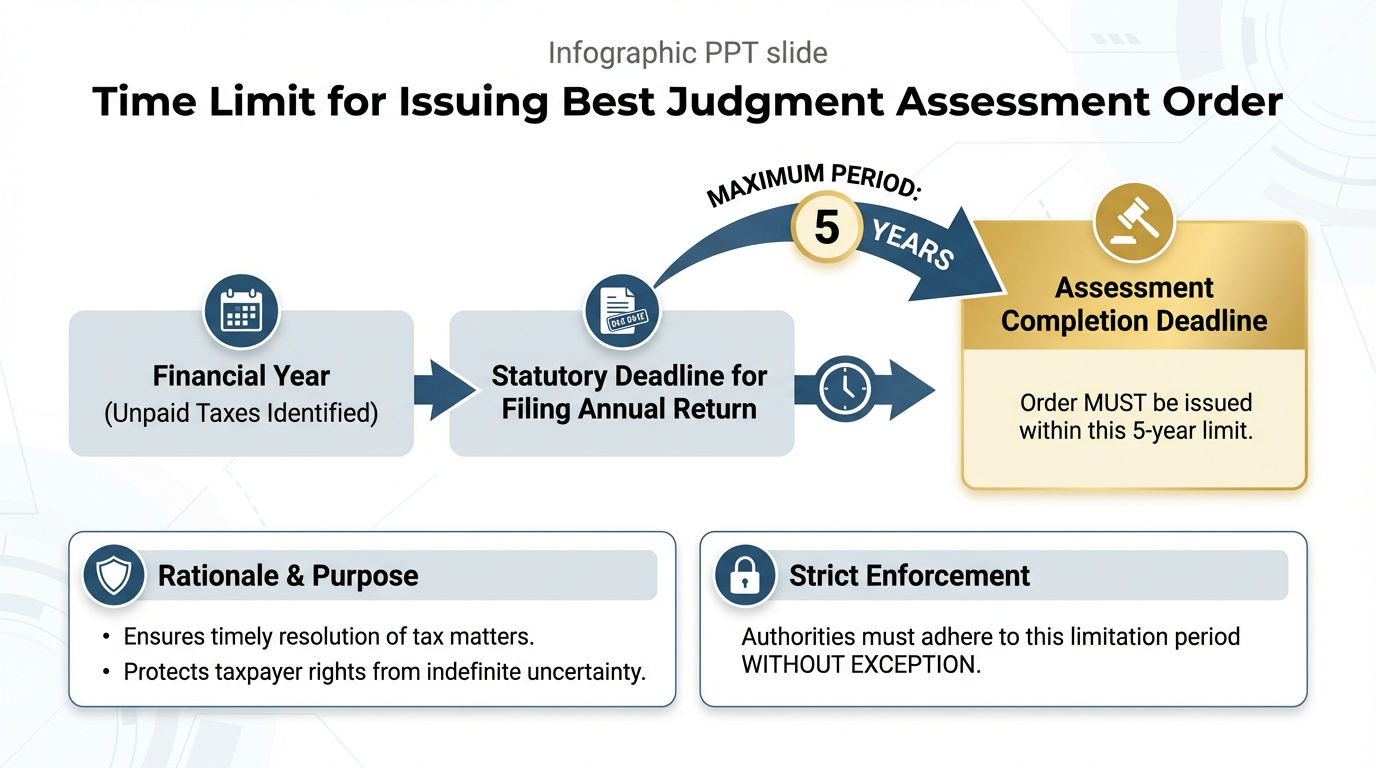

Time Limit for Order

The best judgment assessment order must be issued within a period of five years from the date specified under Section 44 for furnishing the annual return for the financial year to which the tax not paid relates.

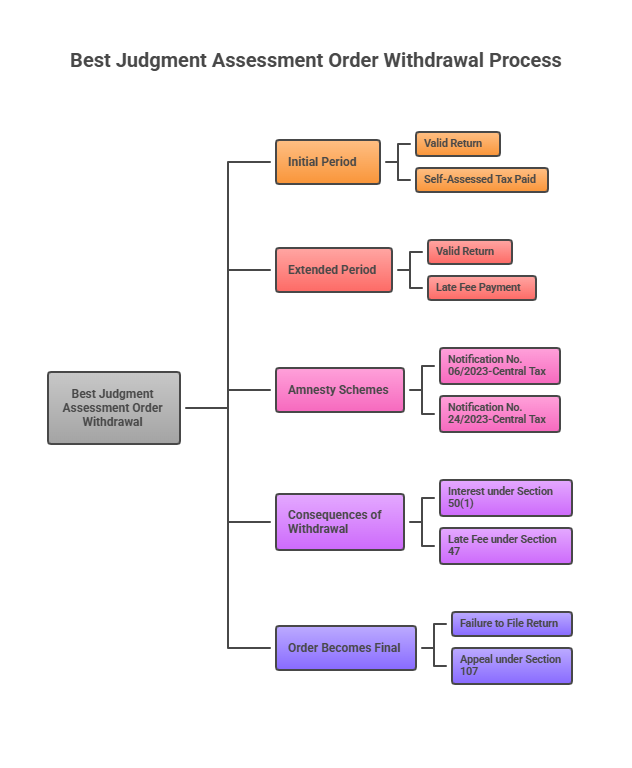

Withdrawal of Assessment Order

A significant feature of Section 62 is its provision for the deemed withdrawal of the assessment order under specific conditions:

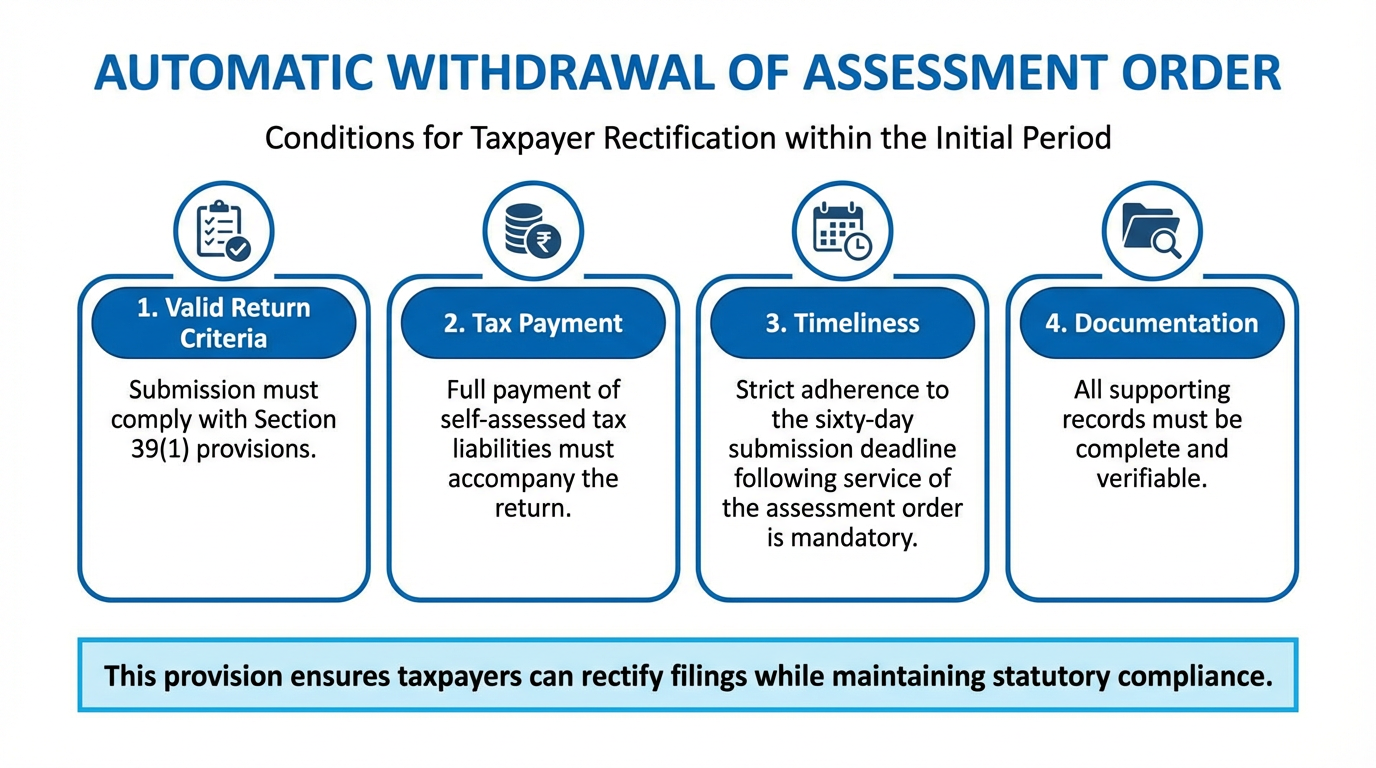

1. Initial Period: If the registered person furnishes a "valid return" within sixty days (this period was previously thirty days) of the service of the assessment order, the order is deemed to have been withdrawn.

◦ A "valid return" is defined as a return filed under Section 39(1) on which self-assessed tax has been paid in full.

2. Extended Period: If a valid return is not filed within the initial sixty days, the person may furnish it within a further period of sixty days. This extended period requires payment of an additional late fee of one hundred rupees for each day of delay beyond the first sixty days.

3. Amnesty Schemes: The Government has also notified amnesty schemes, such as Notification No. 06/2023-Central Tax and Notification No. 24/2023-Central Tax, for the deemed withdrawal of assessment orders issued under Section 62, subject to specific conditions and dates.

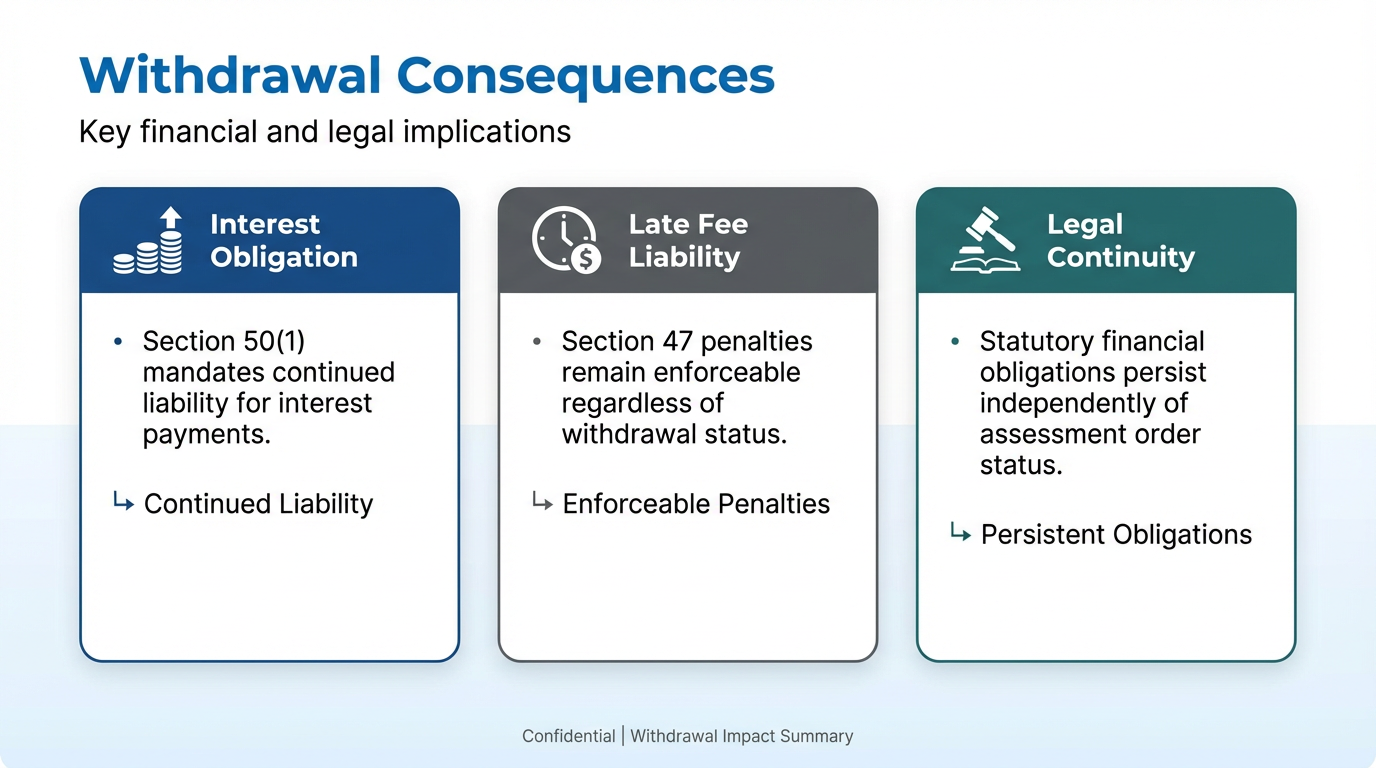

4. Consequences of Withdrawal: Even if the assessment order is deemed withdrawn, the liability for payment of interest under Section 50(1) and late fee under Section 47 shall continue.

5. Order Becomes Final: If the registered person fails to furnish a valid return within both the initial and the extended periods, the assessment order becomes final and cannot be withdrawn. In such a scenario, the only available remedy is to file an appeal under Section 107.

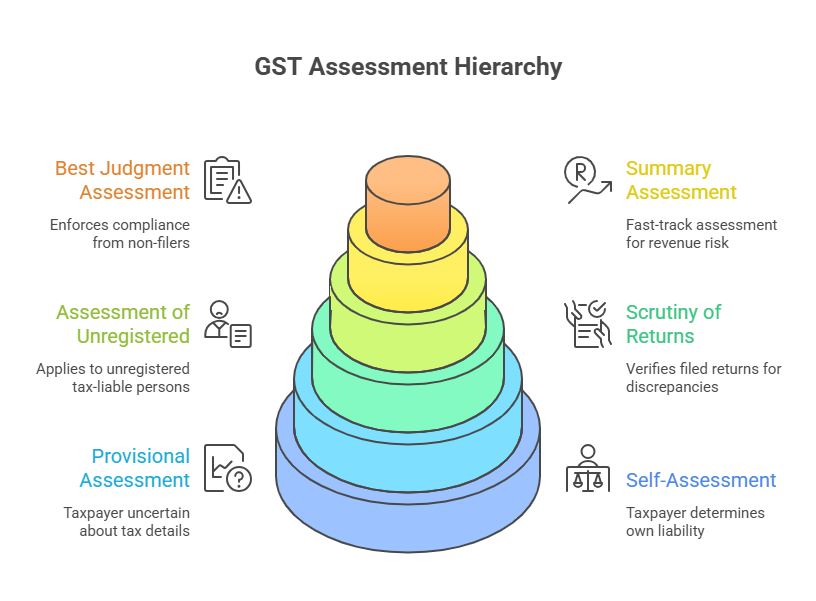

Best Judgment Assessment in the Larger Context of Assessment (Sections 59-64)

Section 62 is a vital component of the assessment framework, distinct from other assessment types:

• Contrast with Self-Assessment (Section 59): Unlike self-assessment, where the taxpayer determines their own liability, Section 62 is an interventionist assessment by the Proper Officer due to a taxpayer's failure to comply with return filing obligations.

• Distinct from Provisional Assessment (Section 60): Provisional assessment is initiated by the taxpayer due to genuine uncertainty in determining value or rate of tax, whereas Section 62 is for non-compliance with filing requirements.

• Distinct from Scrutiny of Returns (Section 61): Scrutiny involves verifying filed returns for discrepancies. Section 62, however, applies when no returns have been filed at all. While scrutiny can lead to demand proceedings under Section 73 or 74, a Section 62 order directly assesses and demands tax.

• Distinct from Assessment of Unregistered Persons (Section 63): Section 62 is specifically for registered persons who fail to file returns, while Section 63 applies to unregistered persons who are liable to pay tax but have not obtained registration.

• Distinct from Summary Assessment (Section 64): Summary assessment is a "fast track" or "protective assessment" in special cases of immediate revenue risk, requiring prior permission from higher authorities. Section 62 is specifically for non-filers, not necessarily for immediate revenue threats, and does not require such prior permission for its initiation (only for the initial Section 46 notice).

• Non-Obstante Clause: Section 62 commences with a non-obstante clause, meaning its provisions apply "Notwithstanding anything to the contrary contained in section 73 or section 74" (and Section 74A). This allows assessment under Section 62 to be carried out independently of the formal show-cause notice and hearing procedures mandated by Sections 73 or 74.

• Link to Demands and Recovery: A summary of the Section 62 order, uploaded in FORM GST DRC-07, is treated as a notice for recovery. If the self-assessed tax in a return remains unpaid, it can be recovered under Section 79. Proceedings under Section 62 can also trigger provisional attachment of property under Section 83 to protect government revenue.

Conclusion:

In essence, Section 62 serves as a stringent enforcement tool under the CGST Act, compelling compliance from registered taxpayers who default on their return-filing obligations by authorising tax authorities to assess and recover the tax liability through a structured best-judgment process, backed by the authority to enforce recovery if the order becomes final.

GST Anti Evasion Department Powers | Powers of GST Officers | DRC-01 | Statement of Facts and Grounds of Appeal Format GST | Valuation Rules Under GST

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified